The Protection Gap: How to Choose Term Life Insurance Without Paying for Extras You Don’t Need

Life insurance is one of the few financial products people buy hoping their family will never need to use. That emotional reality makes it different from most purchases. A person can compare mobile phone plans, mortgage rates, or investment fees with relative detachment. Life insurance asks a harder question: what would happen financially if someone’s income, care, labor, or support suddenly disappeared from the household?

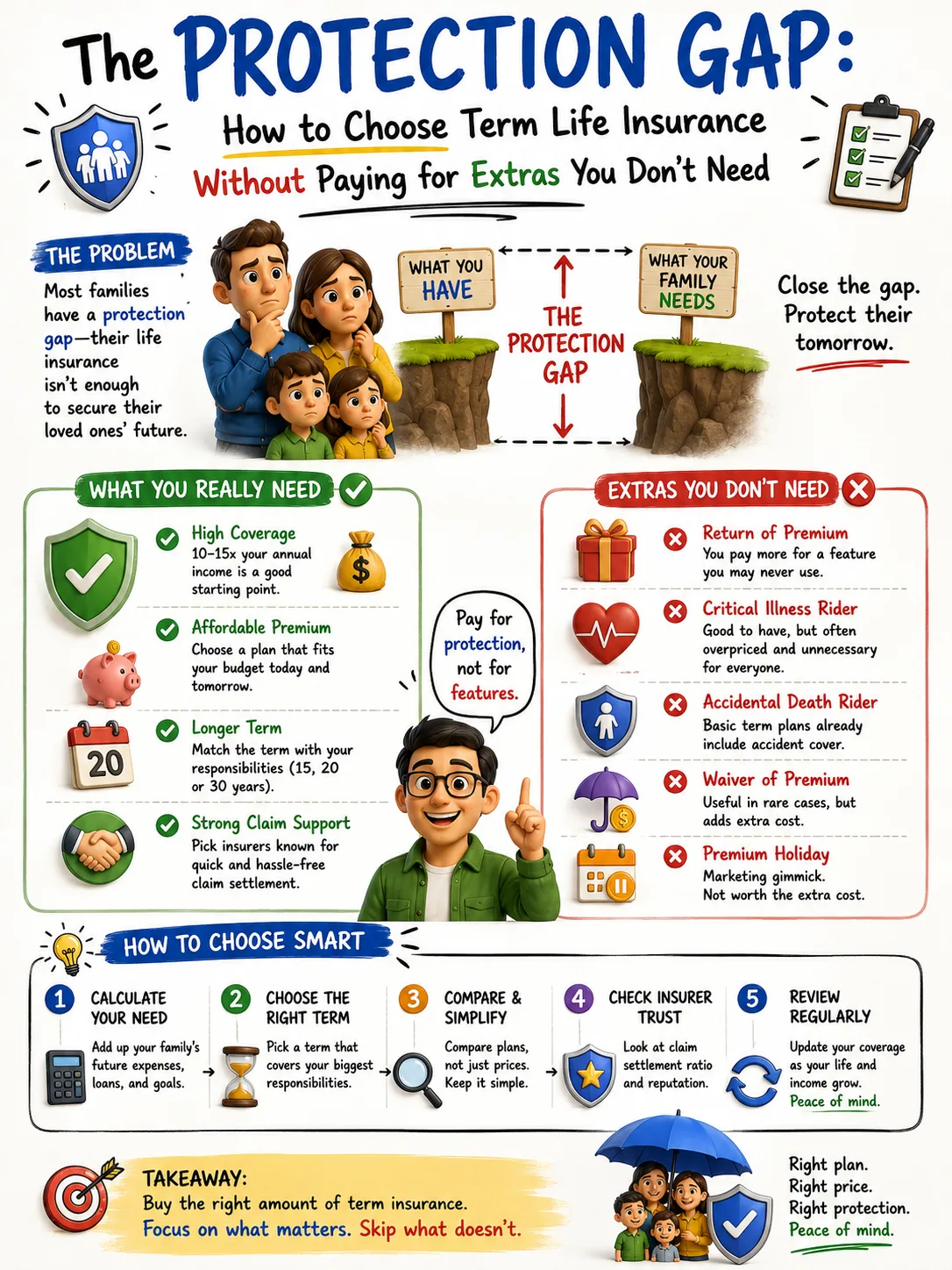

That question is uncomfortable, which is why many people delay answering it. Others move too quickly and buy whatever policy is presented to them first. Some buy too little coverage because they want the cheapest premium possible. Others buy expensive extras because they are afraid of leaving their family exposed. The result is often one of two mistakes: a protection gap or an overbuilt policy.

