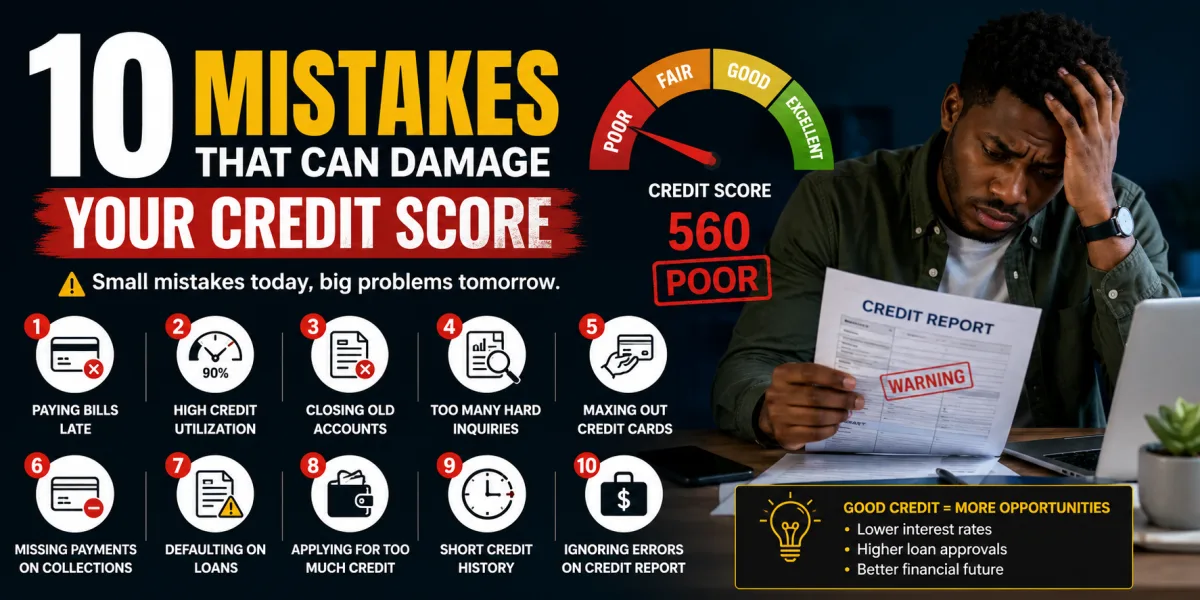

The Credit Damage Map: 10 Mistakes That Can Weaken Your Score for Years

A credit score is not wealth, but it can affect the price of financial life. It can influence whether a borrower is approved for a mortgage, auto loan, personal loan, credit card, apartment, or certain utility arrangements. It can affect the interest rate offered, the size of a required deposit, the credit limit assigned, and the choices available when money is needed quickly. A strong score does not make a person rich. A weak score can make ordinary borrowing more expensive.

This is why credit damage matters. A mistake that takes minutes can affect a credit report for years. A missed payment, maxed-out card, collection account, unnecessary application spree, or ignored credit report error can raise borrowing costs long after the original problem has passed. The financial penalty is not always obvious at first. It may show up later as a higher mortgage rate, a denied rental application, a smaller credit limit, or a personal loan offer with expensive terms.

Credit scoring is built from credit report information. FICO explains that a FICO Score is calculated only from information in a credit report, and that the main categories include payment history, amounts owed, length of credit history, credit mix, and new credit. Payment history accounts for 35 percent of a FICO Score, while amounts owed account for 30 percent.

Those percentages reveal a practical truth: the most damaging credit mistakes usually involve not paying as agreed or carrying too much debt relative to available credit. Other mistakes matter too, but late payments and high balances often do the most visible harm.

The Consumer Financial Protection Bureau advises consumers not to get close to their credit limits and notes that experts generally recommend keeping credit use at no more than 30 percent of total credit limits. The CFPB also explains that a longer credit history helps a score because scores are based on experience over time.

Credit health is therefore not built by tricks. It is built by evidence: payments made on time, balances kept manageable, accounts handled responsibly, reports kept accurate, and new credit used carefully. The mistakes below damage that evidence. Avoiding them is one of the simplest ways to protect financial flexibility.

