The Patience Premium: 10 Long-Term Money Rules That Build Lasting Wealth

Wealth rarely looks dramatic while it is being built.

Most of the habits that create financial security are quiet. They do not announce themselves with luxury cars, expensive watches, or public displays of success. They often look ordinary from the outside: a payroll deduction into a retirement account, a used car kept for a few extra years, a credit card balance paid in full, a skill learned after work, an insurance policy reviewed before disaster arrives, an investment held through an uncomfortable market decline.

Short-term thinking looks more exciting. It offers quick wins, rapid upgrades, market predictions, status purchases, and the illusion that financial progress should feel immediate. Long-term thinking is different. It is patient, almost stubborn. It accepts that the most powerful financial outcomes often come from repeated decisions that seem small in isolation but become extraordinary when given enough time.

This is one reason wealthy households often appear to follow different rules from people who remain financially fragile. The difference is not always intelligence, ambition, or even income. Income matters greatly, and wealth is shaped by opportunity, labor markets, education, health, family obligations, taxes, inflation, and luck. But among the factors an individual can influence, long-term financial behavior is one of the most important.

The phrase “the wealthy follow these principles” should be handled carefully. These principles do not guarantee wealth. They are not exclusive to wealthy people. They do not erase structural inequality or make investment risk disappear. But they are widely associated with stronger financial outcomes because they align personal behavior with the way money compounds, assets grow, careers develop, and risk is managed over time.

Long-term thinking is not simply about waiting. It is about designing a life where time works on your side instead of against you. Debt can compound against you. Impulse can compound against you. Lifestyle inflation can compound against you. Neglected skills can compound against you. But savings, investments, knowledge, relationships, ownership, and discipline can compound for you.

