The Asset Ladder: What People Own When They Start Building Real Wealth

Most people are taught to chase income. Get a job. Earn a salary. Work hard. Get promoted. Earn more. Repeat the cycle until retirement.

Income matters. Without income, it is difficult to save, invest, reduce debt, or buy freedom. But income alone is not wealth. Income is money passing through your hands. Wealth is what remains after the money passes through. More importantly, wealth is what continues working after you stop working.

This is the difference between earning and owning.

A person who earns well but owns little may look successful and still be financially fragile. Their lifestyle depends on the next paycheck, the next contract, the next client, or the next business cycle. A person who owns assets may not always look wealthy from the outside, but their financial life is becoming stronger beneath the surface. Their money is slowly being converted into things that appreciate, generate cash flow, reduce future expenses, or create optionality.

That is how many people become rich. Not by earning once, spending once, and starting over again. They become rich by acquiring assets that keep producing value long after the original effort is finished.

An asset is not merely something expensive. A luxury car is expensive, but it usually loses value. A designer watch may be expensive, but it may or may not be a reliable investment. A large house may feel like wealth, but if it drains every dollar of cash flow, it can become a burden. A true wealth-building asset has one or more of four qualities: it can rise in value, produce income, increase your earning power, or give you control over future opportunities.

The wealthy understand this. They think in terms of ownership. They ask what they can buy, build, control, improve, or compound. They do not see money only as something to spend. They see it as seed capital.

This article explores the assets that are helping people build real wealth. Some are traditional. Some are modern. Some require capital. Some require knowledge. Some require patience. Some require risk. None are magic. But together, they reveal the central principle of wealth building: rich people own things that make money, grow in value, or create leverage.

1. Productive Businesses

The business is one of the oldest and most powerful wealth-building assets in history. A business can turn ideas, labor, systems, products, services, relationships, and capital into profits. Unlike a job, a business can grow beyond the direct time of one person. It can hire employees, serve more customers, open new locations, license products, build brand value, and eventually be sold.

This is why business ownership has created so many fortunes. A salary pays you for work performed. A business pays you for value created. When the value becomes durable, the business itself becomes an asset.

A small business can begin as self-employment. A designer sells services. A plumber serves local homeowners. A consultant advises companies. A baker sells products. At first, the owner may be trading time for money. But if the owner builds systems, hires help, creates repeatable processes, develops customer lists, strengthens the brand, and separates the business from personal labor, the business becomes more valuable.

The transformation happens when the business no longer depends entirely on the owner’s daily effort. A business that cannot operate without the owner is still valuable, but it is closer to a high-pressure job. A business with systems, recurring revenue, strong margins, and trained people is an asset that can produce income and attract buyers.

There are many kinds of productive businesses. A local service business. A software company. A cleaning company. A medical practice. An e-commerce brand. A logistics operation. A financial advisory firm. A restaurant group. A tutoring company. A construction business. A media company. A manufacturing operation. The form varies, but the wealth principle is the same: the owner captures the upside of building something valuable.

Business ownership is not easy. It can involve debt, stress, failed products, difficult customers, lawsuits, employee problems, tax complexity, competition, and long periods without predictable income. Many businesses fail. Many owners discover that revenue is not profit. A business can look impressive from the outside while producing little free cash flow.

But when a business works, it can create wealth in several ways at once. It can pay the owner income. It can build equity value. It can create tax planning opportunities. It can provide employment for family members. It can produce intellectual property. It can be sold. It can become the foundation for other investments.

The lesson is not that everyone should quit a job and start a company. The lesson is that ownership changes the wealth equation. Employees earn from labor. Owners earn from systems, risk, capital, and leverage. A person who wants to become wealthy should at least understand how businesses create value, because even stock investing is ultimately ownership of businesses.

2. Public Stocks

Stocks are one of the most accessible wealth-building assets available to ordinary people. When you buy a stock, you are buying a piece of a company. That company may own factories, software, patents, inventory, customer relationships, distribution networks, brands, cash, and future earnings power. The investor does not need to manage employees or sell products personally. They can participate as an owner through public markets.

This is one of the quiet miracles of modern finance. A person with a modest income can own small pieces of some of the most profitable companies in the world. Through index funds and retirement accounts, they can own hundreds or thousands of businesses at once. They can benefit from innovation, productivity, population growth, pricing power, and reinvested profits.

Stocks can build wealth through appreciation and dividends. Appreciation occurs when the value of the company rises and the stock price follows over time. Dividends are cash distributions paid to shareholders by some companies. Not every strong company pays dividends, and not every dividend stock is a good investment. The deeper value comes from owning businesses that can grow earnings over long periods.

Many people misunderstand stocks because they focus on short-term price movement. They see the stock market as a casino, a prediction game, or a place where professionals manipulate prices. In the short run, markets can be emotional and unpredictable. Prices rise and fall because of interest rates, earnings reports, wars, recessions, elections, inflation fears, investor psychology, and countless other forces.

But long-term stock ownership is not the same as short-term speculation. The long-term investor is not trying to guess tomorrow’s price. The long-term investor is trying to own productive companies for years or decades. This is why diversified investing has been such a powerful wealth tool. It allows ordinary households to buy ownership and let time do much of the work.

The wealthy often use stocks differently from inexperienced investors. They focus on allocation, tax efficiency, risk control, diversification, and time horizon. They do not need every investment to double overnight. They understand that compounding at reasonable rates over long periods can create extraordinary results.

A young investor who consistently buys broad stock funds over several decades can build serious wealth without ever picking a single winning company. That is the power of public markets. They turn ownership into something scalable and accessible.

The danger is impatience. People often buy when excitement is high and sell when fear is high. They chase trends, panic during downturns, overconcentrate in one company, borrow to speculate, or confuse entertainment with investing. Stocks can make people rich, but only when paired with discipline, diversification, and time.

3. Index Funds and Exchange-Traded Funds

Index funds and exchange-traded funds, often called ETFs, are among the most important financial inventions for ordinary wealth builders. They allow investors to own a diversified basket of assets at relatively low cost. Instead of trying to choose one winning stock, an investor can own an entire market, sector, asset class, or strategy.

This matters because most people do not have the time, temperament, or expertise to analyze individual companies well. They may not know how to read balance sheets, evaluate competitive advantages, forecast cash flows, or judge management quality. Index funds solve part of that problem by spreading ownership across many companies.

