Beyond the Paycheck: Building Multiple Streams of Income for Long-Term Wealth

A single paycheck can feel secure until it disappears.

For many households, financial life rests on one source of income: a salary, a wage, a business, a client base, or a professional practice. When that income is steady, the arrangement can feel safe. Bills are paid. Plans are made. The future appears manageable. But when the income is interrupted by job loss, illness, industry disruption, recession, automation, business failure, or a major client leaving, the weakness of depending on one stream becomes visible very quickly.

This is the central argument for building multiple income streams. It is not about chasing every side hustle, buying every investment, or turning life into an endless work project. It is about reducing dependence. It is about creating more than one way for money to enter the household. It is about turning skills into opportunity, income into assets, and assets into future income.

Multiple income streams can create stability, but only when built thoughtfully. More income sources are not automatically better. A second income stream can reduce stress, or it can create exhaustion. A rental property can build wealth, or it can become a cash-draining burden. A business can produce freedom, or it can become another demanding job. A dividend portfolio can provide income, but it can also decline in value. A digital product can sell repeatedly, but it may require marketing, maintenance, and customer support.

The idea is powerful, but it must be handled with maturity. The goal is not to collect income streams like trophies. The goal is to build a financial system that is more resilient than one paycheck alone.

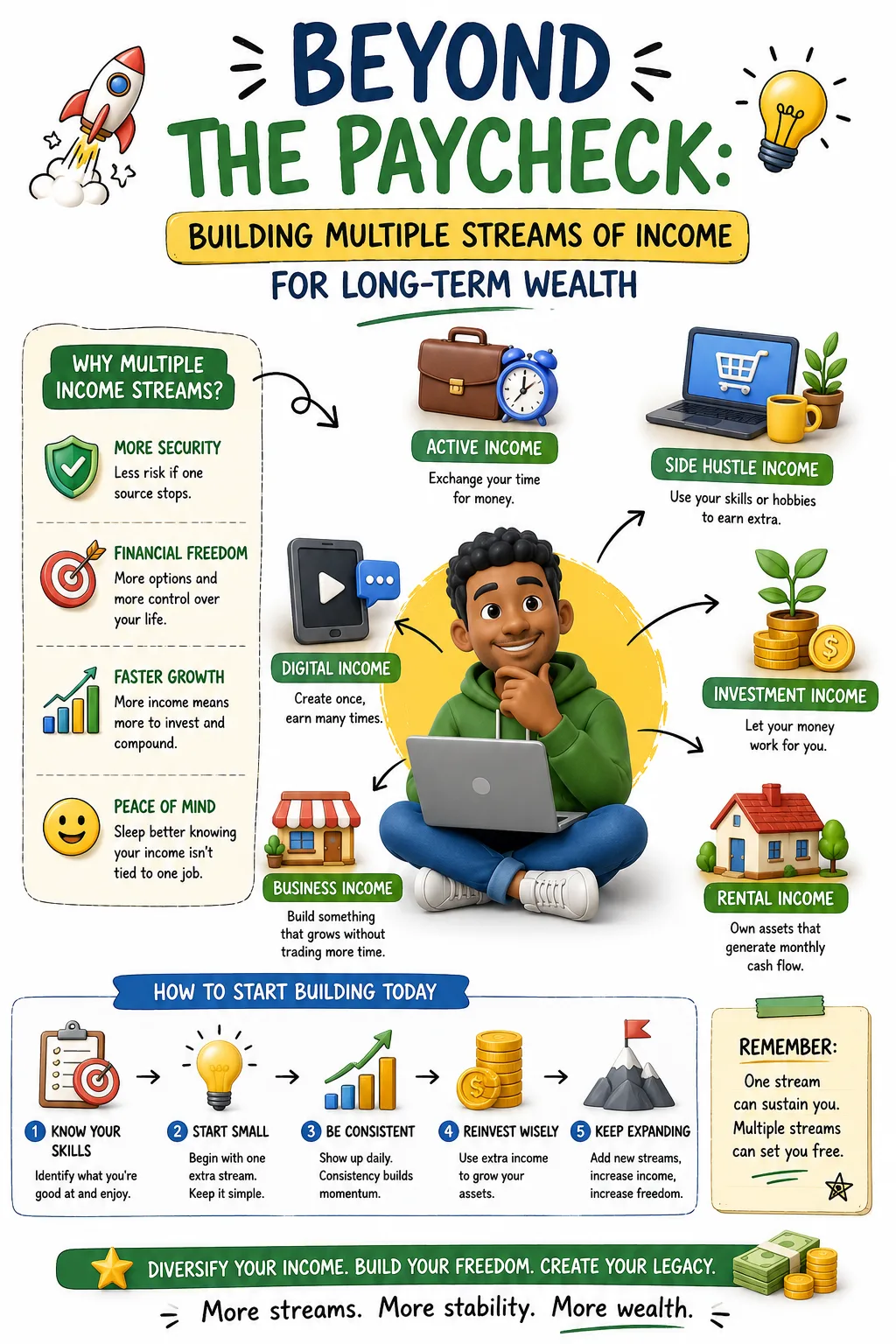

Income diversification is one of the most practical wealth-building concepts because it sits between earning and investing. It begins with human capital: the skills, knowledge, reputation, and relationships that help a person earn. It then moves toward financial capital: the assets that can generate income or appreciate over time. Over years, the strongest households often shift from depending mostly on labor income to receiving a growing share of income from investments, ownership, business systems, royalties, rents, interest, dividends, or other productive assets.

This transition is rarely instant. It is usually built in layers. First, stabilize the main income. Then increase skills. Then create surplus. Then direct surplus into assets. Then reinvest. Then expand carefully. The process is not glamorous, but it can change the balance of power in a financial life.

Why One Income Is Risky

One income source creates concentration risk. Investors understand this concept when they talk about not putting all their money into one stock. The same idea applies to income. If all household income depends on one employer, one customer, one contract, one business, one platform, or one industry, the household is exposed to forces it may not control.

