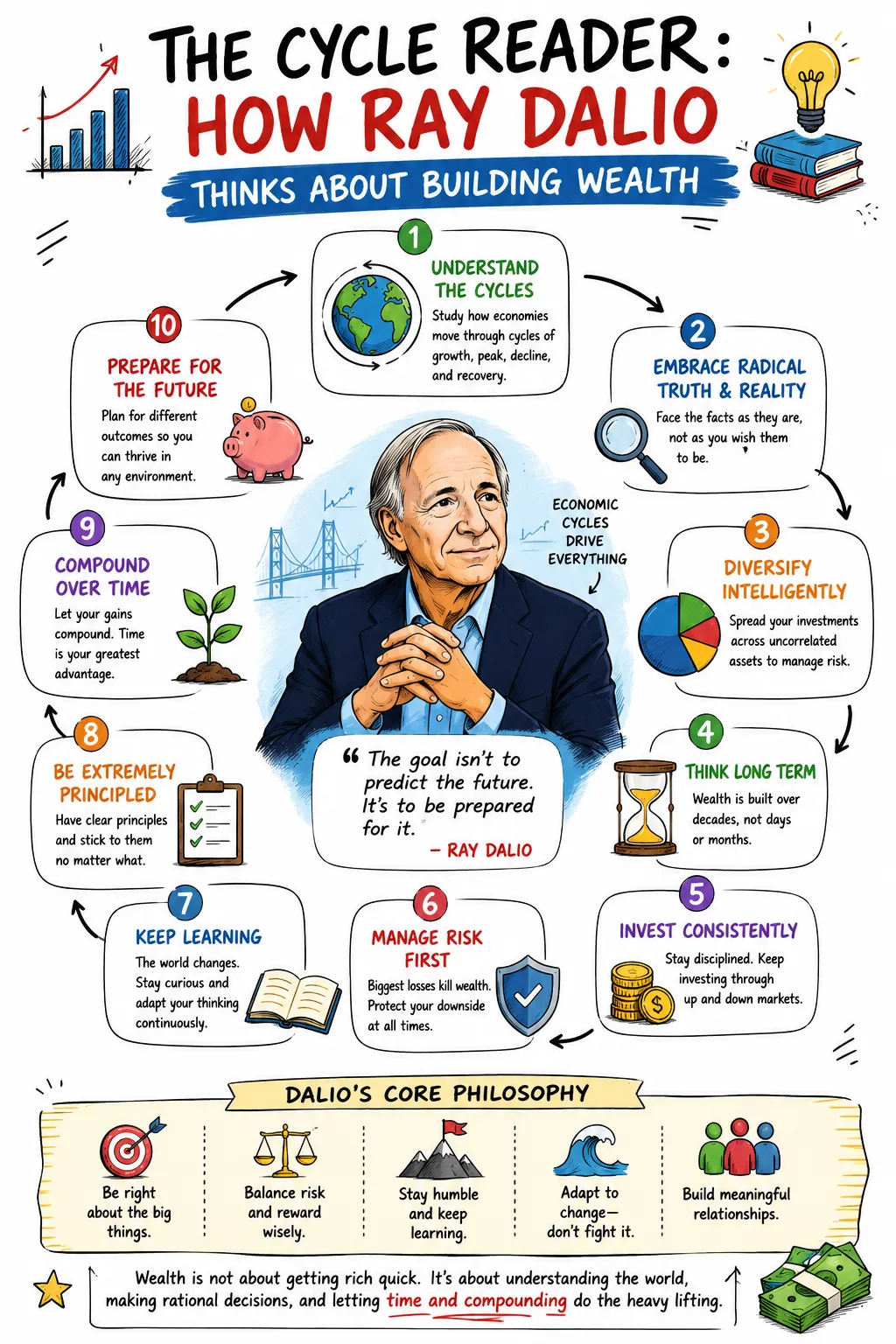

The Cycle Reader: How Ray Dalio Thinks About Building Wealth

Ray Dalio’s approach to getting rich begins with a premise that is both simple and demanding: reality has patterns, and the investor who studies those patterns carefully has an advantage over the investor who merely reacts. Dalio does not present wealth as a prize for guessing the next hot stock, chasing market excitement, or trusting intuition alone. His philosophy is built on understanding how the economic machine works, creating principles for decisions, balancing risk, learning from mistakes, and allowing capital to compound across changing environments.

