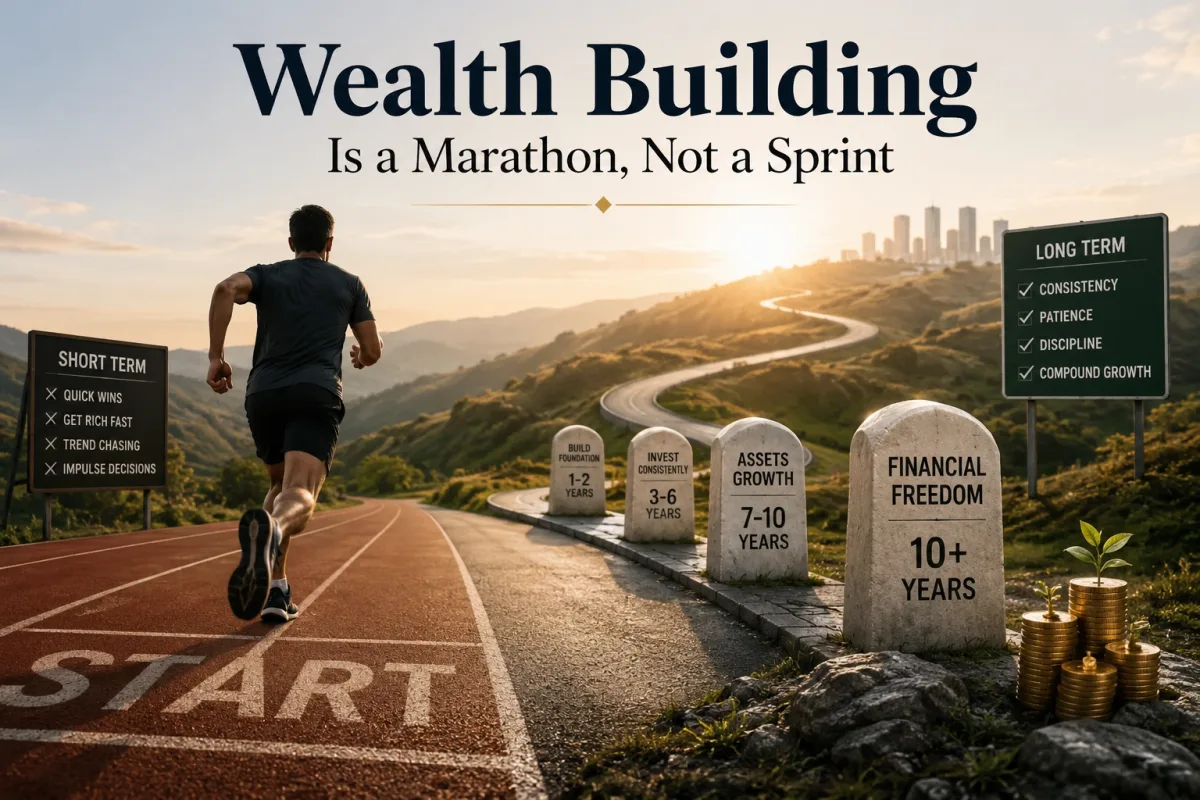

Wealth Building Is a Marathon, Not a Sprint

Every generation has its own version of the shortcut.

For one generation, it was the hot stock tip whispered across a dinner table. For another, it was speculative real estate bought with borrowed money. For another, it was day trading, cryptocurrency euphoria, online businesses promising overnight riches, or social media personalities presenting wealth as if it were a weekend project.

The packaging changes. The temptation does not.

People want wealth to arrive quickly because financial pressure feels urgent. Rent is due now. Children need school fees now. Medical bills arrive now. Groceries cost more now. The desire for fast relief is human. When money feels tight, patience can feel like a luxury reserved for people who already have enough of it.

Yet the central truth of wealth building is both simple and uncomfortable: lasting wealth usually grows slowly before it grows visibly.

It is built through repeated decisions that often look ordinary in the moment. Saving before spending. Investing before consuming. Avoiding unnecessary debt. Building skills. Protecting income. Buying assets. Reinvesting gains. Staying disciplined during market declines. Refusing to confuse appearance with progress. Doing this not for three months, but for years. Often for decades.

This is why wealth building is better understood as a marathon than a sprint. A sprint rewards explosive speed over a short distance. A marathon rewards endurance, pacing, preparation, consistency, and mental control. The fastest person at the start does not always finish strongest. The person who knows how to conserve energy, manage discomfort, and keep moving when excitement fades is often the one who reaches the finish line.

Money works in much the same way.

Many people begin their financial lives believing wealth is created by one dramatic event: a promotion, a business breakthrough, an inheritance, a winning investment, or a sudden opportunity. Those events can help, but they are rarely enough on their own. A high salary can disappear through poor spending. A business windfall can vanish through lifestyle inflation. An inheritance can be consumed in a few years. A lucky investment can create confidence that later turns into recklessness.