An employee can lose a job even after performing well. A company can restructure. A business can be sold. A manager can change. A recession can reduce hiring. Technology can alter an industry. A professional license can become harder to maintain. A major client can leave. A social media platform can change its algorithm. A landlord can lose tenants. A freelancer can face delayed payments. A small-business owner can be affected by supply costs, regulation, competition, or consumer demand.

Many people do not notice income concentration risk because the paycheck arrives predictably. Predictability can create the illusion of permanence. But a paycheck is not a guarantee. It is a current arrangement between a worker and an income source. That arrangement can change.

Multiple income streams create a margin of resilience. If one income source weakens, another may help cover expenses. If a job is lost, investment income may continue. If a freelance client leaves, a salary may remain. If rental income pauses because of vacancy, a portfolio may still produce dividends or interest. If a business slows, consulting income may help. The goal is not to eliminate risk. The goal is to avoid being financially helpless when one source fails.

This does not mean every person must have five income streams immediately. Many people build wealth successfully with one strong primary income, especially when they maintain emergency savings, avoid high-interest debt, invest consistently, and insure major risks. A high-quality career can be a powerful wealth engine. But even then, the long-term goal should be to use that income to acquire assets that eventually produce additional financial support.

The first income stream pays for life. The next streams build options.

The Difference Between Income and Wealth

Income is money received over a period. Wealth is accumulated ownership. A person can have high income and low wealth if they spend everything. Another person can have modest income and meaningful wealth if they consistently save and invest.

This distinction matters because building multiple income streams is not only about earning more. Earning more can help, but extra income that is immediately consumed does not create independence. It may create a better lifestyle, but not necessarily a stronger balance sheet.

The purpose of additional income is to widen the gap between income and expenses. That gap can then be used to pay down bad debt, build reserves, invest, buy productive assets, fund education, start a business, or prepare for retirement. Without that conversion, additional income becomes additional spending.

Many households experience this trap. A person starts freelancing and earns extra money, but the extra income disappears into dining out, gadgets, travel, car upgrades, or convenience spending. A professional receives a raise and immediately increases fixed expenses. A business owner has a good year and upgrades lifestyle before strengthening cash reserves. The income increased, but wealth did not.