A broad stock index fund can give an investor exposure to hundreds or thousands of companies. Some will fail. Some will perform poorly. Some will produce average results. A few may become extraordinary winners. The investor does not need to know in advance which company will dominate the future. They own the field.

This is a different kind of intelligence. It is not the intelligence of prediction. It is the intelligence of humility. The index investor admits that the future is uncertain and chooses broad ownership instead of constant guessing.

ETFs can also provide exposure to bonds, real estate investment trusts, international stocks, commodities, dividend strategies, and specific industries. Used wisely, they can help build a diversified portfolio. Used poorly, they can become tools for speculation. The existence of an ETF does not make the underlying investment safe or suitable.

The wealth-building power of index funds comes from consistency. A worker contributes every paycheck. A business owner invests surplus cash. A household reinvests dividends. Over years, the portfolio grows. During market downturns, contributions buy more shares. During expansions, the accumulated shares rise in value.

This strategy is not glamorous. It does not impress people at dinner. It does not sound like a secret. But many wealthy households use simple, diversified portfolios because simplicity can be a strength. Complexity is not required to build wealth. In many cases, complexity is the enemy of discipline.

Index funds and ETFs are making people rich not because they promise quick gains, but because they provide broad access to ownership, low friction, and the ability to compound quietly for decades.

4. Cash-Flowing Real Estate

Real estate has created wealth for generations because it combines several financial forces in one asset. A rental property can produce monthly income, appreciate over time, use financing, provide tax advantages, and serve a basic human need. People always need places to live, work, store goods, operate businesses, and gather.

The simplest example is a rental home. An investor buys a property, rents it to a tenant, collects rent, pays expenses, and keeps the remaining cash flow. Over time, the tenant’s rent may help pay down the mortgage. The property may rise in value. Rents may increase. The owner’s equity may grow.

This is why real estate can be such a powerful wealth asset. It allows an investor to control a large asset with a smaller down payment. If the property performs well, the owner benefits from appreciation on the whole property, not just the initial cash invested. This use of leverage can magnify returns.

But leverage cuts both ways. A property with too much debt can become dangerous. Vacancies, repairs, insurance increases, property taxes, bad tenants, legal disputes, interest rate changes, and local market declines can turn a promising investment into a financial burden. Real estate is not passive in the beginning. It is often an operating business disguised as an investment.

Wealthy real estate investors focus on cash flow, location, financing, tenant quality, maintenance, tax treatment, and exit strategy. They do not buy only because a property looks attractive. They study the numbers. They ask whether the rent supports the debt. They build reserves. They understand local employment, population trends, zoning, crime, schools, transportation, and supply.

Real estate can make people rich because it rewards patience and operational competence. A property bought wisely and held for decades can become a powerful asset. The mortgage balance falls. Rents rise. Equity grows. Eventually, the owner may refinance, sell, exchange into another property, or live off the income.

The key phrase is bought wisely. A bad real estate deal does not become good because real estate is popular. Paying too much, underestimating repairs, ignoring cash flow, or assuming prices always rise can destroy capital. Real estate wealth is built by disciplined underwriting, not wishful thinking.

5. Land in the Path of Growth

Land is different from buildings. Buildings age, require maintenance, and can become obsolete. Land is fixed. There is only so much of it in desirable locations. This is why land in the path of growth can become a major wealth-building asset.

Not all land is valuable. Some land is cheap for good reason. It may lack access, utilities, water rights, demand, zoning flexibility, or economic purpose. Raw land can sit for years producing no income while still requiring taxes, insurance, maintenance, and patience.

But the right land can become extremely valuable when population, infrastructure, commerce, or development moves toward it. A parcel near a growing city, future highway, expanding industrial corridor, or desirable residential area may appreciate as demand increases. Land can also become more valuable when zoning changes allow higher use.

Wealthy families have long understood this. They buy land before the crowd recognizes its potential. They hold through uncertainty. They lease it for farming, storage, billboards, energy, parking, or commercial use. They wait for developers, municipalities, or businesses to need what they control.

The wealth principle is scarcity plus patience. Land does not send quarterly earnings reports. It does not always produce cash flow. It may look boring for years. Then one road, one employer, one zoning change, one housing shortage, or one infrastructure project can change its value dramatically.

This asset is not ideal for people who need immediate income. Land can be illiquid. Selling may take time. Financing can be harder. Due diligence is crucial. Buyers must understand title, access, environmental issues, zoning, utilities, taxes, easements, flood risk, and local development plans.

When done well, land investing can turn foresight into wealth. The investor is not buying what the land is today. They are buying what it may become when growth arrives.

6. Real Estate Investment Trusts

Real Estate Investment Trusts, or REITs, allow investors to own real estate without directly buying properties. A REIT may own apartments, warehouses, data centers, cell towers, offices, retail centers, hotels, healthcare facilities, storage units, or other income-producing real estate. Investors buy shares and participate in the cash flows and value of the underlying property portfolio.

REITs are powerful because they make real estate ownership more accessible and liquid. A person who cannot afford an apartment building can still own part of a company that owns many apartment buildings. A person who does not want to deal with tenants, repairs, or mortgages can still gain exposure to real estate income.

Different REIT sectors behave differently. Data center REITs may benefit from demand for cloud computing and artificial intelligence infrastructure. Industrial REITs may benefit from logistics and e-commerce. Apartment REITs may benefit from housing demand. Healthcare REITs may benefit from demographic trends. Office REITs may struggle if remote work reduces demand in certain markets.

This is important because “real estate” is not one thing. Owning a warehouse portfolio is different from owning suburban apartments. Owning cell towers is different from owning shopping centers. Investors must understand what they actually own.

REITs can provide dividends, diversification, and professional management. They can also be sensitive to interest rates, debt costs, property cycles, tenant weakness, and market sentiment. Publicly traded REIT prices can fluctuate like stocks, even when the underlying buildings are stable.

For wealth builders, REITs can serve as a bridge between stocks and direct real estate. They provide ownership of property-based businesses without the heavy operational demands of being a landlord. They are not a substitute for due diligence, but they are an important asset class for people who want real estate exposure without direct property management.