Mistake 1: Paying Late

Late payments are one of the most damaging credit mistakes because payment history is the largest factor in many credit scoring models. A lender wants to know whether a borrower pays as promised. A late payment signals that the borrower may not be reliable under the terms of credit.

The damage depends on severity, timing, account type, credit history, and the rest of the file. A payment that is a few days late may trigger a late fee from the lender but may not be reported to the credit bureaus until it reaches a reportable delinquency threshold, often 30 days past due. Once a payment is reported late, the credit damage can be significant. A 60-day late payment is worse. A 90-day late payment is worse still. Eventually, an account can be charged off, sent to collections, repossessed, or foreclosed depending on the debt.

The CFPB states that credit reporting companies can generally report negative information about credit account payment history for up to seven years, while positive information may be reported longer. That means a single serious payment mistake may continue affecting a credit profile long after the bill is finally paid.

Late payments are especially dangerous because they can create a chain reaction. A borrower misses one payment, then faces late fees. The next payment becomes harder. Interest continues. The account becomes more delinquent. The credit score falls. New borrowing becomes more expensive. Cash flow tightens further.

The best protection is automation and margin. Set up automatic minimum payments on every credit card, loan, and recurring debt. Paying only the minimum is not ideal for debt reduction, but the minimum should never be missed because of forgetfulness. Add due-date alerts several days before payment. Keep a small buffer in the payment account. If income is irregular, align due dates with paydays where possible.

If a payment may be missed, contact the lender before the due date. Ask about hardship programs, payment extensions, due-date changes, deferment, or temporary reduced payments. A lender may not always help, but early communication is usually better than silence.

The most important credit habit is simple: pay on time, every time, even when the payment is small.

Mistake 2: Maxing Out Credit Cards

High credit card balances can damage a credit score even if every payment is made on time. This is because credit scoring models look at amounts owed, especially revolving credit utilization. Utilization compares credit card balances to credit limits. A card with a $1,000 limit and a $900 balance is 90 percent utilized. A card with a $1,000 limit and a $100 balance is 10 percent utilized.

FICO explains that amounts owed account for 30 percent of a FICO Score and that higher debt levels can affect the ability to meet monthly obligations. The CFPB also warns consumers not to get close to credit limits and notes that experts advise keeping credit use at no more than 30 percent of total credit limits.

The 30 percent figure is a useful guideline, but it is not a magic line. Lower utilization is generally better. A person using 5 percent of available revolving credit usually looks less risky than someone using 75 percent. A maxed-out card can signal financial stress even when the account is current.

High utilization can also become expensive. Credit card interest can accumulate quickly, especially when balances revolve month after month. A borrower may make payments but see little progress because much of the payment goes toward interest. The score damage and cash-flow pressure reinforce each other.

To reduce utilization, pay down the highest-utilization cards first, especially those near their limits. If possible, pay before the statement closing date so the issuer reports a lower balance to the credit bureaus. Many card issuers report the statement balance, not the balance after the due-date payment. This means a person who pays in full every month can still show high utilization if the balance is high when the statement closes.

Another option is requesting a credit limit increase, but only if it does not trigger unnecessary hard inquiries and will not tempt more spending. A higher limit helps utilization only when balances stay controlled.

Credit cards are powerful when used as payment tools and dangerous when used as income substitutes. The score rewards restraint.

Mistake 3: Applying for Too Much Credit at Once

New credit applications can damage a score when they create hard inquiries and signal increased borrowing risk. One hard inquiry may have a limited effect. Many hard inquiries in a short period can suggest that a borrower is seeking credit urgently or taking on too much debt.

New credit also affects account age. Opening several accounts at once can reduce the average age of accounts, add new payment obligations, and create more opportunities for missed payments. A person who opens multiple store cards, personal loans, or credit cards quickly may appear riskier even if every account is new and clean.

This mistake often happens during major life transitions. A person moves and applies for furniture financing, a store card, a personal loan, and a new credit card. Another person shops for a car and allows many dealers or lenders to submit applications without understanding how inquiries are handled. Someone chasing sign-up bonuses opens several cards in a short period. The result may be a temporary score drop and a more complex debt picture.

Rate shopping for certain loan types, such as mortgages or auto loans, may be treated differently by some scoring models when done within a focused window. But random applications across unrelated credit products are not the same as disciplined rate shopping.

