Savings Rules That Make Wealth Easier: 12 Systems for Turning Income Into Security

Saving money is often presented as a test of willpower.

Spend less. Try harder. Be disciplined. Stop making excuses. Resist temptation. Think about the future. Avoid waste. Make better choices.

There is some truth in that advice, but it is incomplete. Willpower is unstable. It weakens under stress, fatigue, social pressure, scarcity, advertising, family obligations, and emotional spending. A person may be motivated on payday and discouraged two weeks later. They may promise to save after expenses, then discover that expenses have expanded to consume the available money. They may understand the importance of saving and still fail to do it consistently because their financial system is built around leftover money rather than assigned money.

That is why the strongest savings strategies rely less on motivation and more on structure.

Saving becomes easier when it is automatic, separated, tracked, increased gradually, protected from emotion, and connected to long-term purpose. The goal is not to become a perfect financial machine. The goal is to create a system that keeps working when motivation disappears.

This distinction matters because savings are not only about future wealth. They are about present resilience. A household with savings can handle a car repair, medical bill, delayed paycheck, job transition, home expense, family emergency, or opportunity without immediately turning to high-interest debt. Savings buy time. They buy calm. They buy choices.

The Consumer Financial Protection Bureau’s Financial Well-Being Scale connects financial well-being to the ability to meet current obligations, feel secure about the future, and make choices that support life satisfaction. The CFPB’s 2026 score-range guide notes that people with very high financial well-being are much more likely to have high liquid savings and automated deposits into savings or retirement accounts. The Federal Reserve’s Survey of Household Economics and Decisionmaking also tracks emergency savings, including whether adults can cover a $400 emergency expense with cash or its equivalent.

These sources point to a practical truth: saving is not only a personal virtue. It is financial infrastructure.

The 12 rules in this article are designed to make saving easier, more consistent, and more resilient. They are broadly supported by behavioral economics and personal finance research, but they should be adapted to income, living costs, debt, household size, job stability, and financial goals. A person with high-interest debt may need a different savings strategy from a person with no debt and stable income. A freelancer may need larger reserves than a salaried employee. A retiree may think differently from a young professional. A family with dependents may need more liquidity than a single person with low fixed costs.

The rules are not commandments. They are systems. Used well, they help income become security, security become opportunity, and opportunity become wealth.