Term life insurance is designed to solve a specific problem. It provides a death benefit for a set period of time, such as 10, 20, or 30 years. If the insured person dies during that term and the policy is active, the insurer pays the death benefit to the beneficiaries. If the term ends while the insured person is still alive, the coverage usually expires unless renewed or converted under the policy’s rules.

That simplicity is the strength of term life insurance. It is not meant to be an investment account, a retirement plan, or a complicated wealth product. It is financial protection during the years when other people would suffer financially if the insured person were gone. For many households, that makes term life one of the most practical forms of life insurance.

But practical does not mean automatic. The right term life policy depends on the household’s income, debts, dependents, savings, future obligations, and timeline. The goal is not to buy the largest policy available. The goal is to buy enough protection for the right number of years at a cost that leaves room for the rest of the financial plan.

Choosing term life insurance well requires discipline. It means separating genuine protection from emotional upselling. It means understanding which riders may be useful and which ones may add cost without adding much value. It means comparing policies based on financial need rather than fear. Above all, it means remembering the purpose of insurance: to transfer a risk that the household cannot comfortably absorb on its own.

What Term Life Insurance Is Really For

Term life insurance exists to replace financial value that would be lost if the insured person died during a specific period. That value may be income, caregiving, debt support, education funding, business continuity, or the ability of surviving family members to remain financially stable.

A parent with young children may need term life insurance because children depend on the parent’s income, time, and care. A married couple with a mortgage may need coverage so the surviving spouse can remain in the home or pay down debt. A business owner may need coverage to protect partners, employees, or family members from financial disruption. A stay-at-home parent may need coverage because replacing childcare, household management, transportation, and caregiving can be expensive.

The policy is not purchased because death is likely in the near future. It is purchased because the financial consequences would be severe if it happened during the years of dependency.

This distinction matters. Insurance is not about predicting tragedy. It is about preparing for a risk that would be too large to self-fund. A household may be unlikely to experience the event, but if the event would cause devastating financial harm, insurance may be appropriate.

Term life insurance is especially useful when the need is temporary. Children eventually become adults. Mortgages eventually decline or are paid off. Retirement savings hopefully grow. A spouse may become financially independent. A business loan may be repaid. The purpose of term coverage is to protect the vulnerable period before the household has enough assets or independence to absorb the loss.

Why Term Life Is Often Cheaper Than Permanent Life Insurance

Term life insurance is usually less expensive than permanent life insurance for the same death benefit because it covers a defined period and does not typically build cash value. Permanent life insurance, such as whole life or universal life, is designed to last longer and may include a savings or investment-like component. Those features increase cost and complexity.

This does not mean permanent life insurance is always bad. It can have uses in estate planning, business planning, tax planning, and certain long-term dependent-care situations. But many ordinary households looking for income replacement do not need the complexity of permanent coverage. They need a large death benefit during the years when their family is most financially exposed.

Term life insurance often provides that protection more affordably. A lower premium can allow the household to buy adequate coverage while still investing, saving, paying down debt, and funding other goals. This is important because insurance should protect the financial plan, not consume it.

An expensive policy that causes a family to underfund emergency savings or retirement may create a different kind of risk. Insurance decisions should never be made in isolation. The premium must fit into the broader household cash flow.

The First Question: Who Depends on You Financially?

The starting point for choosing term life insurance is dependency. Who would be financially affected if your income, labor, or support disappeared?

Dependents may include a spouse, children, aging parents, siblings, business partners, or anyone else who relies on your financial contribution. They may also include people who rely on unpaid work. A stay-at-home parent may not earn a paycheck, but their work has real economic value. Childcare, transportation, cooking, scheduling, household administration, elder care, and emotional labor may all need replacement if that parent is gone.

A single person with no dependents, no shared debts, and enough savings to cover final expenses may need little or no life insurance. A parent with young children and a mortgage may need substantial coverage. A married couple with no children but one spouse depending heavily on the other’s income may still need coverage. A business owner with personally guaranteed loans may need protection even if family dependents are limited.

