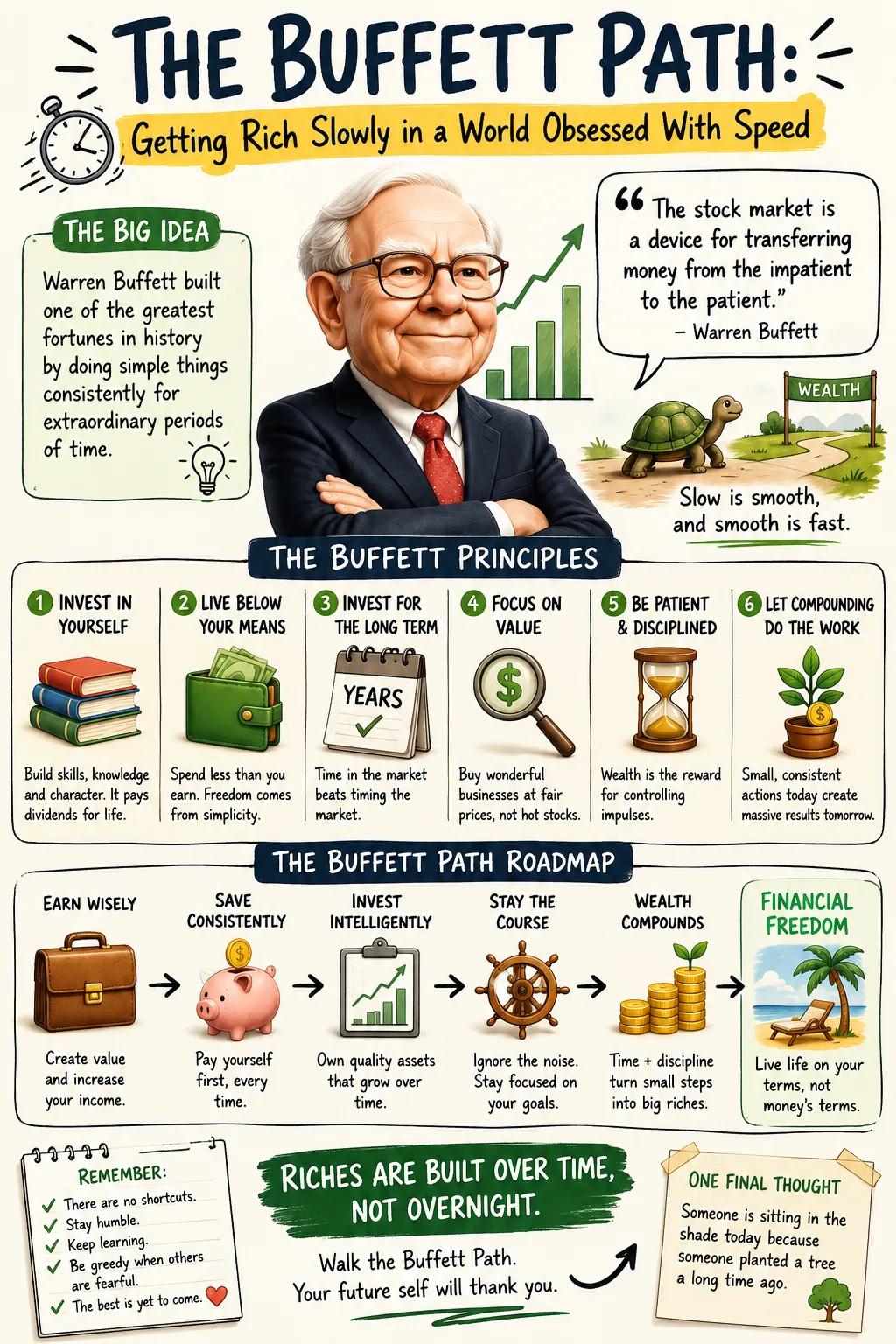

The Buffett Path: Getting Rich Slowly in a World Obsessed With Speed

Warren Buffett’s advice on getting rich is often misunderstood because it sounds too simple. Save more than you spend. Invest in productive assets. Avoid foolish debt. Read constantly. Stay patient. Do not panic when markets fall. Do not chase what you do not understand. Let compounding work for decades.