Wealth is not merely about receiving money. It is about converting money into lasting financial strength.

That conversion requires time.

The Difference Between Getting Money and Building Wealth

One of the most important distinctions in personal finance is the difference between income and wealth.

Income is money that flows in. Wealth is money that remains, grows, and produces future options. Income can create the raw material for wealth, but it is not wealth by itself. A person earning a large salary but spending nearly all of it may look successful while remaining financially fragile. A person earning a moderate income but consistently acquiring assets may appear less impressive yet become stronger with each passing year.

The confusion between income and wealth is one reason people underestimate the marathon nature of financial progress. Income feels immediate. Wealth is quieter. Income shows up in a paycheck. Wealth shows up in net worth, ownership, lower stress, greater resilience, and the ability to make choices without desperation.

A person can receive income every month and still remain dependent on the next paycheck. Wealth begins when part of today’s income is separated from consumption and directed toward tomorrow’s freedom.

That process is rarely glamorous.

It may look like increasing retirement contributions by a small percentage. Paying extra toward high-interest debt. Building an emergency fund. Buying shares of a diversified investment fund month after month. Keeping a reliable car instead of upgrading for status. Learning a valuable skill after work. Saying no to expenses that impress others but weaken the household balance sheet.

These decisions do not create instant transformation. They create direction. Over time, direction becomes distance.

Financial distance matters because wealth is cumulative. The small gap between what a person earns and what they consume becomes capital. Capital becomes assets. Assets produce returns. Returns, when reinvested, create more capital. That cycle becomes more powerful the longer it continues.

The early stages can feel painfully slow because the numbers are small. A person who saves $100 may not feel wealthier. A person who invests $500 may not feel transformed. But the purpose of early financial discipline is not to become rich immediately. It is to create the system through which wealth can grow later.

Why Fast Wealth Often Fails

Stories of rapid wealth attract attention because they seem to compress time. Someone buys an asset before it explodes in value. Someone starts a company that becomes highly profitable. Someone enters a new market early and exits with extraordinary gains. These stories are real, but they are incomplete.

They often leave out the failures, risks, timing, luck, debt, stress, and years of preparation behind the visible outcome. They also leave out what happens afterward.

Sudden wealth can be surprisingly fragile.

When money arrives faster than financial maturity, the money often leaves just as quickly. This is why lottery winners, entertainers, athletes, entrepreneurs, and inheritors can experience dramatic financial decline despite receiving sums that appear life-changing. The problem is not always the amount of money. The problem is the absence of a durable financial system.

Without a system, money becomes fuel for impulse.

Fast money can create fast spending. A person who receives a windfall may upgrade housing, vehicles, travel, clothing, entertainment, and social obligations all at once. The new lifestyle becomes expensive to maintain. Friends and relatives may ask for help. Investment opportunities may appear everywhere. Confidence rises. Caution falls.

The danger is not generosity or enjoyment. The danger is believing that a temporary increase in money justifies a permanent increase in obligations.

Wealth survives when it is protected by structure: budgets, investment plans, tax planning, insurance, estate documents, emergency reserves, and disciplined decision-making. These structures are not exciting, but they are what allow money to remain useful over time.

Fast wealth also fails when people mistake speculation for strategy.

A speculation can make money. It can even make a lot of money. But speculation depends heavily on timing, market mood, and the willingness of someone else to pay more later. Strategy is different. Strategy is based on repeatable principles: spend less than you earn, avoid destructive debt, own productive assets, diversify risk, increase earning power, protect against catastrophe, and let compounding work.

A sprint mindset says, “What can make me rich quickly?”

A marathon mindset asks, “What can make me financially stronger over many years?”

The first question invites urgency. The second invites wisdom.

The Power of Compounding Requires Time

Compounding is one of the most powerful forces in finance, but it is also one of the least emotionally satisfying in the beginning.

Compounding happens when returns generate their own returns. Money earns money, and then that new money also earns money. Over long periods, this can turn modest sums into meaningful wealth. But the effect is not linear. It does not grow in a straight line. It often looks slow for a long time, then increasingly powerful later.

This delayed acceleration is why patience is not optional.

Imagine two investors. One begins investing small amounts in their twenties and continues steadily. The other waits until their forties but invests larger amounts. The second investor may contribute more money overall, but the first investor has something that cannot be purchased later at any price: time.

Time gives compounding room to work. It gives dividends, interest, rental income, business profits, and capital gains the chance to be reinvested. It allows market downturns to be absorbed rather than feared. It turns consistency into leverage.

The challenge is that compounding is invisible at first. In the early years, most growth comes from contributions. The investor does the heavy lifting. Later, if the plan is maintained, the assets begin doing more of the lifting themselves.