The question is not, “Should everyone have life insurance?” The better question is, “Would someone face financial hardship if I died during the next several years?”

If the answer is yes, term life insurance deserves serious consideration.

How Much Term Life Insurance Do You Need?

Many people are told to buy life insurance equal to a multiple of income, such as 10 times annual earnings. This rule can be a useful starting point, but it is too simple to be the final answer. Two people with the same income may need very different amounts of coverage.

A person earning $70,000 with three young children, a mortgage, little savings, and a spouse who works part time may need much more coverage than a person earning the same amount with no children, no debt, and significant investments. Income matters, but obligations matter just as much.

A better approach is to estimate the actual financial gap the policy must fill. This usually includes several categories: income replacement, debt repayment, education costs, childcare or caregiving costs, final expenses, and a cushion for transition.

Income replacement is often the largest need. If your family depends on your income, ask how many years that income would need to be replaced. The answer may depend on the age of your children, your spouse’s earning ability, retirement savings, and other assets.

Debt repayment is another major factor. A surviving spouse may not need every debt paid off immediately, but life insurance can prevent debt from becoming overwhelming. Mortgages, personal loans, private student loans, business debts, and credit card balances should be reviewed carefully.

Education funding may matter if children are young and college or vocational training support is a family goal. The amount does not have to cover every possible education expense, but it should reflect realistic intentions.

Childcare and household support are often underestimated. If one parent dies, the surviving parent may need paid childcare, tutoring, transportation help, housekeeping, elder care, or more flexible work arrangements. These costs can be substantial.

Final expenses and transition costs should also be included. Funerals, legal paperwork, travel, unpaid leave, medical bills, and immediate household adjustments can create short-term pressure.

After adding these needs, subtract existing resources such as savings, investments, existing life insurance, survivor benefits, and assets that could reasonably be used. The remaining gap is the amount of coverage to consider.

A Practical Coverage Example

Consider a household with two parents and two young children. One parent earns most of the income. The family has a mortgage, modest retirement savings, and limited emergency savings. If the higher-earning parent died, the surviving parent would need time, cash, and flexibility.

The family might estimate that they need enough insurance to cover several years of income replacement, pay off or reduce the mortgage, fund part of the children’s education, provide childcare support, and create a transition cushion. They would then subtract current savings and any existing employer-provided coverage.

The final number may be larger than the family expected. That does not mean they should panic or buy every rider offered. It means they have identified the true protection gap. Term life insurance can often cover that gap at a lower cost than many other forms of life insurance.

Now consider a different household. A couple has no children, both spouses earn similar incomes, they rent, and they have strong savings. Their life insurance need may be much smaller. They may only need enough to cover shared obligations, final expenses, and a temporary adjustment period.

The right amount is personal. It should be based on the financial consequences of loss, not on a generic sales formula.

Choosing the Right Term Length

Term length should match the period of financial vulnerability. The policy should last long enough to cover the years when dependents, debts, or obligations would create hardship.

A 20-year term may make sense for parents with young children who want coverage until the children are adults. A 30-year term may fit a new mortgage or a longer dependency period. A 10-year term may work for someone with older children, a short remaining mortgage, or a temporary business obligation.

The temptation is to choose the shortest term because it has the lowest premium. That can be a mistake if the need lasts longer. Buying a 10-year policy when the household really needs 25 years of protection may create trouble later. When the policy expires, the insured person will be older and may have health changes that make new coverage more expensive or difficult to obtain.

The opposite mistake is buying a much longer term than necessary. A 30-year term may be useful for some families, but unnecessary for someone whose dependents will be financially independent in 12 years and whose mortgage is nearly paid off. Longer terms usually cost more because the insurer is covering older ages.

The goal is to match the term to the risk. Ask: when would my family no longer need this death benefit? The answer may be when children are independent, the mortgage is manageable, the surviving spouse has enough assets, or retirement savings are strong.

Why Employer Life Insurance Is Usually Not Enough

Many workers receive group life insurance through an employer. This is helpful, but it is often not enough. Employer coverage may be limited to one or two times salary, which may fall far short of the household’s actual need.