The safest approach is to apply only when credit is needed and when the account fits a clear purpose. Before applying, ask whether the product solves a real problem, whether the payment fits the budget, and whether the timing could interfere with a larger goal such as a mortgage application.

Credit is not a collection hobby. Every application should earn its place.

Mistake 4: Closing Old Accounts Without a Plan

Closing old credit cards can damage a score in two ways. First, closing a card reduces available credit, which can increase utilization if balances remain the same. Second, older accounts contribute to the length and depth of a credit history, and credit scoring models value experience over time.

The CFPB notes that a long credit history helps a score because credit scores are based on experience over time. This does not mean every old account must stay open forever, but it does mean closures should be deliberate.

Consider a borrower with three credit cards: one with a $5,000 limit and no balance, one with a $3,000 limit and a $1,500 balance, and one with a $2,000 limit and no balance. Total available credit is $10,000, and total balance is $1,500, so utilization is 15 percent. If the borrower closes the $5,000 card, available credit falls to $5,000 and utilization jumps to 30 percent. Nothing new was borrowed, but the score profile weakened.

There are valid reasons to close accounts. A card may have a high annual fee, poor terms, security concerns, or a strong temptation to overspend. If a card fuels destructive behavior, protecting the financial life matters more than protecting the score. But when the card has no annual fee and does not create spending risk, keeping it open can support utilization and account age.

A useful compromise is to keep older no-fee accounts active with small occasional purchases paid in full. If an account charges a fee, ask whether it can be downgraded to a no-fee version rather than closed. If closure is necessary, pay down other balances first to prevent utilization from jumping.

Do not close credit accounts as a symbolic cleanup before applying for a loan. A simpler wallet can sometimes create a weaker score.

Mistake 5: Ignoring Credit Report Errors

A credit score is built from credit report data. If the data is wrong, the score may be wrong too. Ignoring credit report errors can damage approvals, rates, rental applications, and borrowing costs.

Errors can include accounts that do not belong to you, incorrect late payments, wrong balances, duplicate collections, accounts listed as open when closed, identity theft accounts, incorrect credit limits, outdated negative items, mixed files, and debts reported by the wrong collector. Even small errors can matter if they affect utilization or payment history.

The FTC states that AnnualCreditReport.com is the only authorized place to get the free annual credit reports consumers are entitled to by law. AnnualCreditReport.com also states that federal law allows consumers to get a free copy of their credit report every 12 months from each credit reporting company and to ensure the information is correct and up to date.

If an error appears, dispute it. The CFPB explains that consumers have the right to dispute errors on credit reports and that fixing an error generally means contacting both the credit reporting company and the company that provided the information.

Disputes should be specific and documented. Identify the account, explain what is wrong, include copies of supporting records, and keep proof of submission. If the problem is identity theft, use official identity theft recovery resources and take immediate steps to prevent further damage.

Credit report review is not only a reaction after denial. It should be routine maintenance. Check reports before applying for a mortgage, auto loan, personal loan, apartment, or major credit product. A false negative item discovered during underwriting can delay or derail an application.

Credit errors are not rare enough to ignore. A clean report is part of financial hygiene.

Mistake 6: Letting Accounts Go to Collections

A collection account can seriously damage credit because it indicates that an original account was not paid and was transferred or sold to a collector. Collections can come from credit cards, medical bills, utilities, phone accounts, apartment charges, personal loans, or other obligations.

The damage is not only the score impact. Collections can create stress, calls, letters, settlement negotiations, possible lawsuits, and confusion about who owns the debt. A collection can also complicate mortgage approval or rental applications even when the score has partly recovered.

The best way to avoid collections is to communicate early when payment trouble begins. If a bill cannot be paid in full, ask for a payment plan before the account is sent out. Medical providers, utilities, lenders, landlords, and service providers may have hardship options, but those options often shrink after an account enters collection.

If a collection already exists, do not ignore it. First, verify that the debt is legitimate, the amount is correct, and the collector has the right to collect. If the debt is inaccurate, dispute it. If it is valid, consider negotiating a payment or settlement agreement in writing. Ask how the account will be reported after payment. Different scoring models and lenders may treat paid collections differently, so payment may not always create an immediate score jump, but unresolved collections can still cause financial friction.