This is similar to planting trees. A young tree provides little shade. For years, it may look unimpressive. But beneath the surface, roots are deepening. Structure is forming. Given enough time, the same tree that once seemed insignificant can become large enough to change the environment around it.

Financial compounding follows a similar rhythm. Early contributions build the root system. Later growth creates the shade.

People who quit too early often do so because they judge the process before the process has had enough time to reveal its power. They save for a year and feel disappointed. They invest for three years and become impatient. They compare their progress to someone else’s highlight reel and decide their own path is too slow.

But slow is not the same as ineffective.

In wealth building, slow progress that continues is often more powerful than dramatic progress that cannot be sustained.

Consistency Beats Intensity

Many people treat financial improvement like a burst of motivation. They become inspired, cut expenses aggressively, make large investment plans, track every dollar, and promise themselves a complete transformation. For a few weeks or months, everything changes. Then the intensity becomes exhausting. Old habits return.

This is not a character flaw. It is a design flaw.

Systems built on intensity often collapse because they require constant emotional energy. Systems built on consistency survive because they reduce the need for willpower.

A marathon runner does not sprint every mile. A strong investor does not need to make heroic financial decisions every week. The goal is not to live in a permanent state of restriction. The goal is to create habits that can be maintained through ordinary life.

Automatic saving is one example. When money is transferred to savings or investments before it reaches everyday spending accounts, discipline becomes easier. The decision is made once, then repeated by the system. Automatic debt payments, retirement contributions, sinking funds, and recurring investment purchases can all turn financial progress into a default rather than a monthly negotiation.

Consistency also protects people from emotional timing mistakes.

Markets rise and fall. Economic headlines shift. Interest rates change. Businesses go through cycles. When people invest only when they feel confident, they often buy after prices have already risen. When they stop investing during fear, they may miss attractive opportunities. A consistent plan helps remove the impossible burden of predicting the perfect moment.

The same principle applies beyond investing.

A person who exercises moderately for years will likely outperform someone who attempts extreme training for one month and quits. A person who reads, learns, and improves skills steadily will likely outperform someone who waits for one dramatic career move. A person who manages spending consistently will likely outperform someone who alternates between deprivation and indulgence.

Consistency is not glamorous, which is why it is underestimated. But wealth does not require every decision to be perfect. It requires enough good decisions, repeated long enough, to overpower the occasional mistake.

The Role of Habits in Long-Term Wealth

Financial outcomes are often the visible expression of invisible habits.

A household’s net worth is not created only by investment returns or income levels. It is shaped by patterns: how people spend when they are stressed, what they do when income rises, how they respond to social pressure, whether they compare prices, whether they maintain insurance, whether they plan for irregular expenses, whether they talk openly about money, whether they delay gratification, and whether they review their finances before problems become emergencies.

Small habits may seem insignificant because each one carries little immediate consequence. Buying lunch instead of preparing food at home will not destroy wealth. A subscription will not ruin a financial plan. One impulsive purchase may not matter. But habits repeat. Repetition turns small decisions into financial architecture.

The goal is not to eliminate all pleasure. A joyless financial plan is unlikely to last. The goal is to distinguish between spending that supports a meaningful life and spending that quietly steals future freedom.

Healthy wealth-building habits often include simple practices.

Reviewing spending regularly. Saving a fixed percentage of income. Increasing investments when income rises. Avoiding high-interest consumer debt. Comparing major purchases. Maintaining an emergency fund. Reading before investing. Keeping lifestyle inflation under control. Discussing financial goals with a spouse or partner. Teaching children the difference between owning assets and buying status.

These habits do more than improve numbers. They shape identity.

A person who repeatedly saves begins to see themselves as a saver. A person who invests regularly begins to see themselves as an owner. A person who pays debt down begins to see themselves as someone who honors future obligations. Identity matters because behavior that fits identity becomes easier to maintain.

Wealth building is not only mathematical. It is behavioral.

The numbers matter, but the numbers respond to choices. Choices respond to beliefs. Beliefs are reinforced by habits. Over time, the person becomes the kind of person who can handle wealth because they have been practicing the behaviors that wealth requires.

Why Asset Ownership Changes Everything

At the center of wealth building is a simple idea: owners build wealth differently from consumers.

Consumers exchange money for goods and services that are used up, worn out, or quickly replaced. Owners acquire things that can produce value over time. These may include shares of businesses, rental properties, bonds, farmland, intellectual property, private businesses, retirement accounts, or other productive assets.

Consumption is not wrong. Every life requires consumption. People need housing, food, transportation, clothing, education, medical care, rest, celebration, and beauty. The issue is not whether a person consumes. The issue is whether consumption absorbs all available income and leaves nothing to own.

Ownership creates a second engine.

