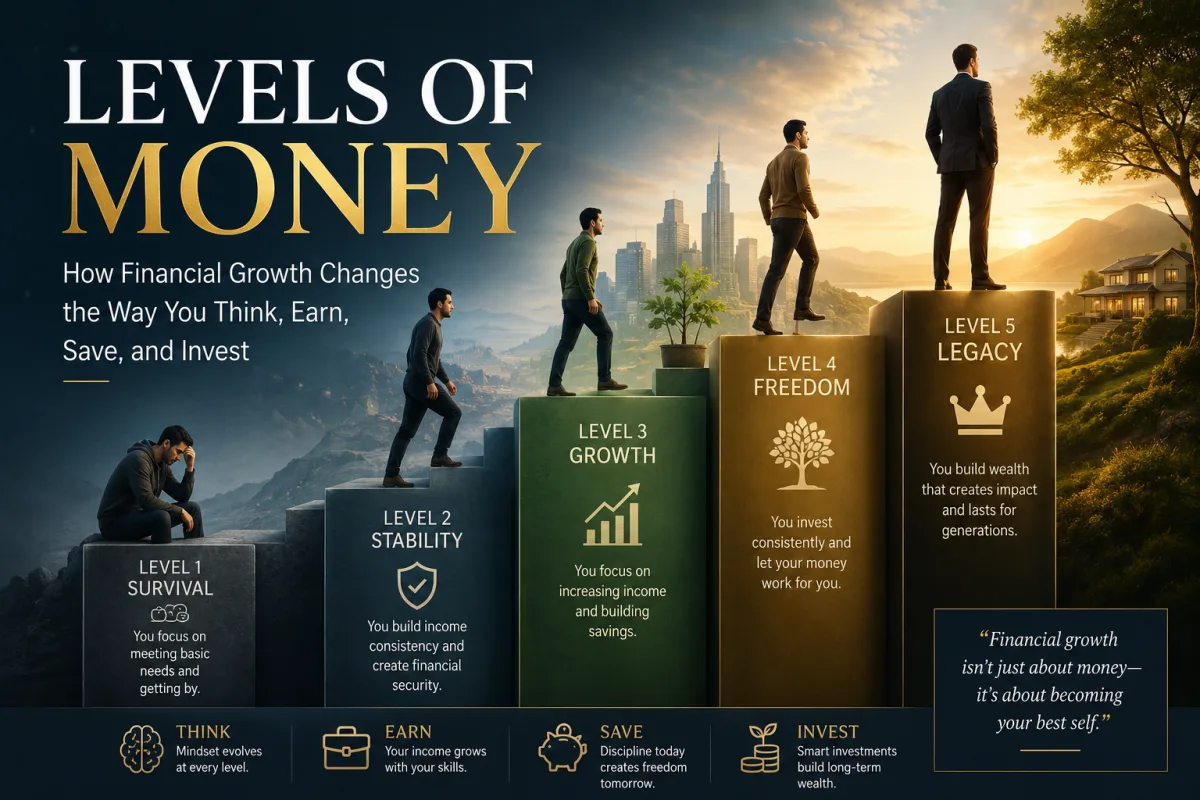

Levels of Money: How Financial Growth Changes the Way You Think, Earn, Save, and Invest

Money is often discussed as if it were one subject. Earn more. Spend less. Save consistently. Invest early. Avoid bad debt. Build assets. These principles matter, but they do not affect every person in the same way because not everyone is operating at the same financial level.

A person trying to keep the lights on does not think about money the same way as someone deciding whether to buy rental property, invest in private businesses, or reduce estate taxes. A family with no emergency fund experiences a car repair differently from a family with twelve months of expenses in cash. A worker depending entirely on one paycheck sees risk differently from an investor whose assets produce income even while they sleep.

The deeper truth is that money changes meaning as your financial position changes.

At one level, money means survival. At another, it means stability. Later, it becomes a tool for freedom, ownership, influence, and legacy. The numbers matter, but the shift is not only mathematical. It is psychological, strategic, and behavioral.

Understanding the levels of money helps explain why some people remain financially stuck even as their income rises, while others quietly build wealth with modest beginnings. It shows why the same financial advice can be powerful for one person and irrelevant for another. It also reveals why wealth is not built by one decision, but by moving through stages with discipline, awareness, and patience.

The First Level: Financial Survival

The first level of money is survival. At this stage, money is not abstract. It is immediate. It is rent, food, transport, school fees, medical bills, electricity, and avoiding embarrassment. Every expense feels urgent because there is little or no margin for error.

Financial survival is not always caused by irresponsibility. Many people begin adult life here because wages are low, family obligations are high, education is incomplete, or previous generations had no wealth to transfer. Others fall into survival after job loss, illness, divorce, business failure, or inflation that outpaces income.

At this level, money is emotional because scarcity is emotional. A small unexpected expense can disrupt the entire month. A delayed payment can create panic. A mistake that seems minor to someone with savings can become a crisis for someone with no buffer.