7. Digital Businesses

Digital businesses have created a new generation of wealth because they can scale quickly and operate with fewer physical constraints than traditional companies. A digital business may sell software, online education, memberships, digital products, templates, advertising, subscriptions, marketplaces, apps, or specialized services delivered through the internet.

The appeal is leverage. A physical store can serve only so many people in one location. A digital product can potentially serve customers across the world. A software product can be sold repeatedly. An online course can be created once and purchased many times. A subscription community can generate recurring revenue. A niche website can attract search traffic and earn income through ads, affiliates, products, or leads.

Digital assets can also have high margins. There may be no inventory, no storefront, and no large distribution network. This does not mean digital businesses are easy. Competition is intense. Customer acquisition can be expensive. Platforms change algorithms. Technology breaks. Content becomes outdated. Trust is hard to build and easy to lose.

Still, the wealth potential is significant. A digital business with loyal customers, recurring revenue, strong brand trust, and low marginal costs can become highly valuable. Buyers often pay for predictable revenue, customer lists, traffic, intellectual property, and systems.

Many people make the mistake of thinking a digital business is simply posting online. Posting is not a business. Attention is not always revenue. A true digital business has an offer, a customer, a way to deliver value, a payment system, and a method for retaining or reacquiring buyers.

Wealthy digital entrepreneurs treat online attention as distribution. They use content to build trust, email lists to preserve relationships, products to monetize expertise, and systems to scale delivery. They understand that the asset is not just the website or social account. The asset is the audience relationship, data, brand, product library, and revenue engine.

Digital businesses are making people rich because they allow knowledge, creativity, and systems to travel farther than the owner’s physical presence.

8. Intellectual Property

Intellectual property is ownership of ideas in a form that can be protected, licensed, sold, or monetized. It includes copyrights, trademarks, patents, trade secrets, proprietary processes, software code, books, music, designs, formulas, databases, and branded methods.

Intellectual property can be powerful because it separates value from physical labor. A book can sell while the author sleeps. A patent can generate licensing income. A song can produce royalties. A software tool can be used by thousands of customers. A trademark can make a brand recognizable and defensible.

The wealthy understand that ideas alone are not assets. An idea becomes an asset when it is developed, protected, distributed, and monetized. A notebook full of concepts is not wealth. A patented invention licensed to manufacturers may be. A catchy name is not wealth. A trusted brand with trademark protection may be.

Intellectual property often grows from expertise. A consultant creates a framework. A teacher develops curriculum. A chef creates recipes and a brand. An engineer develops software. A researcher develops a method. A creator builds a content library. The work begins as knowledge, but it becomes wealth when packaged into a repeatable asset.

There are risks. Legal protection can be expensive. Enforcement can be difficult. Some intellectual property becomes obsolete quickly. A patent may not have commercial value. A copyright may not generate demand. A trademark means little without a brand behind it.

But when intellectual property works, it can produce high returns because it can be replicated at low cost. This is why media companies, software firms, pharmaceutical companies, consumer brands, and entertainment businesses can become so valuable. They own things that can be used repeatedly without being consumed in the same way physical inventory is consumed.

For individuals, the practical lesson is to document and package knowledge. A method, curriculum, software tool, design system, newsletter archive, research database, or brand can become more than work. It can become an asset.

9. High-Income Skills

Skills are not always listed on a balance sheet, but they can be among the most valuable assets a person owns. A high-income skill increases earning power. It can produce better jobs, consulting opportunities, business income, equity participation, and career resilience.

Examples include sales, software development, financial analysis, copywriting, negotiation, leadership, data science, engineering, design, law, medicine, project management, marketing, public speaking, cybersecurity, artificial intelligence implementation, and business strategy. The specific skill matters less than the economic principle: valuable skills solve valuable problems.

A skill becomes especially powerful when it is rare, useful, and connected to money. A person who can help a company increase revenue, reduce costs, manage risk, raise capital, build technology, lead teams, or attract customers can command higher compensation.

Unlike many assets, skills can be built with limited capital. They require time, effort, feedback, practice, and often discomfort. This makes skill acquisition one of the most democratic wealth-building tools. A person may not have money to buy real estate, but they may be able to learn a skill that raises income enough to buy assets later.

Wealthy people often invest heavily in education, coaching, networks, and personal development because they understand that earning power is the first engine of wealth. The stronger the engine, the more capital can be invested.

But skills must be applied. Collecting certificates without market value does not create wealth. Reading without execution does not change income. The goal is not to appear educated. The goal is to become economically useful.

A high-income skill can make someone rich by increasing the surplus available for investment. It can also create pathways to business ownership. Many entrepreneurs begin with a skill, sell it as a service, turn the service into a system, and eventually build a company around it.

10. Personal Brand and Reputation

Reputation is an asset. It affects who trusts you, who hires you, who invests with you, who refers clients, who opens doors, and who wants to work beside you. In a noisy economy, trust is scarce. People with strong reputations attract opportunities that others never see.

A personal brand is not just social media visibility. It is the market’s understanding of who you are, what you know, what you stand for, and what results you can produce. A strong brand reduces friction. It makes selling easier, hiring easier, fundraising easier, and partnership easier.

For professionals, reputation can lead to promotions, speaking opportunities, board seats, clients, book deals, consulting contracts, media appearances, and equity offers. For entrepreneurs, reputation can lower customer acquisition costs. For investors, reputation can attract deal flow. For creators, reputation can build audience loyalty.

Reputation compounds slowly and can be damaged quickly. This is why wealthy people often protect their names carefully. They understand that a short-term gain achieved through dishonesty can destroy long-term opportunity. Trust is difficult to build and expensive to repair.

In the digital era, personal brand can scale. A person can publish ideas, teach, analyze, entertain, explain, or document their work online. Over time, that body of work becomes proof. It can attract clients, employers, investors, customers, or collaborators.

The danger is confusing attention with reputation. Attention can be bought, hacked, or manufactured. Reputation must be earned. A person can be famous and not trusted. A person can have a modest audience and be deeply respected in a valuable niche.

As an asset, reputation produces wealth indirectly. It increases the quality and quantity of opportunities. It makes other assets easier to build. A strong reputation can turn a skilled person into a sought-after person, and that difference can be worth millions over a lifetime.

11. Networks and Relationships

Relationships are not assets in the cold sense of owning people. But a strong network is a form of social capital, and social capital often becomes financial capital. Opportunities move through people. Jobs, deals, investments, partnerships, referrals, mentorship, information, and introductions usually come through relationships.