Multiple income streams should not be built only to support more consumption. They should be built to increase freedom.

Start With Your Skills

The most accessible income-producing asset most people have is not a stock portfolio or a rental property. It is human capital. Human capital includes skills, education, experience, judgment, reputation, credentials, communication ability, technical knowledge, creativity, professional networks, and the ability to solve valuable problems.

Before a person asks, “What side hustle should I start?” a better question is, “What can I already do that someone would pay for?” Skills are often the bridge from one income stream to several. A teacher can tutor, create curriculum, consult for education companies, or build learning materials. An accountant can offer tax support, bookkeeping, financial systems, or small-business advisory services. A designer can freelance, sell templates, consult on branding, or create digital products. A mechanic can repair vehicles after hours, teach maintenance classes, or build a specialized service business. A nurse can provide training, health education, consulting, or specialized care services within legal and professional boundaries.

Skill-based income is powerful because it often requires less upfront capital than asset-based income. A rental property may require a down payment. A stock portfolio requires investable savings. A business may require equipment, inventory, software, or staff. A skill-based service may begin with knowledge, a network, and disciplined execution.

That does not mean skill-based income is easy. It requires time, professionalism, marketing, pricing, delivery, and reliability. Many people underestimate the business side of selling their expertise. Being good at a skill is not the same as acquiring clients, managing invoices, handling taxes, setting boundaries, or creating repeatable systems.

Still, for many households, skills are the best starting point because they can increase income without large financial risk. A person who earns more through skills can then invest the surplus into productive assets. Human capital becomes financial capital.

The Career Itself Can Be the First Expansion

Building multiple income streams does not always mean starting a side business. Sometimes the smartest first move is to strengthen the main income stream. A stronger primary income can create more surplus than a distracting side project.

A worker earning below their potential may benefit more from negotiation, certification, relocation, specialization, or changing employers than from spending nights on a low-margin side hustle. A professional who becomes excellent in a high-demand field may create a larger wealth-building gap than someone who divides attention across too many small ventures. A business owner may improve income more by raising prices, improving margins, retaining customers, or streamlining operations than by launching unrelated projects.

The main income stream should not be neglected. It is often the foundation that funds everything else. If a side income damages performance at work, weakens health, or prevents skill development, it may be counterproductive.

The best income expansion often follows a sequence. First, become valuable in your primary field. Second, capture more value through better pay, better clients, or better business economics. Third, use surplus to invest. Fourth, create additional income streams that complement rather than sabotage the foundation.

Skill-Based Income Streams

Skill-based income streams can take many forms. Freelancing allows a person to sell specific services, such as writing, design, editing, coding, bookkeeping, photography, consulting, translation, tutoring, coaching, or marketing. Consulting allows experienced professionals to advise businesses or individuals. Teaching allows experts to package knowledge into workshops, courses, training sessions, or private instruction. Contract work allows professionals to serve clients without full-time employment. Licensing expertise can lead to templates, manuals, tools, or paid frameworks.

The advantage of skill-based income is flexibility. It can often begin small. A person can test demand before investing heavily. The risk is usually time, not large capital. The income can be directed into savings, debt repayment, or investments.

The limitation is scalability. If income depends entirely on personal labor, it may become another job. A freelance designer who earns only when designing has created an additional active income stream, not passive income. That can still be valuable. But to scale, the designer may need to raise prices, specialize, hire support, create products, build recurring retainers, or turn expertise into assets.

Skill-based income is often the first step toward business ownership. The person begins by selling time. Then they improve pricing. Then they create systems. Then they package knowledge. Then they hire or automate. Eventually, the income stream may become less dependent on each hour worked. This is how active income can evolve toward ownership income.

Turn Income Into Assets

Additional income becomes powerful when it is converted into assets. An asset is something that can produce income, appreciate in value, or strengthen future financial security. Productive assets may include diversified stock portfolios, bonds, mutual funds, exchange-traded funds, retirement accounts, rental properties, private businesses, intellectual property, royalties, or ownership stakes.