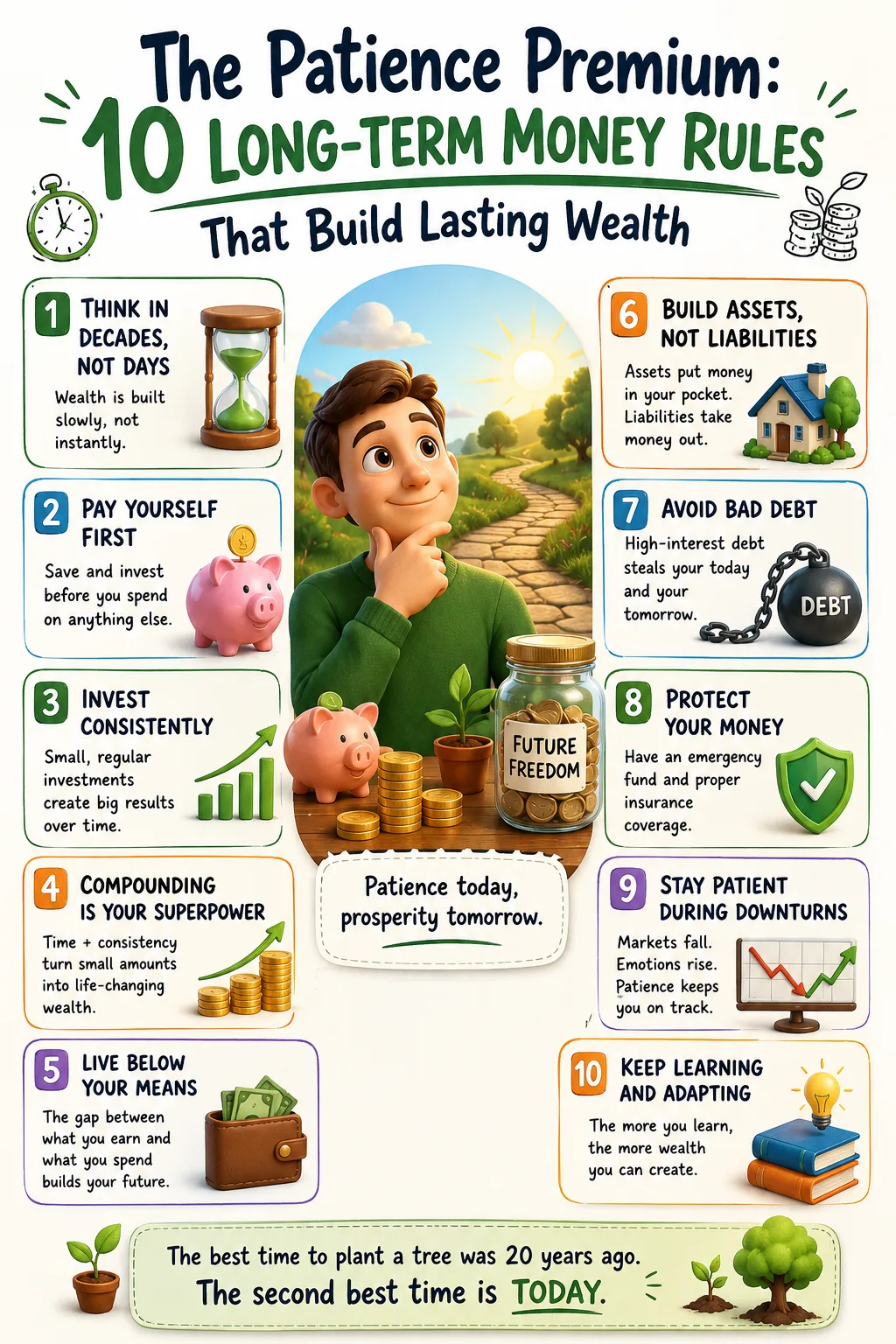

The ten rules that follow are not shortcuts. They are not motivational slogans. They are operating principles for building financial resilience over years and decades.

1. Pay Yourself First

The first rule of long-term wealth is simple: save or invest before discretionary spending has a chance to consume the money.

Many people treat saving as something that happens after life has been paid for. Income arrives, bills are paid, groceries are bought, entertainment happens, small conveniences accumulate, and whatever remains is supposed to become savings. The problem is that life has an almost unlimited ability to absorb unassigned money. If saving depends on leftovers, there may be no leftovers.

Paying yourself first reverses the order. The moment income arrives, a portion is directed toward savings, investing, debt reduction, or another priority. Spending then takes place with what remains. This changes the psychology of money. Instead of hoping discipline survives until the end of the month, the system captures progress at the beginning.

This principle works because it recognizes human behavior. People are not machines. They get tired. They rationalize purchases. They underestimate small expenses. They make decisions under stress. They respond to convenience, advertising, social pressure, and emotion. A system that depends on constant willpower is fragile. A system that automates saving is stronger.

Paying yourself first does not require starting with a large amount. A person with limited income may begin with a small automatic transfer into an emergency fund. Another person may direct a fixed percentage into a retirement account. Someone carrying high-interest debt may treat extra principal payments as a form of paying themselves first because reducing expensive debt increases future cash flow. The amount can grow as income rises, debts decline, or expenses become more controlled.

The deeper benefit is identity. When someone saves first every month, they begin to see themselves as a builder rather than merely a spender. That identity matters. Personal finance is not only arithmetic. It is also habit, self-concept, and environment. People tend to repeat behaviors that fit the story they believe about themselves. Paying yourself first reinforces the story that financial progress is non-negotiable.

There is also a defensive quality to this rule. Savings create options. An emergency fund can prevent a car repair from becoming credit card debt. A retirement contribution can create ownership in assets that may grow over time. A sinking fund can prevent annual bills from creating panic. Each saved dollar reduces dependence on future borrowing.

Many people wait to save until they earn more. Sometimes that is necessary, especially when basic costs consume nearly all income. But when income does rise, the habit of paying yourself first becomes even more important. Without it, raises are easily absorbed by lifestyle inflation. The apartment gets nicer, the car gets newer, the vacations become more expensive, and the sense of financial pressure remains.

The long-term thinker captures part of every increase before the lifestyle expands. This does not mean never enjoying income growth. It means deciding deliberately how much of a raise will improve life today and how much will buy freedom tomorrow.

The rule is not “save everything.” The rule is “save first.” That order is what gives the habit its power.

2. Invest Early and Consistently

Saving protects money. Investing gives money the opportunity to grow.

The reason early investing matters is compound growth. When investment returns remain invested, they can generate additional returns. Over long periods, this creates a powerful relationship between time and money. The earlier an investor begins, the more time each contribution has to work. Waiting does not merely delay progress; it reduces the number of years compounding can operate.

This is why a modest early investor can sometimes outperform a larger late investor. Time is not just a backdrop in investing. Time is one of the engines.

