The Billionaire Thinking Myth: What Wealthy People Actually Do Differently

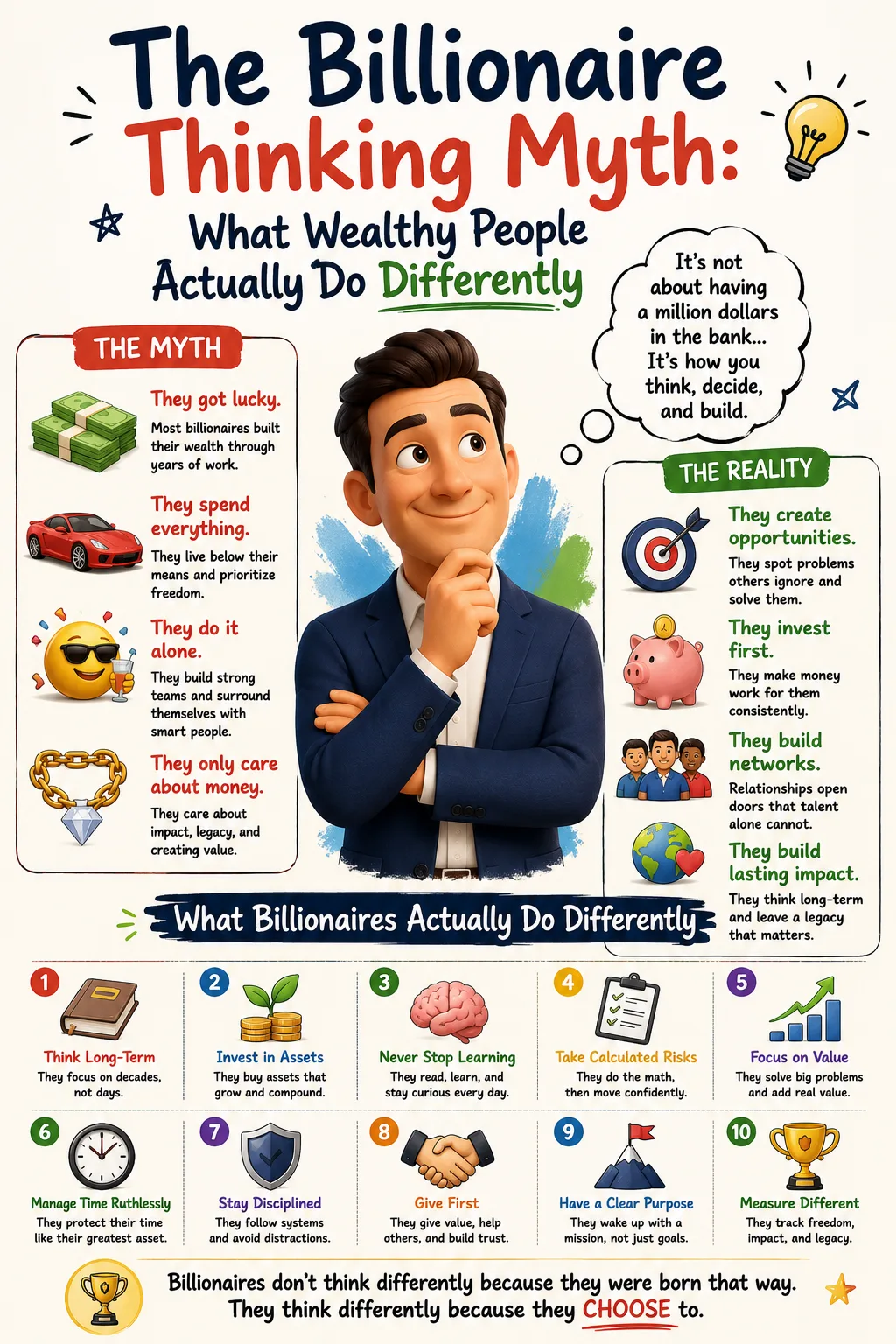

The phrase “billionaire thinking” is seductive because it suggests wealth begins in the mind. Change the way you think, the promise seems to say, and money will follow. Think bigger. Own assets. Play the long game. Build a legacy. The ideas sound polished, powerful, and simple enough to fit on a book page, a social media post, or a framed office print.