Wealthy people often spend years building networks because they understand that who knows you can shape what reaches you. A great opportunity rarely arrives randomly. It is often passed from one trusted person to another.

A network can make someone rich by improving access. Access to better information. Access to capital. Access to talent. Access to customers. Access to mentors. Access to private deals. Access to rooms where decisions are made.

This does not mean networking should be fake or transactional. The best networks are built through value, reliability, generosity, competence, and trust. People refer opportunities to those who make them look wise for doing so. If you consistently deliver, your network becomes stronger.

Many people underestimate relationships because they focus only on technical skill. Skill matters, but skill hidden from the world has limited reach. A talented person who no one knows may struggle. A talented person with a strong network can move much faster.

Building a valuable network requires intention. Attend industry events. Follow up. Help before asking. Share useful information. Maintain old relationships. Introduce people who should know each other. Be reliable. Protect confidences. Do excellent work.

A strong network is not a shortcut around competence. It is a multiplier of competence. The richer the network, the more likely valuable opportunities can find you.

12. Retirement Accounts

Retirement accounts are not exciting, but they are among the most effective wealth-building containers available to ordinary households. A retirement account is not an investment by itself. It is a tax-advantaged structure that can hold investments such as stocks, bonds, funds, and other eligible assets.

The power comes from tax treatment and time. Contributions may reduce taxable income, investments may grow tax-deferred, or qualified withdrawals may be tax-free depending on the type of account. Employer matching contributions can add immediate value. Automatic payroll deductions make consistency easier.

Many people become millionaires through retirement accounts not because they make brilliant investment decisions, but because they contribute steadily for decades. The formula is simple but demanding: start early, invest regularly, diversify, avoid unnecessary withdrawals, increase contributions over time, and let compounding work.

Wealthy households often maximize retirement structures. Business owners may design plans that allow larger contributions. High earners may coordinate traditional and Roth strategies. Families may use spousal retirement accounts. Investors may place tax-inefficient assets in tax-advantaged accounts and tax-efficient assets in taxable accounts.

The average person often underuses retirement accounts because retirement feels far away. But distance is the advantage. The longer the time horizon, the more powerful compounding becomes.

Early withdrawals can damage the wealth engine. Taking money from retirement accounts for short-term spending interrupts compounding and may create taxes or penalties. Wealth builders try to preserve retirement assets unless there is a serious emergency or strategic reason.

Retirement accounts are making people rich quietly. No headlines. No glamour. Just repeated ownership, tax advantages, and time.

13. Cash and Liquidity

Cash rarely makes people rich by itself. Over time, inflation can reduce purchasing power. But cash is still an asset because it provides safety, flexibility, and opportunity. Wealthy people understand the strategic value of liquidity.

A person with no cash is vulnerable. A car repair becomes debt. A medical bill becomes panic. A job loss becomes crisis. A market downturn becomes forced selling. Lack of liquidity causes people to make bad decisions at bad times.

Cash prevents desperation. It allows a person to wait, negotiate, invest during downturns, leave toxic employment, move for opportunity, start a business, or handle emergencies without destroying long-term assets.

The wealthy do not usually keep all their money in cash, because idle cash can lose value after inflation. But they keep enough liquidity to avoid being forced into poor decisions. This is one of the hidden benefits of wealth. It gives people time.

Cash can also become an offensive asset. During recessions, asset prices may fall. Businesses may need capital. Real estate sellers may become motivated. Investors with cash can buy when others are forced to sell. Liquidity turns crisis into opportunity.

The right cash level depends on income stability, expenses, debt, dependents, business risk, and investment strategy. A stable employee may need one level of reserves. An entrepreneur with irregular income may need more. A real estate investor with mortgages and repairs needs property reserves.

The poor financial pattern treats cash as money waiting to be spent. The wealthy pattern treats cash as defense and optionality.

14. Bonds and Income Securities

Bonds are often less exciting than stocks, businesses, or real estate, but they play an important role in wealth preservation and income planning. A bond is essentially a loan made to a government, municipality, or corporation. The investor receives interest and expects repayment of principal under the bond’s terms.

Bonds can provide income, stability, and diversification. They may reduce portfolio volatility and create predictable cash flows. For retirees, institutions, and wealthy families, bonds can help support spending needs without relying entirely on stock sales.

Different bonds carry different risks. U.S. government bonds are generally considered lower credit risk. Corporate bonds may pay higher yields but carry business risk. Municipal bonds may provide tax advantages for certain investors. High-yield bonds can behave more like risky credit investments than safe assets.

Bonds can lose value when interest rates rise. Issuers can default. Inflation can erode fixed payments. Long-term bonds can be sensitive to rate changes. This means bonds are not risk-free, even when they are safer than many other assets.

Wealth builders use bonds strategically. Younger investors may hold fewer bonds because they have long time horizons and can tolerate stock volatility. Older investors or people with near-term cash needs may hold more. Wealthy households may use bonds to match liabilities, preserve capital, or generate tax-efficient income.

Bonds may not make people rich quickly, but they can help people stay rich. That is an important distinction. Building wealth and preserving wealth are related but different games. The assets that create rapid growth may not be the same assets that protect a fortune once built.

15. Royalties

Royalties are payments received for the ongoing use of an asset. They can come from books, music, patents, mineral rights, licensing deals, franchises, software, photography, trademarks, characters, educational content, or creative works.

Royalty income is attractive because it can continue after the original work is complete. A songwriter writes once and may be paid for years. An author publishes a book and earns from future sales. An inventor licenses a patent. A photographer licenses images. A software developer receives recurring payments.

The key is ownership of something others want to use. Royalties are not guaranteed. Most books do not become bestsellers. Most songs do not generate meaningful income. Most patents do not become commercially valuable. But when a royalty-producing asset succeeds, it can create long-term cash flow.

Royalties can also be bought and sold. Investors sometimes purchase music catalogs, mineral royalties, or intellectual property rights. They evaluate expected future cash flows, legal rights, duration, and demand. This turns creative or resource-based income into an investable asset.

For individuals, the royalty mindset is powerful. Instead of only asking, “How can I get paid for this work once?” ask, “Can this work be packaged so it pays repeatedly?” A course, template, book, design, software tool, licensing agreement, or subscription product may create recurring value.

