The Cash Flow Mindset: How Robert Kiyosaki Thinks Wealth Is Built

Robert Kiyosaki did not become one of the most discussed personal finance authors because he introduced a complex investment formula. His influence came from something simpler and more disruptive: he challenged the financial script many people had been taught to follow.

That script usually sounds familiar. Go to school. Get a steady job. Work hard. Save what you can. Buy a house. Avoid debt. Contribute to retirement accounts. Hope that decades of employment and disciplined saving eventually produce security.

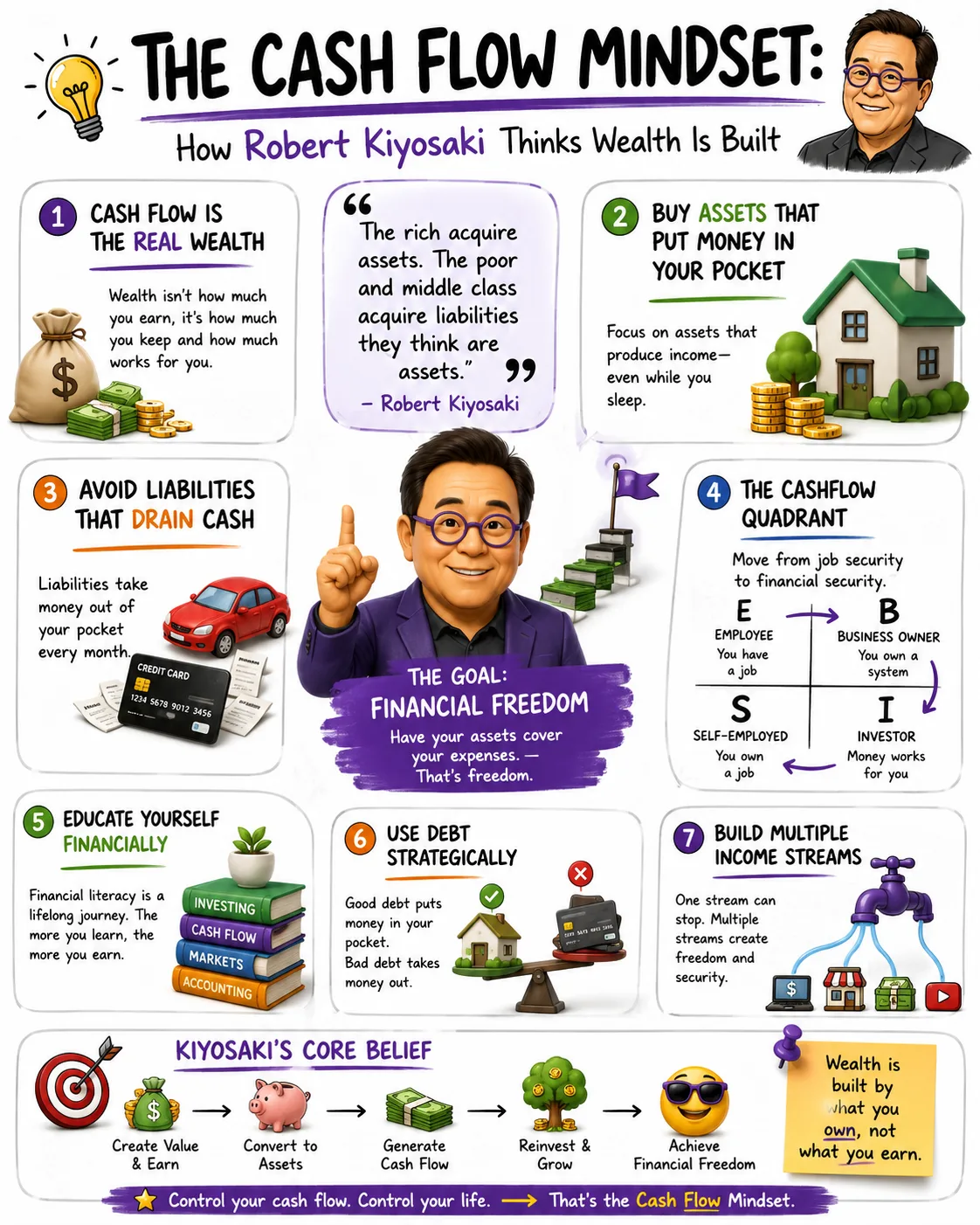

Kiyosaki’s message, popularized through Rich Dad Poor Dad and later expanded through his Cashflow Quadrant framework, questioned whether that path was enough. He argued that many people spend their lives working for money without ever learning how money works. They earn income, pay bills, buy liabilities, take on obligations, and remain dependent on employment because their financial lives are built around consumption rather than ownership.

At the center of his philosophy is a simple idea: the rich do not merely earn money; they acquire assets that produce money.