This is the turning point in wealth building. A person can work more hours forever and still remain financially vulnerable if every dollar is consumed. Assets create the possibility that money can work alongside labor.

Turning income into assets begins with surplus. If a household earns $1,000 in extra monthly income and invests $700 of it consistently, the extra income becomes a wealth engine. If the same household spends all $1,000, the side income improves lifestyle but does not improve long-term security. The difference is not the income itself. It is the allocation.

Assets can produce wealth in different ways. Stocks may appreciate and sometimes pay dividends. Bonds may pay interest. Rental property may generate rent and build equity. Businesses may produce profit and sale value. Intellectual property may generate royalties. Cash reserves may not produce high returns, but they protect against emergencies and forced selling.

The strongest financial plans often combine several asset types. Cash provides liquidity. Investments provide growth. Bonds may provide stability and income. Real estate may provide rent and inflation exposure. Businesses may provide upside and control. Insurance and estate planning help protect what has been built.

Asset ownership does not require complexity at the beginning. A diversified investment account funded consistently can be more effective than a complicated strategy poorly understood. The priority is not to appear sophisticated. The priority is to own productive assets in a way that fits goals, risk tolerance, time horizon, and financial capacity.

The Truth About Passive Income

Passive income is one of the most attractive phrases in personal finance. It suggests money arriving without effort. Build once, earn repeatedly. Sleep while money comes in. Escape the paycheck. Live from assets.

There is truth inside the idea, but the phrase is often exaggerated. Truly passive income is rare. Most income streams require either upfront labor, upfront capital, ongoing management, risk exposure, or all of these. Dividends require investment capital. Rental income requires property acquisition, financing, maintenance, tenants, insurance, taxes, and management. Royalties require creation and distribution. Digital products require marketing, updates, customer service, and platform dependence. A business may produce income without daily owner involvement only after systems, people, processes, and demand are in place.

A more accurate phrase is leveraged income or ownership income. The income may not require direct hourly work forever, but it usually requires something: capital, risk, skill, maintenance, oversight, or judgment.

This matters because unrealistic passive income expectations cause bad decisions. People buy courses promising effortless income. They purchase properties without understanding expenses. They invest in high-yield products without examining risk. They start online businesses expecting sales without distribution. They underestimate taxes, legal requirements, platform changes, customer acquisition costs, and competition.

Passive income is not magic. It is the result of building or buying an asset that can produce cash flow with less ongoing effort than a traditional job. The effort does not disappear. It changes form.

Common Types of Additional Income Streams

Employment Income

Employment income is the foundation for many households. It may include salary, wages, bonuses, commissions, overtime, benefits, retirement contributions, and equity compensation. Although it is often considered a single income stream, it can be strengthened through career strategy.

Increasing employment income may involve learning high-value skills, negotiating compensation, moving to a better employer, entering a stronger industry, pursuing leadership roles, or obtaining credentials. For many people, improving employment income is the highest-return move because it can create recurring surplus without the complexity of starting a new venture.

Freelance and Consulting Income

Freelancing and consulting allow people to monetize skills outside a traditional job. These streams can begin with existing expertise and grow through referrals, reputation, specialization, and better pricing.

The challenge is that freelance income can be inconsistent. Clients may delay payment. Projects may come in waves. Taxes may need to be handled separately. There may be no paid leave, benefits, or employer retirement contributions. A freelancer should build reserves, track expenses, set aside tax money, and avoid depending on best-case months.

Business Ownership

Business ownership can create powerful income and wealth, but it carries real risk. A business can produce profit, build equity value, create tax planning opportunities, employ others, and eventually be sold or passed down. But businesses can also fail, consume capital, create stress, and depend heavily on the owner.

A business becomes a stronger asset when it has repeatable systems, reliable customers, clean financial records, healthy margins, capable employees, and reduced dependence on the founder. Otherwise, it may be self-employment rather than a transferable asset. Self-employment can still be valuable, but it should not be confused with a business that can operate and hold value without the owner’s constant labor.