The challenge is distribution. A royalty asset without demand produces little. The market must know it exists, value it, and continue using it. Creation is only the first step. Protection, marketing, licensing, and maintenance matter too.

Royalties make people rich when creativity meets ownership and distribution.

16. Data and Audience Assets

In the modern economy, attention and data can become valuable assets when they are connected to trust and monetization. An audience may include email subscribers, readers, viewers, podcast listeners, community members, customers, or app users. Data may include customer preferences, purchasing behavior, search behavior, industry information, or proprietary research.

An audience is powerful because it lowers the cost of reaching people. A company with no audience must pay platforms, advertisers, influencers, or sales teams to get attention. A company with a loyal audience can launch products, test ideas, gather feedback, and sell with less friction.

This is why newsletters, podcasts, YouTube channels, niche communities, and specialized media brands can become valuable. The asset is not merely content. It is the relationship with a specific group of people who care about a specific topic.

Email lists are especially valuable because they are less dependent on platform algorithms than social media followers. A social account can be restricted, hacked, or weakened by algorithm changes. An email list is not perfect, but it gives the owner more direct access.

Data assets are valuable when they improve decisions. A company that understands customer behavior can design better products. An investor with proprietary market data may identify opportunities. A business with years of industry benchmarks can sell insights. A software platform with user behavior data can improve retention and pricing.

There are ethical and legal responsibilities. Data must be collected, stored, and used responsibly. Privacy matters. Trust matters. Misusing data can destroy reputation and create legal risk.

Audience and data assets are making people rich because they create leverage in a crowded marketplace. When you control attention and insight, you can build businesses faster.

17. Farmland and Agricultural Assets

Farmland is one of the oldest productive assets. It can produce income through crops, leases, livestock, timber, conservation programs, or specialty agriculture. It can also appreciate over time, especially when high-quality land is scarce and demand for food remains durable.

Farmland attracts wealthy investors because it has real-world utility. People need food. Productive land has intrinsic economic purpose. Unlike some speculative assets, farmland can generate value from actual production.

There are different ways to own agricultural assets. A person may buy farmland directly and lease it to operators. They may invest in agricultural partnerships. They may own timberland. They may invest in companies connected to food production, irrigation, fertilizer, equipment, storage, or distribution.

Direct farmland ownership requires specialized knowledge. Soil quality, water rights, crop economics, tenant quality, climate risk, commodity prices, equipment needs, and local regulations all matter. A beautiful piece of land may be a poor investment if it lacks productive capacity or reliable operators.

Farmland may also serve as an inflation hedge because food and land values can rise over long periods. But it is not risk-free. Weather, drought, pests, disease, commodity price swings, political policy, and changing consumer demand can affect returns.

The wealthy often like farmland because it is tangible, scarce, and productive. It does not depend on an app staying popular or a trend continuing. It depends on one of the most basic human needs.

For ordinary investors, direct farmland may be difficult, but the principle remains useful: assets tied to essential needs can have durable value.

18. Precious Metals and Hard Assets

Gold, silver, and other hard assets have long been used as stores of value. They do not produce cash flow like a business or rental property, but they can serve as protection against currency weakness, financial stress, geopolitical uncertainty, or extreme market fear.

Wealthy families sometimes hold a portion of assets in hard stores of value not to get rich quickly, but to preserve purchasing power across uncertain environments. Gold has survived many monetary systems. It is globally recognized, liquid in many markets, and independent of any single company’s earnings.

That said, precious metals are often misunderstood. Gold does not pay dividends. It does not innovate. It does not hire employees or produce rent. Its value depends largely on supply, demand, investor psychology, central bank behavior, inflation expectations, and confidence in currencies.

Hard assets can also include collectibles, art, rare coins, classic cars, gems, and other tangible stores of value. Some people have become rich through these markets, but they require deep expertise. The difference between a valuable collectible and an overpriced object can be enormous. Storage, insurance, authenticity, liquidity, and transaction costs matter.

For most people, hard assets should not replace productive assets. A portfolio made only of gold or collectibles may lack income and growth. But as a small part of a broader wealth strategy, hard assets can provide diversification and psychological comfort.

The key is to understand the role. Productive assets build wealth by generating cash flow and growth. Hard assets may preserve wealth when trust in financial systems weakens. Both can have a place, but they are not the same tool.

19. Private Equity and Private Investments

Private investments are ownership stakes in companies or assets that are not publicly traded. They may include private equity funds, venture capital, angel investments, private credit, real estate syndications, search funds, or direct ownership in private businesses.

These investments can make people rich because they may offer access to growth before companies become public or before assets are widely recognized. Early investors in successful private companies can earn extraordinary returns. Private business buyers can acquire cash-flowing companies and improve operations. Private real estate sponsors can assemble deals that individual investors might not find alone.

But private investments are also risky and often illiquid. Investors may not be able to sell for years. Information may be limited. Valuations may be uncertain. Fees can be high. Managers may underperform. Startups can fail completely. Real estate syndications can suffer from bad financing, weak operators, or market downturns.

Wealthy investors often access private deals because they have networks, accreditation, capital, advisers, and risk tolerance. They may diversify across many deals, knowing some will fail. They may negotiate terms. They may understand the operator’s track record. They may have the financial strength to wait.

Ordinary investors should be cautious. The phrase “private investment” can sound exclusive, but exclusivity does not guarantee quality. Sometimes the best opportunities are private. Sometimes private deals are simply expensive, illiquid, and poorly governed.

The lesson is that private ownership can create wealth when the investor understands the business, the risks, the people, the structure, and the exit path. Without that understanding, private investing can become speculation wrapped in sophistication.

20. Artificial Intelligence Tools and Automation Systems

Artificial intelligence is not an asset in the traditional sense unless it is owned, built into a product, or used to create economic leverage. But people and companies are becoming wealthier by using AI tools and automation systems to increase productivity, reduce costs, create products, analyze data, and scale output.

A small business can use automation to handle customer service, scheduling, marketing, bookkeeping, reporting, lead follow-up, or content workflows. A software company can integrate AI into products. A consultant can use AI to accelerate research and analysis. A creator can use AI-assisted tools to produce faster. An investor can use data tools to screen opportunities.