That idea has inspired millions of readers to think differently about income, investing, debt, taxes, business ownership, and financial freedom. It has also drawn criticism. Some of Kiyosaki’s definitions are deliberately simplified. Some of his views on debt and real estate can be risky if applied without skill. Some of his market forecasts and investment claims have been challenged by mainstream financial professionals. A serious reader should not treat every statement as investment doctrine.

Yet dismissing his philosophy entirely would miss why it became so influential. Kiyosaki gave ordinary people a vocabulary for thinking about wealth as a system. He taught readers to look beyond salaries and focus on ownership. He reframed financial education as a practical survival skill. He pushed people to ask whether their money was flowing toward assets or away from them through expenses.

To understand how to get rich according to Robert Kiyosaki, the key is not to search for a secret investment. It is to understand the operating system behind his thinking: buy income-producing assets, increase financial intelligence, use leverage carefully, build businesses, create passive cash flow, and reduce dependence on earned income.

The Core Idea: Wealth Is Built Through Assets, Not Income Alone

Kiyosaki’s central principle is that wealth comes from owning assets that generate income. In his teaching, the difference between the wealthy and the financially struggling is not simply how much money they make. It is what they do with the money after they earn it.

Two people can earn the same salary and end up in very different financial positions. One may use income to buy consumer goods, finance a lifestyle, upgrade cars, increase housing costs, and accumulate debt tied to consumption. The other may use income to acquire rental properties, invest in businesses, buy dividend-paying assets, build intellectual property, or purchase productive tools that generate future income.

Over time, the second person begins to own sources of cash flow. Their financial life is no longer powered only by their labor. Their assets begin to participate.

This is the foundation of Kiyosaki’s wealth philosophy. A paycheck may create income, but assets create independence. A salary requires the worker to keep showing up. A productive asset can keep producing whether the owner is present or not, though many assets still require management, expertise, and oversight.

Kiyosaki’s preferred examples often include rental real estate, businesses, royalties, intellectual property, and investments that distribute cash. What matters is not the label attached to the investment. What matters is whether it produces more money than it consumes.

That distinction is why his work focuses so heavily on cash flow. A person may look wealthy because they own expensive things, but if those things require constant payments, maintenance, taxes, interest, and insurance without producing income, they may weaken the owner’s financial position. A person may look ordinary but quietly own assets that send money into their account every month. Kiyosaki wants readers to notice the second person.

This does not mean income is irrelevant. Earned income often provides the starting capital for investment. A high salary can be a powerful tool when paired with discipline and asset acquisition. The problem arises when income becomes the ceiling of one’s financial life rather than the fuel for building something larger.

In Kiyosaki’s view, the rich use earned income to buy assets. The middle class often uses earned income to buy liabilities that appear to be assets. The poor may have too little surplus income to invest at all, making financial education and income growth especially important.

The practical lesson is direct: do not measure financial progress only by income. Measure it by the amount of productive ownership you are accumulating.

The Asset and Liability Framework

One of Kiyosaki’s best-known ideas is his simplified definition of assets and liabilities. In his framework, an asset puts money into your pocket. A liability takes money out of your pocket.

This definition is not the same as formal accounting. In accounting, an asset is a resource owned or controlled by a person or business that has economic value. A personal residence, for example, may be treated as an asset on a balance sheet because it has market value. Kiyosaki’s point is different. He is asking whether that item produces positive cash flow for the owner.

This distinction matters because many households confuse ownership with wealth creation. A large house may appreciate over time, but it may also require mortgage payments, property taxes, insurance, maintenance, repairs, utilities, and furnishing. If it does not produce income, Kiyosaki would not view it as the kind of asset that creates financial freedom. It may be valuable. It may be emotionally important. It may even become profitable if sold. But while it is owned and occupied, it can still function as a monthly cash drain.

The same logic applies to cars, boats, luxury goods, and lifestyle upgrades. They may provide comfort or status, but they usually remove money from the owner’s pocket. They do not build independent income.

Kiyosaki’s definition is useful because it forces a cash-flow question. Does this purchase make me richer each month, or does it make me poorer each month? Does it create income, or does it create obligations? Does it expand my freedom, or does it require more hours of labor to support it?

This framework can be too simple if used carelessly. Some assets do not produce immediate cash flow but can still be valuable. Broad stock market index funds, for example, may compound mainly through appreciation. A primary residence can contribute to long-term household stability even if it is not an income property. Education can increase earning power even though it is not a traditional cash-flow asset.

Still, the framework remains powerful as a behavioral tool. It teaches people to stop judging purchases by appearance and start judging them by financial behavior.

A rental property that generates income above all expenses behaves differently from a vacation home that sits empty most of the year. A small business that produces profit without constant owner labor behaves differently from a self-employed job disguised as a company. A dividend-paying portfolio behaves differently from a financed luxury car. The categories are not just emotional; they are economic.