The defining feature of survival is not poverty alone. It is fragility.

Fragility means there is no cushion between daily life and financial danger. When income arrives, it is already assigned. Debt may be used not for investment or growth, but to bridge the gap between today and the next paycheck. The person may understand good financial habits but feel unable to practice them because the present keeps overpowering the future.

At this level, the most important financial skill is not investing. It is stabilization.

The goal is to create breathing room. That may mean increasing income through overtime, a second skill, small trade, freelancing, negotiation, or a job move. It may also mean reducing recurring expenses, cutting financial leakage, pausing lifestyle upgrades, restructuring debt, or separating needs from habits that only feel necessary.

Survival money requires clear priorities. Food, shelter, basic transport, essential healthcare, and income protection come first. Status spending must wait. Luxury must wait. Even generosity may need boundaries, because giving from an empty financial position can create deeper dependence later.

The mistake many people make at this stage is trying to look stable before becoming stable. They use borrowed money to maintain appearances. They upgrade phones, clothes, cars, celebrations, or housing because social pressure is loud. But appearances do not create security. They often destroy it.

The first victory in financial survival is not becoming rich. It is becoming less vulnerable.

The Second Level: Cash-Flow Awareness

Once survival pressure begins to ease, the next level is cash-flow awareness. This is the stage where a person begins to understand where money actually goes.

Many people think they have an income problem when they also have a visibility problem. Money comes in, money goes out, and the month ends with confusion. The bank balance tells the result, but not the story.

Cash-flow awareness means tracking patterns. It does not require obsession. It requires honesty. How much comes in every month? How much is fixed? How much is flexible? How much disappears through convenience, subscriptions, eating out, fees, impulse purchases, small loans, or unplanned support to others?

This level is powerful because money that is not measured is easily mismanaged.

A person may discover that their largest financial problem is not one dramatic expense but a hundred small leaks. Another may realize that debt repayments are consuming the income that should have built savings. Someone else may see that their lifestyle expanded each time their salary increased, leaving no evidence of progress.

Cash-flow awareness turns money from a mystery into a system.

At this stage, budgeting becomes useful, but not as punishment. A good budget is not a prison. It is a decision-making tool. It tells money where to go before emotion, advertising, urgency, and other people claim it.

The simplest structure is to divide income into four broad uses: living, protection, growth, and giving. Living covers daily needs. Protection covers emergency savings and insurance. Growth covers debt reduction, skills, business, and investments. Giving covers family, community, faith, or causes without allowing generosity to become financial self-harm.

Cash-flow awareness also exposes the difference between affordability and wisdom. A payment may fit into the month and still be unwise. A car loan, apartment upgrade, or expensive membership can be technically affordable but strategically damaging if it prevents saving, investing, or reducing debt.

The lesson of this level is simple: income is not wealth. Income is only the raw material. What happens after income arrives determines whether it becomes consumption, security, or ownership.

The Third Level: Financial Stability

Financial stability begins when money stops feeling like a constant emergency. Bills are paid on time. Basic needs are covered. Debt may still exist, but it is no longer completely controlling the household. There is some savings, some planning, and some ability to absorb ordinary disruptions.

This level feels quiet compared with survival. It may not impress anyone from the outside. There may be no luxury car, no expensive vacation, no dramatic investment story. But stability is one of the most important wealth-building stages because it creates the foundation for every future decision.

The central asset at this level is the emergency fund.

An emergency fund is not glamorous, but it is one of the strongest defenses against financial decline. It prevents ordinary problems from becoming expensive problems. Without cash reserves, a broken appliance can become credit card debt. A medical bill can become a loan. A temporary job disruption can become missed rent, penalties, and damaged credit.

Stability also changes the way a person negotiates life. Someone with savings can leave a harmful job more thoughtfully. They can wait for a better opportunity. They can avoid desperate borrowing. They can make decisions from a place of options rather than fear.

This is where insurance becomes more important. People often dislike paying insurance premiums because nothing visible is gained in the moment. But insurance is not designed to create excitement. It is designed to prevent financial ruin. Health insurance, life insurance for dependents, property insurance, disability cover, and business protection all serve the same purpose: they protect progress from being erased by events too large to handle alone.

At the stability level, the main danger is comfort.

After years of pressure, stability can feel like arrival. A person finally has some breathing room, and the temptation is to reward themselves by increasing lifestyle too quickly. Some reward is healthy. Life should not become endless deprivation. But if every improvement in income becomes a permanent expense, stability never becomes wealth.

The discipline of this level is to protect the gap between income and spending. That gap is the engine of wealth. It funds savings, eliminates debt, buys assets, and creates future freedom.

The Fourth Level: Debt Control

Debt has different meanings at different levels of money. At the survival level, debt is often a rescue tool. At the stability level, it becomes something to manage. At higher levels, certain types of debt may be used strategically. But before debt can become strategic, it must first be controlled.