Employer coverage is also tied to employment. If the worker changes jobs, loses the job, becomes self-employed, or experiences a health issue that affects employment, the coverage may reduce or disappear. Some plans allow conversion or portability, but the terms may not be as favorable as buying individual coverage while healthy.

Employer life insurance should be counted as part of the protection picture, but it should not be the entire plan for a household with serious dependency needs. Individual term life insurance gives the family more control because the policy is not dependent on a particular job.

A practical approach is to treat employer coverage as supplemental. It can add protection, but the core coverage should often be personally owned if the family depends on it.

Understanding Premiums

The premium is the price paid for coverage. For level term policies, the premium usually stays the same during the selected term. This predictability is useful because the household can plan around a stable cost.

Premiums are influenced by age, health, coverage amount, term length, gender, smoking status, medical history, family history, occupation, hobbies, and sometimes driving record or lifestyle factors. Generally, younger and healthier applicants pay less because the risk to the insurer is lower.

This creates an important planning lesson: waiting can make coverage more expensive. A person who knows they need life insurance should not delay unnecessarily. Health can change. Age always increases. The best time to secure coverage is often when the need exists and the applicant is still healthy enough to qualify for favorable rates.

But speed should not replace comparison. Premiums can vary among insurers for similar coverage. One company may view a health condition differently from another. Comparing several quotes can save money over the life of the policy.

Do Not Buy Based on Premium Alone

Price matters, but the cheapest policy is not always the best choice. A good term life policy should come from a financially strong insurer, have clear terms, offer the needed coverage amount and length, and include appropriate conversion options if those matter to the buyer.

The policy’s definitions and limitations should be understood before purchase. Applicants should know when coverage starts, when it ends, how premiums work, what happens if a payment is missed, whether the policy is renewable, whether it is convertible, and what exclusions apply.

Most people do not need a complicated policy, but they do need a reliable one. Insurance is a promise. The quality of that promise matters.

A slightly lower premium may not be worth it if the policy structure is weak, the insurer has poor service, or important options are missing. The best value is not always the lowest monthly cost. It is the right protection at a fair price from a trustworthy company.

Medical Exams and No-Exam Policies

Some term life policies require a medical exam. Others offer simplified issue or no-exam underwriting. No-exam policies can be convenient, especially for people who want faster approval. However, convenience may come at a higher premium or lower coverage limit.

Fully underwritten policies may take longer because the insurer reviews health information more deeply. But healthy applicants may receive better rates through full underwriting. Someone in excellent health should not assume a no-exam policy is the cheapest option.

For applicants with certain health conditions, underwriting can be more complicated. Different insurers may price the same condition differently. Working with an independent agent or comparing multiple companies can be useful because one insurer may be more favorable than another.

The key is honesty. Life insurance applications require accurate information. Misrepresenting health, smoking, income, risky hobbies, or medical history can create serious problems later, including denial of a claim during the contestability period. The purpose of insurance is to protect the family. That protection should not be weakened by inaccurate answers.

Understanding Riders

Riders are optional features that can be added to a life insurance policy. Some riders are included automatically. Others cost extra. Riders can be useful, but they are also where unnecessary extras often enter the policy.

The most important question for any rider is simple: does this solve a real problem that is not already covered elsewhere?

If the answer is yes, the rider may be worth considering. If the answer is no, it may only increase the premium without improving the household’s financial security.

Life insurance should not become overloaded with features simply because they sound reassuring. Every added cost reduces money available for savings, investing, debt repayment, emergency funds, and other forms of protection.

The Waiver of Premium Rider

A waiver of premium rider may allow the policyholder to stop paying premiums if they become disabled under the rider’s definition. The policy remains active even though premiums are waived.

This rider can be useful because disability can damage income and make it harder to keep insurance in force. However, the rider’s value depends on its cost, definitions, waiting period, and exclusions.

Before paying for this rider, the buyer should compare it with disability insurance. Disability insurance directly replaces part of income if the insured person cannot work. A waiver of premium rider only keeps the life insurance policy active. It does not pay household bills.

For some buyers, the rider is worth the modest added cost. For others, the money may be better directed toward a strong disability insurance policy. The decision should be based on the broader protection plan.

The Accelerated Death Benefit Rider

An accelerated death benefit rider allows the insured person to access part of the death benefit while still alive if diagnosed with a qualifying terminal illness. Many policies include some version of this rider at no extra cost, though terms vary.