A worker without assets depends almost entirely on labor income. If they stop working, income stops or declines sharply. A worker who gradually builds assets begins creating income streams that do not depend solely on daily labor. Dividends, interest, rents, business profits, and capital appreciation can supplement earned income and eventually reduce dependence on it.

This transition does not happen overnight. It is usually slow. At first, investment income may be tiny. A few dollars of dividends. A small amount of interest. A modest retirement account balance. But the size is not the only thing that matters. The direction matters. The person has begun crossing from pure consumption into ownership.

That crossing is one of the most important financial shifts a household can make.

Income pays the bills. Ownership changes the future.

For many families, the first major asset is not a stock portfolio but a home, a business, a pension, or a retirement account. The specific path varies by country, income level, opportunity, and personal circumstances. But the principle remains: wealth grows when money is converted into assets that can store or produce value.

A marathon mindset helps because asset ownership requires holding through uncertainty. Businesses face recessions. Real estate markets cool. Stock markets decline. Interest rates move. Tenants leave. Maintenance costs appear. Companies disappoint. Investors who expect a smooth sprint may panic at the first sign of discomfort. Owners who understand the marathon accept that volatility is part of the path.

They do not ignore risk. They manage it. They diversify. They maintain reserves. They study what they own. They avoid overborrowing. They think in years, not days.

The Quiet Enemy: Lifestyle Inflation

One of the most subtle threats to wealth is not poverty, market decline, or lack of opportunity. It is the tendency for expenses to rise whenever income rises.

Lifestyle inflation feels natural. A person works hard, earns more, and wants life to improve. There is nothing wrong with enjoying progress. The danger begins when every raise, bonus, commission, business gain, or side income is immediately converted into higher fixed costs.

A better apartment becomes a larger mortgage. A better car becomes a larger payment. Occasional travel becomes expected travel. Dining out becomes routine. Private school, clubs, subscriptions, upgraded phones, designer clothing, and social obligations all become part of the new normal.

The person earns more but does not become freer.

This is why some high earners remain financially anxious. Their income increased, but their obligations increased with it. They may have more impressive surroundings, but less flexibility. They may appear wealthier while being more dependent on uninterrupted income than ever before.

A marathon approach does not require refusing every upgrade. It requires capturing part of every income increase for wealth building before lifestyle expands.

For example, when income rises, a household might decide that half of the increase goes toward investments, debt reduction, or emergency reserves, while the other half improves lifestyle. This allows life to get better while financial strength also grows. The exact percentage can vary, but the principle is powerful: do not let lifestyle consume the entire reward of progress.

Lifestyle inflation is especially dangerous because it disguises itself as success. The visible signs of spending are easy to admire. The invisible signs of wealth are quieter: a growing portfolio, a paid-off loan, a stronger emergency fund, lower financial stress, freedom to change jobs, ability to help family without panic, and confidence during economic uncertainty.

Wealth is not always visible. In many cases, that is precisely why it lasts.

Debt Can Either Slow the Race or Support the Strategy

Debt is often described in simple moral terms, as if all borrowing is either good or bad. In reality, debt is a tool. Like any tool, it can build or destroy depending on how it is used.

Destructive debt usually finances consumption that does not produce lasting value. High-interest credit card balances, payday loans, unnecessary vehicle loans, and repeated borrowing for lifestyle expenses can trap households in a cycle where future income is already promised to past spending. This weakens the ability to save, invest, and respond to emergencies.

Productive debt, when used carefully, may support asset building. A mortgage on an affordable home, a business loan with disciplined cash flow, or education debt tied to realistic earning potential can sometimes improve long-term financial position. But even productive debt becomes dangerous when the borrower ignores risk, overestimates future income, or carries obligations too heavy for their financial foundation.

The marathon mindset treats debt with respect.

A runner carrying unnecessary weight becomes tired faster. A household carrying expensive debt has less room to move. Every interest payment is money unavailable for investment, protection, education, or opportunity. Debt can turn minor setbacks into crises because fixed payments continue even when income falls.

This does not mean everyone must be debt-free before building wealth. In many cases, households save, invest, and pay down debt at the same time. But high-interest debt deserves urgency because it often compounds against the borrower. While investments compound for the owner, expensive debt compounds for the lender.

One of the most powerful early wealth-building moves is to reduce financial drag.

Financial drag includes high-interest debt, unnecessary fees, unused subscriptions, tax inefficiencies, insurance gaps, poor spending habits, and preventable penalties. Removing drag does not feel as exciting as chasing a new investment idea, but it can improve financial speed with less risk.

The wealth marathon is not only about running faster. It is also about carrying less unnecessary weight.

Risk Management Keeps You in the Race

Many people think wealth building is mainly about offense: earning more, investing more, growing faster. Offense matters. But defense is what keeps a household from being forced to start over.