There is truth inside some of these ideas. Wealth does begin with certain mental habits: patience, discipline, curiosity, ambition, emotional control, and the ability to think beyond immediate consumption. Yet there is also danger in turning financial success into slogans. No one becomes wealthy because they repeated the right phrases. No household escapes financial fragility through motivation alone. No investor builds durable capital without savings, ownership, risk management, time, and judgment.

The useful question is not whether “billionaire thinking” sounds inspiring. The useful question is which parts of it can be translated into practical financial behavior.

Seven common principles appear again and again in wealth-building discussions: think bigger, focus on value, own assets, play long-term games, protect your reputation, learn constantly, and build a legacy. They are not guaranteed rules for becoming wealthy. They are not formulas. They do not erase the role of opportunity, education, family background, geography, luck, tax systems, market cycles, or social networks. But when interpreted carefully, they can become a powerful framework for personal finance and wealth building.

The key is to separate inspiration from execution. Inspiration may start movement. Execution builds wealth.

Why “Billionaire Thinking” Appeals to So Many People

People are drawn to billionaire thinking because extreme wealth feels mysterious. Most people understand wages. They know what it means to trade hours for income. They know what it means to receive a paycheck, pay bills, save what is left, and hope the future becomes more secure. But billionaires operate on a different financial scale. Their wealth often comes from ownership, equity appreciation, businesses, intellectual property, real estate, marketable securities, private companies, or financial structures that are far removed from ordinary household budgeting.

Because the scale is unusual, people search for unusual explanations. They look for secret habits, daily routines, mental models, morning schedules, reading lists, and productivity systems. Some of these observations are useful. Many wealthy people are disciplined. Many are long-term thinkers. Many are skilled at spotting value. Many understand leverage. Many continue learning. But the mental habit alone is not the asset. The asset is the business, stock, property, brand, patent, fund, platform, or contractual right that produces economic value.

This distinction matters. A person can “think rich” and remain broke if they never save, never invest, never acquire skills, never manage risk, and never own anything that grows. Another person may never use motivational language but still build wealth through consistent saving, diversified investing, careful career decisions, business ownership, and patient compounding.

Mindset matters because it shapes behavior. It does not replace behavior.

Rule One: Think Bigger

“Think bigger” is one of the most common wealth slogans. It is also one of the easiest to misunderstand. Thinking bigger does not mean fantasizing about luxury. It does not mean ignoring constraints. It does not mean quitting a job without a plan, borrowing recklessly, or confusing confidence with competence.

At its best, thinking bigger means refusing to let today’s circumstances define the outer limit of tomorrow’s possibilities. It means asking better questions. Instead of asking, “How can I survive until payday?” a person begins asking, “How can I increase my earning power?” Instead of asking, “Can I afford this monthly payment?” they ask, “Will this purchase improve or weaken my financial position?” Instead of asking, “How do I get a raise?” they ask, “What problems can I solve that are valuable enough to increase my income significantly?”

Big thinking is useful when it expands the field of action. A worker who thinks only in terms of small raises may never consider acquiring a high-value skill, moving to a stronger market, starting a side business, negotiating equity, buying income-producing assets, or building a professional network. A small-business owner who thinks only in terms of daily sales may never build systems, hire capable people, improve margins, develop recurring revenue, or create a brand that can scale.

But big thinking becomes dangerous when it detaches from reality. Financial history is full of people who thought big and failed because they ignored cash flow, debt, market demand, skill gaps, taxes, legal obligations, competition, and timing. Ambition is not strategy. Optimism is not underwriting. Vision is not execution.

The practical version of thinking bigger is strategic ambition. It combines aspiration with math. It asks: What larger financial outcome do I want? What skills, assets, systems, relationships, and time horizon would make that outcome possible? What risks could destroy the plan? What must be true for this to work?

For a young professional, thinking bigger may mean choosing a career path based on long-term earning power rather than immediate comfort. For a family, it may mean building a savings rate high enough to buy assets consistently. For an entrepreneur, it may mean designing a business that is not fully dependent on the owner’s personal labor. For an investor, it may mean moving from speculation to ownership of diversified productive assets.

The lesson is not to dream without limits. The lesson is to stop making financial decisions from a permanently small frame.

The Financial Application of Thinking Bigger

A small financial frame often focuses on reducing discomfort. A large financial frame focuses on increasing capability. Both have a place. Cutting unnecessary spending matters. Avoiding high-interest debt matters. Living within one’s means matters. But wealth is rarely built by expense control alone. At some point, the plan must include higher income, higher savings, and ownership of assets that can grow beyond the owner’s direct labor.