This rider can provide flexibility during a difficult period. It may help with medical bills, care needs, or family expenses. However, using it reduces the amount paid to beneficiaries after death.

Buyers should understand the conditions required to use the rider, any fees, how much can be accessed, and how the remaining death benefit is affected. If included at no additional cost, it can be a valuable feature. If it costs extra, the buyer should weigh the price against the likelihood and usefulness of the benefit.

Child Term Riders

A child term rider provides a small amount of life insurance coverage for children. This is emotionally sensitive because no parent wants to imagine needing it. The financial purpose is usually to cover final expenses and allow parents time away from work during a crisis.

Child riders are often inexpensive, but they should not distract from the main insurance need: protecting the income and caregiving capacity of the parents. A household should not buy child coverage while leaving the parents underinsured.

For some families, a child rider provides peace of mind at a low cost. For others, an emergency fund may be a better solution. The rider should be viewed as limited protection, not a core wealth strategy.

Return of Premium Riders

A return of premium rider refunds some or all premiums if the insured person outlives the term. This sounds attractive because many people dislike the idea of paying for insurance and receiving nothing back.

But term life insurance is not a savings account. It is risk protection. The reason standard term life is affordable is that it pays only if the insured dies during the term. Return of premium features usually increase the cost significantly.

The buyer should compare the added cost with what could be done by investing or saving the difference. In many cases, a standard term policy plus disciplined investing may be more flexible and efficient. The return of premium feature can appeal emotionally, but it may not be the best financial use of money.

This is one of the clearest examples of an extra that should be examined carefully. It solves the emotional discomfort of “getting nothing back,” but the household may pay heavily for that feeling.

Accidental Death Benefit Riders

An accidental death benefit rider pays an additional amount if death results from a qualifying accident. The appeal is obvious: it can increase the payout for a relatively low additional premium.

The limitation is that families need financial protection regardless of how death occurs. A surviving spouse or child does not need less money because the death resulted from illness rather than an accident. The core policy should provide adequate coverage for all covered causes, not rely on an accidental death rider to make the benefit sufficient.

Accidental death riders can create a false sense of protection. A person may see a larger potential payout and feel well covered, even though the extra benefit only applies in specific circumstances. For most households, it is better to buy the right base death benefit than to depend on accident-only enhancements.

Conversion Options

A conversion option allows the policyholder to convert some or all of a term policy into permanent life insurance without going through new medical underwriting. This can be valuable if health changes and the insured person later needs lifelong coverage.

Not everyone will use conversion. Many term buyers never need permanent insurance. But having the option can add flexibility. The details matter: when conversion is allowed, what products are available, how premiums are calculated, and whether the option expires before the term ends.

A strong conversion option may be worth considering, especially for people who want flexibility or have family histories that could affect future insurability. However, buyers should not purchase an expensive policy solely because conversion is mentioned. They should understand the actual terms.

Renewability

Some term policies are renewable after the initial term, but renewal premiums may rise sharply because they are based on older age. Renewability can provide temporary protection if the insured still needs coverage after the term ends and cannot qualify for a new policy.

However, renewal should not be the primary plan. It is often expensive. The better strategy is to choose an appropriate term length at the beginning. Renewal is a backup, not a substitute for proper planning.

Avoiding the Most Common Upsells

Unnecessary extras often enter the insurance conversation through emotion. A feature sounds comforting, so the buyer accepts it without analyzing the cost. Over time, several small extras can make the policy more expensive than it needs to be.

The most common upsells include return of premium features, accidental death add-ons, excessive riders, larger coverage amounts than justified by the financial need, and permanent insurance presented to buyers who mainly need temporary protection.

This does not mean every extra is bad. Some riders are useful. Some families need specialized coverage. Some permanent policies are appropriate. The danger is buying complexity without a clear purpose.

A disciplined buyer should ask four questions before accepting any add-on. What specific risk does this cover? Do I already have protection for that risk? How much does the rider cost over the life of the policy? Would that money be better used elsewhere?

If the answer is unclear, pause before buying.

Comparing Quotes the Right Way

When comparing term life quotes, make sure the policies are truly comparable. The coverage amount, term length, health class, premium structure, riders, and insurer quality should be similar. A 20-year policy with no riders cannot be compared directly with a 30-year policy that includes several optional features.