That makes Dalio different from many modern wealth voices. Some emphasize entrepreneurship. Some emphasize frugality. Some emphasize passive index investing. Dalio’s center of gravity is macroeconomic understanding and decision quality. He wants investors to understand credit, debt, interest rates, inflation, productivity, central banks, currencies, and the long arcs of history. He believes markets are not random noise, even though they are difficult to predict. They are complex systems driven by incentives, liquidity, leverage, policy, psychology, and productivity.

Dalio founded Bridgewater Associates in 1975 from his two-bedroom apartment, and the firm grew into one of the most influential investment institutions in the world. Bridgewater’s official founder profile states that Dalio served over time as CEO, CIO, and Chairman, and that he shaped the firm’s investing approaches and culture before stepping down from those formal roles between 2017 and 2021.

His reputation rests not only on wealth, but on a system. Dalio is associated with principles-based decision-making, radical truth, radical transparency, global macro investing, and the All Weather approach. Bridgewater describes the All Weather strategy as the foundation of the risk parity movement, a way of building portfolios intended to survive different economic environments rather than depend entirely on one forecast.

To understand how to get rich according to Ray Dalio, it is necessary to start with what he is not saying. He is not saying that wealth comes from certainty. He is not saying that investors can reliably know the future. He is not saying that a single asset class will always be enough. He is not saying that intelligence alone defeats markets. His philosophy is more cautious and more durable: build principles, diversify intelligently, control emotion, think probabilistically, study history, and keep improving your decision system.

Dalio’s wealth philosophy is less glamorous than a get-rich-quick story. It is also more useful. It treats investing as a lifelong discipline rather than a series of lucky trades. It treats mistakes as data. It treats risk as something to be measured, not ignored. It treats money as one part of a meaningful life, not the entire definition of success.

Wealth Begins With Understanding the Economic Machine

Dalio’s first major lesson is that wealth is built inside an economic system. Investors do not operate in a vacuum. Their portfolios are affected by credit conditions, interest rates, inflation, monetary policy, fiscal policy, productivity growth, currency movements, geopolitical conflict, and investor psychology. A person who ignores these forces may still build wealth, but often does so without understanding the weather around them.

Dalio often uses the language of machines and cycles. The economy is not a literal machine, but the metaphor is helpful. Income, spending, borrowing, lending, production, and policy interact in repeatable ways. One person’s spending is another person’s income. One borrower’s debt is another lender’s asset. When credit expands, spending power can rise faster than income. When credit contracts, spending can fall, asset prices can decline, and financial stress can spread.

This is why debt cycles matter in Dalio’s worldview. A household can understand this intuitively. When credit is easy, people can buy homes, cars, businesses, and investments with borrowed money. That borrowing increases demand. Rising demand can lift prices. Rising prices can increase confidence. Confidence can encourage more borrowing. The cycle can feel self-reinforcing on the way up.

But debt creates future obligations. Borrowed money must be serviced. If income growth does not keep up, or if interest rates rise, or if asset prices fall, the same debt that once accelerated wealth can become a source of distress. Borrowers cut spending. Lenders tighten standards. Asset sales increase. Confidence weakens. A boom can become a contraction.

Dalio’s point is not that debt is always bad. Debt can finance productive investment, housing, infrastructure, education, and business growth. The question is whether debt is used productively and whether the system can service it under changing conditions. At the personal level, the same rule applies. Debt that increases earning power or acquires a durable asset may be useful. Debt that funds lifestyle inflation without future cash flow can become a trap.

Understanding interest rates is equally important. Interest rates influence the price of money. When rates are low, borrowing becomes cheaper, future cash flows become more valuable, and investors may accept higher prices for assets. When rates rise, borrowing costs increase, valuations can compress, and highly leveraged investors may be forced to adjust. A stock portfolio, a bond portfolio, a mortgage decision, a business valuation, and a real estate purchase are all shaped by the level and direction of rates.

Inflation adds another layer. Inflation reduces the purchasing power of money. Cash may feel safe because its nominal value is stable, but inflation can quietly erode what that cash can buy. Assets that perform well in disinflationary growth may not perform the same way during inflationary pressure. Dalio’s framework pushes investors to ask how their wealth would behave under different conditions rather than assuming the recent past will repeat.