None of this sounds like a secret. It does not resemble the language of speculation, leverage, sudden riches, or market timing. Buffett’s philosophy is not built around finding a magical stock tip before everyone else. It is built around behavior. His central insight is that wealth is rarely created by a single brilliant move. It is usually built by a series of rational decisions repeated for a very long time.

That is why Buffett’s path to wealth feels almost unfashionable. It asks people to slow down in a financial culture that rewards urgency. It asks investors to think like owners when the market encourages them to behave like gamblers. It asks households to protect cash flow, avoid destructive liabilities, and invest in assets that can produce value long after the original decision has been made.

Buffett did not become one of the world’s most admired investors by trying to get rich quickly. He became wealthy because he understood the mathematics of compounding, the psychology of markets, and the economic power of owning productive businesses. His fortune is not merely the result of high returns. It is the result of high returns sustained over extraordinary time.

The lesson is not that the average person can copy Buffett’s portfolio or reproduce Berkshire Hathaway’s history. They cannot. Buffett has had unusual skill, unusual temperament, unusual access to deals, and an unusually long investing career. The useful lesson is deeper: the principles behind his success can improve how ordinary people earn, save, invest, borrow, and make financial decisions.

The First Rule: Invest in Yourself Before You Invest in Anything Else

Buffett has repeatedly said that the best investment a person can make is in themselves. This idea sits at the foundation of his wealth philosophy because every financial plan begins with human capital. Before a person owns stocks, real estate, a business, or bonds, they own their ability to earn, learn, adapt, communicate, and make decisions.

Human capital is the invisible asset most people underestimate. It does not appear on a household balance sheet, yet it often determines everything else on that balance sheet. A person with valuable skills can earn more, recover from setbacks faster, identify better opportunities, negotiate more effectively, and avoid being trapped by one employer, one industry, or one income stream.

Buffett has often emphasized communication as one of the highest-return personal investments. That may surprise people who assume investing success is only about mathematics. But money moves through relationships. Careers are shaped by trust. Businesses are built by persuasion. Leadership depends on clarity. A person who can explain ideas, write clearly, speak confidently, and understand others has an advantage that compounds across decades.

This is one of the most practical parts of Buffett’s advice because it applies before a person has significant capital. A young worker who cannot yet invest large sums can still increase future earning power. Learning accounting, sales, writing, coding, management, negotiation, financial literacy, or industry-specific technical skills can raise income for years. The earlier those skills are acquired, the longer they can produce returns.

Investing in yourself also protects against financial fragility. Markets can decline. Companies can restructure. Industries can be disrupted. But a person who keeps learning is less dependent on any single economic environment. Buffett’s reading habit is not separate from his investing record; it is part of it. He has spent much of his life absorbing annual reports, business histories, newspapers, financial statements, and industry information because better inputs lead to better judgment.

The practical application is clear. Before chasing complex investments, build the asset that makes all other investing possible. Increase your earning capacity. Improve your judgment. Learn how businesses work. Understand debt, taxes, inflation, risk, and incentives. Develop a reputation for reliability. These are not soft ideas. They are economic assets.

Start Early Because Time Is the Investor’s Greatest Advantage

Buffett bought his first stock at age 11 and later joked that he started too late. The humor contains a serious lesson. The earlier money begins compounding, the less pressure an investor needs to place on heroic returns.

Compounding is often described too casually. People hear that money grows over time and assume they understand it. But compounding is not ordinary growth. It is growth that feeds on itself. Investment returns generate future returns. Those future returns generate still more returns. Over short periods, the difference may look modest. Over decades, the difference can become enormous.

The U.S. Securities and Exchange Commission’s Investor.gov explains compound interest as growth on both the original principal and the interest already earned, and its educational materials emphasize that starting early can have major long-term benefits. This is the same principle that sits beneath Buffett’s fortune. The mathematics rewards time, consistency, and reinvestment.

Consider two investors. One begins investing at 25. The other waits until 40. The first investor does not merely have 15 extra years of contributions. They have 15 extra years of compounding. By retirement age, the gap can be dramatic even if both investors earn the same annual return. The early investor’s money has had more time to double, redouble, and multiply.