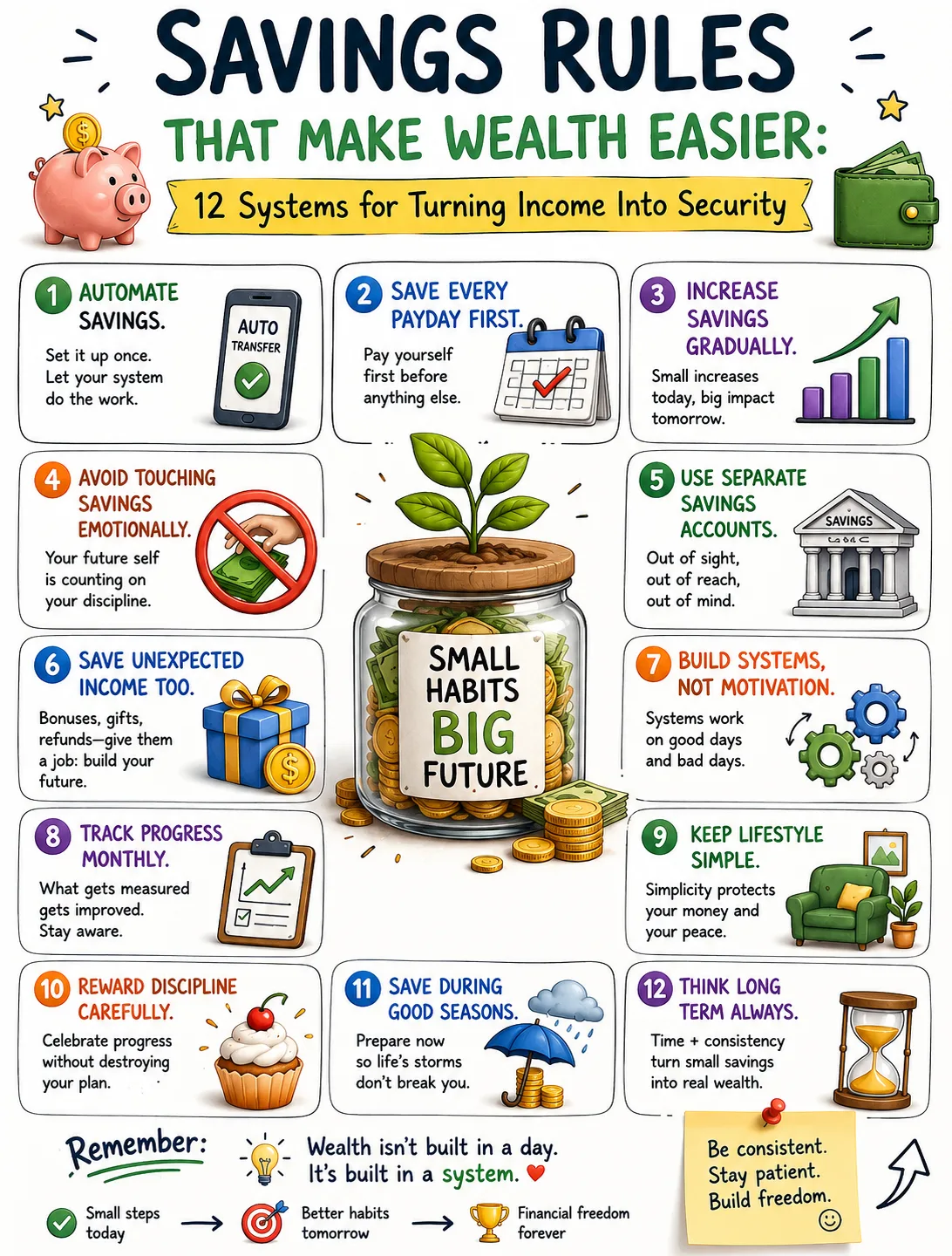

1. Automate Savings Immediately

The first savings rule is to remove saving from the list of things you must remember to do.

Automatic saving works because it changes the default. Instead of waiting to see what remains after spending, money is transferred before spending has the chance to claim it. The decision is made once, then repeated by the system.

This is powerful because most people do not fail to save from lack of knowledge. They fail because life happens. Bills arrive. Friends invite them out. Children need something. A subscription renews. A stressful day leads to a purchase. A bank balance looks larger than it really is because future expenses have not yet cleared. By the end of the month, the money that was supposed to be saved has quietly disappeared.

Automation protects savings from daily negotiation.

The simplest version is an automatic transfer from checking to savings on payday. Another version is automatic payroll deduction into a retirement plan. A household may automate transfers into an emergency fund, home down payment account, education account, tax account, investment account, or sinking fund for irregular expenses.

Automation is also one reason retirement plan design has received so much attention in behavioral economics. Richard Thaler and Shlomo Benartzi’s Save More Tomorrow program asked workers to commit in advance to directing part of future pay increases into retirement savings, using behavioral design to increase saving over time. The principle is simple: make the beneficial action easier before the emotional moment arrives.

Automation does not mean ignoring your finances. Automated transfers should be reviewed to ensure they remain affordable, aligned with goals, and coordinated with bills. An automatic transfer that causes overdrafts is not a good system. But when designed well, automation makes saving ordinary.

Start with an amount you can sustain. The number does not need to be impressive. The first purpose is to build the habit and prove that saving can happen without monthly debate. Once the system is stable, the amount can rise.

Automation turns saving from an intention into a scheduled event.

2. Save Every Payday First

The phrase “pay yourself first” has survived because it solves a common problem: people try to save what is left over, but leftover money often does not survive the month.