This does not mean the individual investor must become a professional macro trader. Most people do not need to forecast central bank decisions or trade currencies. But they do need to understand that the economy moves in cycles, and portfolios should be built with humility about the future. Dalio’s philosophy begins by replacing financial naivety with economic awareness.

Compounding Is the Quiet Engine of Wealth

Dalio’s wealth philosophy respects the power of compounding. Compounding is the process by which returns generate additional returns over time. It is the difference between earning money once and letting money become a productive base for future growth.

The arithmetic is familiar, but the emotional challenge is often underestimated. Compounding works best when investors reinvest returns, avoid unnecessary interruption, and allow time to do the heavy lifting. Yet markets constantly tempt people to interfere. A sharp decline creates panic. A rapid boom creates greed. A fashionable trend creates envy. A boring portfolio feels inadequate when others appear to be getting rich faster.

Dalio’s philosophy is useful because it places compounding inside a broader decision system. The investor’s job is not merely to know that compounding exists. The investor’s job is to behave in a way that allows compounding to continue. That requires adequate liquidity, diversification, emotional control, and a realistic understanding of risk.

Consider two investors. The first earns high returns for a few years by concentrating heavily in a fashionable asset. The second earns more moderate returns through a diversified portfolio and stays invested for decades. The first investor may appear smarter during the boom, but if the concentrated asset collapses and the investor sells under pressure, the compounding chain breaks. The second investor may look less exciting, but consistency can become decisive over time.

Compounding rewards survival. This is one of the deepest links between Dalio’s investing philosophy and his risk management philosophy. If a portfolio is so fragile that one bad environment forces liquidation, it may never benefit from long-term compounding. If a household has no emergency reserve, it may be forced to sell investments during a downturn. If an investor uses too much leverage, a temporary decline can become permanent damage.

The lesson is not to avoid risk entirely. Without risk, there is usually limited return. The lesson is to take risks that can be endured. A long investment horizon is valuable only if the investor can remain in the game long enough for the horizon to matter.

This is why Dalio’s approach is more patient than speculative. Sustainable wealth is usually not built by constantly jumping from one idea to another. It is built by repeatedly allocating capital to productive assets, reinvesting gains, managing risk, and avoiding the behavioral mistakes that interrupt the process.

Diversification Is Not Decoration

Diversification is one of the most repeated concepts in investing, but Dalio gives it a deeper meaning. Many people think they are diversified because they own many investments. But owning many things that behave the same way is not true diversification. A portfolio of twenty high-growth technology stocks may contain twenty tickers, yet it can still be heavily exposed to the same economic forces: equity risk, valuation risk, interest-rate sensitivity, and investor sentiment.

Dalio’s version of diversification focuses on how assets behave under different environments. Stocks may do well during periods of economic growth. Government bonds may help during deflationary recessions or falling-rate environments. Inflation-linked assets, commodities, and gold may be more useful when inflation surprises investors or confidence in currency weakens. Cash may drag on returns during some periods, but it provides liquidity, optionality, and psychological stability.

The purpose is not to own everything blindly. The purpose is to avoid dependence on one version of the future. A portfolio that performs only when growth is strong and inflation is low is not prepared for all environments. A portfolio that performs only when inflation rises may struggle if inflation falls. A portfolio that depends entirely on falling interest rates may suffer when the rate cycle changes.

Bridgewater’s All Weather research is built around this problem. The firm describes the All Weather strategy as a portfolio approach created to perform across different economic environments and as the foundation of risk parity. The core idea is that investors should not need to know exactly which environment is coming in order to build a resilient portfolio.

For individual investors, this principle can be liberating. It reduces the pressure to predict perfectly. Instead of asking, “What will happen next?” the investor asks, “What would happen to my portfolio if I am wrong?” That question is more practical, because every investor will be wrong at some point.

Diversification also protects against emotional overconfidence. During long bull markets, concentrated portfolios can appear brilliant. Investors begin to believe that recent winners are permanent winners. They forget that asset classes move through seasons. The same asset that creates wealth in one environment may destroy wealth in another if purchased at the wrong price or held without risk control.

Dalio’s philosophy encourages investors to think like risk engineers. Where are the hidden concentrations? Which assets are exposed to the same shock? What happens if inflation rises? What happens if growth slows? What happens if rates stay higher than expected? What happens if a currency weakens? What happens if liquidity disappears?