Debt control means understanding the difference between debt that consumes wealth and debt that may help build it.

Consumer debt is usually the most dangerous. Credit cards, payday loans, buy-now-pay-later balances, high-interest personal loans, and borrowing for lifestyle purchases often transfer future income to past consumption. The borrower enjoys the product once but pays for it repeatedly.

This creates a hidden problem: debt reduces future flexibility.

A person with heavy monthly repayments may appear successful because they own visible goods, but their income is already claimed before they receive it. They cannot easily invest, change jobs, start a business, help family wisely, or handle emergencies because debt has captured their cash flow.

Debt control begins with listing every obligation: lender, balance, interest rate, minimum payment, due date, and purpose. This simple act often changes behavior because vague debt feels less urgent than visible debt.

Two common repayment strategies are the snowball and the avalanche. The snowball method pays the smallest balances first to build momentum. The avalanche method pays the highest-interest debt first to reduce total cost. The better method is the one a person will actually follow, though high-interest debt deserves special attention because it grows aggressively.

Not all debt should be treated equally. A mortgage on a reasonably priced home may differ from a loan used to buy luxury goods. A business loan used carefully to expand profitable operations differs from borrowing to cover a failing lifestyle. Student debt used for a valuable qualification differs from debt taken for a credential with poor earning prospects.

The lesson is not that all debt is evil. The lesson is that debt must be understood before it is used.

At this level, a person begins to reclaim income. Every debt eliminated releases cash flow. That cash flow can then be redirected toward emergency savings, investments, skill development, or asset purchases. Debt repayment is not only about becoming debt-free. It is about buying back control over future income.

The Fifth Level: Income Expansion

Many financial conversations focus heavily on cutting expenses. That matters, especially at the lower levels. But there is a limit to how much a person can cut. There is no fixed limit to how much value a person can learn to create.

Income expansion is the level where financial growth becomes proactive.

At this stage, the question changes from “How do I survive with what I have?” to “How do I increase my earning power?” This shift is essential because wealth requires surplus. A person cannot save, invest, insure, and build assets meaningfully if income remains too small relative to obligations.

Income expansion can happen through several paths. One is career growth: improving skills, gaining credentials, negotiating compensation, changing employers, moving into higher-value roles, or taking leadership responsibility. Another is entrepreneurship: selling products, services, expertise, or systems. A third is asset income: dividends, interest, rent, royalties, or business distributions.

The most accessible path for many people is skill growth.

Skills are economic engines. A person who becomes better at sales, coding, design, accounting, writing, management, nursing, engineering, teaching, logistics, repair, marketing, or analysis can often increase income without waiting for luck. The market pays for problems solved, value created, risk managed, and results delivered.

However, income expansion is not only about working more hours. Working more can help temporarily, but time is limited. The deeper goal is to increase the value of each hour or to build income streams that are not directly tied to every hour worked.

This is why specialization matters. General effort earns general rewards. Specific, valuable, scarce skills often earn more. A person who can solve expensive problems becomes economically stronger than someone who only performs easily replaceable tasks.

At this level, networking also becomes financial. Relationships create information, opportunity, trust, referrals, partnerships, and access. Many people underestimate this because networking sounds social, but in economic life, trust is a form of capital.

The main danger of income expansion is lifestyle inflation. When income rises, spending often rises quietly. Better restaurants, better housing, better clothes, better devices, better entertainment, and more generous commitments can absorb the increase before it becomes wealth.

The wise approach is to capture part of every income increase for the future before lifestyle adjusts. If income rises by 20 percent, a disciplined person may invest half of the increase and enjoy the rest. This allows life to improve while wealth also grows.

Income expansion is not the finish line. It is the fuel. Without discipline, higher income only finances higher consumption. With discipline, higher income becomes the bridge to ownership.

The Sixth Level: Capital Formation

Capital formation is the point where surplus income begins turning into productive money.

Capital is money set aside not merely to be spent later, but to create more options, more income, or more assets. It includes savings, investment contributions, business reserves, down payments, education funds, and money available for opportunity.

This level is where many people fail quietly. They earn enough to build capital, but they do not. Their surplus is consumed by convenience, social comparison, emotional spending, or poor planning. They make enough money to become investors, but they remain consumers.

The first rule of capital formation is paying yourself first. This means allocating money to savings and investments before discretionary spending expands. It is easier to build wealth by removing money from temptation early than by hoping something remains at the end of the month.

Automation can help. Automatic transfers to savings, retirement accounts, brokerage accounts, or debt repayment plans reduce the need for repeated willpower. Wealth is easier to build when good behavior becomes the default.

Capital formation also requires understanding liquidity. Not all money should be locked away. Emergency funds need to be accessible. Investment money can be long-term. Business reserves may need a different structure. A person who invests every dollar but has no cash may be forced to sell assets at a bad time during an emergency.

This stage introduces a more mature question: what is this money for?