Thinking bigger may begin with one uncomfortable realization: income is not fixed forever. Many people treat income as something that happens to them. They earn what their employer pays, spend what life demands, and save what remains. Wealth builders tend to be more active. They ask how income can be improved through skill, negotiation, credentials, relocation, entrepreneurship, sales ability, leadership, specialization, or ownership.

This does not mean everyone should become an entrepreneur. Entrepreneurship is risky and often less glamorous than it appears. Many people build significant wealth as employees by choosing high-value fields, investing consistently, avoiding lifestyle inflation, and negotiating intelligently. Thinking bigger is not about copying billionaires. It is about refusing to manage money as though the only variable under your control is spending.

Rule Two: Focus on Value

“Focus on value” sounds simple, but it is one of the deepest principles in economics and wealth building. Money flows toward perceived value. Employers pay for valuable labor. Customers pay for valuable products and services. Investors pay for ownership in valuable assets. Markets reward companies that solve problems profitably. Professional reputations grow when people create value for others.

Value is not the same as effort. This is difficult but essential. A person can work hard on something the market does not reward. A business can spend years developing a product customers do not want. An employee can be busy all day without doing work that affects revenue, risk, efficiency, customer retention, or strategic outcomes. Wealth rewards value delivered, not exhaustion performed.

To focus on value, ask what problem is being solved, who cares about the solution, how urgent the problem is, how much money is connected to the problem, and how many alternatives exist. A surgeon, software engineer, skilled salesperson, logistics expert, tax adviser, electrician, designer, business owner, or investor may all create value in different ways. The market does not pay equally for all forms of value because scarcity, demand, risk, scale, and replaceability differ.

For personal finance, focusing on value changes how people think about work. Instead of asking only, “What job do I want?” they ask, “What valuable skill can I develop?” Instead of asking, “How can I look productive?” they ask, “What measurable outcome can I improve?” Instead of asking, “How can I make money quickly?” they ask, “What can I build that people will continue paying for?”

In business, value is the difference between revenue and noise. A company that creates genuine value solves a real problem at a price customers accept while managing costs well enough to remain profitable. Many businesses fail because they confuse attention with value. Popularity may help, but it is not enough. A product can go viral and still lose money. A brand can be admired and still fail if the economics do not work.

In investing, value has a specific meaning, but the broader principle still applies. An investor is not buying a ticker symbol. They are buying a claim on future cash flows, assets, earnings, dividends, rents, interest, or appreciation. The price paid matters. The quality of the asset matters. The durability of the income matters. The risk matters.

“Value attracts wealth” is partly true, but incomplete. Value must be created, communicated, captured, protected, and scaled. Many people create value but do not capture enough of it. A talented employee may create millions in value for an employer while receiving only a salary. That may still be a good trade if the salary is strong and risk is low. But ownership changes the equation. Owners can capture upside when value grows.

Rule Three: Own Assets

Of the seven principles, “own assets” is the most directly connected to wealth building. Most large fortunes are built through ownership. Not simply income. Ownership.

An asset is something that can produce future economic benefit. Productive assets may include shares of businesses, rental properties, private companies, intellectual property, farmland, bonds, royalties, equity compensation, or other claims on income and value. Not every asset is equally attractive. Not every asset is safe. Not every asset is appropriate for every person. But the general principle holds: people who own productive assets participate in growth beyond their labor.

A paycheck pays for work already performed. An asset can pay because capital is working. A salary may stop when the worker stops. A well-chosen asset may continue producing income or appreciation. This is the ownership advantage.

The modern economy rewards ownership powerfully. Employees may receive wages, but shareholders receive the residual value after expenses, reinvestment, and growth. Property owners may receive rent and appreciation. Business owners may benefit from profits, sale value, tax planning opportunities, and control. Investors in broad markets may participate in the growth of many companies at once.

This does not mean ownership is easy. Assets carry risk. Stocks fall. Businesses fail. Tenants leave. Properties need repairs. Bonds can lose value. Private investments can become illiquid. Concentrated ownership can create enormous gains or devastating losses. The point is not to own anything blindly. The point is to understand that wealth usually requires converting income into ownership.