Consistency matters because markets are unpredictable in the short run. Many people want to invest at the perfect moment, but perfect moments are only obvious in hindsight. Waiting for clarity can become a costly habit. There is almost always a reason to hesitate: recessions, elections, inflation, wars, interest rates, market highs, market lows, disappointing headlines, or predictions of collapse. Long-term investors accept that uncertainty is permanent.

Regular investing reduces dependence on market timing. By contributing consistently, an investor buys through different market conditions. Sometimes prices are high. Sometimes prices are low. Sometimes the market feels optimistic. Sometimes it feels frightening. The discipline is to keep building ownership in a diversified way according to a plan rather than emotion.

This does not mean all investments are safe or that every asset will grow. Investing involves risk. Stocks can decline. Bonds can lose value when interest rates move. Real estate can become overleveraged. Businesses can fail. Concentrated bets can disappoint. A long-term approach does not eliminate risk, but it can help investors avoid one of the most common mistakes: reacting emotionally to short-term volatility.

Investing early also changes how people think about income. Without investing, income is mostly consumed. With investing, income can be converted into assets. That conversion is the heart of wealth building. A paycheck is active income. An asset is a claim on future value, income, or appreciation. Long-term wealth grows when more of today’s income is transformed into tomorrow’s ownership.

For most people, the practical foundation is not complicated. Build an emergency fund first so investments are not constantly raided for short-term needs. Eliminate or aggressively reduce high-interest debt. Then invest regularly in diversified assets aligned with goals, risk tolerance, and time horizon. For retirement, tax-advantaged accounts can be especially useful when available. For shorter-term goals, the investment approach should usually be more conservative because there is less time to recover from losses.

One of the quiet challenges of investing is boredom. Good investing is often repetitive. It can involve buying diversified funds, reinvesting dividends, increasing contributions, ignoring noise, and reviewing occasionally. This feels less exciting than chasing the latest hot asset or reacting to market drama. But excitement is not the same as effectiveness.

The long-term investor understands that wealth is often built by owning productive assets through many ordinary years, not by constantly searching for extraordinary moments.

3. Think in Decades, Not Days

Short-term thinking asks, “What is happening now?” Long-term thinking asks, “What will this become if I repeat it for ten, twenty, or thirty years?”

This shift changes nearly every financial decision.

A daily market decline looks frightening when judged in isolation. Over decades, market declines become part of the landscape investors must cross. A small monthly investment looks unimpressive today. Over a career, it can become meaningful capital. A decision to learn a valuable skill may not increase income next week. Over years, it can change a person’s earning power. A choice to avoid a high-cost loan may not feel glamorous. Over time, it prevents income from being captured by interest payments.

Thinking in decades does not mean ignoring the present. Bills must be paid now. Emergencies happen now. Health, family, and work obligations cannot always wait. The point is not to sacrifice today blindly for the future. The point is to stop letting temporary emotions dominate decisions with permanent consequences.

Behavioral finance shows that people often react strongly to recent events. A market drop feels like proof that investing is dangerous. A market rally feels like proof that risk has disappeared. A neighbor’s success creates pressure to copy. A short period of strong income can create confidence that spending can rise indefinitely. Long-term thinking slows these reactions down.

The decades mindset is especially valuable in investing. Investors who check portfolios constantly may experience more anxiety because they are exposed to every fluctuation. The more often someone looks, the more often they will see losses, even in an investment that performs well over long periods. Daily attention can create emotional pressure to act, and action is not always helpful.

Long-term thinking also applies to careers. A person choosing between job opportunities should consider not only the next paycheck but the skills, network, reputation, and future opportunities each role creates. A slightly lower-paying position that builds valuable expertise may produce better long-term results than a higher-paying role with limited growth. The same logic applies to education, entrepreneurship, and professional relationships.

In spending, the decades mindset exposes hidden costs. A car payment is not only a monthly amount; it is a claim on future income. A lifestyle upgrade is not only a reward; it may become a new baseline. A habit of carrying credit card debt is not only a temporary solution; it may become years of interest. Long-term thinking asks what each decision will demand later.

This rule also encourages patience with progress. Many people abandon good financial habits because results feel slow. The emergency fund grows slowly. Debt declines slowly. Investments fluctuate. Income growth takes time. But slow progress is still progress. The financial world rewards consistency because consistency is rare.