Some capital protects. Some capital grows. Some capital creates income. Some capital buys time. Some capital funds opportunity. Without purpose, money can be misallocated. A person saving for a house deposit should not treat that money the same way as retirement money. A business owner’s operating reserves should not be exposed to the same risk as long-term investments.

Capital formation is also where patience becomes visible. Small amounts invested consistently may feel unimpressive in the beginning. The early years can be slow because the balance is mostly built from contributions, not returns. Over time, compounding begins to matter more. Eventually, money starts contributing alongside the person.

The emotional challenge is that consumption gives immediate feedback. Investing often does not. A new purchase is visible today. A growing investment account may feel abstract. The investor must learn to value invisible progress.

This is one of the great dividing lines in personal finance: consumers seek immediate evidence of money spent; wealth builders accept delayed evidence of money invested.

The Seventh Level: Ownership

Ownership is the level where money begins to change character.

At earlier levels, money is mainly earned through labor. At the ownership level, money is increasingly earned through assets. This does not mean work stops. It means work is no longer the only financial engine.

Ownership can take many forms: shares in public companies, rental property, private business equity, intellectual property, farmland, digital assets, royalties, partnerships, or ownership of a professional practice. The form matters less than the principle. Owners benefit when assets produce value.

This is the level where the difference between income and wealth becomes impossible to ignore.

A high-income earner who owns few assets may still depend entirely on continued labor. A moderate-income person who consistently buys productive assets may become wealthier over time because their money begins to work independently.

Ownership is powerful because assets can compound. A business can reinvest profits. A property can produce rent and appreciate. A stock portfolio can grow as companies increase earnings. Royalties can continue after the original work is done. The owner participates in economic output beyond their personal hours.

But ownership also introduces risk.

Assets fluctuate. Businesses fail. Tenants leave. Markets decline. Interest rates change. Regulations shift. Maintenance costs rise. Customers disappear. Ownership is not magic. It is responsibility.

The mature owner does not chase assets blindly. They study cash flow, valuation, risk, debt, management, diversification, taxes, and time horizon. They understand that an asset is not good simply because it is called an investment. A bad investment can be worse than no investment because it consumes capital, attention, and confidence.

The ownership level also requires emotional discipline. Markets move. People panic. Headlines create fear. Friends promote trends. Social media celebrates sudden wealth without showing hidden losses. The investor must learn to separate signal from noise.

One of the most important principles at this stage is that ownership rewards patience more often than excitement. Many people lose money not because they chose terrible assets, but because they lacked the temperament to hold quality assets through discomfort or because they bought assets they did not understand.

Ownership changes identity. The person no longer sees money only as something to earn and spend. They see it as something to allocate. Every dollar can become a worker, a seed, a shield, or a vote for the future.

The Eighth Level: Financial Optionality

Financial optionality is the level where money begins to buy choices.

Optionality does not necessarily mean extreme wealth. It means having enough financial strength to make decisions without being trapped by immediate necessity. It is the ability to say no, wait, change direction, negotiate, rest, learn, relocate, start again, or take a calculated risk.

This level is deeply underrated because it is less visible than luxury. A person with optionality may not look rich. They may drive a modest car, live in a reasonable home, and avoid dramatic displays. But they possess something more valuable than appearance: room to maneuver.

Optionality can show up in ordinary life. A worker can leave a toxic employer without financial collapse. A parent can take time off for a child. A business owner can reject a bad client. An investor can buy during a downturn instead of selling in panic. A family can handle a medical emergency without destroying long-term plans.

Money at this level becomes a buffer between values and pressure.

Without optionality, people often accept terms they dislike. They stay in unhealthy jobs, remain in bad business relationships, borrow at terrible rates, sell assets too early, or make decisions from fear. With optionality, they can choose more carefully.

Optionality is built through liquidity, low fixed expenses, diversified income, strong skills, good credit, and assets that are not overleveraged. It is not just the size of net worth. A person with a large house, expensive car, high debt, and little cash may have less optionality than someone with a smaller net worth but more liquidity and fewer obligations.

This is why lifestyle design matters. The more expensive your life becomes, the more income you must generate just to remain in place. High fixed costs reduce freedom. They turn success into a treadmill.

At this level, the question is no longer only “Can I afford it?” The better question is “What does this do to my freedom?”

A larger home may be affordable, but does it require more years of stressful work? A luxury car may be within reach, but does it delay investment capital? A prestigious lifestyle may impress others, but does it reduce the ability to make independent choices?

Optionality is one of the purest forms of wealth because it is experienced internally. It is calm. It is confidence. It is the knowledge that one setback will not destroy everything.

The Ninth Level: Strategic Risk

At lower levels of money, risk often appears as danger. The goal is to avoid mistakes because there is little room to recover. At higher levels, risk becomes something to evaluate, price, manage, and sometimes accept.

Strategic risk is not gambling. It is not speculation disguised as courage. It is the thoughtful use of capital, time, reputation, or effort in pursuit of a return that is worth the uncertainty.