For most households, the path begins simply. Spend less than you earn. Keep emergency savings. Avoid high-interest debt. Invest consistently in diversified assets. Increase contributions as income rises. Use tax-advantaged accounts where available. Reinvest returns. Stay patient. Over time, the household balance sheet begins to shift. More of its future depends on assets, less on labor alone.

Ownership also changes behavior. A consumer asks, “Can I buy this?” An owner asks, “Will this help me acquire more assets?” A consumer sees money as purchasing power. An owner sees money as seed capital. A consumer may measure success by lifestyle. An owner measures success by increasing productive capacity.

The difference can be quiet. Two people may earn the same income for twenty years. One spends most of it on depreciating goods, status purchases, and debt payments. The other directs a meaningful share into diversified investments, a business, or property. At first, their lifestyles may look similar. Later, their balance sheets may look entirely different.

The Difference Between Assets and Appearances

One of the great traps of modern personal finance is confusing visible wealth with actual wealth. Luxury cars, designer clothes, expensive vacations, and large homes may signal high spending, not high net worth. Some people can afford these things easily. Others buy them by sacrificing future security.

Assets are often boring from the outside. A retirement account is not flashy. A diversified index fund does not impress dinner guests. A paid-off rental property may look ordinary. A profitable small business may not go viral. An emergency fund has no glamour. Yet these are the building blocks of financial independence.

Appearances consume capital. Assets preserve and multiply capital. The wealthy may enjoy luxury, but wealth is not created by luxury. It is created by ownership, cash flow, appreciation, and disciplined allocation.

This is why “own assets” is more than a rule. It is a worldview. Every surplus dollar can either be spent, stored, or invested. Spending may improve life, and there is nothing wrong with enjoying money responsibly. But money that is always spent never becomes capital. Wealth begins when some portion of income is consistently converted into ownership.

Rule Four: Play Long-Term Games

Long-term thinking is one of the most reliable differences between wealth builders and wealth chasers. Wealth chasers want quick results. Wealth builders understand compounding.

Compounding is often explained through investment returns, but it applies more broadly. Skills compound. Relationships compound. Reputation compounds. Knowledge compounds. Business systems compound. Health habits compound. Poor decisions compound too. Debt compounds. Neglect compounds. Bad reputations compound. Lifestyle inflation compounds.

Playing long-term games means choosing activities where patience improves the odds. A diversified investment portfolio held for decades is a long-term game. A career built on rare and valuable skills is a long-term game. A business with recurring customers is a long-term game. A reputation for reliability is a long-term game. A family culture of financial literacy is a long-term game.

Short-term games are not always bad. People need income now. Businesses need quarterly cash flow. Investors must manage liquidity. Families must handle emergencies. The problem arises when every decision is optimized for immediate gratification. The person who always chooses now over later struggles to build anything durable.

In investing, long-term games require emotional discipline. Markets rise and fall. News cycles provoke fear. Social media rewards urgency. Speculation looks exciting when prices are rising. Panic feels rational when prices are falling. Long-term investors must resist the pressure to react constantly.

Patience does not mean passivity. A long-term investor still reviews asset allocation, risk, fees, taxes, and goals. A business owner still adapts. A professional still learns new skills. Long-term thinking is not doing nothing. It is acting in ways that allow compounding to work.

One of the hardest parts of long-term wealth building is that the early years can feel unimpressive. The first investment contributions may seem small. The first business systems may feel clumsy. The first professional skills may not command premium pay. The first reputation gains may be invisible. Compounding rewards consistency after the foundation is built.

People often quit before the compounding curve becomes meaningful. They change strategies too often. They chase trends. They compare their early stage to someone else’s mature result. They mistake slow progress for no progress. Long-term games require faith in process before the outcome becomes obvious.

Rule Five: Protect Your Reputation

Reputation is an intangible asset. It does not appear on a personal balance sheet, but it affects income, opportunity, trust, access, and resilience. A strong reputation can open doors that credentials alone cannot. A damaged reputation can close doors even when talent remains.

In business, reputation lowers friction. People prefer to work with those who keep promises, communicate clearly, solve problems, respect confidentiality, and act ethically under pressure. Trust reduces transaction costs. It makes deals easier, partnerships stronger, referrals more likely, and forgiveness more available when mistakes occur.

In careers, reputation compounds through repeated behavior. The person who consistently delivers high-quality work becomes known. The person who is honest about limitations becomes trusted. The person who takes responsibility becomes valuable. The person who blames others, exaggerates, misses deadlines, or plays political games may win small moments but lose long-term credibility.