A diversified portfolio will not always outperform a concentrated one. During a powerful equity bull market, diversification can feel like a drag. That is the price of resilience. Dalio’s argument is not that diversification wins every year. It is that diversification can improve the odds of staying solvent, disciplined, and invested across many years.

Balance Risk, Not Just Dollars

One of Dalio’s most important contributions to modern portfolio thinking is the distinction between allocating capital and allocating risk. A traditional investor might put 60 percent of a portfolio in stocks and 40 percent in bonds and assume the portfolio is balanced. But the risk of the portfolio may still be dominated by stocks because stocks are generally more volatile than high-quality bonds.

This distinction matters. A portfolio can look diversified by dollars while being concentrated by risk. If the equity portion drives most of the volatility, then the investor’s actual experience will depend heavily on equity market outcomes. When stocks fall sharply, the portfolio may fall more than expected, even though the investor thought the bond allocation provided balance.

Risk parity tries to address this by allocating risk more evenly across asset classes. Instead of asking only how many dollars go into each asset, it asks how much each asset contributes to total portfolio risk. Bridgewater’s All Weather approach is widely associated with this movement, and Bridgewater itself describes All Weather as the foundation of risk parity.

For institutional investors, risk parity can involve sophisticated modeling, leverage, derivatives, and dynamic risk management. Individual investors should be careful before attempting to copy institutional strategies directly. The principle, however, remains valuable: understand what actually drives the risk of your portfolio.

A household may believe it is diversified because it owns a home, a retirement account, and employer stock. But if the job, home value, and investments are all tied to the same industry or local economy, the household may be more concentrated than it appears. A technology employee with company stock, a home in a technology-heavy region, and a portfolio tilted toward technology funds has multiple exposures to the same economic engine. If that engine weakens, income, net worth, and housing value may all be pressured together.

Balancing risk also applies to debt. A family with a variable-rate mortgage, leveraged real estate, and cyclical employment may be exposed to rising rates and downturns in ways that are not obvious during good times. A business owner whose personal wealth is almost entirely tied to the business may have high upside, but also high concentration risk.

Dalio’s framework encourages people to look through labels and identify underlying exposure. A portfolio is not balanced because it contains many accounts. It is balanced when the forces that can damage it are understood, measured, and intentionally managed.

Build Principles Instead of Chasing Predictions

Dalio is famous for principles. His official Principles site describes his approach as an idea meritocracy that strives for meaningful work and meaningful relationships through radical transparency. For investors, the key lesson is that principles are decision rules created from experience, evidence, and reflection.

Predictions are fragile. Principles are more durable. A prediction says, “This market will rise next year.” A principle says, “I will not build a portfolio that depends on one forecast being right.” A prediction says, “Inflation has peaked.” A principle says, “I will understand how my assets behave if inflation remains higher than expected.” A prediction says, “This stock cannot fall much further.” A principle says, “I will size positions so that being wrong does not permanently impair my capital.”

Dalio’s philosophy does not reject forecasting entirely. Bridgewater is a global macro firm, and macro investors necessarily form views about economic conditions. But Dalio’s broader lesson for the public is humility. Since the future is uncertain, investors need systems that can survive error.

Principles are especially valuable because emotions are inconsistent. The investor who makes decisions only by feeling will often become more aggressive after gains and more fearful after losses. A principles-based investor can predefine behavior. How much cash should be held? How often should the portfolio be rebalanced? What level of debt is acceptable? What would trigger a sale? How much can be invested in speculative assets? What is the plan during a 30 percent market decline?

These questions should be answered before stress arrives. During calm periods, people can think more clearly. During panic, they often seek relief. A written principle can prevent a temporary emotional state from becoming a permanent financial mistake.

At the personal level, principles might include: never carry high-interest consumer debt without an aggressive repayment plan; maintain an emergency fund before taking illiquid risk; diversify across asset classes and income sources; avoid investments that cannot be explained clearly; never invest money needed for near-term obligations in volatile assets; rebalance periodically; increase savings when income rises; and treat mistakes as diagnostic information rather than personal failure.

The exact principles will differ by person. A young entrepreneur, a retiree, a salaried professional, and a family business owner face different constraints. What matters is the habit of converting lessons into rules. Dalio’s wealth philosophy is not merely about knowing more. It is about becoming the kind of person whose decisions improve over time.