Start with the base policy. Compare the premium for the same death benefit and term length across multiple insurers. Then evaluate optional features separately. This prevents riders from hiding the true cost of coverage.

It can help to request quotes with and without riders. Seeing the price difference makes the decision clearer. A rider that sounds inexpensive monthly may cost hundreds or thousands over the full term.

The comparison should also include the insurer’s financial strength and reputation. Life insurance is a long-term promise. The company should be strong enough to honor claims decades in the future.

Why Beneficiary Designations Matter

Choosing the right policy is only part of the process. The beneficiary designation determines who receives the death benefit. This must be handled carefully.

Beneficiaries may include a spouse, adult child, trust, business partner, or other person or entity. Naming minor children directly can create complications because minors usually cannot receive insurance proceeds outright. A trust or guardian arrangement may be more appropriate, depending on local law and the family’s estate plan.

Beneficiary designations should be reviewed after major life events such as marriage, divorce, childbirth, adoption, death of a beneficiary, business changes, or estate planning updates. An outdated beneficiary designation can create painful and expensive problems.

Life insurance should work with the broader estate plan. A policy that names the wrong person or fails to account for minor children may not accomplish its intended purpose.

How Much Can You Afford?

The right policy must be affordable enough to keep. A large death benefit is useless if the premiums become too expensive and the policy lapses.

Affordability should be judged in the context of the whole financial plan. The premium should leave room for emergency savings, debt repayment, retirement investing, housing, food, transportation, and other necessary expenses. Insurance should protect the household from catastrophe, not create monthly strain.

If the ideal coverage amount feels too expensive, consider adjusting the term length, comparing more insurers, improving health factors before applying if appropriate, or using multiple policies with different terms. Some households use a laddering strategy, buying several policies that expire at different times as financial needs decline.

For example, a parent may buy one 30-year policy for long-term protection and a smaller 20-year policy for the years when children are at home. As obligations decline, coverage declines too. This can sometimes reduce cost compared with one large policy lasting longer than necessary.

Laddering Term Life Policies

Laddering means using multiple term life policies with different expiration dates. This strategy recognizes that insurance needs often decline over time.

A young family may need substantial coverage while children are small, the mortgage is large, and savings are limited. Twenty years later, the children may be independent, the mortgage may be lower, and investments may have grown. The household may no longer need the same death benefit.

Instead of buying one large 30-year policy, the family might buy a combination of 10-year, 20-year, and 30-year policies. The total coverage is highest during the early years and gradually decreases as obligations fall.

Laddering can save money, but it adds complexity. The buyer must manage multiple policies and make sure coverage does not drop too soon. It works best for people who understand their timeline and are willing to maintain the structure.

Term Life for Stay-at-Home Parents

One of the most common insurance mistakes is ignoring the economic value of a stay-at-home parent. Because there is no paycheck, some families assume there is no need for life insurance. That assumption can be costly.

A stay-at-home parent may provide childcare, transportation, meal preparation, household administration, tutoring, elder care, emotional support, and scheduling. If that parent dies, the surviving parent may need to pay for services, reduce work hours, change jobs, or rely on family support.

Term life insurance for a stay-at-home parent does not replace salary. It replaces economic contribution. The coverage amount may be lower than for a high-earning spouse, but it should not be dismissed automatically.

A thoughtful estimate should include childcare costs, household help, time away from work, education support, and a transition cushion. The purpose is to give the surviving family options during a difficult period.

Term Life for Single Parents

Single parents often have a strong need for life insurance because children may depend heavily on one income and one caregiver. The policy must be designed carefully because the beneficiary structure matters.

A single parent should consider who would manage the money for the children, who would become guardian, how education and living expenses would be funded, and whether a trust is appropriate. Naming minor children directly may not provide the smooth protection intended.

The coverage amount may need to include income replacement, childcare, housing, education, healthcare, and support for the guardian. The goal is not only to leave money, but to leave a workable plan.

Term Life for Business Owners

Business owners may need term life insurance for both family and business reasons. A business may depend on the owner’s relationships, expertise, debt guarantees, or management. If the owner dies, the family may inherit not only assets but obligations.