Risk management is the part of wealth building that people often appreciate only after something goes wrong.

An emergency fund may seem boring until a job is lost. Health insurance may seem expensive until a medical crisis occurs. Disability coverage may seem unnecessary until income is interrupted. Life insurance may feel abstract until dependents are left behind. Diversification may seem conservative until a concentrated investment collapses. Estate planning may feel premature until a family faces confusion during grief.

A marathon runner prepares for more than ideal conditions. Weather can change. Muscles can cramp. Shoes can fail. The course can become harder than expected. Financial life is the same. No plan survives exactly as imagined.

Risk management is not pessimism. It is respect for reality.

A household that protects against major risks can continue building wealth after setbacks. A household without protection may be forced to sell assets at the wrong time, borrow at high interest, abandon investments, or depend on relatives under stress.

The most basic layer is liquidity. Cash reserves may not produce impressive returns, but they provide options. They prevent ordinary emergencies from becoming debt problems. They allow investors to leave long-term assets untouched during short-term disruption.

The next layer is insurance. Insurance transfers certain catastrophic risks to a larger pool. Not every risk needs insurance, and not every policy is worth buying. But the risks that could financially devastate a household deserve careful attention. Health events, premature death, disability, property loss, liability claims, and business interruption can undo years of progress if ignored.

Another layer is diversification. Concentration can build wealth, especially for entrepreneurs and early investors, but it can also destroy wealth. Diversification accepts that the future is uncertain. It avoids placing the entire financial future on one company, one property, one industry, one currency, one employer, or one market cycle.

Long-term wealth is not only about maximizing returns. It is about surviving long enough for good returns to matter.

The Market Rewards Patience, Not Panic

Financial markets are powerful wealth-building tools because they allow ordinary people to own pieces of businesses, lend to governments or companies, and participate in economic growth. But markets also test temperament.

Prices move daily. Headlines amplify fear and excitement. A portfolio that looked strong one month can appear weak the next. Investors who enter markets expecting a smooth sprint often become discouraged by volatility. They may buy during optimism, sell during panic, and repeat the cycle at great cost.

The market does not reward emotional certainty. It rewards disciplined participation.

Patience matters because volatility is the price of admission for long-term growth assets. Stocks, real estate, and businesses can produce meaningful returns over time, but they do not do so in a straight line. Declines are not rare accidents. They are part of the structure.

A marathon investor prepares mentally for difficult stretches before they arrive. They decide in advance what they own, why they own it, how it fits their plan, and what would justify a change. They do not treat every market decline as a signal to abandon the race.

This does not mean holding every investment forever. Some investments deserve to be sold. Circumstances change. Valuations can become extreme. Businesses can deteriorate. Personal goals evolve. But there is a difference between thoughtful adjustment and emotional reaction.

One of the hardest lessons in investing is that activity can feel productive even when it is harmful. Checking prices constantly, changing strategies repeatedly, chasing recent winners, and reacting to forecasts may create the sensation of control. Yet many successful investment strategies depend less on constant action than on disciplined inaction.

Long-term investors often benefit from humility. They accept that they cannot reliably predict every recession, interest rate move, election outcome, technological disruption, or market rotation. Instead of building a plan that requires perfect prediction, they build one that can survive uncertainty.

That is the essence of the marathon approach.

Income Growth Still Matters

Patience should not be confused with passivity.

Wealth building may be a marathon, but that does not mean a person should move slowly in every area. Increasing income can dramatically improve the journey when the extra income is used wisely. A higher income creates more room to save, invest, pay down debt, build reserves, and support family goals.

The key is to understand income growth as fuel, not as the finish line.

People can increase income through career advancement, professional skills, entrepreneurship, side businesses, sales ability, technical training, negotiation, relocation, certifications, leadership, and reputation. In many cases, the highest-return investment a person can make is in their own earning power.

A young professional who learns valuable skills, communicates well, builds trust, and solves important problems may increase lifetime income far more than they could through small investment tweaks. A business owner who improves operations, customer retention, pricing, and cash flow may create wealth through enterprise value. A worker who develops rare expertise may gain bargaining power and resilience.

But income growth must be paired with capital discipline.

Without discipline, higher income simply funds a more expensive version of the same financial fragility. With discipline, higher income can shorten debt timelines, increase investment contributions, and accelerate ownership.

This balance is important. Some financial advice focuses so heavily on cutting expenses that it ignores the power of earning more. Other advice focuses so heavily on income that it ignores the danger of spending everything. Wealth requires both sides: a strong offense and a controlled defense.

The marathon runner trains to become stronger, but also learns to pace. The wealth builder works to earn more, but also learns to keep more and invest more.

Financial Seasons Require Different Strategies

A marathon is not experienced as one identical stretch of road. The beginning, middle, and final miles feel different. Wealth building also moves through seasons.