Paying yourself first means treating saving as a priority expense. When income arrives, a portion is immediately directed toward future security before discretionary spending begins. This reverses the usual pattern. Instead of saving after life has consumed the paycheck, saving becomes part of the paycheck’s first assignment.

This rule matters because spending tends to expand into available money. If the full paycheck remains visible in a checking account, it can feel spendable. Even people with good intentions may mentally overestimate what is available because they forget upcoming bills, irregular expenses, or future goals. Paying yourself first reduces that illusion.

The rule also changes identity. A person who saves every payday begins to see themselves not only as a spender of income but as a builder of reserves. That identity can become self-reinforcing. The savings transfer becomes as normal as paying rent, utilities, or insurance.

For households with tight finances, paying yourself first may need to start very small. Saving $5, $10, or $25 per payday may feel insignificant, but it establishes the pattern. The first goal is not to become wealthy overnight. It is to create proof that some income can remain unspent.

For households with stronger cash flow, the payday-first rule can be expanded. Retirement contributions, brokerage investments, emergency savings, education funds, and sinking funds can all be paid before lifestyle spending. The household can still enjoy money, but enjoyment comes after the future has been funded.

This is not deprivation. It is sequencing.

The person who saves first does not ask, “What can I save after spending?” They ask, “What can I spend after saving?” That small reversal can change a financial life.

3. Increase Savings Gradually

Many people fail at saving because they try to change too much at once.

They decide to save aggressively, cut every enjoyable expense, and transform their financial life in one month. The plan works briefly, then collapses because it is too severe. The household returns to old habits and concludes that saving is impossible.

Gradual increases are often more sustainable. Saving an additional 1 percent of income, increasing transfers after a raise, or adding a small amount every quarter may feel manageable. Over time, these small changes can produce meaningful results.

This rule is especially effective after income increases. A raise creates a rare opportunity because the household has not yet fully adjusted to the higher income. If part of the raise is immediately directed into savings or investments, wealth building improves without requiring a painful cut from the previous lifestyle.

Gradual increases also fight lifestyle inflation. Lifestyle inflation happens when spending rises as income rises. A better job leads to a better apartment, newer car, more restaurants, better holidays, more subscriptions, and higher expectations. None of these upgrades may feel reckless individually, but together they can absorb every raise.

Saving increases should be tied to financial milestones. When income rises, increase savings. When a debt is paid off, redirect part of the old payment to savings or investments. When a bonus arrives, save a predetermined percentage. When a subscription is canceled, redirect the amount. When a child-related expense ends, assign part of the freed cash to long-term goals.

Fidelity has emphasized that even a 1 percent increase in retirement contributions can make a meaningful difference over time, and it encourages savers who cannot immediately reach larger targets to begin where they can and raise contributions after raises or promotions.

The rule is not to save painfully. The rule is to save progressively.

Wealth is often built when small increases become permanent before lifestyle can claim them.

4. Avoid Touching Savings Emotionally

Savings should be accessible enough to help in a real emergency and protected enough to avoid emotional withdrawals.

This balance is important. An emergency fund is meant to be used when genuine emergencies occur. If income stops, a medical bill arrives, a car repair is necessary, or an essential household expense cannot wait, savings should reduce the need for high-interest borrowing. The problem is not using savings for real needs. The problem is raiding savings for temporary emotions.

Emotional withdrawals often occur after stress, boredom, comparison, frustration, or excitement. A person sees something they want, notices money in savings, and tells themselves they will replace it later. Sometimes they do. Often, they do not. The savings account becomes a holding account for future spending rather than a protective reserve.

One way to prevent this is to define savings categories clearly. Emergency savings are for emergencies. A travel fund is for travel. A tax fund is for taxes. A home repair fund is for repairs. When every savings dollar has a specific job, it becomes harder to justify using it casually.