The asset is not merely the tool. Tools are widely available. The asset is the system built around the tool: workflows, proprietary data, trained processes, customer integration, and human judgment. If everyone can access the same technology, advantage comes from using it better.

AI can make people rich when it increases output per person. A small team can do what once required a larger team. A solo entrepreneur can launch faster. A company can personalize service at scale. A professional can handle more complex work. This productivity gain can translate into higher margins and faster growth.

But AI also creates risk. Some skills may become less valuable. Some business models may be disrupted. Low-quality automated content can damage trust. Overreliance on tools can create errors. Privacy, accuracy, and ethics matter.

The wealthy approach emerging technology with both curiosity and discipline. They do not assume every trend is a gold rush. They ask where the technology creates measurable value, who captures that value, and what asset can be built from it.

In the AI era, the rich may not be the people who merely use tools. They may be the people who own the workflows, products, data, brands, and companies that make the tools economically useful.

21. Energy Assets

Energy is central to modern civilization. Homes, factories, vehicles, data centers, hospitals, farms, and communication systems all require energy. This makes energy assets important for wealth creation.

Energy assets can include oil and gas interests, mineral rights, pipelines, renewable energy projects, battery storage, solar farms, wind farms, energy infrastructure companies, utilities, and service providers. Some produce income through royalties or distributions. Others appreciate as demand grows or technology improves.

Energy wealth often comes from control of scarce resources or essential infrastructure. A landowner with mineral rights may receive royalties. An investor in pipeline infrastructure may receive income tied to transport. A developer of renewable projects may benefit from long-term power purchase agreements. A company that solves energy storage problems may become extremely valuable.

Energy investing is complex. Commodity prices are volatile. Regulations matter. Environmental concerns are significant. Technology changes. Capital requirements can be high. Political decisions can affect profitability. Projects can take years to develop.

Still, energy remains a foundational asset class because economic growth requires power. The rise of artificial intelligence, electric vehicles, cloud computing, and industrial reshoring has increased attention on electricity demand, grid capacity, and energy infrastructure.

For individuals, energy exposure may come through public companies, funds, partnerships, royalty interests, or private projects. Each structure has different risks and tax implications.

The broader principle is that assets tied to essential infrastructure can create durable wealth. Energy is not a trend. It is a requirement.

22. Education and Credential Assets

Education is not automatically an asset. A degree that creates debt without increasing earning power can become a liability. But the right education, credential, license, or certification can be a powerful wealth-building asset.

Medical licenses, legal credentials, engineering qualifications, accounting certifications, aviation licenses, trade licenses, cybersecurity certifications, project management credentials, financial designations, and technical training can all increase earning potential. In some fields, a credential is the gatekeeper to high-income work.

The asset value of education depends on return on investment. What does it cost? How long does it take? What income can it realistically produce? How stable is demand? How transferable is the skill? How much debt is required? What are the opportunity costs?

Wealth builders evaluate education like investors. They do not assume all education is good at any price. They compare programs, outcomes, costs, scholarships, employer reimbursement, apprenticeship routes, and alternative paths.

A credential can also create business opportunities. A licensed professional can start a practice. A certified expert can consult. A trained technician can build a service company. A specialized qualification can become the foundation for equity.

The danger is prestige without economics. Some people buy expensive degrees because they want status, not because the market will reward the investment. Others avoid education entirely because they fear cost, even when a practical credential could transform income.

The wealthy mindset asks: will this education increase my ability to create value, earn income, own assets, or access opportunity? If yes, it may be one of the best investments available.

23. Franchises

A franchise is a business model where an owner operates under an established brand and system. Common examples include restaurants, fitness centers, cleaning companies, tutoring centers, home services, hotels, and retail concepts. The franchisee pays fees and follows the franchisor’s model in exchange for brand recognition, training, systems, and support.

Franchises can make people rich because they reduce some of the uncertainty of starting from scratch. The product, branding, operations, vendor relationships, and customer expectations may already be developed. A strong franchise system can help an owner scale faster than an independent startup.

But franchises are not guaranteed wealth machines. Startup costs can be high. Royalties and marketing fees reduce profit. Locations matter. Labor matters. The franchisor’s reputation matters. The owner must follow rules. Some franchisees discover that they bought themselves an expensive job rather than a scalable asset.

The best franchise operators think like business owners, not passive investors. They study unit economics, margins, labor models, lease terms, financing, local demand, competition, and expansion potential. They speak with existing franchisees. They understand the difference between revenue and owner profit.

Franchise wealth often comes from multi-unit ownership. One location may provide income. Several well-run locations can create management leverage and enterprise value. The owner builds a local operating company under a larger brand umbrella.

For people who want business ownership but prefer a proven model, franchises can be attractive. The key is due diligence. A franchise is still a business, and a business must produce profit after all costs, fees, debt service, and owner effort are considered.

24. Debt as an Asset When You Are the Lender

Most people experience debt as a burden. They owe money on credit cards, cars, student loans, mortgages, or personal loans. Wealthy people often experience debt from the other side. They lend money and receive interest.

Debt can be an asset when you own the loan. A bond is one example. Private credit is another. Mortgage notes, business loans, hard money lending, peer lending, and structured credit are all ways investors may act as lenders.

The lender’s wealth comes from interest, fees, collateral, and repayment terms. Instead of paying interest, the investor collects it. This is a major shift. The same financial system that drains borrowers can enrich lenders.

Private lending can produce attractive income, but it requires careful risk control. Borrowers can default. Collateral can be overvalued. Legal enforcement can be slow. Economic downturns can weaken repayment. A high interest rate may signal high risk, not easy profit.

Professional lenders focus on underwriting. They evaluate borrower quality, collateral value, loan-to-value ratios, cash flow, legal documents, seniority, covenants, and exit strategies. They ask what happens if everything goes wrong.

For ordinary investors, high-quality bonds or bond funds may provide simpler exposure to lending. More advanced investors may explore private credit with caution and professional advice.

The wealth lesson is profound: money can be positioned either as a servant or a master. Borrowers work to pay capital. Lenders allow capital to work for them.

25. The Home You Can Actually Afford

A primary residence is complicated. It is both a place to live and a financial asset. It can build wealth through appreciation, mortgage paydown, stability, and forced savings. But it can also become a financial trap if purchased at the wrong price or with too much debt.