Investment Income

Investment income may include dividends, interest, distributions, and capital gains. Diversified portfolios can help households participate in economic growth without owning and managing individual businesses directly. Retirement accounts and tax-advantaged structures may improve long-term results depending on jurisdiction.

Investment income requires capital. It usually grows slowly at first because the portfolio is small. This can discourage beginners. But consistent contributions and reinvestment can become meaningful over time. The investor should focus on asset allocation, diversification, fees, taxes, risk tolerance, and time horizon rather than chasing the highest advertised yield.

Rental Income

Rental property is one of the most familiar income streams. It can provide rent, potential appreciation, tax benefits in some jurisdictions, and the use of leverage. It can also involve vacancies, repairs, difficult tenants, property taxes, insurance, legal compliance, financing risk, and market downturns.

The key to rental income is realistic math. Expected rent must be compared with mortgage payments, taxes, insurance, maintenance, management, vacancies, capital expenditures, and reserves. A property that looks profitable before expenses may be weak after expenses. Real estate can build wealth, but it is not automatically passive and not automatically safe.

Royalties and Intellectual Property

Royalties can come from books, music, patents, software, photography, design assets, licensing agreements, online courses, or other intellectual property. The appeal is that one creation can potentially generate repeated income.

The difficulty is distribution. Creating something valuable is only part of the work. People must discover it, trust it, buy it, and continue finding it. Intellectual property income often requires marketing, platform management, legal protection, updates, and audience building. Some creators earn meaningful royalties. Many earn little. The stream can be excellent when paired with strong expertise and distribution.

Digital Products

Digital products include courses, templates, ebooks, software tools, paid communities, newsletters, design files, spreadsheets, and educational resources. They can be attractive because inventory costs may be low and products can be sold repeatedly.

But digital products are competitive. Success usually requires a clear audience, a real problem, credible expertise, strong positioning, good delivery, marketing, customer support, and ongoing improvement. A digital product is not passive simply because it is digital. It is an asset only if it solves a problem people are willing to pay for.

The Order Matters

Many people try to build multiple income streams in the wrong order. They chase complexity before stability. They invest before building reserves. They start businesses before understanding cash flow. They buy properties while carrying expensive consumer debt. They create products before developing expertise. They attempt five ventures at once and execute none well.

A stronger order begins with financial defense. Build an emergency fund. Reduce high-interest debt. Protect against major risks with appropriate insurance. Know monthly expenses. Stabilize the main income. Then expand.

Once the foundation is in place, look for the highest-value opportunity. For some, that is a better job. For others, it is freelancing. For others, it is investing more consistently. For others, it is buying or building a business. For others, it is rental property. The right order depends on time, skill, capital, risk tolerance, family responsibilities, and goals.

There is no universal path. But there is a universal warning: too much complexity too early can weaken the plan.

Expansion Has Costs

Every income stream has hidden costs. It may require time, attention, money, taxes, legal structure, insurance, accounting, software, maintenance, customer service, marketing, or emotional energy. A household should count these costs before celebrating gross income.

A side business that earns $2,000 a month but consumes every evening, increases taxes, damages health, and prevents career advancement may not be as profitable as it appears. A rental property that produces rent but requires constant repairs may produce weak net returns. A digital product that sells occasionally but requires constant advertising may not justify the effort. A consulting practice with high revenue but unpredictable clients may require a large cash reserve.

Net income matters more than gross income. After-tax income matters. Time-adjusted income matters. Risk-adjusted income matters. Quality of life matters.

The goal is not to be busy. The goal is to be freer.

How to Evaluate a New Income Stream

Before starting a new income stream, ask several questions. What problem does this income stream solve? Who pays for it? Why would they choose you or this asset? How much upfront capital is required? How much time is required? What skills are needed? What are the ongoing costs? What taxes apply? What legal or regulatory requirements exist? What could go wrong? How quickly can the stream be stopped if it fails? Does it complement or conflict with your main income?

A good income stream fits the owner’s resources. A busy parent with limited time may prefer automated investing or a small, high-value consulting offer over a labor-intensive side business. A skilled professional with strong savings may prefer investment assets. A person with construction knowledge may understand rental property better than someone who has never managed repairs. A writer with an audience may succeed with digital products. A person with no audience may struggle.