For Kiyosaki, becoming rich begins with learning to classify money decisions correctly. Many people stay stuck because they call liabilities assets. They believe they are building wealth when they are actually building payment obligations.

Why Financial Education Comes Before Investing

Kiyosaki repeatedly argues that financial education is one of the most important differences between those who build wealth and those who remain dependent on wages. His criticism of traditional schooling is that it often prepares people to earn income but not to manage, invest, protect, or multiply it.

A person can graduate with technical expertise, earn a respectable salary, and still have little understanding of cash flow, taxes, debt, inflation, accounting, business valuation, real estate analysis, or portfolio risk. That person may be professionally educated but financially untrained.

Kiyosaki’s version of financial education is practical. It is not merely knowing financial vocabulary. It is knowing how money moves.

He encourages people to learn how to read financial statements. This matters because wealth is recorded in numbers before it is experienced in lifestyle. An income statement shows whether money is being earned or lost. A balance sheet shows what is owned and owed. A cash-flow statement shows whether money is actually available. These tools are not only for corporations. Households have financial statements too, even if they do not formally prepare them.

Consider a family earning a high income but spending nearly all of it. Their income statement may look strong, but their cash-flow reality may be fragile. If one income source disappears, the lifestyle collapses. Now consider a lower-income household that consistently buys productive assets, avoids destructive debt, and grows investment income. The second household may have less status today but a stronger financial trajectory.

Financial education also includes understanding taxes. Kiyosaki frequently emphasizes that employees, business owners, and investors are taxed differently depending on jurisdiction, income type, entity structure, deductions, depreciation rules, and local law. His broader point is that tax knowledge can affect wealth outcomes. The goal is not evasion; it is understanding the legal structure of financial life.

Real estate investors, for example, may benefit from deductions, depreciation, and financing structures that are not available in the same way to wage earners. Business owners may deduct legitimate business expenses before calculating taxable profit. Investors may face different tax treatment on qualified dividends, capital gains, rental income, or interest income. The details vary by country and change over time, so professional advice matters. But the principle remains: financial ignorance can be expensive.

Kiyosaki also wants people to understand debt. Many personal finance systems teach debt avoidance as a universal rule. Kiyosaki takes a more nuanced but riskier position. He argues that debt used to buy income-producing assets can be useful, while debt used for consumption can be destructive. To make that distinction safely, a person must understand interest rates, loan terms, coverage ratios, vacancy risk, refinancing risk, asset values, liquidity, and downside scenarios.

Without financial education, leverage becomes gambling. With education, it can become a tool, though never a risk-free one.

This is one reason Kiyosaki’s philosophy cannot be reduced to “buy real estate” or “use debt.” The deeper message is that people should not invest in what they do not understand. Financial education is the filter that separates calculated risk from reckless optimism.

The Cashflow Quadrant: Employee, Self-Employed, Business Owner, Investor

Kiyosaki’s Cashflow Quadrant is one of his most influential teaching frameworks. It divides income into four categories: Employee, Self-employed, Business owner, and Investor.

The Employee earns money by working for an organization. The Self-employed person earns money by working for themselves. The Business owner builds or owns a system that can generate income beyond their personal labor. The Investor uses money to acquire assets that produce returns.

The framework is not meant to insult employment or self-employment. Many employees build substantial wealth through high income, disciplined investing, and long-term ownership of diversified assets. Many self-employed professionals earn excellent incomes and enjoy autonomy. But Kiyosaki argues that the right side of the quadrant, business ownership and investing, offers greater leverage.

An employee sells time. A self-employed person may also sell time, even if they have more control. A business owner owns a system. An investor owns assets. The further a person moves toward systems and assets, the less their income depends solely on their personal hours.

This distinction is especially important for high earners. A doctor, attorney, consultant, designer, or contractor may earn a large income but still be trapped if every dollar depends on personal effort. When they stop working, income slows or stops. Their income may be high, but it is still active.

Kiyosaki’s question is: what are you building that can operate without your constant labor?

A true business owner creates processes, teams, products, distribution channels, intellectual property, customer relationships, and operating systems. The business may still require leadership, but it is not merely a job owned by the founder. It has value beyond the owner’s daily work.

An investor takes another step. Instead of building every system personally, the investor allocates capital into systems operated by others. That may include rental properties, public companies, private businesses, funds, lending arrangements, or partnerships. The investor’s work is analysis, capital allocation, risk management, and oversight.

The Cashflow Quadrant is useful because it helps people identify the source of their income. A person may say they want financial freedom, but if all their income comes from employment, they are vulnerable to job loss, health issues, industry disruption, and age-related earning limitations. A person with multiple income sources across the quadrant may have greater resilience.

The mistake is assuming that one quadrant is morally superior. The better interpretation is strategic. Each quadrant has strengths and weaknesses. Employment can provide stable income, benefits, training, and capital for investing. Self-employment can provide autonomy and higher upside. Business ownership can create scale and enterprise value. Investing can create passive or semi-passive income.