This is why delayed investing is expensive. The cost is not only the money that was not invested. It is the future growth that money could have produced. A dollar invested in youth can become far more powerful than a dollar invested later because it has more time to participate in the compounding process.

Buffett’s life illustrates the strange shape of compounding. Most of his wealth accumulated later in life, not because he suddenly discovered investing, but because the base being compounded became enormous. This is how compounding works. The early years may feel slow. The later years can feel explosive. The curve is not a straight line. It bends upward.

For ordinary investors, the lesson is not to wait until conditions feel perfect. Many people postpone investing because they think they need more knowledge, more income, or a better market. Education matters, but perfection is not required to begin sensible long-term investing. A diversified, low-cost, disciplined approach started early can be more powerful than an elaborate strategy started too late.

Live Below Your Means So Capital Has Somewhere to Come From

Buffett’s personal frugality has become part of his public legend. He has lived in the same Omaha home since 1958, long after he could have afforded almost any residence in the world. The point is not that everyone must imitate his lifestyle. The point is that wealth requires surplus.

No investing strategy can overcome a permanently negative cash flow. A person who spends everything they earn has no capital to compound. A household that increases spending every time income rises can look prosperous while remaining financially fragile. Buffett’s philosophy begins with the gap between income and expenses. That gap is the engine of wealth.

Living below your means is often misunderstood as deprivation. In Buffett’s framework, it is freedom. It gives a person choices. It creates investable capital. It reduces dependence on debt. It allows patience during career transitions, recessions, emergencies, and market downturns. It turns income into ownership.

The modern economy makes this difficult. Consumer culture encourages people to convert rising income into visible consumption: larger homes, newer cars, upgraded devices, expensive subscriptions, luxury travel, status purchases, and lifestyle inflation. The danger is not enjoyment itself. The danger is allowing consumption to absorb every raise, bonus, and windfall.

Buffett’s example cuts against that pattern. He has often distinguished between price and value, and that distinction applies to personal spending as much as investing. A purchase may be affordable and still be unwise. A luxury may bring pleasure, but if it prevents investment, its long-term cost is higher than the receipt suggests.

Investor.gov’s introductory materials encourage people to make a plan or budget, prioritize long-term saving and investing goals, automate contributions, and live within their means. That advice may sound basic, but Buffett’s life shows that basics executed for decades can beat sophisticated plans executed inconsistently.

The practical question is not, “Can I buy this?” It is, “What will this decision do to my future options?” Spending is not only about today’s enjoyment. It is also about tomorrow’s ownership. Every dollar has a job. It can be consumed, saved, invested, donated, or wasted. Wealth builders become more intentional about assigning those jobs.

Buy Productive Assets, Not Financial Illusions

Buffett’s wealth philosophy centers on owning assets that produce economic value. He prefers businesses, stocks representing ownership in businesses, and other productive assets capable of generating cash flows over time. This is one of the clearest distinctions between building wealth and appearing wealthy.

A productive asset creates or supports future income. A strong business sells goods or services at a profit. A rental property can produce rent. A farm can produce crops. A bond can produce interest. A stock can represent ownership in a company that earns money, reinvests, pays dividends, or increases intrinsic value.

A liability, by contrast, consumes future income. Some liabilities are necessary or useful when handled carefully, such as a reasonable mortgage or a loan used to acquire productive skills. But many liabilities exist only to finance consumption. High-interest consumer debt is especially dangerous because it compounds against the borrower.

This is where Buffett’s thinking becomes extremely practical. To get rich, a person must gradually shift from being primarily a consumer of other people’s assets to being an owner of assets themselves. The worker who spends every paycheck remains dependent on labor income alone. The worker who consistently buys productive assets slowly builds a second economic engine.

This does not require glamour. In fact, many productive assets are boring. A broad stock index fund, a retirement account, a profitable small business, a paid-down rental property, or equity in a durable company may not provide the emotional excitement of speculation. But wealth is not built by excitement. It is built by ownership.

Buffett’s genius has been his ability to look at stocks not as flashing prices but as pieces of businesses. This mental shift matters. A stock chart can tempt an investor to ask, “Will this go up next week?” A business owner asks better questions. Does the company have durable demand? Does it earn attractive returns on capital? Is management honest and capable? Can it raise prices? Does it carry too much debt? Is the price reasonable relative to future cash flows?