Protecting reputation does not mean avoiding all risk or pleasing everyone. It means understanding that trust is capital. It takes years to build and moments to damage. Many financial opportunities come through people: investors, employers, clients, partners, mentors, lenders, advisers, and customers. If people do not trust you, your opportunity set shrinks.

The wealth connection is practical. A trusted professional may receive promotions, referrals, equity opportunities, client introductions, board invitations, speaking engagements, or partnership offers. A trusted business may retain customers and attract better employees. A trusted borrower may access capital on better terms. A trusted family member may be chosen to manage assets or lead a business.

Reputation also protects during downturns. When markets weaken, businesses struggle, or mistakes happen, people with strong reputations often receive more support. Creditors may negotiate. Clients may stay. Partners may help. Employees may remain loyal. Reputation cannot eliminate hardship, but it can create a margin of goodwill.

The practical rule is clear: do not trade reputation for short-term gain. Do not deceive customers to boost revenue. Do not hide risks from investors. Do not exploit employees. Do not misuse family trust. Do not make promises you cannot keep. Do not attach your name to ventures you do not understand. Money lost can sometimes be rebuilt. Trust lost may not return.

Rule Six: Learn Constantly

Learning is one of the few advantages available to almost everyone, though not equally. Access to education, time, mentors, and resources varies. Still, the habit of learning remains central to financial progress because economies change. Skills lose value. Industries evolve. Technology alters work. Tax rules shift. Investment products multiply. Consumer traps become more sophisticated.

Continuous learning improves earning power and decision quality. A person who learns valuable skills can become more productive. A person who understands finance can avoid obvious mistakes. A person who studies markets can become less vulnerable to hype. A person who learns negotiation can increase income. A person who learns tax basics can ask better questions. A person who learns estate planning concepts can protect family members from confusion.

Learning constantly does not mean consuming random information all day. Information is abundant. Wisdom is scarce. The goal is not to know everything. The goal is to learn what improves judgment and action.

Financial learning should begin with fundamentals: budgeting, saving, debt, interest, compounding, inflation, diversification, taxes, insurance, retirement accounts, estate documents, and risk. These basics are not exciting, but they prevent expensive mistakes. Only after the foundation is strong should most people spend time on complex strategies.

Professional learning should focus on skills the market values. Communication, sales, technical expertise, leadership, data analysis, financial literacy, project management, coding, design, operations, legal knowledge, healthcare expertise, trade skills, and entrepreneurship can all increase earning power depending on the field. The best skill investments are those that improve the ability to solve costly problems.

Investment learning should produce humility. The more a person studies markets seriously, the more they understand uncertainty. This humility is protective. It discourages overconfidence, concentration in fashionable assets, market timing, and blind trust in charismatic promoters.

Learning also reduces fear. People fear what they do not understand. A person who understands market volatility is less likely to panic during downturns. A person who understands insurance is less likely to buy inappropriate coverage. A person who understands estate planning is less likely to delay important documents. Knowledge turns vague anxiety into specific action.

The Difference Between Learning and Consuming

Modern financial media creates the illusion of learning. A person can watch endless videos, read daily market predictions, follow influencers, listen to podcasts, and still make poor decisions. Consumption becomes entertainment when it does not change behavior.

Real learning produces evidence. It shows up in a higher savings rate, a better investment plan, a stronger career strategy, cleaner insurance coverage, updated beneficiaries, reduced debt, improved negotiation, clearer documents, or better business economics. If information does not improve decisions, it is noise.

A disciplined learner asks three questions: What did I learn? How does it apply to my life? What action should change because of it?

This protects against the endless search for secrets. Most wealth building does not require secrets. It requires doing important things consistently for a long time.

Rule Seven: Build a Legacy

Legacy is often misunderstood as something that begins after wealth is already large. In reality, legacy begins with the way money is earned, used, discussed, and transferred. It includes family values, education, generosity, ownership habits, estate planning, philanthropy, business culture, and the example set for the next generation.

Building a legacy does not require billionaire status. A parent who teaches children to avoid destructive debt is building a legacy. A grandparent who funds education is building a legacy. A business owner who treats employees well is building a legacy. A professional who mentors younger workers is building a legacy. A household that creates a clear estate plan is building a legacy. A person who gives intentionally is building a legacy.