Coverage may be needed to repay business debt, fund a buy-sell agreement, protect a partner, provide liquidity, or give the family time to sell or transition the business. Business-owned policies require careful planning because ownership, beneficiary designations, tax treatment, and legal agreements matter.

Business owners should not treat personal and business life insurance needs as the same. Each should be calculated separately. A personal family policy protects dependents. A business policy protects the company, partners, creditors, or succession plan.

What Happens When the Term Ends?

When the term ends, coverage usually expires unless the policy allows renewal or conversion. Ideally, the household no longer needs the same level of protection by that time. Children may be independent, debts may be lower, savings may be larger, and retirement may be closer.

But life does not always follow the original plan. Some people still need coverage at the end of the term because of late-in-life children, divorce, debt, health issues, dependent relatives, or insufficient savings. This is why term length and conversion options should be considered carefully at purchase.

As the end of the term approaches, review the household’s needs several years in advance. Do not wait until the policy is about to expire. If new coverage is needed, applying earlier may improve options.

When You May No Longer Need Life Insurance

Life insurance is not always a lifetime necessity. A person may no longer need coverage when no one depends on their income, debts are manageable, final expenses can be paid from savings, and assets are sufficient to support surviving family members.

This is the ideal outcome for many term life buyers. The policy protects the family during vulnerable years. Over time, the household builds wealth and reduces dependency. Eventually, the need for insurance declines because the family can self-insure.

Self-insurance means having enough assets to absorb the financial loss without transferring the risk to an insurer. It is not about being careless. It is about reaching a level of financial independence where the death benefit is no longer necessary for survival.

Term life insurance should be seen as a bridge. It protects the family while wealth is being built.

Red Flags When Buying Term Life Insurance

Be cautious if someone pressures you to buy immediately without explaining the policy. Life insurance is important, but pressure is not advice.

Be cautious if the recommendation focuses more on fear than numbers. A good policy should be justified by a clear financial need.

Be cautious if the base policy is hard to understand because of added features. Complexity often makes comparison harder.

Be cautious if permanent life insurance is presented as the only responsible choice when your need is temporary income protection.

Be cautious if the agent cannot clearly explain the cost of each rider, the term length, renewal rules, conversion option, exclusions, and total premium commitment.

Be cautious if the suggested coverage amount seems disconnected from your actual debts, income, dependents, savings, and goals.

A good insurance conversation should leave you clearer, not more confused.

A Practical Term Life Buying Checklist

Start by identifying who depends on your income, care, labor, or financial support.

Estimate the financial gap your death would create, including income replacement, debts, childcare, education, final expenses, and transition costs.

Subtract existing resources such as savings, investments, employer coverage, and survivor benefits.

Choose a term length that matches the years of financial vulnerability.

Compare quotes from multiple insurers for the same coverage amount and term.

Evaluate the insurer’s financial strength and reputation.

Review riders separately and ask whether each one solves a real problem.

Avoid relying on accidental death riders to make an inadequate base policy look sufficient.

Think carefully before paying extra for return of premium features.

Review beneficiary designations and update them after major life events.

Make sure the premium is affordable enough to maintain for the full term.

Revisit coverage every few years or after major changes in income, marriage, children, debt, homeownership, business ownership, or financial assets.

The Right Policy Is Usually the One That Does Its Job Cleanly

The best term life policy is often not the most complicated policy. It is the one that provides the right amount of protection for the right period at a fair price. It gives the family breathing room if the worst happens. It allows debts to be managed, children to be supported, housing to remain stable, and surviving loved ones to make decisions without immediate financial panic.

Unnecessary extras can distract from that mission. A policy does not become better simply because it has more features. A rider does not become valuable simply because it sounds comforting. Insurance should be judged by how well it solves a specific financial risk.

For most families considering term life, the central task is straightforward: identify the financial gap, cover it during the years it exists, and avoid paying for features that do not materially improve protection.

Life insurance is an act of responsibility, not an act of fear. It is a way of saying that the people who depend on you should not have to face financial collapse on top of emotional loss. But responsibility also means buying intelligently. Overpaying for unnecessary extras can weaken the same financial plan the policy is meant to protect.

The right term life policy should feel clear. You should know why you bought it, how much it pays, how long it lasts, who receives the benefit, what it costs, and what role it plays in your household’s larger financial life.

That clarity is the real protection. Not just a death benefit, but a policy chosen with purpose.