In the early stage, the focus is often stability. This may include building an emergency fund, reducing high-interest debt, learning basic money management, protecting income, and developing employable skills. The early stage can feel frustrating because progress is measured in small balances and avoided mistakes. But this stage creates the foundation.

In the accumulation stage, the focus shifts toward consistent investing and asset acquisition. Income may be higher. Debt may be more controlled. The household may contribute to retirement accounts, taxable investment accounts, real estate, business ventures, or education funds. The main challenge becomes consistency through life changes: marriage, children, relocation, career transitions, caregiving, and economic cycles.

In the expansion stage, assets begin playing a larger role. Investment returns may become more noticeable. Business equity may grow. Rental income, dividends, or portfolio gains may start to matter. The challenge becomes avoiding overconfidence. People who have accumulated some wealth may be tempted by unnecessary complexity, excessive leverage, concentrated bets, or status spending.

In the preservation stage, the focus often becomes protecting what has been built while still allowing growth. This may include estate planning, tax strategy, income planning, healthcare planning, charitable giving, and intergenerational education. The question shifts from “How do I build?” to “How do I sustain, use, and transfer wisely?”

These stages are not perfectly tied to age. A person can restart after divorce, migration, business failure, illness, or job loss. A family can move backward and forward. The point is not to compare one person’s season with another’s. The point is to use the right strategy for the current stage.

A beginning investor does not need the same complexity as a wealthy retiree. A household drowning in high-interest debt may need a different plan from a household choosing between tax strategies. A business owner with volatile income needs different reserves from an employee with stable benefits.

Marathon thinking allows for seasons. It does not demand that every mile look the same.

The Emotional Side of Slow Progress

One reason people abandon wealth-building plans is that slow progress can feel emotionally unrewarding.

Human beings are wired to notice immediate feedback. Spend money on a vacation, restaurant, outfit, or device, and the reward is instant. Transfer money into an investment account, and the reward may be invisible. Pay down debt, and life may feel the same the next morning. Build an emergency fund, and nothing exciting happens unless something goes wrong.

This creates an emotional disadvantage for good financial behavior.

Consumption provides immediate pleasure. Wealth building provides delayed power.

To stay committed, people need ways to make progress visible. Tracking net worth can help. So can reviewing debt balances, investment contributions, savings rates, emergency fund months, passive income, or retirement projections. These measures turn invisible progress into something observable.

Milestones also matter. The first $1,000 saved. The first debt eliminated. The first investment purchase. The first month of expenses covered by cash reserves. The first dividend payment. The first year without credit card interest. The first time investment gains exceed monthly contributions. These moments should be recognized because they mark identity shifts.

Another emotional challenge is comparison.

People rarely compare themselves to the full reality of someone else’s financial life. They compare themselves to visible consumption: homes, cars, trips, weddings, clothing, schools, restaurants, and social media images. But visible spending does not reveal debt, stress, family support, income instability, or lack of savings.

Comparison can make responsible financial choices feel like failure. A person building wealth quietly may feel behind someone spending visibly. But the marathon is not won by looking fastest at the starting line.

The better comparison is internal: Are you stronger than you were last year? Is your debt lower? Is your savings rate higher? Are your assets growing? Are your skills more valuable? Is your family more protected? Are you making decisions with less fear?

Those questions matter more than appearances.

Why Boring Financial Decisions Are Often the Best Ones

There is a reason many effective wealth-building strategies sound boring.

Live below your means. Invest regularly. Diversify. Avoid high-interest debt. Build an emergency fund. Increase income. Protect against major risks. Reinvest returns. Keep costs low. Think long term.

These principles are repeated so often that people may dismiss them as too simple. But simple does not mean easy. Simple does not mean weak. In finance, many of the most powerful ideas are simple enough to understand and difficult enough to practice for decades.

Boring decisions work because they reduce dependence on luck.

A person who saves consistently does not need one perfect opportunity to change their life. A person who diversifies does not need every investment to succeed. A person who avoids lifestyle inflation does not need income to rise forever. A person who maintains insurance does not need life to go exactly as planned. A person who invests over decades does not need to predict every short-term market move.

The boring path is not free of risk. Nothing in finance is. But it is built around resilience rather than excitement.

This is difficult in a culture that celebrates speed. Fast wealth gets attention. Slow wealth rarely does. A viral success story may reach millions. A family quietly investing for thirty years may never be noticed. Yet the unnoticed family may be far more financially secure.

Wealth that lasts often looks ordinary while it is being built.

The Hidden Wealth in Avoiding Mistakes

People often think wealth comes only from brilliant decisions. Sometimes it does. But for many households, a large part of wealth comes from avoiding major mistakes.