The long-term thinker is not indifferent to short-term pain. They simply refuse to let short-term discomfort destroy long-term advantage.

4. Avoid Bad Debt and Unnecessary Liabilities

Debt is not one thing. It can be a tool, a bridge, a burden, or a trap.

One of the most damaging financial mistakes is treating all borrowed money as equal. A mortgage used to buy an affordable home is different from a credit card balance created by lifestyle spending. A student loan for a program with strong earning potential is different from debt taken on for a credential with weak prospects. A business loan funding profitable growth is different from a personal loan used to maintain appearances.

The real issue is whether the debt improves future financial capacity or drains it.

Bad debt is usually high-cost, consumption-driven, and unsupported by a realistic repayment plan. Credit card debt is the common example because interest rates can be punishing and balances often represent past spending rather than productive investment. Payday loans, high-cost installment loans, and unnecessary personal loans can be even more damaging. They convert today’s shortage into tomorrow’s larger obligation.

Unnecessary liabilities are broader than debt. A liability is anything that requires future cash outflow. A luxury car with high insurance, maintenance, and depreciation can be a liability even if the loan payment is technically affordable. A house purchased at the edge of affordability can become a liability if it prevents saving, investing, or handling repairs. A subscription-heavy lifestyle can become a web of small liabilities. Even business overhead can become dangerous if it is added before revenue is stable.

The long-term thinker asks more than “Can I make the payment?” That question is too weak. Many financially harmful decisions can be justified by the monthly payment. The stronger questions are: “What is the total cost? What income will this debt require from me in the future? Does this purchase appreciate, generate income, improve earning power, or protect stability? What happens if my income falls?”

Productive debt can make sense when used carefully. A reasonable mortgage may help a household build housing stability and potential equity. Education financing may be worthwhile if the expected career returns are strong and the debt level is manageable. A business loan may be rational if it supports cash-flowing growth. But even productive debt becomes dangerous when the amount is too large, the interest rate is too high, or the repayment depends on optimistic assumptions.

A useful rule is to be conservative with fixed obligations. The more fixed payments a household carries, the less flexible it becomes. Flexibility is a form of wealth. It allows a person to change jobs, survive emergencies, invest during downturns, help family, or take calculated risks. Heavy debt reduces flexibility because income is already promised to lenders.

Debt management should be strategic. High-interest debt usually deserves urgent attention. Lower-interest debt may be managed alongside investing, depending on rates, risk tolerance, and goals. The goal is not always to be debt-free at any cost. The goal is to prevent debt from controlling the household’s future.

Long-term wealth is easier to build when income is not constantly pulled backward by yesterday’s spending.

5. Build Multiple Income Streams

A single income source can create stability, but it can also create vulnerability.

Many households depend almost entirely on one paycheck. As long as that paycheck continues, life works. But if the job disappears, hours are reduced, health changes, the industry weakens, or the employer restructures, the household’s financial foundation can shake quickly. Multiple income streams can reduce that dependence.

Income diversification can take many forms. A person may earn a salary, freelance on the side, build a small business, receive rental income, collect dividends or interest, earn royalties, sell digital products, consult, teach, or invest in assets that produce cash flow. Not every income stream is passive. Many require time, skill, risk, capital, or years of development. But the broader principle is sound: relying on one source of income can be risky.

That said, this rule is often oversimplified. Not everyone has the time, health, childcare support, capital, or schedule flexibility to build multiple income streams immediately. A parent working long hours may not be able to add a side business without damaging health or family life. A low-wage worker may need skill development before side income becomes realistic. A person carrying heavy debt may need stability before taking entrepreneurial risk.

Multiple income streams should not become a slogan that ignores real constraints. They should be understood as a long-term goal, not a moral judgment.

The first and most important income stream for many people is human capital: the ability to earn through skills, knowledge, experience, and reputation. Before chasing side hustles, it may be more valuable to increase the earning power of the main career. A certification, negotiation, promotion, job change, portfolio, apprenticeship, or technical skill may produce more income than a scattered set of small side projects.

Once the primary income is stable, additional streams can be built deliberately. A side business may begin as a skill-based service. Investment income may begin with small recurring contributions. Rental income may require years of saving and careful analysis. Royalties may come from creative work or intellectual property. Business ownership may begin as a small operation before becoming meaningful.