Be careful with old debts. Depending on state law, making a payment or promise to pay may affect collection timelines. If the amount is large, old, or disputed, consider nonprofit credit counseling or legal advice before acting.

Collections are easier to prevent than repair. The earlier a borrower responds, the more options usually remain.

Mistake 7: Co-Signing Without Understanding the Risk

Co-signing can damage credit because the co-signer becomes legally responsible for the debt. Many people treat co-signing as a character reference. Lenders treat it as a repayment guarantee.

If the primary borrower pays late, the late payment may appear on the co-signer’s credit report. If the borrower defaults, the lender can pursue the co-signer. The account may increase the co-signer’s debt-to-income ratio, making it harder to qualify for a mortgage, auto loan, or personal loan. Even if the borrower pays on time, the co-signed obligation can reduce future borrowing capacity.

Co-signing is emotionally difficult because it often involves helping family or friends. A parent co-signs for a child’s car. A relative co-signs for an apartment. A partner co-signs a personal loan. The relationship creates pressure, but the credit system does not care about intentions. It records payment behavior.

Before co-signing, ask whether you could afford to make the payment yourself if the borrower fails. If not, do not co-sign. Ask whether the account will report to credit bureaus, whether you will receive statements, whether there is a co-signer release option, and how missed payments will be communicated. Put expectations in writing with the borrower.

Co-signing can be generous. It can also be financially dangerous. Never lend your credit casually.

Mistake 8: Using Debt Consolidation as a Reset Button

Debt consolidation can help or hurt a credit score depending on behavior. A personal loan or balance transfer may lower interest, simplify payments, and reduce credit card utilization. That can support credit improvement. But consolidation becomes damaging when the borrower pays off cards and then uses them again.

This mistake is common because consolidation creates emotional relief. Several balances disappear. Minimum payments fall. The credit cards look available again. The borrower feels as if progress has been made. But if spending patterns do not change, the old balances return while the consolidation loan remains. The household now has more total debt than before.

Debt consolidation does not solve overspending, income instability, medical cost pressure, irregular budgeting, or lack of emergency savings. It only restructures debt. If the root problem remains, consolidation can create a larger credit problem later.

Used well, consolidation can improve payment consistency and reduce high revolving balances. Used poorly, it can damage credit through higher total debt, new missed payments, and renewed utilization.

Before consolidating, close the behavioral gap. Create a budget. Stop using paid-off cards for new debt. Build a starter emergency fund. Compare APRs and total repayment cost. Avoid loans with large fees or terms that stretch repayment unnecessarily. If debt is already unmanageable, consider nonprofit credit counseling before borrowing more.

Consolidation should be an exit ramp from debt, not a revolving door back into it.

Mistake 9: Carrying Balances Because You Think It Helps Credit

One persistent credit myth is that carrying a credit card balance helps build credit. It does not. Credit scores can reward responsible use, but responsible use does not require paying interest.

A borrower can use a card for small purchases, receive a statement, and pay the balance in full by the due date. That activity can show account use and on-time payment without carrying debt. Paying interest is not a credit-building requirement. It is a cost.

Carrying balances can damage credit through higher utilization and can damage finances through interest charges. It can also normalize debt. A borrower may begin with a small balance and slowly accept larger balances as ordinary. Over time, the credit card becomes a permanent loan instead of a payment tool.

This mistake is especially costly when borrowers carry balances on high-interest cards while keeping cash in low-yield accounts. Some emergency savings are essential, but beyond a reasonable cash cushion, paying down high-interest revolving debt may produce a stronger financial return than letting balances continue.

The healthiest credit card strategy is simple: use the card only for spending already covered by cash, keep utilization low, and pay in full. If paying in full is not possible, stop adding new charges and create a payoff plan.

You do not need credit card debt to have good credit. You need evidence of reliable repayment.

Mistake 10: Ignoring Identity Theft and Fraud Warning Signs

Identity theft can damage a credit score quickly. A fraudster may open accounts, run up balances, miss payments, or send accounts to collections under someone else’s name. The victim may not discover the damage until a lender denies an application, a collector calls, or a credit alert appears.