Fit matters. The best income stream for one person may be a poor choice for another.

From Active Income to Scalable Income

Many people begin with active income because it is easiest to understand. Work an hour, get paid. Complete a project, receive money. Serve a client, earn a fee. Active income can be valuable, especially when it pays well.

The next stage is scalable income. Scalable income is not tied perfectly to each hour worked. A consultant may create a group program instead of only one-on-one work. A freelancer may sell templates. A teacher may build a course. A business owner may hire employees. An investor may buy assets. A creator may license intellectual property. A professional may negotiate equity compensation.

Scalable income requires systems. It may require branding, automation, delegation, documentation, product design, capital investment, or distribution. It is harder to build than active income, but it can become more powerful because it separates income from direct time.

The final stage is ownership income. This is income from assets that continue producing with less daily involvement. It may come from investment portfolios, mature businesses, royalties, rental properties with management, or equity stakes. Ownership income is what many people mean when they say passive income, though it still requires oversight.

A sensible path moves gradually from active income to scalable income to ownership income. Skipping steps can be expensive.

Use Extra Income to Buy Back Freedom

The highest use of extra income is not always more consumption. Often, it is buying back freedom. Freedom can mean paying off high-interest debt. It can mean building a six-month emergency fund. It can mean investing enough to retire earlier. It can mean leaving a toxic job. It can mean caring for family. It can mean starting a business with less desperation. It can mean choosing work based on purpose rather than panic.

Every dollar of extra income should be given a role. Some may be spent and enjoyed. That is healthy. But a meaningful share should strengthen the future. Without intentional allocation, lifestyle inflation will quietly absorb the benefit.

A practical approach is to decide in advance how extra income will be divided. For example, a household might direct a portion to taxes, a portion to emergency reserves, a portion to debt repayment, a portion to investments, and a portion to enjoyment. The exact percentages should fit the situation. The important point is that extra income should not arrive without a plan.

The Role of Taxes

Additional income often creates tax complexity. Freelancers, landlords, investors, business owners, and creators may need to track income, expenses, deductions, estimated payments, sales taxes, payroll taxes, capital gains, depreciation, or local reporting requirements. Rules vary widely by jurisdiction.

Ignoring taxes can make an income stream look more profitable than it is. A side business may generate cash, but part of that cash may belong to the tax authority. Rental income may be offset by expenses, but documentation matters. Investment income may be taxed differently depending on account type and holding period. Digital products may create sales tax or value-added tax obligations in some locations.

Good recordkeeping is part of income diversification. Separate business and personal finances where appropriate. Track expenses. Save for taxes. Understand filing obligations. Seek professional advice when complexity increases. Wealth is not only about earning money. It is about keeping money legally and efficiently.

Risk Management for Multiple Income Streams

Multiple income streams can reduce one kind of risk while creating others. A side business may create liability risk. A rental property may create property and tenant risk. A portfolio may create market risk. A digital business may create platform risk. A consulting practice may create contract risk. A business partnership may create relationship risk.

Risk management should grow with income complexity. This may include insurance, legal agreements, emergency reserves, business entities, accounting systems, cybersecurity, diversified investments, written contracts, professional advice, and estate planning.

Protection matters because building income is only half the game. Keeping it is the other half. A lawsuit, uninsured loss, tax problem, fraud event, or poorly structured partnership can erase years of progress.

Do Not Let Side Income Destroy Your Main Asset

For many people, the main asset is still earning power. A side project should not damage it casually. If a side business causes poor performance at work, harms health, strains family relationships, or prevents sleep, the true cost may be higher than the income.

There are seasons when intense effort is worthwhile. Building a business may require sacrifice. Paying off debt may require temporary extra work. Launching a product may require evenings and weekends. But a permanent state of exhaustion is not freedom.

Income diversification should be designed around sustainability. The goal is not to work every waking hour. The goal is to create income sources that eventually reduce fragility.