Examples include starting a business after building savings, investing during market declines, buying property after careful analysis, changing careers to enter a higher-growth field, expanding a profitable company, or pursuing advanced training with a clear economic payoff.

The key difference between reckless risk and strategic risk is preparation.

Reckless risk ignores downside. Strategic risk studies it. Reckless risk depends on hope. Strategic risk uses probabilities. Reckless risk bets the future on one outcome. Strategic risk preserves the ability to survive being wrong.

At this level, the investor or wealth builder learns that avoiding all risk can become a risk itself. Cash loses purchasing power over time when inflation rises. Staying in a stagnant career can be risky. Keeping all income dependent on one employer can be risky. Refusing to invest can be risky. Overprotecting oneself from volatility can create long-term weakness.

Strategic risk requires a margin of safety. This concept applies across finance. An investor may buy assets below estimated value. A household may keep extra cash. A business may avoid relying on one major customer. A landlord may budget for vacancies and repairs. A borrower may choose a smaller loan than the maximum approved.

The margin of safety acknowledges that life does not obey spreadsheets. Costs rise. Timelines stretch. Markets surprise. People change. The wise financial planner leaves room for reality.

Strategic risk also requires position sizing. Even a good opportunity can become dangerous if too much is committed to it. A person who puts all capital into one business, one property, one stock, or one trend may be right about the opportunity and still financially vulnerable because concentration magnifies consequences.

At this level, humility becomes a financial asset. The person who admits uncertainty prepares better than the person who believes confidence guarantees success.

The Tenth Level: Time Freedom

Time freedom is the level many people imagine when they think about wealth. It is the ability to control one’s time because financial obligations no longer require constant labor in the same way.

This does not always mean retirement. Many financially free people continue working. The difference is that work becomes more chosen than forced. They may work on projects they care about, build businesses, teach, invest, create, mentor, or serve. The financial pressure behind the work changes.

Time freedom is built when assets, savings, and income systems can support a meaningful portion of life expenses. The exact number varies by lifestyle, location, family size, health, and goals. Someone with modest expenses may reach meaningful freedom with far less than someone whose life requires high spending.

This is why the path to time freedom has two sides: building assets and managing lifestyle.

A person can increase investments aggressively, but if spending rises just as fast, freedom remains distant. Another person can live modestly but fail to invest enough, also delaying freedom. The balance matters.

Time freedom forces a person to calculate the cost of their life. How much does it take to live comfortably? How much is necessary? How much is preference? How much is status? How much spending genuinely improves life, and how much simply maintains an image?

These questions can be uncomfortable because they reveal that some people are not trapped by income alone. They are trapped by the lifestyle their income has been trained to support.

At this level, assets become time machines. Every investment that produces income or appreciates responsibly can reduce future dependence on labor. Every unnecessary liability can extend that dependence.

Time freedom also raises a deeper issue: what will you do with freedom when you have it?

Many people spend years wanting escape without designing a life worth entering. They dream of not working, but they do not cultivate purpose, relationships, health, curiosity, or contribution. Money can create space, but it cannot automatically fill that space with meaning.

The healthiest version of time freedom is not idleness. It is alignment. Time, energy, money, and values begin to point in the same direction.

The Eleventh Level: Financial Independence

Financial independence is often described as the point where work becomes optional because assets can support living expenses. This is a major milestone, but it should be understood carefully.

Independence is not only a number. It is a relationship between assets, spending, risk, taxes, inflation, healthcare, family needs, and time horizon. A person with high assets and high spending may be less independent than they appear. A person with moderate assets and low obligations may be stronger than outsiders assume.

Financial independence requires systems. Investment policy matters. Withdrawal strategy matters. Tax planning matters. Estate documents matter. Insurance matters. Asset allocation matters. Cash reserves matter. Without structure, even substantial wealth can be mismanaged.

At this level, the danger often shifts from not having enough to not managing enough wisely.

People who accumulate wealth through high income may not automatically know how to preserve it. Entrepreneurs who sell businesses may struggle to adjust from active control to portfolio management. Professionals who retire may underestimate healthcare costs, family support, market volatility, or the emotional transition away from career identity.

Financial independence also changes relationships. Family members may expect help. Friends may make assumptions. Adult children may need support. Aging parents may require care. Wealth can create opportunity, but it can also create obligation and tension.

The independent person needs boundaries as much as generosity. Helping others is honorable, but unstructured help can weaken both sides. It can create dependency, resentment, or financial strain. Wise giving has limits, purpose, and clarity.

At this level, preservation becomes as important as growth. The wealth builder must avoid catastrophic mistakes: excessive leverage, fraud, concentrated bets, lifestyle explosion, poor legal planning, and emotional decision-making during market stress.

Financial independence is not the end of financial education. It is the beginning of a more complex form of stewardship.