The danger is confusing income streams with distractions. A person trying five side hustles without focus may earn little and burn out. A long-term thinker looks for income streams that match skills, resources, and strategy. The goal is not to be busy. The goal is to become more financially resilient.

Investment income deserves special attention because it represents a transition from labor to ownership. At first, dividends, interest, and appreciation may seem small. Over time, as capital grows, investment income can become more meaningful. This is one of the central paths from working for money to having money work alongside you.

Multiple income streams do not guarantee wealth. They can fail. They can be taxed. They can require maintenance. They can create complexity. But when built thoughtfully, they reduce dependence on a single employer and create more pathways for financial progress.

6. Control Your Expenses

Income is powerful, but it does not automatically create wealth.

A person can earn a high salary and remain financially fragile if expenses rise to meet or exceed income. Another person with a moderate income can build meaningful wealth if they maintain a strong savings rate over time. Wealth is not determined by income alone. It is determined by the gap between what comes in and what goes out, and by what happens to that gap.

Expense control is the discipline of protecting that gap.

This does not mean living cheaply for its own sake. Extreme frugality can become exhausting and unrealistic. The goal is not to remove all pleasure from life. The goal is to spend in a way that reflects priorities rather than impulse, status pressure, or habit.

Lifestyle inflation is one of the biggest threats to long-term wealth. As income rises, spending often rises with it. A raise becomes a nicer apartment. A bonus becomes a vacation. A promotion becomes a more expensive car. Some lifestyle improvement is reasonable. Money should improve life. But if every income increase is fully consumed, the person may appear more successful while remaining financially dependent on the next paycheck.

The wealthy-looking lifestyle and the wealth-building lifestyle are often different. The first emphasizes visible consumption. The second emphasizes assets, liquidity, flexibility, and ownership. A person who spends heavily on status may look rich while having little net worth. A person who lives below their means may look ordinary while quietly accumulating assets.

Expense control begins with knowing fixed costs. Housing, transportation, insurance, debt payments, and childcare often determine whether a budget has room to breathe. Small expenses matter, but large recurring expenses shape the financial architecture. If the fixed cost structure is too heavy, every month becomes difficult.

Variable spending also needs limits. Dining out, shopping, entertainment, travel, subscriptions, hobbies, and convenience purchases can expand quickly without clear boundaries. A good budget allows these categories but assigns them numbers. The point is not to say no to everything. The point is to say yes within a plan.

Expense control also creates opportunity. Cash flow can fund emergency savings, investments, education, business ideas, travel without debt, generosity, and career flexibility. Every dollar not permanently committed to consumption remains available for choice.

There is a psychological benefit as well. People who control expenses often feel less trapped. Lower fixed obligations mean less pressure to tolerate bad jobs, unhealthy work environments, or risky financial arrangements. Financial freedom is not only about having a large portfolio. It is also about needing less to maintain stability.

The most effective expense control is values-based. Cut aggressively on what does not matter. Spend intentionally on what does. A family that values travel may drive older cars. A person who values entrepreneurship may live modestly to fund a business. A household that values education may reduce entertainment spending. This is not deprivation. It is alignment.

Long-term wealth requires a surplus. Expense control protects it.

7. Stay Patient and Disciplined

Financial discipline is easy to admire and difficult to practice.

It is easy to say you will invest for the long term when markets are rising. It is harder when account balances fall. It is easy to say you will avoid lifestyle inflation before the raise arrives. It is harder when coworkers upgrade their lives. It is easy to promise debt repayment when motivation is high. It is harder after months of slow progress.

Patience and discipline matter because financial success often requires doing sensible things long after they stop feeling exciting.

Investors face this constantly. Markets move through cycles of optimism and fear. During booms, people may feel pressure to take more risk because everyone else seems to be making money. During downturns, they may feel pressure to sell because losses feel unbearable. Both reactions can damage long-term results. The disciplined investor follows a plan rather than the crowd.

Discipline does not mean refusing to change. A plan should evolve when goals, time horizons, income, family circumstances, or risk tolerance change. But discipline does mean avoiding constant reaction to noise. There is a difference between thoughtful adjustment and emotional reversal.

Patience is also necessary in debt repayment. Paying off debt can feel slow, especially when interest has accumulated for years. The early stages may produce little visible progress. But each payment reduces future interest and increases future flexibility. The discipline is to continue even when the reward is delayed.