The Psychology of Multiple Income Streams

Multiple income streams can change how a person feels about money. A household with only one income source may feel trapped by an employer or client. A household with savings, investments, and side income may negotiate with more confidence. A business owner with diverse customers may sleep better than one dependent on a single buyer. An investor with dividends, interest, and emergency reserves may feel less panic during job uncertainty.

This psychological benefit is important. Financial stress narrows decision-making. People under pressure often accept bad terms, stay in unhealthy situations, borrow expensively, or sell assets at poor times. Additional income streams can create breathing room. Breathing room improves judgment.

But multiple income streams can also create anxiety if poorly managed. Too many projects, accounts, obligations, clients, properties, and deadlines can overwhelm. Simplicity has value. The right number of income streams is not the largest number possible. It is the number that improves resilience without creating chaos.

A Practical Framework for Building Multiple Income Streams

Begin with the base. Know your monthly expenses. Build an emergency fund. Reduce high-interest debt. Protect against major risks. Strengthen your primary income. This creates the stability needed to expand.

Next, identify your highest-value skills. What do people already ask you for help with? What problems can you solve? What credentials, experience, or knowledge do you have? What could be packaged into freelance work, consulting, teaching, or a small service offer?

Then choose one additional income stream to test. Start small. Measure demand. Track time and expenses. Learn whether the work is profitable, sustainable, and aligned with your life. Avoid launching several streams at once unless you already have strong systems.

Use the income intentionally. Set aside taxes. Build reserves. Pay down bad debt. Invest in diversified assets. Reinvest in the income stream only if the returns justify it. Avoid letting every extra dollar become lifestyle spending.

As assets grow, shift attention from active side income to ownership income. This may include investment portfolios, retirement accounts, business equity, real estate, royalties, or other productive assets. The long-term goal is not to keep adding labor. It is to increase the share of income generated by assets.

Review the system regularly. Drop income streams that are low-profit, high-stress, or strategically irrelevant. Expand those that are profitable, resilient, and aligned with your goals. A strong income system is curated, not cluttered.

What to Avoid

Avoid chasing every income trend. Avoid buying investments you do not understand. Avoid calling something passive when it requires constant attention. Avoid borrowing heavily to create an income stream without stress testing the downside. Avoid ignoring taxes. Avoid sacrificing health for small amounts of extra money. Avoid letting side income become side spending. Avoid overextending into too many projects.

Avoid comparing your income streams to someone else’s highlight reel. Some people exaggerate revenue and hide expenses. Some promote business models because they sell courses about them. Some display lifestyle funded by debt, not profit. Your financial plan should be based on your numbers, your risk tolerance, your skills, and your goals.

What to Do

Start with stability. Build cash reserves. Control bad debt. Protect your household. Increase your primary earning power. Use skills to create additional income where practical. Convert surplus income into productive assets. Reinvest patiently. Expand one stream at a time. Track net income, not just revenue. Keep records. Plan for taxes. Protect assets. Review regularly.

Most importantly, connect every income stream to a larger purpose. Are you building retirement security? Paying off debt? Funding education? Buying freedom from a stressful job? Creating a business? Supporting family? Building a legacy? Purpose helps prevent extra income from disappearing into lifestyle drift.

The Real Goal Is Optionality

The greatest benefit of multiple income streams is not simply more money. It is optionality.

Optionality means having choices. The choice to leave a bad job. The choice to invest during downturns. The choice to help family without financial panic. The choice to retire gradually. The choice to start a business with reserves. The choice to say no to poor opportunities. The choice to live with less fear.

One income source can support a life. Multiple well-built income streams can support resilience. But the process must be deliberate. Start with skills. Protect the base. Turn income into assets. Treat passive income realistically. Expand with discipline. Keep the system simple enough to manage and strong enough to matter.

Financial freedom rarely arrives from one paycheck, one investment, or one lucky break. It is built by creating a widening distance between dependence and control. Each income stream, if chosen wisely, adds another layer of strength. Each asset adds another claim on the future. Each reinvested dollar gives compounding more material to work with.

The paycheck may be the beginning. It should not be the entire plan.