Kiyosaki’s philosophy encourages people to use the first two quadrants as stepping stones toward the last two. Earn actively, learn constantly, then buy or build assets that reduce dependence on active income.

Making Money Work for You

The phrase “make money work for you” is often repeated in personal finance, but Kiyosaki gives it a specific meaning. Money works for you when it is used to acquire assets that create more money.

This is different from simply saving cash. Cash savings are essential for liquidity, emergencies, and optionality. But cash sitting idle may lose purchasing power over long periods if inflation exceeds the interest earned. Kiyosaki often emphasizes the danger of relying only on saving because saved money does not necessarily multiply fast enough to create financial freedom.

His preferred approach is to turn surplus income into productive ownership. The process may begin slowly. A person saves a portion of income, studies an asset class, makes a small investment, reinvests the income, and gradually expands. Over time, each asset becomes a small worker in the financial system.

A rental property may send net income each month after expenses. A dividend portfolio may distribute cash quarterly. A business may produce profits. A book, course, patent, software product, or licensing agreement may generate royalties. A well-structured partnership may distribute income from operations.

None of these are truly effortless. “Passive income” is often oversold. Rental properties require tenant selection, repairs, financing, insurance, legal compliance, and management. Businesses require strategy, people, systems, marketing, and capital. Dividend portfolios require risk tolerance and patience. Intellectual property requires creation, distribution, and protection.

Kiyosaki’s point is not that wealth requires no work. His point is that the work should eventually create assets rather than only wages.

There is a major difference between being paid once for labor and being paid repeatedly from ownership. A salaried worker may receive income every two weeks, but the payment stops when the work stops. An author may write a book once and receive royalties for years if the book continues selling. A real estate investor may acquire a property once and receive rent for decades if the investment is managed well. A business owner may build a company that continues to generate profit even as employees handle daily operations.

This is the transition Kiyosaki wants readers to understand: from transaction income to asset income.

Transaction income pays you for an event. Asset income pays you because you own something productive. Getting rich, in his philosophy, means increasing the share of your life funded by asset income.

Why Kiyosaki Emphasizes Real Estate

Real estate occupies a central place in Kiyosaki’s wealth philosophy. He often presents it as one of the most accessible and powerful asset classes for building cash flow, using leverage, benefiting from tax rules, and creating long-term wealth.

Rental real estate can produce income in several ways. The most visible is rent. If rent exceeds mortgage payments, taxes, insurance, repairs, vacancy, management costs, and capital reserves, the property may produce positive cash flow. Over time, the property may also appreciate. Tenants may effectively help pay down the mortgage through their rent. Tax rules may allow certain deductions, depending on location and circumstances.

This combination attracts Kiyosaki because it can connect cash flow, leverage, inflation protection, and ownership. A well-bought property can produce monthly income while also increasing in equity over time. If rents rise with inflation and the mortgage is fixed, the investor may benefit from widening cash flow. If the property is financed prudently, the investor controls a larger asset than they could have purchased with cash alone.

But real estate is not automatically a good investment. Kiyosaki’s simplified examples can make property investing sound easier than it is. A property that looks profitable on paper can become a burden if the investor underestimates repairs, overestimates rent, ignores vacancies, accepts poor financing, buys in a weak location, or fails to screen tenants. A rising interest rate environment can reduce cash flow and pressure valuations. Local regulation can affect rent increases, evictions, taxes, short-term rentals, and zoning. Insurance costs can rise. Maintenance can surprise even experienced owners.

The difference between a wealth-building property and a wealth-draining property is analysis.

A serious real estate investor studies the purchase price, expected rent, operating expenses, financing terms, taxes, insurance, reserves, local employment trends, population growth, supply conditions, tenant demand, and exit options. They calculate whether the property remains viable under stress. What happens if rent is lower than expected? What happens if the property is vacant for two months? What happens if the roof fails? What happens if refinancing becomes expensive? What happens if home prices fall?

Kiyosaki’s real estate philosophy is strongest when interpreted through disciplined underwriting. It is weakest when readers assume any property bought with borrowed money is automatically an asset.

Under his own cash-flow definition, a rental property that loses money every month is not the asset he is describing. It may become profitable later through appreciation, but that is speculation unless supported by strong evidence. His framework demands that investors ask a blunt question before buying: will this property put money into my pocket after all costs?

That question can prevent expensive mistakes.

Good Debt, Bad Debt, and the Discipline of Leverage

Kiyosaki is known for distinguishing between good debt and bad debt. Bad debt finances consumption. Good debt finances assets that generate income.

Credit card balances used for lifestyle spending are a classic example of bad debt. Auto loans for expensive vehicles can also become bad debt when they finance depreciating assets that do not produce income. Personal loans used to maintain an unaffordable lifestyle weaken financial flexibility because they create payments without creating productive assets.