For most individuals, the most realistic way to apply this principle is not to analyze hundreds of companies like Buffett. It is to consistently buy diversified, low-cost ownership in productive assets while avoiding speculative overconcentration. The SEC describes index funds as mutual funds or exchange-traded funds that seek to track the returns of a market index, such as the S&P 500 or broader market indexes. That structure gives ordinary investors a simple way to own a diversified basket of businesses rather than betting everything on a few predictions.

Understand Intrinsic Value Before You Trust Market Price

One of Buffett’s most important concepts is intrinsic value. Market price is what someone is willing to pay today. Intrinsic value is the estimated economic value of an asset based on its future cash-generating ability. The two are not always the same.

This difference is the foundation of value investing. Markets are powerful, but they are not perfectly calm. Prices move because of earnings, interest rates, inflation expectations, fear, greed, liquidity, headlines, forced selling, index flows, and changing narratives. Sometimes prices reflect business value reasonably well. Sometimes they do not.

Buffett’s mentor Benjamin Graham famously taught that the market is a voting machine in the short run and a weighing machine in the long run. Buffett absorbed that lesson and built on it. He does not believe investors should ignore price. He believes they should understand what price represents. Paying too much for a wonderful asset can still lead to poor returns. Paying a sensible price for a wonderful business can allow time and compounding to work.

Berkshire Hathaway’s shareholder letters remain one of the primary sources for Buffett’s thinking, and Berkshire maintains an archive of those annual letters for shareholders and interested readers. Across those letters, Buffett repeatedly returns to the idea that investors should evaluate businesses rather than react mechanically to market movements.

Intrinsic value is not a precise number. It is an estimate. That is why Buffett also emphasizes margin of safety. Because the future is uncertain and valuation requires assumptions, investors need room for error. Buying with a margin of safety means paying less than a conservative estimate of value so that mistakes, bad luck, or temporary difficulties do not destroy the investment case.

Ordinary investors can apply this idea even without becoming professional analysts. Before buying an individual stock, ask: What does this company actually do? How does it make money? Why should customers keep buying from it? What could damage its economics? How much debt does it carry? What expectations are already embedded in the price? What would have to go right for this investment to work?

If those questions cannot be answered, Buffett’s philosophy suggests restraint. Not every opportunity needs to be pursued. Avoiding bad investments is itself a form of wealth creation because losses interrupt compounding.

Stay Inside Your Circle of Competence

Buffett’s circle of competence is one of his most valuable mental models. It means investors should focus on businesses and industries they can understand and avoid pretending to know everything. The size of the circle matters less than knowing its boundaries.

This idea runs against ego. Many investors want to appear sophisticated. They want opinions on every new technology, commodity, currency, startup trend, and market theme. Buffett’s approach is more humble. He is willing to say no. He is willing to pass on opportunities that others find exciting. He is willing to wait for situations where his understanding is strong enough to act with conviction.

A circle of competence protects investors from speculation disguised as intelligence. When someone buys an asset they cannot explain, they become dependent on other people’s confidence. They may hold while the story sounds good and panic when sentiment changes. Without understanding, conviction is borrowed. Borrowed conviction tends to disappear during volatility.

This is especially relevant in markets filled with complex products, viral stock ideas, options strategies, private investments, cryptocurrencies, leveraged funds, and social-media-driven speculation. Complexity is not automatically bad, but complexity without understanding is dangerous. Buffett’s discipline is not merely choosing good investments. It is refusing unclear ones.

Staying within a circle of competence does not mean never learning new areas. Buffett has adapted over time. Berkshire’s investment universe has changed as the economy has changed. But expansion of competence requires study, not impulse. A person can widen the circle by reading, analyzing, asking better questions, and observing businesses over time.

The practical application is simple. Create two lists. The first list contains businesses, industries, and financial products you understand well enough to evaluate. The second contains areas where you are guessing. The second list is not a failure. It is a risk-control tool. Wealth is often preserved by knowing where not to play.