The Twelfth Level: Influence and Stewardship

As wealth grows beyond personal security, money becomes a tool of influence. This influence may be quiet or public. It can shape families, businesses, communities, institutions, charities, political causes, education, housing, employment, and culture.

At this level, the central question changes from “How do I build wealth?” to “What should this wealth do?”

Stewardship means managing resources with responsibility beyond immediate personal consumption. It recognizes that money carries consequences. How it is invested, spent, donated, lent, inherited, and discussed can affect many lives.

A business owner who employs people practices stewardship. An investor who funds productive enterprises practices stewardship. A parent who teaches children financial discipline practices stewardship. A philanthropist who gives thoughtfully practices stewardship. A landlord who maintains safe housing practices stewardship.

Influence without wisdom can be harmful. Wealth can amplify ego, control, vanity, or poor judgment. It can also enable patience, education, innovation, stability, and opportunity. Money magnifies the person or system directing it.

This level requires values. Without values, wealth becomes reactive. It follows trends, pressure, tax avoidance, family demands, or personal insecurity. With values, wealth becomes intentional.

For families, stewardship often means preparing heirs. Many families focus on transferring assets but fail to transfer judgment. Children may inherit money without discipline, gratitude, skill, or purpose. In those cases, wealth can become a burden rather than a blessing.

Teaching financial maturity matters more than simply leaving financial resources. Heirs need to understand work, budgeting, investing, generosity, taxes, risk, and responsibility. They need to see money used as a tool, not as a substitute for character.

At this level, wealth planning becomes multi-generational. Wills, trusts, business succession plans, charitable structures, family governance, insurance, and tax strategy become important. These tools are not only for the ultra-rich. They are ways of reducing confusion, conflict, and waste.

Stewardship is the level where wealth becomes less about possession and more about direction.

The Hidden Level: Money as Identity

Behind every level of money is a hidden level: identity.

People do not only manage money with calculators. They manage it with stories. Some people see themselves as survivors and struggle to feel safe even after becoming stable. Some see themselves as spenders because consumption once made them feel successful. Some avoid investing because they believe wealth is for other people. Some sabotage progress because financial growth creates guilt, fear, or distance from their community.

Money beliefs often come from childhood. A person raised in scarcity may hoard cash and fear risk. Another raised around financial chaos may avoid looking at money altogether. Someone who saw wealth used arrogantly may reject wealth emotionally while still needing it practically. Someone praised only for achievement may use money to prove worth.

This is why financial education must include self-awareness.

A person can learn investment theory and still make poor decisions if fear controls them. They can earn high income and still overspend if status drives them. They can build wealth and still feel anxious if their identity never adjusts.

Healthy financial identity is not arrogance. It is alignment between behavior and long-term values. It allows a person to say, “I am someone who manages money responsibly. I am someone who builds assets. I am someone who protects my family. I am someone who can enjoy money without being controlled by it.”

Identity also affects patience. Investors who see themselves as long-term owners behave differently from people chasing quick wins. Families who see themselves as stewards behave differently from families trying to impress neighbors. Workers who see themselves as value creators behave differently from workers waiting passively for raises.

The deepest financial shifts often happen when a person stops asking only, “What should I do with money?” and starts asking, “Who am I becoming through the way I handle money?”

Why People Get Stuck Between Levels

Financial growth is not automatic. Many people remain stuck not because they lack intelligence, but because each level requires a different mindset and skill set.

The habits that help someone survive may not help them build wealth. Survival may require urgency, caution, and short-term thinking. Wealth building requires planning, patience, and trust in delayed results. A person who has spent years reacting to emergencies may struggle to think ten years ahead.

People also get stuck because they confuse income growth with level growth. They earn more but do not become more stable. They buy more but do not own more. They appear wealthier but become more obligated.

Social comparison is another trap. Money is personal, but spending is public. People see the car, wedding, vacation, watch, house, or restaurant. They do not see the debt, stress, missed investments, or lack of savings behind it. Trying to match visible lifestyles can delay invisible wealth.

Family pressure can also keep people stuck. In many households, the first person to earn more becomes the financial rescue system for everyone else. Supporting family can be noble, but without structure it can prevent the wealth builder from ever creating the foundation that would allow them to help more sustainably later.

Another reason people get stuck is fear of risk. After reaching stability, some become so protective that they never invest, never build skills, never start businesses, and never pursue growth. They avoid loss so completely that they also avoid opportunity.

Others get stuck because they take too much risk too soon. They skip emergency savings and jump into speculative investments. They borrow heavily for ideas they have not tested. They chase trends because they want to escape lower levels quickly. Impatience can destroy progress.

The path through the levels of money requires sequencing. Stabilize before speculating. Learn before leveraging. Build cash flow before buying status. Protect before expanding. Own before showing off. Preserve before distributing.

How to Move Up One Level at a Time

The most practical way to use the levels of money is to identify your current level honestly and focus on the next step, not the final destination.