Good debt, in Kiyosaki’s framework, might include a mortgage used to buy a cash-flow-positive rental property, a business loan used to acquire productive equipment, or financing used to purchase an asset that produces income above the cost of debt.

The idea is financially valid in principle. Leverage can increase returns when the asset produces a return higher than the borrowing cost. But leverage also magnifies mistakes. If the asset underperforms, the debt still requires payment. If income falls, expenses rise, or asset values decline, the borrower can face losses larger than the original equity invested.

This is the part of Kiyosaki’s philosophy that requires the most caution.

Debt is not good because it is used to buy an investment. Debt is useful only when the investment is sound, the cash flow is resilient, the borrower has adequate reserves, and the downside is survivable. Many people have gone broke using debt to buy things they believed were assets.

Leverage changes the emotional experience of investing. An unleveraged investor who owns a stock portfolio may dislike volatility, but they are not usually forced to sell because of a monthly debt payment tied to the portfolio. A leveraged property investor must service debt regardless of vacancies or repairs. A business owner with loans must make payments even when sales slow. A margin investor can face forced liquidation when asset prices fall.

Kiyosaki’s language can sound aggressive because he often criticizes fear of debt. A more balanced interpretation is that investors should fear ignorance, not debt itself. Debt is a tool. In trained hands, it can accelerate asset acquisition. In untrained hands, it can destroy wealth faster than almost anything else in personal finance.

The practical discipline is to separate the purpose of the debt from the quality of the deal. Borrowing to buy a rental property is not automatically good. Borrowing to buy inventory is not automatically good. Borrowing to start a business is not automatically good. The debt becomes useful only if the underlying asset can realistically produce enough cash flow to justify the obligation.

Before using leverage, an investor should understand the interest rate, repayment schedule, collateral, guarantees, refinancing risk, break-even point, liquidity needs, and worst-case scenario. They should know how many months they can survive without income from the asset. They should know whether the asset can be sold quickly and at what discount. They should know whether a downturn would be uncomfortable or catastrophic.

Kiyosaki’s debt philosophy is not an invitation to borrow recklessly. Properly understood, it is a challenge to become financially skilled enough to distinguish productive leverage from financial self-harm.

Cash Flow Over Net Worth

Kiyosaki places unusual emphasis on cash flow rather than net worth alone. This is one of the most important features of his philosophy.

Net worth measures what you own minus what you owe. It is a useful measure of financial position. But net worth does not always tell you whether you are financially free. A person can have a high net worth on paper and still struggle with liquidity if their wealth is tied up in illiquid assets that produce little income.

Imagine someone who owns a valuable property but has little cash, no rental income, high maintenance costs, and no investment income. Their balance sheet may look strong, but their daily life may depend entirely on employment income. If the job disappears, they may be forced to sell assets under pressure.

Now imagine another person with a smaller net worth but enough rental income, dividends, business distributions, and interest income to cover living expenses. That person may have more practical freedom, even if their balance sheet is less impressive.

This is why Kiyosaki defines financial freedom as the point where passive or semi-passive income covers living expenses. Under that definition, freedom is not a net-worth number. It is a cash-flow relationship.

If monthly living expenses are $4,000 and investment income is $1,000, the person is not financially free. If investment income rises to $4,500 and is reasonably stable, the person has reached a form of independence. Their assets support their lifestyle.

This framing can be useful because it turns financial freedom into a measurable target. Instead of asking, “How much money do I need to be rich?” the person asks, “How much monthly cash flow do I need to cover my life?”

The answer depends on expenses. A household that needs $15,000 a month requires far more asset income than one that needs $4,000. Kiyosaki’s framework therefore encourages both asset building and expense awareness. Financial freedom can be reached by increasing investment income, reducing lifestyle costs, or doing both.

Still, cash flow should not be the only measure. Some investments produce low current income but strong long-term total returns. A diversified equity portfolio may create wealth through appreciation rather than high distributions. A growing business may reinvest profits instead of distributing cash. A young investor may reasonably prioritize total return over immediate income.

The best interpretation is not that net worth does not matter. It is that net worth without liquidity or income may not create freedom. Kiyosaki’s contribution is to remind readers that wealth should be judged by what it can do for your life, not only by how large it looks on paper.

Pay Yourself First

Kiyosaki also supports the principle of paying yourself first. This means setting aside money for saving and investing before discretionary spending consumes it.

Many people follow the opposite pattern. They earn income, pay bills, spend on lifestyle, and save whatever remains. The problem is that little often remains. Modern life is designed to absorb income. Housing, transportation, subscriptions, dining, travel, technology, insurance, debt payments, and social expectations can expand to match earnings.

Paying yourself first reverses the order. The first claim on income goes to future wealth. Money is directed into savings, investments, debt reduction, business capital, or asset acquisition before lifestyle spending begins.