Think Like a Business Owner, Not a Ticker Watcher

Buffett’s favorite holding period has famously been described as forever. The phrase is often misused. It does not mean every stock should be held regardless of changing facts. It means Buffett prefers to buy businesses so good that selling is unnecessary unless the business deteriorates, the price becomes irrational, or a better use of capital appears.

This mindset changes the investor’s relationship with volatility. A ticker watcher sees a falling price and feels failure. A business owner asks whether the underlying business has changed. If a company’s long-term economics remain strong, a lower price may represent opportunity rather than danger. If the business has weakened, a lower price may be a warning rather than a bargain.

The distinction between price movement and business performance is central to Buffett’s temperament. Markets quote prices every second, but businesses create value over years. The constant availability of prices can make investors feel that every movement requires a decision. Buffett’s approach suggests the opposite. Most price movements require no action at all.

This is where long-term investing becomes psychologically difficult. It is easy to say you are long term when markets are rising. It is harder when headlines are frightening, account balances are falling, and others appear to be selling. Buffett’s advantage is not only analytical. It is emotional. He has trained himself to view market declines as part of the investment landscape rather than as emergencies.

Academic research supports caution around frequent trading. Brad Barber and Terrance Odean’s well-known study, “Trading Is Hazardous to Your Wealth,” found that individual investors who traded common stocks actively paid a significant performance penalty. This aligns with Buffett’s warning against excessive activity. The more often investors trade, the more chances they create for costs, taxes, timing errors, and emotional decisions to erode returns.

For ordinary investors, thinking like an owner means building an investment policy before emotions are tested. Decide what you own, why you own it, how much risk you can tolerate, how you will rebalance, and what circumstances would justify selling. Without a plan, the market becomes your emotional manager.

Use Index Funds When You Do Not Have Buffett’s Skill Set

One of the most useful parts of Buffett’s advice is also one of the most overlooked. He does not tell most people to become professional stock pickers. He has often recommended low-cost index funds for the average investor. That advice is humble and practical.

Buffett understands how difficult it is to beat the market after costs over long periods. Professional investors compete against each other with enormous resources, advanced data, expert teams, and constant research. Even then, many fail to outperform broad indexes consistently. The average household does not need to win that game to build wealth.

In Berkshire Hathaway’s 2013 shareholder letter, Buffett discussed instructions for his wife’s inheritance, saying the cash should be invested mostly in a very low-cost S&P 500 index fund, with the remainder in short-term government bonds. The significance is hard to overstate. One of history’s greatest stock pickers has said that for most people, simplicity is not a weakness. It is protection.

Index investing works because it aligns with several Buffett principles at once. It owns productive assets. It reduces the need for prediction. It lowers costs. It discourages overtrading. It gives investors broad diversification. It allows compounding to occur without requiring constant decisions.

This does not mean index funds are risk-free. Stocks can decline sharply. Broad markets can experience long periods of poor returns. Investors still need emergency savings, appropriate asset allocation, time horizon discipline, and the emotional ability to keep investing through downturns. But for many people, a low-cost diversified portfolio is more reliable than attempting to identify the next great company.

The key word is low-cost. Fees matter because they subtract from compounding. A small annual fee difference may appear harmless in one year but become substantial over decades. Buffett has criticized the investment industry when high fees capture too much of the return that should belong to investors. The wealth-building lesson is clear: keep more of what your assets earn.

Let Compound Interest Work Without Interrupting It

Many people understand compounding mathematically but sabotage it behaviorally. They invest, then withdraw. They start, then stop. They buy after markets rise and sell after markets fall. They change strategies every time a new trend appears. They interrupt the very process they need.

Buffett’s wealth is a monument to uninterrupted compounding. Berkshire Hathaway retained earnings, reinvested capital, acquired businesses, and allowed value to build over time. The strategy worked not because every decision was perfect, but because the broad system favored patience, reinvestment, and rational capital allocation.

For households, uninterrupted compounding requires structure. Automatic investing helps because it removes the need to decide every month. Retirement accounts help because they create friction around withdrawals. Emergency funds help because they reduce the need to sell investments during crises. Diversification helps because it lowers the risk that one mistake destroys the plan.

Compounding also requires realistic expectations. Investors who expect wealth to arrive quickly may abandon a sensible strategy before it has time to work. The early stages can feel disappointing because the account balance is small and the returns appear modest. But compounding is back-loaded. The largest gains often arrive after years of discipline.