Another method is friction. Keep emergency savings in a separate high-yield savings account rather than in the same checking account used for daily spending. Avoid linking the account to a debit card. Use a bank that allows transfers but not instant impulse access. The goal is not to make savings impossible to use. The goal is to create enough delay for emotion to cool.

A household can also use a written rule: before withdrawing from savings, name the purpose, amount, replacement plan, and whether the expense is urgent, necessary, or discretionary. This simple pause can prevent many withdrawals driven by mood.

Protecting savings emotionally is not about being rigid. It is about respecting the purpose of the money. Savings are stored choices. Every unnecessary withdrawal spends not only cash but future flexibility.

5. Create Separate Savings Accounts

Separate savings accounts turn vague money into specific goals.

Behavioral economists often describe mental accounting as the tendency to categorize money into different mental buckets. In strict economic theory, money is fungible: one dollar is the same as another. In real life, people behave differently when money is labeled. A dollar in an emergency fund feels different from a dollar in a vacation fund. A tax account feels different from a spending account.

This tendency can be used constructively. Separate accounts help households organize money by purpose. Emergency fund. Rent buffer. Taxes. Annual insurance premiums. Car repairs. Home maintenance. Education. Travel. Medical expenses. Business expenses. Down payment. Holiday spending. Each account answers a specific future need.

The benefit is clarity. Without separate accounts, a single savings balance can be misleading. A person may have $5,000 saved and feel secure, but $2,000 is needed for taxes, $1,000 for annual insurance, and $1,500 for a planned move. The true emergency reserve may be much smaller than it appears. Separate accounts prevent accidental double-counting.

Separate accounts also reduce guilt around planned spending. If money has been intentionally saved for a holiday, using it for that purpose does not feel like failure. The problem with spending is not always the spending itself. It is unplanned spending that steals from higher priorities.

Digital banking has made this easier. Many banks allow multiple savings accounts or subaccounts with labels. Some budgeting apps simulate the same effect. A spreadsheet can also work if the household is disciplined about tracking.

Separate accounts should not become too complicated. Too many categories can create confusion. The right number depends on the household. A simple structure might include emergency fund, annual bills, short-term goals, and long-term investing. A more complex household may need more buckets.

The rule is straightforward: money with a name is harder to misuse.

6. Save Unexpected Income Too

Windfalls disappear quickly when they are not assigned in advance.

Unexpected income can include bonuses, tax refunds, gifts, commissions, overtime, freelance payments, business profits, inheritance, rebates, refunds, or one-time sales of unused items. Because this money feels separate from ordinary income, people often treat it as permission to spend. The result is predictable: the windfall creates a brief sense of abundance and leaves little long-term trace.

A better approach is to create a windfall rule before the money arrives.

For example, a household might save or invest 50 percent of every bonus, use 30 percent for debt repayment, and spend 20 percent freely. Another might direct all tax refunds to emergency savings until a target is reached. A freelancer might put a fixed percentage of every large payment into taxes, savings, and retirement before using the remainder.

The exact formula is personal. The important point is precommitment. When the rule exists before the money arrives, emotion has less power. The household does not need to decide in the excitement of receiving extra cash.

Windfalls can accelerate financial progress because they are not already built into the monthly budget. A bonus can complete an emergency fund. A tax refund can eliminate a credit card balance. A gift can start an investment account. A commission check can fund a certification. A business profit distribution can become capital rather than consumption.

That said, it is reasonable to enjoy part of unexpected income if the household’s financial foundation allows it. A savings system that never permits enjoyment may become emotionally unsustainable. The key is to reward yourself from a planned portion, not from the entire windfall.

Unexpected income should not create unexpected lifestyle inflation. It should create unexpected progress.

7. Build Systems, Not Motivation

Motivation is a spark. Systems are the engine.

A person may feel motivated after reading a finance book, watching an inspiring video, paying off a debt, or seeing a savings goal become possible. But motivation fades. Systems keep acting when emotion changes.