Legacy thinking changes financial priorities. It asks what should remain after consumption. This does not mean hoarding money or sacrificing all present enjoyment. It means recognizing that wealth can serve purposes beyond personal comfort.

Estate planning is the technical side of legacy. It turns intentions into instructions. A will, trust, beneficiary designation, power of attorney, healthcare directive, and asset inventory may not feel inspiring, but they are acts of care. They reduce confusion. They protect vulnerable people. They preserve family relationships. They allow wealth to move with purpose.

Family communication is the emotional side of legacy. Money transferred without values can be wasted. Money transferred without explanation can create resentment. Money transferred through unclear documents can divide families. A strong legacy includes conversations about responsibility, opportunity, stewardship, generosity, and expectations.

Charitable giving can also be part of legacy. Some families give during life so they can see the impact. Others give through estate plans. Some create donor-advised funds, charitable trusts, foundations, scholarships, or direct community support. The best charitable strategies align money with values rather than tax benefits alone.

Legacy should not be reduced to inheritance. The greatest legacy may be capability. Teaching the next generation how money works can matter more than leaving money alone. Financial literacy, work ethic, emotional discipline, and ownership habits can outlast a single transfer.

The Hidden Eighth Rule: Avoid Ruin

Any serious wealth framework needs an eighth rule: avoid ruin. Ambition, value creation, ownership, patience, reputation, learning, and legacy all fail if one catastrophic decision destroys the foundation.

Ruin can come from excessive debt, uninsured risk, legal problems, fraud, addiction, speculation, concentration, poor partners, tax neglect, lifestyle inflation, health crises, or family conflict. The wealthy are not immune. Some fortunes disappear because the owner confused past success with permanent invincibility.

Avoiding ruin is not pessimism. It is survival strategy. It means keeping emergency reserves. It means avoiding debt that cannot be serviced under stress. It means diversifying. It means using insurance where appropriate. It means reading contracts. It means separating personal and business finances. It means avoiding investments that require everything to go right. It means not risking essential capital for nonessential gain.

The first rule of compounding is to stay in the game. A person who earns moderate returns for decades may outperform someone who makes spectacular gains and then loses everything. Wealth building rewards endurance.

How Ordinary Households Can Apply These Principles

The billionaire framing can make wealth principles feel distant. Most people are not building global companies or managing enormous portfolios. Yet the underlying behaviors can be applied at ordinary income levels.

Think bigger by increasing earning power and setting financial goals beyond survival. Focus on value by becoming better at solving problems that employers, clients, or customers care about. Own assets by turning part of every paycheck into investments or business equity where appropriate. Play long-term games by resisting speculation and allowing compounding to work. Protect reputation by becoming trustworthy in every financial and professional relationship. Learn constantly by improving skills and financial judgment. Build a legacy by creating documents, teaching values, and using money intentionally.

These actions do not guarantee extreme wealth. But they can improve financial security, resilience, and opportunity. That is the point. The goal for most people should not be to imitate billionaires. It should be to build a life where money creates freedom rather than pressure.

A household earning a middle income can still build meaningful wealth if it saves consistently, avoids bad debt, invests in diversified assets, increases income over time, protects against major risks, and plans for transfer. A high-income household can still end up fragile if it spends everything, borrows heavily, speculates recklessly, ignores taxes, and fails to plan. Income helps. Behavior determines how much income becomes wealth.

What These Rules Get Right

The seven rules are useful because they point away from consumption and toward creation. They encourage ambition, service, ownership, patience, integrity, education, and responsibility. These are better principles than instant gratification, status spending, short-term speculation, or financial passivity.

They also remind readers that wealth is not only a technical subject. Spreadsheets matter, but so do habits. Asset allocation matters, but so does emotional discipline. Tax strategy matters, but so does reputation. Estate planning matters, but so does family communication. Financial success is a mixture of math, behavior, judgment, and time.

The rules are strongest when treated as prompts. Think bigger: Where am I setting my goals too low? Focus on value: What problem am I solving? Own assets: How much of my income becomes ownership? Play long-term games: What am I building that can compound? Protect reputation: Where must I choose trust over short-term gain? Learn constantly: What knowledge would improve my decisions? Build a legacy: What should my wealth make possible for others?

These questions can produce real change.