The same is true of career growth. Building valuable skills, reputation, and income often takes years. The long-term thinker is willing to endure periods of learning, apprenticeship, rejection, and repetition because they understand that human capital compounds. A skill learned today may create opportunities years later.

Discipline is easier when systems support it. Automatic investing, spending limits, debt repayment schedules, separate savings accounts, and regular financial reviews reduce the need for constant motivation. A disciplined life is not built by willpower alone. It is built by designing defaults that make good behavior easier.

Patience should not be confused with passivity. Waiting is not enough. A person who waits without saving, investing, learning, or managing risk is not practicing long-term thinking. They are simply delaying. Productive patience combines action with time. It plants seeds and allows them to grow.

One of the hardest parts of long-term finance is accepting that results are uneven. Investments may grow in bursts. Careers may advance suddenly after years of preparation. Businesses may struggle before gaining traction. Savings may increase slowly, then accelerate as debts are eliminated. Progress does not always arrive smoothly.

The disciplined person keeps the process alive long enough for compounding to matter.

8. Keep Learning and Adapting

Money rewards people who keep learning because the economy does not stand still.

Industries change. Technology reshapes work. Markets evolve. Tax rules shift. Investment products multiply. Fraud becomes more sophisticated. Healthcare, housing, education, and retirement systems become more complex. A financial plan that made sense ten years ago may need adjustment today.

Continuous learning increases human capital. Human capital is the set of skills, knowledge, experience, judgment, and relationships that affect earning power. For most people, especially early in life, human capital is their largest asset. Before they have a large investment portfolio, they have the ability to earn, improve, and adapt.

This makes career learning a core wealth-building strategy. A person who becomes more valuable in the labor market can increase income, improve job security, and create more options. That learning may come through formal education, certifications, apprenticeships, reading, mentorship, projects, sales skills, technical skills, management experience, communication skills, or entrepreneurship.

Financial literacy is another form of learning. Understanding interest, inflation, diversification, taxes, insurance, credit scores, investment fees, estate planning, and behavioral bias can prevent costly mistakes. A lack of financial knowledge can make people vulnerable to bad products, scams, excessive fees, and poor decisions made under pressure.

The challenge is that financial information is abundant but not always reliable. The internet offers education, but it also offers hype. Some voices sell urgency. Others promise guaranteed returns. Some confuse entertainment with advice. Long-term thinkers develop judgment about sources. They look for evidence, incentives, risk disclosures, and whether the advice fits their actual situation.

Learning also requires humility. What worked in one market cycle may not work forever. A business model can weaken. A job skill can become less valuable. An investment strategy can become overcrowded. A personal budget can become outdated after a family change. Adaptation is not failure. It is maintenance.

The most financially resilient people often combine stable principles with flexible tactics. The principles remain: live below your means, invest consistently, manage risk, avoid destructive debt, protect assets, and keep building value. The tactics may change: career moves, asset allocation, tax planning, business strategy, housing decisions, or technology tools.

Continuous learning also helps people recognize opportunity. A person who understands a changing industry may position their career before demand rises. An investor who understands basic valuation and risk may avoid obvious speculation. An entrepreneur who studies customers may build a more durable business. A household that learns about insurance and estate planning may prevent a crisis from destroying years of progress.

Wealth is not only stored money. It is also stored capability. The ability to learn, adapt, and make better decisions is one of the few assets that can travel with a person across jobs, markets, and life stages.

9. Protect Your Assets

Building wealth is only half the work. The other half is keeping it.

Many financial plans focus heavily on accumulation: earn more, save more, invest more, buy assets. But wealth that is not protected can disappear quickly. A lawsuit, medical event, uninsured loss, concentrated investment, cyber theft, business failure, disability, death, or poor estate planning can undo years of progress.

Asset protection begins with risk management. The first layer is liquidity. An emergency fund protects against temporary shocks. Without cash reserves, even a manageable setback can force a household into debt or require selling investments at a bad time. Cash may not produce high returns, but it provides stability.

The second layer is insurance. Health insurance, auto insurance, homeowners or renters insurance, disability insurance, life insurance, liability coverage, and business insurance can all play important roles depending on circumstances. Insurance is often disliked because premiums feel like money spent on something that may never happen. But that is the point. Insurance transfers risks that could be financially devastating.