A savings system includes automatic transfers, separate accounts, clear goals, spending alerts, monthly reviews, direct payroll deposits, employer retirement contributions, scheduled debt payments, and rules for windfalls. These structures reduce the number of decisions required. They make saving the path of least resistance.

This idea is central to modern behavioral finance. People often make better decisions when the environment is designed to support those decisions. Automatic enrollment, automatic escalation, default contribution rates, and payroll deduction all use system design to improve saving behavior. Recent discussions of retirement plan design also show that automatic features help but must be protected from leakage, job transitions, and inadequate default rates. Vanguard research on job transitions, for example, has noted that automatic enrollment does not always create long-lasting saving habits when workers change jobs and contribution rates reset or assets are cashed out.

This is a crucial lesson: systems must be maintained.

Automation can get a person started, but it should not become autopilot neglect. If you change jobs, re-enroll in retirement plans. If income rises, increase contributions. If expenses change, adjust transfers. If emergency savings are used, rebuild them. If a bank account changes, confirm that automatic transfers still work.

Systems are not designed to replace awareness. They are designed to reduce friction.

A strong savings system should answer four questions: how much is saved, when it is saved, where it goes, and what it is for. If those questions are answered clearly, saving becomes less dependent on mood.

People often say they need more discipline. In many cases, they need better architecture.

8. Track Progress Monthly

Monthly tracking gives savings a feedback loop.

Without tracking, financial progress can feel vague. A person may be saving but not know whether they are moving fast enough. They may feel behind when they are actually improving. Or they may feel secure while hidden problems are growing. A monthly review replaces guesswork with information.

A good monthly review does not need to be complicated. Check account balances. Review spending. Confirm savings transfers. Track debt balances. Compare progress with goals. Identify upcoming irregular expenses. Note any emotional spending patterns. Adjust the next month if necessary.

Monthly tracking is frequent enough to catch problems early but not so frequent that every small fluctuation becomes stressful. Daily checking can encourage anxiety, especially for investment accounts. Annual review may be too infrequent for households trying to build new habits. Monthly review is a practical middle ground.

Progress should be measured in several ways. Emergency fund balance. Savings rate. Debt reduction. Net worth. Retirement contributions. Investment contributions. Cash reserved for annual expenses. Number of months of essential expenses covered. These metrics tell a fuller story than income alone.

Tracking also creates motivation of a healthier kind. Seeing progress can reinforce behavior. Watching a debt balance fall or an emergency fund grow gives the household evidence that sacrifice is producing results. This is especially important in the early stage when compounding has not yet become visible.

But tracking should not become self-punishment. Some months will be difficult. Emergencies happen. Income may fluctuate. A household may need to use savings for a legitimate purpose. The monthly review is not a trial. It is a steering wheel.

What gets tracked becomes easier to improve because it becomes harder to ignore.

9. Keep Lifestyle Simple

A simple lifestyle is not necessarily a cheap lifestyle. It is an intentional lifestyle.

Keeping lifestyle simple means resisting unnecessary complexity, obligation, and status pressure. It means choosing expenses that match values rather than copying peers, influencers, colleagues, or neighbors. It means avoiding the habit of upgrading everything just because income rises.

Lifestyle complexity is expensive. Larger homes require more maintenance, furniture, utilities, insurance, and taxes. Expensive cars bring higher payments, insurance, repairs, and depreciation. Premium memberships, subscriptions, schools, holidays, hobbies, and social circles can create recurring expectations. Each upgrade may be affordable alone, but together they can consume the surplus needed for saving and investing.

A simple lifestyle creates flexibility. Lower fixed costs make it easier to save, handle emergencies, change jobs, start a business, take parental leave, recover from income loss, or invest during downturns. Flexibility is a form of wealth because it expands choices.

This does not mean everyone should pursue extreme frugality. Excessive cost-cutting can harm health, relationships, education, career growth, and quality of life. A person should spend on what genuinely matters. The problem is not spending; it is unconscious escalation.