Avoiding high-interest debt. Avoiding scams. Avoiding panic selling. Avoiding uninsured catastrophe. Avoiding business partnerships without clear agreements. Avoiding investments one does not understand. Avoiding excessive leverage. Avoiding lifestyle commitments that require perfect income. Avoiding tax neglect. Avoiding the belief that one good year guarantees permanent prosperity.

These avoided mistakes do not appear as income. No one receives a statement showing the money they did not lose. But the effect can be enormous.

A single bad financial decision can erase years of progress. An unaffordable home can strain a household for decades. A failed speculative investment made with borrowed money can create long-lasting damage. A lack of disability insurance can turn a health problem into a financial crisis. A poorly planned business expansion can consume savings and credit. A panic sale during a market decline can lock in losses and delay recovery.

Marathon thinking is naturally cautious about irreversible damage.

This does not mean avoiding all risk. Wealth cannot grow without some risk. Careers, businesses, investments, and property all involve uncertainty. But successful wealth builders distinguish between risks they can survive and risks that can remove them from the race.

A survivable risk may be uncomfortable but manageable. An irreversible risk threatens the foundation. The wise investor, business owner, or household leader asks: If this goes wrong, can we recover? What is the downside? Are we being compensated for the risk? Do we understand it? Are we risking money we cannot afford to lose? Is this decision aligned with our long-term plan?

Those questions slow people down. That is their value.

Family Wealth Requires More Than Money

When wealth is viewed as a marathon, the race often extends beyond one person. It affects spouses, children, parents, siblings, communities, and future generations.

Family wealth is not only a balance sheet. It is also education, values, communication, habits, expectations, and stewardship.

Many families focus on leaving assets but neglect preparing heirs. This can create problems. Children who inherit money without financial maturity may feel entitled, overwhelmed, or unprepared. Relatives may disagree over property, business ownership, or caregiving responsibilities. Wealth can become a source of conflict if families avoid difficult conversations.

Building durable family wealth requires teaching the principles behind the money.

Children benefit from understanding budgeting, saving, giving, investing, work, ownership, debt, insurance, and delayed gratification. They need to see that money is not merely for consumption or status. It is a tool for responsibility, opportunity, protection, and service.

Spouses and partners benefit from shared clarity. A financial plan is stronger when both people understand the goals, accounts, debts, insurance coverage, estate documents, and decision-making process. Money secrecy can weaken trust. Money conversations, handled respectfully, can strengthen the household.

Older generations benefit from planning before crisis. Wills, beneficiaries, powers of attorney, healthcare directives, property titles, business succession plans, and insurance documents may not be pleasant topics, but they prevent confusion during vulnerable moments.

Family wealth is built through assets, but preserved through wisdom.

The Role of Purpose in Financial Endurance

People are more likely to stay disciplined when they understand what the discipline is for.

Wealth building without purpose can become either exhausting or empty. A person may save and invest aggressively but never feel satisfied. Another may lose motivation because the goal feels abstract. “Be rich” is not always strong enough to guide decades of decisions.

Purpose gives money direction.

For one person, wealth means freedom from constant financial anxiety. For another, it means giving children better opportunities. For another, it means caring for aging parents. For another, it means leaving employment that damages health. For another, it means supporting a community, building a business, funding education, traveling with family, or creating time for meaningful work.

Clear purpose makes sacrifice easier to understand. Skipping an unnecessary purchase is easier when the money is moving toward a home deposit, debt freedom, business capital, or retirement security. Investing through market volatility is easier when the portfolio represents future independence rather than numbers on a screen.

Purpose also helps prevent wealth from becoming a moving target.

Without purpose, people may keep raising the definition of enough. A higher income demands a larger house. A larger house demands more furniture. A larger portfolio demands a more luxurious lifestyle. The finish line keeps moving because it was never defined.

A marathon needs a destination. Financial life does too.

Practical Lessons for the Wealth Marathon

The marathon approach to wealth can be translated into practical principles.

Start before you feel ready

Many people delay because they believe they need more income, more knowledge, or better timing. Knowledge matters, but waiting for perfect conditions can become a lifelong excuse. Start with what is possible. Save a small amount. Pay down one debt. Open the account. Learn the basics. Build the habit. Increase as capacity grows.

Measure the right numbers

Income is only one measure. Track net worth, savings rate, debt levels, investment contributions, emergency reserves, insurance coverage, and asset income. These numbers reveal whether financial strength is improving.

Make good behavior automatic

Automation reduces emotional friction. Automatic transfers, investment contributions, bill payments, and debt repayments help turn intention into action. The best financial plan is not the one that requires constant motivation. It is the one that continues through ordinary months.

Protect your foundation

Before chasing high returns, protect against events that can force you backward. Maintain liquidity, appropriate insurance, clear records, and manageable debt. A strong foundation allows you to take intelligent risks without endangering survival.