Many households think buying the biggest possible home is a sign of wealth. Wealth builders are more careful. They understand that a home carries hidden costs: property taxes, insurance, repairs, utilities, furnishings, maintenance, transaction fees, and opportunity cost. A house that consumes all surplus cash can delay investing for years.

A home becomes a wealth-building asset when it is affordable, located in a stable or improving area, financed responsibly, maintained well, and integrated into a broader plan. It can provide housing security and long-term equity. It can protect against rent increases. It can become a source of future options through sale, refinancing, downsizing, or rental conversion.

But a home is not automatically an investment just because it appreciates. If the owner spends decades paying interest, taxes, repairs, and upgrades, the real return may be lower than expected. Emotional attachment can also distort decisions. People may overbuy because they imagine a lifestyle, not because the numbers work.

The wealthy do not always buy the most house they can qualify for. They buy the house that supports the life and balance sheet they want. That difference matters.

Homeownership can help people become rich when it creates stability and equity without destroying cash flow. It becomes dangerous when it turns into a monument to status.

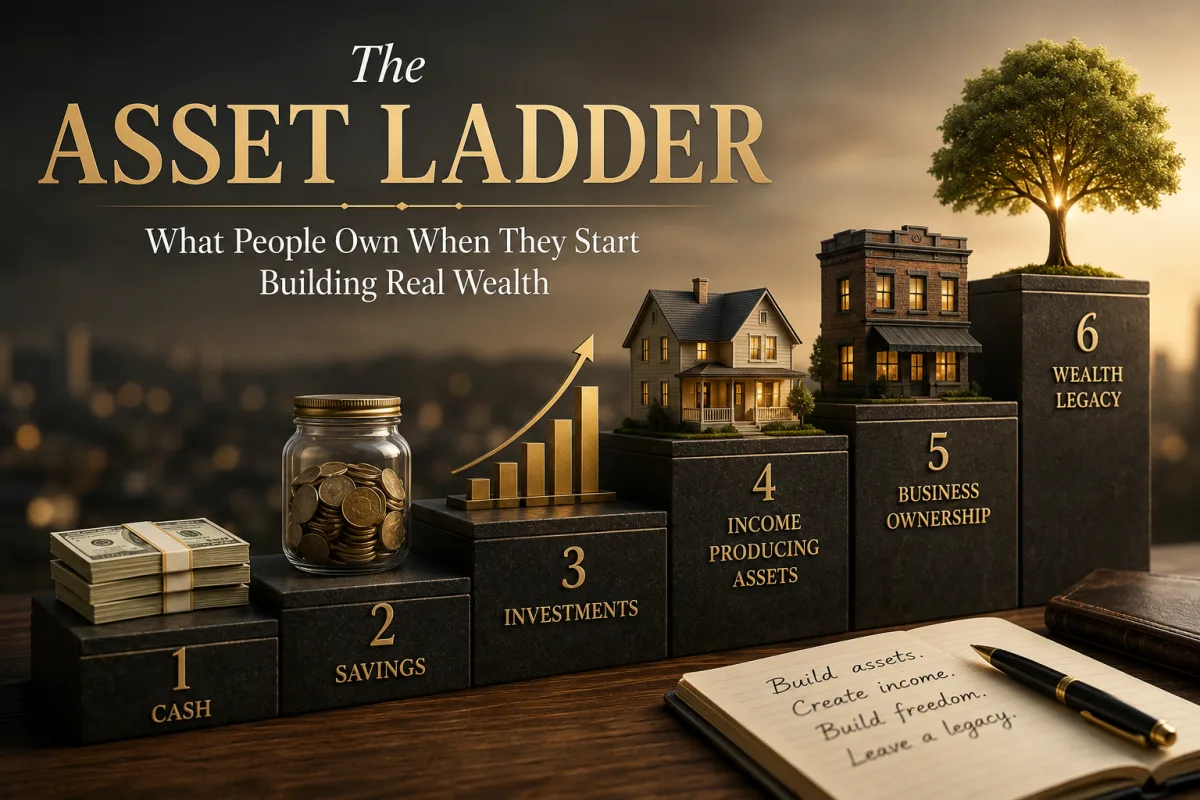

The Asset Ladder: How Wealth Usually Progresses

People rarely start by owning advanced assets. Most begin with income. Then, if they manage that income well, they build savings. Savings create stability. Stability allows investing. Investing creates ownership. Ownership creates cash flow and appreciation. Cash flow and appreciation create more capital. More capital allows larger assets. This is the asset ladder.

The first rung is human capital: skills, discipline, health, and earning power. Without income or value creation, it is difficult to acquire financial assets.

The second rung is liquidity: emergency savings, cash reserves, and reduced financial fragility. This protects the person from being forced backward by every unexpected event.

The third rung is simple ownership: retirement accounts, index funds, and diversified investments. These build wealth quietly and teach the habit of investing.

The fourth rung is concentrated skill-based opportunity: a business, real estate, career equity, or specialized expertise. This is where wealth can accelerate, but risk also increases.

The fifth rung is advanced ownership: private investments, intellectual property, tax-advantaged structures, multi-unit businesses, land, lending, and estate planning. These require more knowledge, capital, and professional advice.

The mistake many people make is trying to jump to the top without building the lower rungs. They chase private deals before building an emergency fund. They speculate in trends before learning basic investing. They buy rental property without cash reserves. They start businesses without understanding cash flow. They use leverage before they have discipline.

Wealth is built faster when the ladder is climbed in order. Each rung supports the next.

What Makes an Asset Truly Powerful?

Not all assets are equal. Some grow slowly. Some produce income. Some require constant work. Some are liquid. Some are difficult to sell. Some protect wealth. Some create wealth. Some only appear valuable during bubbles.

A powerful asset usually has several traits.

First, it has demand. Someone must want what the asset produces or represents. A business needs customers. A rental property needs tenants. A stock needs underlying company profits. A royalty needs users. Land needs future utility.

Second, it has durability. Wealth-building assets should not depend entirely on a temporary trend. They should have value beyond the current excitement.

Third, it has scalability or appreciation potential. The asset should be able to grow in value, increase output, raise prices, expand reach, or become more desirable over time.

Fourth, it has defensibility. A strong brand, location, patent, network, data set, cost advantage, license, or customer relationship can protect value from competition.