This principle is not unique to Kiyosaki, but it fits his broader philosophy because it creates capital for buying assets. Without surplus, the asset column cannot grow. A person may understand cash flow intellectually but remain stuck if every dollar is spent.

The practical application is automation. Automatic transfers to investment accounts, emergency funds, retirement accounts, or separate asset-purchase accounts can remove the need for constant willpower. The system acts before emotion intervenes.

Paying yourself first also creates pressure to become more resourceful. If a person invests first and has less money available for discretionary spending, they must make choices. They may negotiate bills, avoid unnecessary purchases, increase income, delay gratification, or become more intentional. Kiyosaki often frames this pressure as productive because it forces financial creativity.

There is a limit. Paying yourself first should not mean ignoring essential obligations or creating financial chaos. A household needs food, housing, utilities, insurance, transportation, and debt payments. The principle works best when paired with a realistic budget and emergency reserves.

The deeper lesson is that wealth rarely happens by accident. If investment receives only leftover money, it will usually remain small. If asset acquisition becomes a non-negotiable priority, the financial trajectory changes.

Business Ownership as a Wealth Engine

Kiyosaki views business ownership as one of the major paths to wealth because a business can scale beyond the owner’s personal labor. A job pays for time. A strong business creates a system that can serve customers, employ people, generate profit, and increase in value.

The wealth potential of business ownership comes from several sources. First, a business can produce income. Second, it can grow in value as revenue, profit, brand strength, systems, and customer relationships improve. Third, it may provide tax advantages through legitimate business expenses and entity structures, depending on local law. Fourth, it can create leverage through people, technology, capital, and distribution.

A small example illustrates the difference. A self-employed web designer may earn money only when completing client projects. If they stop working, income stops. A business owner may build an agency with designers, project managers, sales systems, recurring contracts, and standardized processes. The owner may still lead the company, but income no longer depends only on their personal design hours. The company itself has value.

That is the kind of transition Kiyosaki wants people to understand. Self-employment can be a step toward freedom, but it can also become a demanding job. Business ownership requires building a machine, not merely owning a task.

Modern entrepreneurship has expanded the possibilities. Digital products, software, online education, content businesses, e-commerce brands, newsletters, licensing models, and service agencies can all become assets if they are built with systems and profitability. The internet has lowered some barriers to starting, though it has also increased competition.

Kiyosaki’s business philosophy is especially relevant because wages alone rarely create great wealth unless the income is high and the savings rate is substantial. Business ownership offers upside that employment usually does not. A founder may create something that can be sold. An owner may benefit from profit growth. A business can generate income even when the owner is not performing every task.

Yet business ownership is risky. Many small businesses fail. Owners may face inconsistent revenue, payroll obligations, competition, legal requirements, taxes, debt, operational complexity, and emotional stress. A business can consume capital for years before it produces reliable profit. It can also become a liability if it requires constant cash injections.

Kiyosaki’s framework still applies: a business is not an asset merely because it exists. It becomes an asset when it produces sustainable cash flow or has credible value to others. A struggling company that drains savings and depends entirely on the owner’s unpaid labor may be closer to a liability.

The goal is not to romanticize entrepreneurship. The goal is to understand why ownership has wealth-building power. Employees earn from participation. Owners earn from systems.

Multiple Income Streams and Financial Resilience

Kiyosaki encourages building multiple income streams because dependence on one paycheck creates vulnerability. A single income source may feel stable until it disappears. A layoff, illness, industry shift, recession, business failure, or family emergency can expose how fragile a one-source financial life can be.

Multiple income streams do not guarantee wealth, but they improve resilience when built intelligently. A household might have employment income, rental income, dividends, business income, royalties, interest income, consulting income, or partnership distributions. If one source weakens, others may help absorb the shock.

The key is quality, not quantity. Many people confuse multiple income streams with scattered side hustles. Working three low-paying jobs is not the same as building assets. Kiyosaki’s preferred income streams are tied to ownership and leverage. They are meant to reduce dependence on labor, not multiply exhaustion.

A strong income stream has several characteristics. It is understandable. It has a clear source of demand. It produces cash above expenses. It can survive reasonable stress. It does not require constant emergency attention. It fits the owner’s skills, capital, and risk tolerance.

For a beginner, the first additional income stream may be modest. It may come from dividend investments, a small digital product, a rented room, a part-time business, or a carefully chosen investment account. The amount matters less than the habit of building beyond wages.

Over time, the investor can ask a strategic question: which income streams deserve more capital, time, and attention? Not every opportunity should be pursued. Some are distractions. Some are too risky. Some do not scale. Some require expertise the person does not yet have.

Kiyosaki’s philosophy favors learning through action, but action should be paired with evaluation. If a side business teaches sales, accounting, customer service, and marketing, it may be valuable even before it generates large profit. If a rental property teaches underwriting and management while producing cash flow, it may become the foundation for a portfolio. If dividend investing teaches patience and ownership, it may build long-term discipline.