A useful way to think about compounding is as a partnership between money and time. Money provides the base. Time provides the multiplier. Behavior protects the process. When any of the three is missing, the result weakens.

This is why Buffett’s advice can feel boring in the short run and profound in the long run. He is not trying to maximize entertainment. He is trying to maximize durable wealth. The investor’s job is not to create constant action. The job is to create conditions where compounding can continue.

Avoid Bad Debt Because It Compounds in the Wrong Direction

Buffett has repeatedly warned against high-interest consumer debt, especially credit card debt. This is the dark mirror of compounding. Investment returns compound for the owner. High-interest debt compounds against the borrower.

A person earning a reasonable investment return while paying very high credit card interest is usually running in place. The debt may grow faster than safe investments can reasonably offset. This is why paying down destructive debt can be one of the highest-return financial moves available to a household.

Not all debt is the same. A mortgage used prudently to buy a home can be different from a credit card balance used to finance lifestyle inflation. A student loan used to acquire valuable skills can be different from a personal loan used for consumption. Business debt used carefully to acquire productive assets can be different from borrowing to speculate.

Buffett’s philosophy does not require a person to fear all debt. Berkshire itself has used financing in various forms. But Buffett has always emphasized resilience, liquidity, and avoiding obligations that can force bad decisions. Debt becomes dangerous when it removes flexibility.

For individuals, debt risk is not only about interest rates. It is also about monthly cash flow. Large fixed payments reduce freedom. They make it harder to invest. They make job loss more dangerous. They create stress that can lead to short-term decisions. A person may appear successful while being financially trapped by obligations.

The practical Buffett-style rule is to be cautious with any debt that does not increase long-term earning power or ownership of productive assets. Pay particular attention to interest rates, repayment terms, and the risk of income disruption. Debt should serve the wealth plan. It should not become the plan.

Ignore Market Noise Without Ignoring Reality

Buffett’s famous line about being fearful when others are greedy and greedy when others are fearful captures his contrarian temperament. It does not mean automatically buying every falling asset or selling every rising one. It means recognizing that crowds can become emotionally extreme.

Markets are not just calculators. They are arenas of human behavior. Prices reflect expectations, but expectations can swing from euphoria to despair. When investors are greedy, they may overpay for optimistic stories. When they are fearful, they may sell valuable assets too cheaply. Buffett’s advantage has often been his ability to remain rational when others are emotionally overstimulated.

This is easier to admire than to practice. Market noise is constant. Financial news, social media, analyst opinions, economic forecasts, political headlines, and daily price movements all compete for attention. The more often investors check prices, the more opportunities they create for anxiety. Anxiety often demands action, even when action is harmful.

Ignoring market noise does not mean ignoring fundamentals. Buffett is not passive about business reality. If a company’s competitive position deteriorates, debt becomes excessive, management destroys value, or industry economics change, the facts matter. Patience is not an excuse for denial.

The discipline is to separate signal from noise. A recession may affect earnings. A technological shift may damage a business model. A regulatory change may alter an industry. Those are signals. A one-day market decline, a viral opinion, or a frightening headline may be noise unless it changes long-term value.

Investors can protect themselves by reducing unnecessary inputs. Checking a long-term portfolio several times a day does not improve long-term returns. Reading every prediction does not increase wisdom. Buffett reads deeply, but he is not reacting to every market opinion. There is a difference between information and agitation.

Read Constantly Because Judgment Compounds Too

Buffett’s reading habit is legendary. He has reportedly spent much of his workday reading for decades. This is not trivia. It is one of the least appreciated reasons for his success.

Financial judgment improves when a person studies businesses, markets, history, accounting, incentives, psychology, and human behavior. Patterns become easier to recognize. Risks become more visible. Promotional language becomes less persuasive. The investor develops a library of mental models that can be applied across situations.

Reading also slows down decision-making in a useful way. Speculation thrives on speed. Investing benefits from thought. A person who reads annual reports and studies business models is less likely to buy merely because a stock is popular. A person who studies financial history is less likely to believe that the current market cycle is entirely new.