Fifth, it has favorable economics. Revenue is not enough. The asset should have profit, cash flow, or a clear path to value creation after costs.

Sixth, it fits the owner. A rental property may be a great asset for one person and a nightmare for another. A business may create wealth for one owner and stress for another. The best asset is not the one that sounds impressive. It is the one you can understand, manage, hold, and improve.

Why Income Alone Does Not Make People Rich

High income can hide weak financial habits. A person earning a large salary may still be financially dependent if they spend most of it. Expensive houses, cars, schools, vacations, staff, taxes, and debt can absorb income quickly. The outside world sees success. The balance sheet may tell a different story.

Assets solve a problem that income cannot solve alone: they create value without requiring every dollar to come from current labor. A portfolio can grow while the owner works. A rental property can collect rent while the owner sleeps. A business can operate through employees and systems. Intellectual property can earn royalties. Land can appreciate while sitting quietly. A reputation can attract opportunities without cold outreach.

This is the transition from labor income to asset income. It is not instant. It may take years. In the beginning, labor funds the assets. Later, assets begin to fund the life.

That is financial freedom in practical terms. It is not necessarily private jets or mansions. It is the point where your assets carry enough of the burden that your choices expand. You can work differently. Negotiate better. Take time off. Leave bad environments. Invest in health. Help family. Build legacy.

The rich are not rich simply because they earn more. They are rich because they own more of the things that benefit from growth.

The Danger of Buying Assets You Do Not Understand

The desire to get rich can make people vulnerable. When an asset class becomes popular, promoters appear. They sell dreams, shortcuts, urgency, and social proof. They make risk look small and returns look inevitable.

This happens in real estate, crypto, stocks, private equity, franchises, online businesses, collectibles, land, and every other wealth category. The asset may be legitimate, but the investor may still lose money by buying at the wrong price, using too much debt, trusting the wrong people, or misunderstanding the economics.

The first rule of asset ownership is to know what you own. How does it make money? What can go wrong? What are the costs? How liquid is it? Who controls it? What assumptions must be true for the investment to work? What happens in a recession? What happens if interest rates rise? What happens if customers leave? What happens if regulations change?

Wealthy investors are not immune to mistakes, but experienced ones respect risk. They know that return of capital matters before return on capital. They know that a bad deal can damage years of progress.

The poor investor asks, “How much can I make?” The disciplined investor asks, “How much can I lose, and can I survive it?”

How Ordinary People Can Begin Buying Assets

The asset ladder can seem intimidating, but the beginning is simple. Start by creating a surplus. Spend less than you earn, or increase what you earn, or both. Without surplus, asset buying remains theory.

Next, build a cash buffer. This prevents emergencies from forcing debt or liquidation. A person with no savings may have to sell investments at the worst possible time. Liquidity protects the plan.

Then buy simple assets consistently. Retirement accounts, diversified funds, and education that increases earning power are often the most practical starting points. These may not feel exciting, but they build the habit of ownership.

As knowledge and capital grow, consider more active assets. A small business. A rental property. A digital product. A professional certification. A side income stream. The goal is not to chase everything. The goal is to find the asset class that fits your skills, temperament, and resources.

Reinvest gains. This is where wealth accelerates. Income from assets should not immediately become lifestyle spending. In the early stages, asset income should buy more assets. Dividends buy more shares. Business profits fund growth. Rental cash flow builds reserves or funds the next property. Royalties fund new intellectual property. Skills fund higher income, which funds investments.

Finally, protect what you build. Use insurance. Avoid reckless debt. Keep records. Diversify. Pay taxes properly. Update legal documents. Maintain health. Choose partners carefully.

Wealth building is not only acquisition. It is also preservation.

The Mindset Shift: From Consumer to Owner

The most important asset may be the mindset that seeks assets in the first place. Consumers ask, “What can I buy?” Owners ask, “What can I build or acquire that will pay me later?”

A consumer sees a successful company and buys its products. An owner asks whether they can buy its stock. A consumer watches content. An owner builds a media asset. A consumer pays rent. An owner studies real estate. A consumer uses software. An owner asks who profits from it. A consumer follows trends. An owner asks which assets will remain valuable after the trend fades.

This does not mean life should become joyless or purely financial. Money is meant to support a meaningful life. But the order matters. When consumption always comes first, ownership remains distant. When ownership comes first, consumption can eventually be funded by assets rather than constant labor.

The wealthy are not wealthy because they never spend. They are wealthy because they buy assets before they buy too many symbols of wealth.

The Assets That Matter Most

There is no single asset that makes everyone rich. Stocks work for patient investors. Real estate works for disciplined operators. Businesses work for builders. Skills work for ambitious learners. Intellectual property works for creators. Networks work for trustworthy people. Cash works for resilience. Bonds work for preservation. Land works for patient capital. Digital assets work for people who understand distribution.

The best asset depends on the person. A doctor may build wealth through high income, retirement accounts, index funds, and medical practice ownership. A software developer may build wealth through equity compensation, startups, and digital products. A contractor may build wealth through a service business and rental properties. A writer may build wealth through audience, books, royalties, and intellectual property. A family may build wealth through disciplined investing and home equity.

The asset is only one side of the equation. The owner matters too. Knowledge, discipline, patience, ethics, and risk management determine whether an asset becomes wealth or regret.

The central truth is clear: people become rich by owning things that grow, pay, or create leverage. The sooner a person understands that, the sooner they stop measuring success only by income and start measuring it by ownership.

The Quiet Formula

Wealth rarely arrives all at once. It usually follows a quieter formula.

Earn money. Keep part of it. Buy assets. Improve those assets when possible. Let time work. Reinvest the returns. Avoid catastrophic mistakes. Increase earning power. Buy more assets. Protect the balance sheet. Repeat for years.

This formula is not glamorous, but it is powerful. It works because it aligns with compounding. Each asset becomes a worker. Each worker produces more capital. That capital buys more workers. Eventually, the financial system begins to support itself.

The poor remain trapped when all income becomes consumption. The middle class remains pressured when all income becomes payments. The wealthy become free when income becomes ownership.

That is the asset ladder. It is how people move from working for money to having money work for them.

The question is not simply how much you earn. The better question is: what do you own that can make you richer while you sleep?

Answer that honestly, and you will know where you are on the ladder.