Multiple income streams are not built overnight. They are layered. Earned income funds the first assets. The first assets produce cash flow. Cash flow helps buy more assets. Knowledge improves the quality of decisions. The process compounds.

Calculated Risk and the Role of Mistakes

Kiyosaki often criticizes excessive fear. In his view, many people avoid investing because they fear losing money, but that avoidance can become its own risk. Money kept entirely outside productive assets may fail to grow. A person who never learns to invest may remain dependent on employment forever.

His answer is not blind risk-taking. It is calculated risk. That means learning enough to understand what can go wrong, investing within one’s capacity, and treating mistakes as tuition rather than identity-shattering failure.

This mindset is common among entrepreneurs and investors. Skill develops through study and experience. Reading about real estate is useful, but managing a property teaches lessons that books cannot fully capture. Studying business is useful, but selling to real customers reveals whether the market cares. Learning about stocks is useful, but living through volatility teaches emotional discipline.

The danger is using the language of education to excuse recklessness. Not every loss is productive. Some losses are avoidable. Some are too large. Some come from ignoring basic risk controls. A mistake that teaches a lesson while leaving the investor solvent may be useful. A mistake that destroys credit, savings, relationships, and future optionality may be devastating.

Calculated risk requires sizing. A beginner should not risk financial ruin to prove courage. A new investor can start small, use simulations, partner with experienced people, build reserves, study historical downturns, and avoid commitments they do not understand. The goal is to survive long enough to become skilled.

Kiyosaki’s philosophy values courage, but courage in finance should be disciplined. The best investors are not fearless. They are risk-aware. They ask what they might be missing. They prepare for bad outcomes. They preserve liquidity. They do not confuse confidence with competence.

This is especially important with leverage. A person may be right about an asset over the long term but still fail because short-term cash flow cannot support the debt. Timing, liquidity, and financing terms matter. Calculated risk means respecting the path, not only the destination.

The practical lesson is to build financial muscles gradually. Learn the vocabulary. Read financial statements. Analyze deals. Track personal cash flow. Study taxes. Understand interest. Start with manageable investments. Review mistakes. Improve. Repeat.

Where Kiyosaki Aligns With Mainstream Wealth Principles

Some of Kiyosaki’s ideas are debated, but several align with widely accepted wealth-building principles.

The first is financial literacy. Few serious financial professionals would argue against learning how money, debt, taxes, investing, and business work. Financial ignorance can lead to overspending, poor borrowing decisions, underinvestment, fraud exposure, and missed opportunities. Kiyosaki’s insistence on financial education is one of his strongest contributions.

The second is ownership. Wealth is usually built through owning appreciating or income-producing assets. Whether through public equities, private businesses, real estate, intellectual property, or diversified funds, ownership allows people to benefit from economic productivity beyond their personal labor.

The third is disciplined saving and investing. Paying yourself first, controlling lifestyle inflation, and consistently directing capital toward assets are core principles across many financial traditions.

The fourth is the importance of cash flow. Businesses fail when they run out of cash. Households become fragile when expenses exceed income. Investments become dangerous when they cannot support their obligations. Kiyosaki’s focus on cash flow is practical and valuable.

The fifth is entrepreneurship. Business ownership has created significant wealth throughout history. From small local companies to global enterprises, scalable systems can produce income and equity value far beyond wages.

These ideas are not controversial when stated carefully. The debates arise around emphasis, execution, and risk.

Where Readers Should Be Careful

Kiyosaki’s philosophy can be powerful, but readers should apply it with judgment. The first caution is diversification. Kiyosaki often emphasizes real estate, business ownership, precious metals, and entrepreneurship. These can be useful, but concentrating too heavily in one asset class can increase risk. A person with most of their wealth in leveraged local real estate may be exposed to interest rates, local employment conditions, tenant issues, regulation, and property-specific problems.

Diversified index investing, though less dramatic than real estate entrepreneurship, has strong support among many mainstream financial professionals because it spreads ownership across many companies and sectors. Kiyosaki’s readers should understand both approaches. Cash-flow assets and diversified public markets do not have to be enemies. Many investors use both.

The second caution is leverage. Debt can accelerate wealth creation, but it can also accelerate failure. The phrase “good debt” should never replace underwriting. The numbers must work. The borrower must have reserves. The downside must be survivable.

The third caution is oversimplification. Kiyosaki’s asset-liability definition is useful for behavior but not complete for accounting or planning. A primary residence, education, or growth investment may have value even if it does not produce immediate cash flow. Readers should use his framework as a lens, not as the only financial definition they ever need.

The fourth caution is speculation. Kiyosaki has made public market and economic predictions over the years, some of which have been controversial. A reader can learn from his educational frameworks without accepting every forecast. Investing should be based on evidence, valuation, risk tolerance, time horizon, and personal circumstances.