If you are in survival, your priority is immediate stabilization. Increase income where possible. Reduce financial leakage. Protect essentials. Avoid high-interest debt. Build the first small emergency buffer, even if it begins with a modest amount. The goal is to interrupt crisis mode.

If you have cash-flow awareness but little stability, create a system. Track income and spending. Separate fixed and variable expenses. Assign money before spending it. Start building reserves. Reduce the expenses that create stress without adding real value.

If you are stable but carrying harmful debt, attack the debt strategically. Know your balances and interest rates. Stop adding new consumer debt. Use a repayment method that fits your psychology. Redirect freed payments toward savings and investments.

If debt is controlled, expand income. Build skills. Negotiate. Seek better opportunities. Start a side enterprise if appropriate. Learn to sell your value. Capture a portion of every income increase for wealth building.

If income is growing, form capital. Automate savings and investments. Build liquidity. Create separate accounts for emergencies, opportunities, taxes, and long-term investing. Give money a job before lifestyle absorbs it.

If you have capital, pursue ownership. Learn asset classes. Understand risk. Invest consistently. Avoid trends you cannot explain. Diversify. Think like an owner rather than a consumer.

If you own assets, build optionality. Keep fixed expenses reasonable. Avoid overleverage. Maintain liquidity. Develop multiple income sources. Protect your ability to make decisions without desperation.

If you have optionality, take strategic risks. Invest in growth, but preserve your downside. Use position sizing. Study opportunities carefully. Accept uncertainty without becoming careless.

If you approach time freedom, define enough. Calculate your real cost of living. Decide what work you want to keep doing. Build a withdrawal or income strategy. Prepare emotionally for a life less driven by obligation.

If you reach independence, practice stewardship. Protect wealth. Teach heirs. Give wisely. Plan legally. Use money to support values rather than ego.

The Role of Investing Across the Levels

Investing is often presented as the central act of wealth building, but its role changes depending on the level.

At survival, the best investment may be transportation to work, a certification, a safer living arrangement, or paying off predatory debt. At stability, the best investment may be an emergency fund because it prevents future borrowing. At debt control, eliminating high-interest debt may produce a stronger guaranteed benefit than many market investments.

Once capital formation begins, investing in financial assets becomes more central. Retirement accounts, index funds, dividend-paying companies, bonds, real estate, and business ownership can all play roles depending on goals and risk tolerance.

The purpose of investing is not simply to become rich quickly. It is to move money from consumption into productive ownership. Investing allows a person to participate in growth beyond their own labor.

Good investing requires time horizon. Money needed soon should not be exposed to the same volatility as money intended for decades ahead. A young investor saving for retirement may handle market swings differently from a family saving for a home deposit next year.

Good investing also requires behavior. Many investors underperform not because markets fail them, but because they buy high, sell low, chase performance, panic during declines, follow hype, ignore fees, or concentrate too heavily in what recently worked.

Across the levels of money, investing becomes more effective when the foundation is strong. A person with cash reserves can stay invested during downturns. A person with low debt has more flexibility. A person with stable income can contribute consistently. A person with financial education can avoid obvious traps.

Investing is not a substitute for financial maturity. It is an expression of it.

The Role of Saving Across the Levels

Saving is sometimes dismissed as too slow to build wealth, especially when compared with investing or entrepreneurship. But saving has a different function. Saving creates control.

At lower levels, saving protects survival. At middle levels, it creates stability and opportunity. At higher levels, it supports strategy, tax planning, investment timing, and peace of mind.

Cash does not always produce high returns, but it produces readiness. The person with cash can handle emergencies, negotiate from strength, avoid forced selling, and move when opportunity appears.

The mistake is not saving. The mistake is saving without purpose or saving only in cash forever. Too little cash creates fragility. Too much idle cash can slow long-term growth. The right balance depends on life stage, obligations, risk, and goals.

Saving also builds the muscle of delayed gratification. Before someone can invest successfully, they must first spend less than they earn. Saving proves that the gap exists. It trains the behavior that makes investing possible.

The Role of Debt Across the Levels

Debt is one of the most misunderstood financial tools because it can either accelerate growth or accelerate failure.

At low levels of money, debt often reflects lack of options. People borrow because they must. At middle levels, debt must be reduced and controlled. At higher levels, debt may be used carefully to acquire assets, expand businesses, or optimize capital structure.

The danger is using advanced debt strategies with a beginner’s foundation.

Borrowing to invest can be destructive if income is unstable, emergency savings are weak, interest rates are high, or the investor does not understand the asset. Leverage magnifies outcomes. It can increase returns, but it can also increase losses and pressure.

A simple test is whether the debt improves future cash flow or only satisfies present desire. Debt used for consumption usually weakens the future. Debt used for productive purposes may help if the numbers, risks, and timing are sound.

Even productive debt requires respect. A rental property with a mortgage still needs tenants, maintenance, insurance, taxes, and reserves. A business loan still needs customers and profit. An education loan still needs earning power. Debt does not forgive poor assumptions.