Use income increases wisely

When income rises, decide in advance how much will go toward wealth building. Without a plan, lifestyle inflation will often absorb the increase. Let life improve, but make sure freedom improves too.

Invest like an owner

Do not treat investments as lottery tickets. Understand what you own and why you own it. Favor assets and strategies that align with your goals, risk tolerance, time horizon, and need for liquidity. Ownership requires patience and responsibility.

Avoid irreversible mistakes

Before major financial decisions, examine the downside. Can you recover if things go wrong? Are you relying on perfect conditions? Are you borrowing too much? Do you understand the risk? Protecting against disaster is part of building wealth.

Review without obsessing

Financial plans need attention, but not constant anxiety. Set a rhythm for review: monthly spending, quarterly net worth, annual insurance and investment checks, periodic estate planning updates. Review enough to stay informed, not so much that every fluctuation controls your emotions.

Keep learning

Financial education compounds too. The more you understand taxes, investing, business, insurance, credit, real estate, negotiation, and behavioral finance, the better your decisions become. Learning reduces dependence on hype.

Define enough

Without a sense of enough, wealth building can become endless accumulation without peace. Enough does not mean complacency. It means understanding what kind of life your money is meant to support.

The Long Road Is the Advantage

At first, the idea that wealth takes time can feel discouraging. People want the shortcut. They want the sprint. They want proof that their financial life can change quickly.

But the long road is not only a burden. It is also an advantage.

A long time horizon allows ordinary people to participate in extraordinary outcomes. It allows modest contributions to compound. It allows mistakes to be corrected. It allows skills to improve. It allows income to grow. It allows assets to recover from downturns. It allows financial wisdom to deepen. It allows families to change direction before crisis becomes permanent.

The marathon rewards people who may not begin with privilege, high income, or perfect knowledge. It rewards those who keep learning, keep saving, keep investing, keep protecting, and keep moving.

This does not mean the journey is fair or easy. Economic systems are unequal. Wages, healthcare costs, housing prices, education access, family obligations, and national conditions affect the path. Some people run with advantages; others run with heavy burdens. Serious financial education should never pretend that everyone starts from the same line.

But within the reality of unequal starting points, principles still matter. A household that builds habits, controls debt, increases skills, owns assets, protects against risk, and thinks long term is usually stronger than it would be without those behaviors. The marathon mindset does not erase hardship, but it creates a framework for progress.

Progress may be slow. Slow progress is still progress.

What Wealth Really Buys

At its best, wealth is not about showing superiority. It is about increasing freedom, resilience, and choice.

Wealth can buy time with family. It can buy the ability to leave harmful employment. It can buy medical options. It can buy education. It can buy the freedom to be generous without self-destruction. It can buy the ability to take career risks, start businesses, support aging parents, weather recessions, and retire with dignity.

These are not sprint rewards. They are endurance rewards.

The person who builds wealth slowly may not attract attention. They may not appear impressive in the early years. They may drive a modest car, live below their means, and ignore trends that excite others. But behind the scenes, they are buying something more valuable than applause. They are buying control over their future.

That control grows one decision at a time.

One month of saving. One debt payment. One investment contribution. One avoided impulse. One skill learned. One policy reviewed. One raise invested. One emergency handled without borrowing. One market downturn endured. One year after another.

This is how financial strength is built.

Not all at once. Not without mistakes. Not without setbacks. But steadily.

The Finish Line Is Not a Number

Many people imagine financial success as a single number. A certain portfolio value. A certain salary. A certain property portfolio. A certain business valuation. Numbers matter because they help define goals and measure readiness. But the real finish line is broader than a number.

The deeper goal is financial independence of mind and life.

It is the ability to make decisions from strength rather than fear. It is knowing that a temporary setback will not destroy the household. It is having assets that support future needs. It is being able to say no to bad opportunities and yes to meaningful ones. It is having enough clarity to use money rather than be controlled by it.

For some, that may require great wealth. For others, it may require a modest but well-structured financial life. The number depends on location, family size, health, values, obligations, and desired lifestyle. The principle does not change: wealth should serve life, not replace it.

A marathon runner does not succeed by copying another runner’s body, pace, or strategy. They succeed by understanding the course, training consistently, managing their energy, and finishing their own race.

Financial life works the same way.

Your income, background, responsibilities, opportunities, and goals may differ from someone else’s. Your race is your own. But the principles of endurance remain remarkably stable. Spend less than you earn. Build reserves. Avoid destructive debt. Increase earning power. Own productive assets. Manage risk. Stay invested in your future. Keep learning. Let time work.

Wealth building is a marathon, not a sprint, because the purpose is not merely to become rich quickly. The purpose is to become financially strong permanently.

That kind of strength is not rushed.

It is trained. It is practiced. It is protected. It is compounded.

And over time, it can change everything.