The right amount of insurance depends on the household. A single person with no dependents may not need the same life insurance as a parent whose income supports children. A high-income professional may need strong disability coverage because future earnings are a major asset. A business owner may need liability protection. A homeowner may need adequate property coverage. The goal is not to buy every policy available. The goal is to protect against risks that would be difficult or impossible to absorb alone.

Diversification is another form of protection. Concentration can create wealth, especially for entrepreneurs and early investors, but it can also destroy wealth. Holding too much of one stock, relying on one property, depending on one customer, or keeping all income tied to one business can create vulnerability. Diversification spreads risk so that one failure does not ruin the entire plan.

Legal and estate planning also matter. Wills, beneficiary designations, powers of attorney, healthcare directives, trusts, business structures, and succession plans can determine how assets are handled during incapacity or after death. Many people delay estate planning because it feels uncomfortable or because they assume it is only for the very wealthy. But even modest households need clarity. Confusion during a crisis can be expensive and painful.

Cybersecurity has become part of asset protection as well. Strong passwords, multi-factor authentication, careful handling of financial information, credit monitoring, and fraud awareness can prevent losses that did not exist in the same way generations ago. As money becomes more digital, protection must become more digital too.

Asset protection is not pessimism. It is respect for uncertainty. The long-term thinker understands that wealth is built over years but can be damaged quickly. Protection keeps one bad event from becoming a financial collapse.

10. Think Legacy, Not Luxury

Luxury is about consumption. Legacy is about continuity.

This does not mean luxury is always wrong. Money can and should be used to create comfort, beauty, rest, celebration, and memorable experiences. A life devoted only to accumulation can become hollow. But when luxury becomes the main symbol of success, it can pull money away from the deeper work of building lasting security.

Legacy thinking asks a different question: “What do I want my money to make possible beyond immediate pleasure?”

For some people, legacy means family security. They want children or grandchildren to have education, housing stability, or a financial foundation. For others, legacy means philanthropy, community investment, business succession, creative work, mentorship, or institutions that outlast them. Some define legacy privately: freedom from debt, dignity in retirement, or not becoming a financial burden to loved ones.

Legacy is personal. It should not be reduced to inheritance alone. Not everyone has children. Not everyone wants to transfer wealth across generations. Some people use money to support causes, build businesses, teach, care for relatives, create art, or improve their communities. The common thread is that money is directed toward something larger than short-term display.

Luxury thinking often asks how wealth can be seen. Legacy thinking asks how wealth can serve.

This distinction matters because visible consumption can become endless. There is always a more expensive neighborhood, car, watch, trip, handbag, restaurant, or status symbol. If the goal is to prove success through consumption, the finish line keeps moving. Legacy creates a more durable standard. It focuses on impact, security, ownership, and values.

Legacy thinking can also improve everyday decisions. A person who wants to fund a child’s education may think differently about a car upgrade. A business owner who wants to create generational stability may think differently about profit distributions. A retiree who wants to support charitable causes may think differently about portfolio withdrawals. A young professional who wants future independence may think differently about lifestyle inflation.

Legacy requires planning. It may involve investing, insurance, estate documents, tax strategy, family conversations, charitable structures, business systems, or financial education for heirs. Without planning, even accumulated wealth can be lost through conflict, taxes, poor decisions, or lack of preparation.

There is also an emotional side. Many people inherit not only money habits but money beliefs. A legacy can include teaching financial literacy, modeling discipline, discussing values, and preparing the next generation to manage resources responsibly. Passing down wealth without wisdom can create fragility. Passing down wisdom, even without great wealth, can change a family’s financial trajectory.

Thinking legacy instead of luxury does not require being rich today. It begins with asking what kind of financial life is worth building. The answer may shape saving, investing, spending, giving, and planning for decades.

Why These Rules Work Together

Each rule is useful on its own, but the real power comes from the way they reinforce one another.

Paying yourself first creates savings. Investing early gives those savings time to grow. Thinking in decades keeps short-term volatility from disrupting the plan. Avoiding bad debt protects future income. Multiple income streams increase resilience. Expense control preserves the surplus needed for investing. Patience and discipline keep the process alive. Learning improves earning power and decision-making. Asset protection guards against major setbacks. Legacy thinking gives the entire system a deeper purpose.