The fifth caution is suitability. Not everyone should become a landlord, entrepreneur, or leveraged investor. Some people are better suited to building wealth through high earnings, disciplined saving, diversified investing, and gradual asset accumulation. Financial freedom has multiple paths.

The strongest version of Kiyosaki’s philosophy is not a rigid formula. It is a set of questions: Am I buying assets or liabilities? Is my income dependent only on my labor? Do I understand the numbers? Is this debt productive or dangerous? Does this investment produce cash flow? Am I becoming more financially intelligent?

How to Apply Kiyosaki’s Ideas Without Becoming Reckless

A practical Kiyosaki-inspired wealth plan begins with personal financial clarity. Before buying a rental property or starting a business, a person should know their income, expenses, debts, savings rate, emergency reserves, credit position, and current assets. Wealth building begins with measurement.

The next step is separating expenses from asset purchases. Review the last three months of spending and ask which payments improved long-term financial strength. Some expenses are necessary. Others are lifestyle choices. The goal is not deprivation; it is awareness. Every dollar spent on consumption is a dollar unavailable for ownership.

Then build a financial base. This includes an emergency fund, insurance appropriate to the household, manageable debt levels, and protection against catastrophic setbacks. Kiyosaki often emphasizes bold action, but durable wealth requires resilience. A person without reserves may be forced to sell assets or borrow at bad terms during a crisis.

After that, choose an asset class to study deeply. Kiyosaki’s readers often gravitate toward real estate, but the principle applies broadly. Study one area long enough to understand its language and risks. If it is real estate, learn cap rates, cash-on-cash return, vacancy, repairs, financing, rent comparables, property taxes, insurance, and local market analysis. If it is equities, learn valuation, diversification, volatility, dividends, index funds, and long-term compounding. If it is business, learn unit economics, customer acquisition, margins, operations, and cash conversion.

The next step is small execution. The first investment should be sized to teach without threatening survival. A person might begin with a diversified investment account, a small business experiment, a real estate partnership, a house hack, or a modest income-producing project. The exact choice depends on capital, time, skill, and temperament.

Track results like an owner. Kiyosaki’s philosophy is built around financial statements, so create them. Track monthly income, expenses, assets, liabilities, and cash flow. Review whether each asset is performing as expected. Identify which decisions increased freedom and which increased stress.

Reinvest intelligently. Cash flow from assets should not immediately become lifestyle spending. In the early stages, reinvestment is the engine. Rental income can build reserves or fund the next down payment. Business profits can improve systems or acquire customers. Dividends can buy more shares. Royalties can fund new intellectual property.

As income streams grow, protect the downside. Use proper legal structures where appropriate. Maintain insurance. Keep cash reserves. Avoid overconcentration. Understand tax obligations. Work with qualified professionals when decisions become complex.

This approach preserves the best part of Kiyosaki’s message while reducing the danger of imitation without expertise.

The Real Meaning of “Rich” in Kiyosaki’s Philosophy

To Kiyosaki, getting rich is not only about having a large pile of money. It is about escaping dependence on a paycheck. The rich person, in his framework, owns assets that cover expenses and create choices.

This definition shifts the focus from status to freedom. A person driving an expensive car with large payments may look rich while being financially trapped. A person living modestly with strong cash flow may be far closer to freedom. The visible signs of wealth can be misleading.

Kiyosaki’s version of wealth is built quietly. It is built through financial education when others avoid the subject. It is built through asset purchases when others upgrade lifestyle. It is built through business systems when others sell only time. It is built through calculated risks when others remain frozen. It is built through cash flow that gradually replaces the need for active labor.

The path is not easy. It requires patience, study, discipline, and emotional control. It requires resisting social pressure. It requires learning from mistakes without being destroyed by them. It requires recognizing that not every opportunity is worth taking.

The most valuable lesson from Kiyosaki may be that financial freedom is not an accident reserved for the already wealthy. It is a design problem. Income must be directed. Assets must be acquired. Liabilities must be controlled. Knowledge must be increased. Cash flow must be measured. Risk must be managed.

For readers who want a simple formula, Kiyosaki’s philosophy can be summarized this way: earn money, keep a meaningful portion of it, use it to buy or build income-producing assets, reinvest the cash flow, increase financial intelligence, and repeat until asset income can support your life.

That formula is simple to understand and difficult to execute. The difficulty is why so few people do it consistently.

The promise of Kiyosaki’s work is not that everyone should follow the same investment path. It is that everyone should learn to think like an owner. Employees can think like owners. Entrepreneurs can think like owners. Investors can think like owners. The mindset begins when a person stops asking only how much they can earn and starts asking what they can own.

That is the cash flow mindset. It is the belief that wealth is not merely received through income. It is built through assets, systems, discipline, and education. Whether one agrees with every Kiyosaki recommendation or not, that idea remains one of the most important lessons in modern personal finance.