What These Rules Leave Out

The rules become misleading when presented as universal laws. Not everyone starts from the same position. Family wealth, education, country, health, discrimination, social networks, economic cycles, and luck all influence outcomes. Some people work hard and still face structural barriers. Some people take risks and lose because timing turns against them. Some inherit advantages they did not create.

A responsible wealth philosophy acknowledges both agency and reality. Individuals can make better decisions, but personal decisions operate within broader systems. Good advice should empower without blaming people for every financial hardship. It should encourage action without pretending success is fully controllable.

The rules also leave out risk management. Many motivational frameworks celebrate boldness but ignore downside. Wealth is not built only by seeking upside. It is protected by managing downside. The person who avoids ruin has more chances to benefit from opportunity.

Finally, the rules can overemphasize mindset while underemphasizing mechanics. To build wealth, people need concrete systems: budgets, automatic transfers, diversified portfolios, retirement contributions, debt repayment plans, insurance reviews, estate documents, tax planning, and income strategies. Thinking matters most when it becomes structure.

A Better Version of the Seven Rules

A more financially grounded version of the seven rules would read differently.

Think bigger means build a plan that expands income, ownership, and opportunity over time. Focus on value means solve problems that people or markets are willing to pay for. Own assets means convert income into productive capital consistently. Play long-term games means allow compounding to work while managing risk. Protect your reputation means treat trust as an economic asset. Learn constantly means improve skills and judgment in ways that change decisions. Build a legacy means use wealth to create continuity, opportunity, and responsibility beyond yourself.

This version is less glamorous, but more useful. It does not promise billionaire status. It offers a durable way to think about money.

The Practical Wealth Plan Behind the Mindset

To translate these principles into action, start with a personal balance sheet. List assets and liabilities. Know what you own and what you owe. Many people avoid this exercise because it can be uncomfortable. But clarity is the beginning of control.

Next, examine cash flow. How much income comes in? How much leaves? Which expenses are fixed? Which are discretionary? Which payments build assets? Which payments support past consumption? Wealth grows when the gap between income and spending is directed toward productive uses.

Then build financial defenses. Create an emergency fund. Reduce high-interest debt. Maintain appropriate insurance. Protect income. Keep essential documents organized. Avoid investments you do not understand. Make sure one financial setback cannot destroy the household.

After defense comes accumulation. Invest consistently in diversified assets suited to your goals, time horizon, and risk tolerance. Use retirement accounts or tax-efficient structures where available. Increase contributions with raises. Reinvest returns. Avoid unnecessary trading. Keep fees reasonable. Review periodically.

Then improve earning power. Identify skills that can increase income. Seek roles where performance is rewarded. Build a network based on trust and competence. Negotiate when appropriate. Consider business ownership or side income if it fits your skills and risk capacity.

Finally, plan for transfer. Update beneficiaries. Create a will. Consider powers of attorney and healthcare directives. Evaluate whether a trust is useful. Keep an asset inventory. Discuss key intentions with trusted people. Legacy is not built at the end. It is built through preparation.

The Real Meaning of Billionaire Thinking

The best interpretation of billionaire thinking is not that everyone should chase billionaire status. Extreme wealth is rare, and the pursuit of it can distort priorities if it becomes the only measure of success. A person can be financially successful without becoming famous, owning a global company, or appearing on a rich list.

The real meaning is that wealth builders tend to think in terms of assets, systems, time, trust, and value. They ask how money can work beyond labor. They understand that reputation has economic power. They treat learning as an advantage. They know that compounding rewards patience. They recognize that wealth without purpose can become empty or destructive.

For ordinary investors, professionals, families, and entrepreneurs, these ideas are most valuable when scaled to real life. The goal is not to mimic the external life of billionaires. The goal is to adopt the useful internal disciplines of wealth creation while rejecting hype, shortcuts, and vanity.

Think bigger, but stay grounded. Focus on value, but learn how to capture it. Own assets, but understand risk. Play long-term games, but do not ignore present obligations. Protect your reputation, but do not confuse approval with integrity. Learn constantly, but turn knowledge into action. Build a legacy, but begin with the people and responsibilities already in front of you.

Wealth is not created by slogans. It is created by repeated decisions that move money from consumption to ownership, from reaction to strategy, from short-term desire to long-term capability. The mindset matters because it shapes those decisions. The results come from what the mindset causes you to do.

That is the difference between inspirational thinking and financial wisdom.