This is how long-term financial success is usually built: not by one spectacular decision, but by a network of sensible decisions repeated for years.

The rules also protect against common financial traps. They reduce the chance that income growth will be wasted. They make it harder for lifestyle inflation to consume raises. They limit the damage of emotional investing. They prevent debt from quietly taking over cash flow. They make risk visible before disaster arrives.

Most importantly, these rules shift attention from appearance to substance. A person following them may not look wealthy at first. They may drive an ordinary car, live in a reasonable home, avoid unnecessary debt, and invest quietly. But beneath the surface, their balance sheet may be strengthening every year.

Long-term wealth often begins as invisible progress.

The Limits of Long-Term Financial Rules

These principles are powerful, but they are not magic.

They do not guarantee high investment returns. They do not prevent recessions. They do not remove medical risk, job loss, discrimination, family emergencies, or economic instability. They do not make low wages sufficient in expensive cities. They do not mean every person has the same starting line or the same opportunities.

A serious wealth-building philosophy must admit that personal finance exists inside a larger economic reality. People build wealth more easily when they have stable income, affordable housing, access to education, healthcare, safe communities, functioning markets, and fair opportunity. When those conditions are weak, even disciplined people can struggle.

But acknowledging structural reality does not make personal strategy irrelevant. It makes strategy more important. When conditions are difficult, the margin for error narrows. Good habits cannot solve every problem, but bad habits can make hard problems worse. The goal is to control what can be controlled while recognizing what cannot.

For some people, the next best financial move may be saving more. For others, it may be increasing income. For others, it may be reducing debt, changing careers, seeking benefits, moving to a lower-cost area, protecting health, or leaving a financially destructive relationship. Long-term thinking is not one-size-fits-all. It is a framework for making decisions that improve future options.

A Practical Way to Start

The best way to apply these rules is not to attempt everything at once. Start with the foundation.

First, create a clear picture of income, expenses, debts, and savings. Without visibility, long-term planning becomes guesswork. Then automate a small amount of saving or investing. The amount can increase later. What matters is building the habit.

Next, identify destructive debt. High-interest consumer debt should usually be treated as an urgent financial leak. Create a repayment plan and avoid adding new balances. At the same time, build at least a small emergency fund so every surprise does not return you to borrowing.

Then examine fixed expenses. Housing, transportation, insurance, and debt payments often determine whether the budget has room for wealth building. If these costs are too high, small cuts alone may not be enough.

After that, increase long-term investing as income allows. Use diversified investments appropriate for the goal and time horizon. Avoid reacting to every market movement. Review periodically, but do not confuse constant attention with control.

Continue building human capital. Learn skills that can increase income, improve job security, or create future options. In many lives, career growth funds the investment plan. The more valuable the skill set, the more powerful the financial system can become.

Finally, protect what you build. Maintain insurance, emergency savings, diversification, cybersecurity, and estate documents appropriate to your situation. Wealth without protection is vulnerable.

The process is not glamorous. But it is durable.

The Quiet Advantage of Long-Term Thinking

Long-term thinking gives ordinary decisions extraordinary weight.

A single saved dollar may not change a life. A habit of saving can. One investment contribution may not create wealth. Decades of contributions can. One avoided impulse purchase may not matter. A lifestyle built around intentional spending can. One skill may not transform income immediately. A career of learning can.

The wealthy are often associated with assets, ownership, and opportunity. But before assets become large, habits must become consistent. Before ownership grows, income must be directed. Before legacy is built, luxury must be put in its proper place. Before financial freedom becomes visible, discipline must operate quietly.

The patience premium is the reward for letting good decisions compound.

It is earned by saving before spending, investing before feeling ready, holding a long view when others panic, avoiding liabilities that drain the future, building income capacity, controlling expenses, staying disciplined, learning continuously, protecting assets, and using money for something larger than display.

These rules do not promise instant wealth. They offer something better: a reliable direction.

Over a lifetime, direction matters. A person does not need every decision to be perfect. They need enough decisions pointing toward ownership, resilience, and freedom. Long-term wealth is built when the daily use of money begins to serve the life a person wants decades from now.

That is the real difference between short-term money and long-term wealth. Short-term money is spent to feel successful today. Long-term wealth is built to create security, choice, and impact tomorrow.