The Role of Lifestyle Across the Levels

Lifestyle is where financial theory meets daily behavior.

Most people do not ruin their finances through one large decision. They do it through repeated lifestyle choices that become permanent obligations. A more expensive apartment. A higher car payment. Frequent convenience spending. Upgraded subscriptions. Social events that strain the budget. Gifts given from pressure rather than planning.

Lifestyle is not the enemy. A good life is part of the reason people pursue financial progress. The danger is unconscious lifestyle expansion.

The wealth-building question is not “How little can I enjoy?” It is “Which forms of spending genuinely improve my life, and which only create the appearance of progress?”

Some spending is deeply worthwhile. Good healthcare, quality education, safe housing, meaningful travel, tools for work, healthy food, and experiences with loved ones can be valuable. Other spending is mostly performance. It exists to signal success to people who may not matter.

As people rise through the levels of money, lifestyle should improve intentionally, not automatically. The best approach is conscious upgrading. Choose what matters. Fund it without sacrificing stability, ownership, or freedom. Let wealth change life, but do not let lifestyle consume wealth before it matures.

The Role of Community and Family

Money is personal, but it is rarely isolated. Family expectations, cultural norms, friendships, community obligations, and social environments shape financial decisions.

For some people, wealth building is not an individual journey. It is complicated by dependents, relatives, siblings, parents, children, and community responsibilities. The first person in a family to earn stable income may become the emergency fund for everyone else.

This creates a difficult tension. Ignoring family can feel selfish. Supporting everyone without boundaries can prevent progress. The answer is not coldness. It is structure.

Structured support means deciding in advance how much help is sustainable, what type of help is productive, and where boundaries must exist. Paying for education, medical needs, or income-generating tools may be more helpful than repeatedly funding consumption. Creating a family support budget may prevent emotional decisions from damaging core financial goals.

Communication matters. People may not like boundaries, especially if they benefited from the absence of them. But unclear generosity can create resentment on both sides. The giver feels drained. The receiver feels judged when support changes.

At higher levels, family financial education becomes essential. Teaching budgeting, investing, work ethic, and responsibility may do more good than giving money without guidance.

Signs You Are Moving Up Financially

Progress through the levels of money is not always dramatic. Sometimes it appears as reduced anxiety. Sometimes it appears as better decisions. Sometimes it appears as saying no to things that once controlled you.

You know you are moving up when emergencies become inconveniences rather than disasters. You know you are moving up when income increases do not disappear immediately. You know you are moving up when debt balances shrink and asset balances grow. You know you are moving up when you think in years instead of only days.

You are progressing when you can discuss money honestly without shame. You are progressing when you understand your numbers. You are progressing when you buy assets before status. You are progressing when financial decisions align with values rather than pressure.

The most powerful sign is optionality. When you have more choices than before, your money is beginning to serve you.

The Real Purpose of Understanding the Levels of Money

The levels of money are not meant to create judgment. They are meant to create clarity.

Someone at the survival level is not inferior to someone at the ownership level. They are simply facing different constraints. Someone with wealth is not automatically wise. They may have high assets and poor judgment. Someone with modest income may be developing the habits that lead to long-term strength.

The point is to understand the level you are in, master its lessons, and avoid copying strategies that belong to a different stage.

A person in survival should not feel ashamed for prioritizing cash flow over investing. A person with high-interest debt should not feel behind because they are paying it down instead of chasing market trends. A person building capital should not be distracted by luxury signals. A person with assets should not become careless because the numbers are growing.

Each level has a job.

Survival teaches urgency. Awareness teaches honesty. Stability teaches protection. Debt control teaches discipline. Income expansion teaches value creation. Capital formation teaches delayed gratification. Ownership teaches patience. Optionality teaches freedom. Strategic risk teaches judgment. Time freedom teaches alignment. Independence teaches preservation. Stewardship teaches responsibility.

Money grows best when each lesson is learned in order.

Final Thoughts

Money is not just a balance in an account. It is a progression of skills, choices, beliefs, and responsibilities.

At first, money helps you survive. Then it helps you stabilize. Later, it helps you build, own, choose, protect, and give. The journey is not always smooth. People move forward, fall back, recover, and rebuild. But the direction matters.

The mistake is thinking wealth begins only when the numbers become large. Wealth begins earlier, when a person starts treating money with intention. It begins when spending becomes conscious, debt becomes visible, income becomes expandable, saving becomes automatic, investing becomes disciplined, and ownership becomes the goal.

The highest levels of money are not defined only by luxury or status. They are defined by freedom, resilience, wisdom, and the ability to use resources well.

To move up financially, do not ask only how to get more money. Ask what level you are currently operating from. Ask what skill that level requires. Ask what habit must change. Ask what risk must be reduced, what asset must be built, what belief must be challenged, and what decision your future self will thank you for making.

Money has levels because life has levels. The goal is not merely to have more. The goal is to become capable of managing more with clarity, patience, and purpose.