Warning signs include accounts you do not recognize, inquiries you did not authorize, addresses that are not yours, collection notices for unfamiliar debts, missing bills, unexpected authentication messages, tax or benefit issues, or sudden score changes. Credit report review helps detect these signs early.

AnnualCreditReport.com notes that reviewing credit reports helps consumers catch signs of identity theft early. This matters because the faster fraud is identified, the faster the victim can dispute accounts, freeze credit, file reports, and prevent new damage.

A credit freeze can restrict access to credit reports, making it harder for criminals to open new accounts. Fraud alerts can warn lenders to verify identity before extending credit. If identity theft occurs, victims should use official recovery resources, file disputes, contact affected lenders, and keep detailed records.

Ignoring suspicious activity gives fraud time to compound. Credit damage from identity theft is not the victim’s fault, but it still requires action to repair.

How These Mistakes Compound

Credit damage often compounds because one mistake leads to another. A borrower carries high balances. The minimum payments grow. Cash flow tightens. A payment is missed. The score drops. A new emergency requires borrowing, but the borrower now qualifies only for higher-cost credit. The higher-cost credit creates larger payments. Another account becomes late. Eventually, collections appear.

This is why credit protection is not only about scores. It is about household stability. Emergency savings, realistic budgets, lower fixed expenses, and debt discipline all protect credit because they reduce the chance that bills are missed or cards are overused.

A good credit score is often the visible result of deeper habits. Pay on time. Keep balances low. Avoid unnecessary debt. Review reports. Use credit intentionally. Build cash reserves. These habits sound ordinary because they are. Credit damage often comes from abandoning the ordinary under pressure.

How to Recover After Credit Damage

If your score is already damaged, the first step is to stop new damage. Bring current accounts up to date where possible. Contact lenders before accounts worsen. Stop adding new credit card balances. Build a small cash buffer. Review credit reports and dispute errors. Organize debts by balance, APR, payment status, and urgency.

Next, lower utilization. Paying down credit cards can improve a score once lower balances are reported. Focus first on maxed-out cards and high-interest revolving debt. If you cannot pay balances down quickly, consider a structured payoff plan.

Then rebuild positive history. Make every payment on time. Use a secured card carefully if you need an active positive account. Keep old no-fee accounts open if they are not causing spending problems. Avoid unnecessary applications. Give the file time to heal.

Do not fall for credit repair promises that sound too easy. Accurate negative information generally cannot be erased simply because it hurts. Legitimate improvement comes from accurate reporting, debt reduction, on-time payments, and time.

A Credit Protection Checklist

Set up automatic minimum payments on every credit account.

Keep credit card utilization low, preferably well below 30 percent where possible.

Pay credit cards before the statement closing date when preparing for a major application.

Check all three credit reports regularly through the authorized free-report source.

Dispute real errors with documentation.

Avoid unnecessary applications before a mortgage, auto loan, or rental application.

Keep older no-fee accounts open when they do not create spending risk.

Never co-sign unless you can afford to repay the debt yourself.

Use debt consolidation only with a plan to avoid new balances.

Act immediately on fraud, unfamiliar accounts, and collection notices.

The Wealth Lesson

A credit score is built from patterns. The most damaging mistakes are the ones that break those patterns: paying late, using too much available credit, applying too often, closing accounts carelessly, ignoring errors, allowing collections, co-signing without protection, consolidating debt without changing behavior, carrying balances unnecessarily, and failing to respond to fraud.

These mistakes matter because credit damage is not isolated. It can raise borrowing costs, shrink financial options, increase stress, and make future emergencies harder to manage. A weak score can turn a necessary loan into an expensive loan. A strong score can give a household more choices when timing matters.

The good news is that credit protection does not require financial genius. It requires systems. Automate payments. Keep balances low. Review reports. Dispute errors. Borrow only when there is a purpose. Preserve older accounts when useful. Avoid turning short-term pressure into long-term damage.

Credit is not the foundation of wealth, but it is part of financial access. Protect it the way you protect any valuable tool. Use it carefully, maintain it regularly, and never confuse available credit with available money.

The strongest credit score is not built by chasing loopholes. It is built by proving, month after month, that lenders can trust the record you are creating.