The most powerful moment to keep lifestyle simple is after income increases. If income rises and the household keeps major expenses stable, the savings rate can increase quickly. If income rises and every category expands, the household may remain just as financially stressed at a higher income level.

A useful question is: what parts of my lifestyle produce lasting value, and what parts merely maintain an image?

Simplicity is not about looking poor. It is about refusing to let appearances consume the money that could buy freedom.

10. Reward Discipline Carefully

Financial discipline is easier to sustain when it includes planned enjoyment.

A savings plan that permits no pleasure can become brittle. People are not machines. If every dollar is assigned only to duty, resentment may build. Eventually, the person may rebel against the plan through impulsive spending.

Careful rewards solve this problem. A reward acknowledges progress without undermining it. It might be a modest meal out after reaching a savings milestone, a planned purchase from a discretionary fund, a weekend trip already saved for, or a small celebration after paying off a debt.

The word “carefully” matters. A reward should not erase the progress it celebrates. Paying off $1,000 of debt and then financing a $1,500 luxury purchase is not a reward; it is reversal. Saving for three months and then raiding the emergency fund for a status item weakens the system. A good reward is affordable, planned, and proportionate.

Rewards can also be non-financial. Time off, a low-cost experience, a personal ritual, a progress chart, or sharing the milestone with someone supportive can reinforce discipline without large spending.

Behaviorally, rewards help because they make long-term goals feel more immediate. Saving for retirement may feel distant. Building an emergency fund may feel responsible but not exciting. Small milestones create intermediate satisfaction.

The household can create a reward schedule. When the emergency fund reaches the first target, celebrate modestly. When credit card debt falls below a threshold, celebrate. When a retirement contribution rate increases, celebrate. When a monthly review is completed for six months, celebrate.

Financial discipline should feel serious, not joyless. The goal is to build a life worth living, not merely an account balance worth admiring.

11. Save During Good Seasons

Good financial seasons are not permanent, which is why they should be used wisely.

A good season may include stable employment, rising income, bonuses, strong business sales, low expenses, lower family obligations, health, or a favorable economy. During these periods, it is tempting to assume the current condition will continue. Spending rises. Savings targets are postponed. Debt feels manageable. Risk feels smaller.

But financial life moves in cycles. Jobs change. Clients leave. Business slows. Health changes. Children are born. Parents need support. Repairs happen. Economies weaken. Interest rates rise. Prices increase. The household that saved during good seasons is better prepared for difficult ones.

Saving during good seasons is not pessimism. It is seasonal wisdom. Farmers store after harvest because they understand that harvest is not every day. Households should think similarly. When income is strong, build reserves. Pay down expensive debt. Increase investments. Fund annual expenses. Strengthen insurance. Prepare for known future costs.

This rule is especially important for people with variable income: freelancers, business owners, commission-based workers, seasonal workers, creators, contractors, and investors. A high-income month should not be treated as the new normal until it is proven durable. Variable earners may need larger cash reserves and more conservative spending rules.

One practical method is to base lifestyle on average or conservative income rather than peak income. Extra income then flows into savings, taxes, debt reduction, or investment. This prevents strong months from creating obligations that weak months cannot support.

The Federal Reserve’s 2026 SHED savings data continues to focus on emergency savings and unexpected expenses, underscoring how important liquid reserves remain for household resilience.

Good seasons are opportunities to reduce the damage of bad seasons before they arrive.

12. Think Long Term Always

Long-term thinking gives saving its purpose.

Without a long-term view, saving can feel like restriction. With a long-term view, saving becomes the purchase of future options. It can fund freedom from high-interest debt, career flexibility, homeownership, education, business capital, retirement, generosity, health choices, family stability, and peace of mind.

Long-term thinking also prevents emotional overreaction. A person who understands their goals can distinguish between a true emergency and a temporary desire. They can decide whether extra money should go to savings, debt, investing, or planned spending. They can tolerate slow progress because they understand the direction.