Buffett’s reading has always been connected to practical analysis. Annual reports reveal how companies earn money, allocate capital, discuss risk, compensate executives, and describe competition. Financial statements reveal margins, debt, cash flow, and returns on capital. Business histories reveal how industries evolve. Biographies reveal character and incentives.

For ordinary investors, the goal is not to read as much as Buffett. The goal is to build a habit of deliberate learning. Read about personal finance before making large financial commitments. Read about index funds before investing retirement savings. Read about debt before borrowing. Read about business before buying individual stocks. Read about behavioral finance before assuming your emotions are harmless.

Knowledge compounds like money. Early learning improves later decisions. Later decisions shape future opportunities. The person who reads consistently for years develops an edge that may not be visible at first but becomes powerful over time.

Protect Your Reputation Because Trust Is Economic Capital

Buffett has said that it takes years to build a reputation and only minutes to ruin it. This principle belongs in a wealth article because reputation has financial value. Trust affects careers, partnerships, customers, investors, promotions, referrals, creditworthiness, and leadership opportunities.

Many people think of wealth only in terms of assets. Buffett thinks in terms of character as well. A brilliant person who cannot be trusted is financially dangerous. In business, integrity reduces transaction costs. People prefer to work with those who do what they say, communicate honestly, and act predictably under pressure.

Reputation also protects opportunity. A person known for reliability may be offered roles, partnerships, clients, or investment opportunities that others never see. A person known for dishonesty may find that doors close quietly. The market for trust is not always visible, but it is always operating.

This applies to personal finance more than many people realize. Paying obligations on time, honoring agreements, being transparent with partners, avoiding fraud, and treating money seriously all shape the financial ecosystem around a person. Wealth built through deception is unstable because it depends on concealment. Wealth built through trust can compound across relationships.

Buffett’s insistence on reputation is also a warning against short-term thinking. Many unethical choices are attempts to pull future rewards into the present. Inflate numbers. Hide risk. Mislead a customer. Break an agreement. Borrow without a plan. These actions may provide temporary advantage, but they damage the asset that takes longest to rebuild.

Be Patient, But Do Not Be Passive

Buffett’s patience is often mistaken for inactivity. In reality, his patience is active. He reads, studies, waits, evaluates, and prepares. Then, when an attractive opportunity appears, he can act decisively.

This distinction matters for ordinary investors. Patience does not mean ignoring your finances. It means avoiding unnecessary motion while continuing to improve the plan. A patient investor still saves consistently, rebalances when appropriate, reviews goals, manages risk, improves skills, and avoids destructive behavior.

Buffett has often compared investing opportunities to baseball without called strikes. Investors do not have to swing at every pitch. They can wait for situations they understand. This is a powerful idea because many financial mistakes come from the feeling that action is mandatory. Someone else is making money. A trend is moving. A stock is rising. A friend is excited. The fear of missing out becomes a substitute for analysis.

Patience creates selectivity. Selectivity improves decision quality. Decision quality protects capital. Protected capital continues compounding.

At the household level, patience also affects career and spending decisions. It may mean delaying lifestyle inflation after a raise. It may mean building an emergency fund before investing aggressively. It may mean staying invested during a bear market. It may mean declining an investment that sounds exciting but cannot be understood. It may mean giving a business or portfolio enough time to mature.

Patience is not glamorous, but it is one of the few advantages available to almost everyone. Institutions may have better data. Professionals may have more resources. Wealthy investors may have better access. But an ordinary person can still choose discipline over panic, consistency over interruption, and long-term ownership over short-term reaction.

What Buffett’s Philosophy Does Not Mean

Buffett’s ideas are powerful, but they can be misapplied. The first misunderstanding is that “hold forever” means never sell. That is not what disciplined investing requires. If the facts change, the decision may need to change. A company can lose its competitive advantage. Management can allocate capital poorly. Debt can become excessive. A price can become detached from reality. Tax considerations may matter. Personal goals can change.

The second misunderstanding is that patience alone guarantees success. It does not. Patiently holding a bad asset can be costly. Patience works best when paired with quality, valuation discipline, diversification, and sound judgment.