Long-term thinking is also essential because savings alone may not be enough for every goal. Emergency funds and short-term goals should generally remain liquid and relatively safe. But long-term goals often require investing to outpace inflation and grow purchasing power. Holding too much cash for decades can expose wealth to inflation risk. The right balance depends on time horizon, risk tolerance, and purpose.

This is where many savings discussions need nuance. Saving is the foundation, but investing is often the growth engine. A person may first build emergency savings, then pay down high-interest debt, then invest consistently for long-term goals. The order can vary, but the distinction matters. Cash protects short-term stability. Investments pursue long-term growth.

Long-term thinking also helps households avoid all-or-nothing decisions. If the emergency fund is not complete, begin where possible. If retirement feels far away, start small. If debt is large, create a plan. If income is low, focus on both savings habits and earning power. The long-term thinker does not demand perfection before progress.

Wealth is built when today’s money is connected to tomorrow’s life.

When Saving Should Come Before Investing

Saving and investing are related, but they are not the same.

Saving is usually for safety and near-term needs. Investing is usually for growth and long-term goals. A financially resilient household needs both, but the order matters.

Saving should generally come first when a household has no emergency buffer, unstable income, essential expenses at risk, upcoming short-term obligations, or high uncertainty. Investing money that may be needed next month can create danger because markets can fall at the wrong time. A person forced to sell investments during a downturn may turn a temporary decline into a permanent loss.

A starter emergency fund can be built before aggressive investing. Once the household has a basic buffer, it may divide surplus between debt repayment, expanded emergency savings, retirement contributions, and other goals. The exact balance depends on interest rates, employer retirement matches, tax benefits, income stability, and risk tolerance.

High-interest debt complicates the decision. Paying down expensive debt may produce a more reliable improvement than holding large amounts of excess cash or investing aggressively. A household carrying credit card debt at a high interest rate should think carefully before building cash far beyond an emergency buffer while the debt compounds against them.

The practical sequence often looks like this: stabilize essentials, build a small emergency fund, capture any valuable employer retirement match if available, attack high-interest debt, expand emergency savings, then increase long-term investing. This sequence can be adjusted, but it reflects the need to protect both short-term survival and long-term growth.

Savings make investing sustainable because they prevent life from interrupting the investment plan.

How Much Should You Save?

There is no universal savings rate that fits every household.

A single person with stable income and low expenses may save aggressively. A family with childcare costs, medical expenses, and housing pressure may struggle to save much at all. A high earner with lifestyle inflation may have more room than they admit. A low-income worker may need income growth or public support before savings goals become realistic.

The right savings rate depends on income, cost of living, debt, dependents, age, retirement goals, job stability, health, and existing assets. Common recommendations can be useful starting points, but they should not become moral judgments.

For emergency savings, many financial planners suggest three to six months of essential expenses. This is a guideline, not a rule. Some households need less; others need more. A dual-income household with stable jobs may need less than a single-income household with children and a mortgage. A freelancer may need more than a salaried employee. A person with health risks or family obligations may need more liquidity.

For retirement, contribution targets vary by country and pension system. In the United States, Fidelity often references a 15 percent retirement savings benchmark, including employer contributions, while acknowledging that people may need to work up to it gradually. Other systems and households may require different targets.

The best approach is to begin with what is possible, then increase over time. A low starting rate is not failure if it becomes the foundation for higher savings later. The danger is waiting until the perfect rate is affordable and saving nothing in the meantime.

Save something. Automate it. Increase it. Protect it. Then align it with your actual goals.

Saving With Irregular Income

Irregular income requires a different savings system.

Freelancers, business owners, commission earners, contractors, creators, and seasonal workers often cannot rely on the same paycheck every month. This makes traditional budgeting harder. A strong month can create false confidence. A weak month can create panic.

The first rule for irregular income is to separate business or income inflows from personal spending. When money arrives, it should be divided into taxes, business expenses, emergency reserves, personal income, debt repayment, and savings. Treating every deposit as spendable income is dangerous.