The third misunderstanding is that ordinary investors should copy Buffett’s stock portfolio. Berkshire’s holdings reflect Berkshire’s size, tax position, insurance operations, cash flows, regulatory filings, deal access, and investment history. A household has different goals, liquidity needs, risk tolerance, and time horizons. Copying positions without understanding them is not Buffett-style investing. It is imitation without competence.

The fourth misunderstanding is that Buffett’s success proves diversification is unnecessary. Buffett has concentrated when he understood the opportunity deeply. Most investors do not have his skill, resources, or emotional control. Diversification remains a practical defense against ignorance, bad luck, and overconfidence.

The fifth misunderstanding is that value investing means buying statistically cheap stocks. Buffett evolved beyond buying mediocre businesses at bargain prices. He became known for preferring excellent businesses at reasonable prices. Quality matters because time is the friend of a good business and the enemy of a weak one.

The Ordinary Investor’s Buffett Plan

A practical Buffett-inspired wealth plan does not need to be complicated. It begins with personal economics. Spend less than you earn. Build an emergency fund. Eliminate high-interest consumer debt. Protect your income and household against major risks. Increase earning power through skills, reputation, and learning.

Then convert surplus into ownership. For most people, this may mean automatic contributions to diversified, low-cost index funds through retirement accounts and taxable investment accounts. The goal is not to trade constantly. The goal is to own productive assets for long periods.

Asset allocation should reflect age, goals, income stability, risk tolerance, and time horizon. A young investor with decades ahead may hold more equities. A retiree may need more stability and income. Buffett’s principles support rational investing, not one-size-fits-all portfolios.

Investors who choose individual stocks should treat them as business ownership. Study the company. Understand the industry. Evaluate management. Examine financial statements. Estimate value. Demand a margin of safety. Limit position sizes to what you can emotionally and financially tolerate. Avoid buying because of hype.

Every investor should create rules for downturns before downturns arrive. Decide how much cash to hold. Decide when to rebalance. Decide how to continue contributions during market declines. Decide what would justify selling. The worst time to design an investment philosophy is during panic.

The Buffett plan also includes continuous learning. Read financial statements, shareholder letters, business books, market history, and investor education materials. Learn enough accounting to understand profits and cash flow. Learn enough psychology to recognize fear, greed, envy, and overconfidence in yourself.

Most of all, respect time. Wealth building is not a weekend project. It is a multi-decade process in which habits matter more than excitement. Buffett’s fortune shows what can happen when intelligence, discipline, and compounding remain aligned for a lifetime. Ordinary investors do not need to become Buffett to learn from him. They need to build systems that make rational behavior easier and destructive behavior harder.

The Real Secret Is Temperament

The deepest Buffett lesson is not a stock-picking formula. It is temperament. Many people know what they should do financially. Fewer people do it consistently. They know they should save, but they overspend. They know they should avoid high-interest debt, but they borrow for consumption. They know they should invest for the long term, but they panic during declines. They know they should diversify, but they chase excitement. They know they should learn, but they prefer predictions.

Buffett’s advantage is that he built a life around rationality. His environment, habits, reading, business structure, and decision rules all support long-term thinking. He does not need the market to entertain him. He does not need constant approval. He does not confuse activity with progress.

That may be the most realistic model for anyone trying to build wealth. Do not rely on willpower alone. Build systems. Automate saving. Reduce bad temptations. Keep debt manageable. Hold diversified assets. Study before acting. Surround yourself with people who value discipline. Measure progress in years, not days.

Getting rich according to Warren Buffett is not about finding a shortcut. It is about refusing shortcuts that lead away from durable wealth. It is about understanding that money grows best when attached to productive assets, protected by good behavior, and given enough time to compound.

The path is not fast. That is precisely why it works. Most people abandon slow wealth because it feels unimpressive at the beginning. Buffett embraced it. He allowed small advantages to accumulate, good decisions to stack, knowledge to deepen, reputation to strengthen, and capital to compound. Over time, the ordinary became extraordinary.

The lesson is available to anyone, even if the results will differ. Invest in yourself. Spend with intention. Avoid bad debt. Buy productive assets. Keep costs low. Think like an owner. Stay within your competence. Read constantly. Protect your reputation. Be patient. Let time do what time does best.

That is the Buffett path. Not sudden riches. Sustainable wealth.