The second rule is to build a larger buffer. Variable earners often need more than three months of essential expenses because income gaps can be longer and less predictable. They may also need separate tax reserves and business reserves.

The third rule is to pay yourself a stable salary where possible. Instead of spending based on the best month, draw a consistent amount from the income account. Surplus from strong months stays in reserves. This creates stability even when revenue fluctuates.

The fourth rule is to save aggressively during peak seasons. Irregular earners should treat high-income periods as harvest periods, not lifestyle permission. Strong months fund weak months.

The freedom of irregular income comes with the responsibility of irregular risk. Savings are the bridge between the two.

The Inflation Problem: Why Cash Alone Is Not Enough

Savings protect against short-term emergencies, but cash has limits.

Inflation reduces purchasing power over time. Money sitting in cash may be stable in nominal terms but weaker in real terms if prices rise. This is why long-term goals often require investing rather than holding everything in savings accounts.

The key is matching money to time horizon. Short-term money should prioritize safety and liquidity. Emergency funds, near-term purchases, taxes, and upcoming bills should generally not be exposed to major market volatility. Long-term money, such as retirement savings decades away, often needs growth assets to preserve and increase purchasing power.

This does not mean every household should rush into risky investments. Investing requires understanding risk, diversification, fees, taxes, and time horizon. But it does mean that saving and investing should work together. Savings create stability. Investments create long-term growth potential.

A household that saves but never invests may become secure in the short run but underprepared in the long run. A household that invests without savings may be forced to sell during emergencies. The two systems need each other.

Cash is a shield. Investments are an engine. A strong financial life usually needs both.

Why These Rules Work

The 12 savings rules work because they address human behavior rather than pretending humans are perfectly rational.

Automation reduces decision fatigue. Payday saving avoids leftover-money failure. Gradual increases reduce resistance. Emotional withdrawal rules protect reserves. Separate accounts use mental accounting constructively. Windfall rules prevent sudden money from disappearing. Systems reduce reliance on motivation. Monthly tracking creates feedback. Simple lifestyles preserve surplus. Careful rewards sustain morale. Saving during good seasons builds resilience. Long-term thinking gives every habit a reason.

These rules also work because they create a direction for income. Without direction, income often flows toward the most immediate desire or obligation. With direction, income flows toward security, ownership, and choice.

But the rules must be adapted. A household facing food insecurity needs stability before aggressive saving. A household with high-interest debt may prioritize debt repayment after a starter emergency fund. A household with excess cash and long-term goals may need investing. A household with irregular income needs larger reserves. A household with dependents needs stronger protection.

Good savings advice should be practical, not rigid.

Final Thought: Saving Is How Income Becomes Freedom

Saving money is not only about accumulating cash. It is about changing the relationship between today’s income and tomorrow’s choices.

Automate savings immediately. Save every payday first. Increase savings gradually. Avoid touching savings emotionally. Create separate savings accounts. Save unexpected income. Build systems, not motivation. Track progress monthly. Keep lifestyle simple. Reward discipline carefully. Save during good seasons. Think long term always.

Each rule is simple. Together, they create a financial architecture that can withstand stress, support opportunity, and turn income into lasting strength.

The most important shift is from effort to design. Do not rely on feeling motivated every month. Build a system that saves before you spend, separates money by purpose, protects reserves from emotion, and grows stronger as income rises.

Savings do not solve every financial problem. Income, housing costs, health, family responsibilities, economic conditions, and debt all matter. But savings remain one of the most powerful controllable tools in personal finance. They reduce dependence on borrowing. They create room to think. They support investing. They allow people to survive difficult seasons and use good seasons wisely.

Wealth becomes easier when saving stops being an occasional act and becomes the default direction of money.

The first saved dollar may not look like freedom. But repeated long enough, protected carefully enough, and invested wisely enough, savings can become exactly that.