Mistakes Are Expensive Tuition Unless They Become Principles

Dalio treats mistakes as central to learning. This is one of the most practical parts of his philosophy. Everyone makes financial mistakes. The difference between a costly mistake and a valuable one is whether the lesson changes future behavior.

A person who loses money in a speculative investment can respond in several ways. They can blame the market, blame bad luck, chase the loss, swear off investing entirely, or diagnose what happened. Did they misunderstand the asset? Did they size the position too large? Did they confuse a story with evidence? Did they rely on someone else’s conviction? Did they ignore liquidity risk? Did they invest money they could not afford to lose? Did they lack an exit rule?

The Dalio method is to identify the mistake, diagnose the root cause, create a solution, and convert the solution into a principle. This process turns pain into improved judgment. Without it, the same mistake repeats in different clothing.

Financial history is full of repeated mistakes because human nature does not change quickly. People overborrow during booms. They extrapolate recent returns. They assume liquidity will be available. They underestimate tail risk. They sell in panic. They believe complexity means sophistication. They trust impressive people without understanding incentives. They mistake luck for skill.

The investor who studies mistakes becomes harder to fool. Not impossible, but harder. Every personal error becomes a case study. Every market cycle becomes evidence. Every poor decision becomes a chance to refine the system.

This is also why radical honesty matters. If a person cannot admit the real reason for a mistake, they cannot fix it. A failed investment may not have failed because of unforeseeable events. It may have failed because the investor ignored valuation, concentration, leverage, or competence. A budget may not fail because of one emergency. It may fail because fixed costs are too high. A career may not stagnate because of unfairness alone. It may stagnate because the person stopped building scarce skills.

Dalio’s culture of radical truth can be uncomfortable, and critics have questioned how well such a culture works in practice. But the underlying personal finance lesson is strong: self-deception is expensive. Wealth grows more reliably when people are willing to see reality clearly.

Radical Truth and Radical Transparency as Financial Habits

Dalio’s management philosophy is often discussed in the context of Bridgewater’s culture, but it also applies to household and individual finance. Radical truth means facing facts as they are. Radical transparency means making relevant information visible enough that better decisions can be made. Principles.com states that embracing radical truth and radical transparency can bring more meaningful work and meaningful relationships.

In personal finance, lack of transparency causes damage. Couples avoid discussing debt. Families hide spending. Business partners delay hard conversations. Investors refuse to calculate real returns. Employees avoid asking whether their skills are still competitive. Retirees underestimate longevity risk. Entrepreneurs avoid confronting unit economics. The facts do not disappear because they are uncomfortable.

A truth-based financial life begins with accurate numbers. What is your net worth? What are your liabilities? What is your savings rate? Which expenses are fixed? Which debts carry the highest interest rates? What percentage of wealth is tied to one employer, property, currency, or asset class? How long could you survive without income? What insurance gaps exist? What assumptions must be true for your plan to work?

These questions can create discomfort, but discomfort is not the enemy. False comfort is. A household that knows the truth can adjust. A household that avoids the truth often drifts until forced adjustment becomes painful.

Radical transparency does not mean sharing every private detail with everyone. It means the people affected by financial decisions need access to the information required for wise choices. Spouses should understand the financial picture. Business partners should understand risks and obligations. Heirs may need clarity about estate plans. Advisors need accurate information to give useful guidance.

Dalio’s broader point is that reality is the foundation of progress. You cannot improve what you refuse to measure. You cannot manage risk you refuse to see. You cannot build wealth on denial.

Control Emotions Before They Control the Portfolio

Dalio’s investment philosophy is deeply aware of emotion. Markets are not only mathematical systems. They are human systems. Prices move because people, institutions, governments, and algorithms respond to incentives, fear, greed, liquidity, and expectations. The individual investor is not separate from this psychology. They are part of it.

Emotional decision-making is dangerous because it often feels most convincing at precisely the wrong time. Near market tops, optimism feels rational. Stories are abundant. Recent returns confirm confidence. People who warn about risk look foolish. Near market bottoms, pessimism feels rational. Losses are visible. Headlines are frightening. Selling feels like self-protection.

A disciplined investor must learn to distrust emotional intensity. The feeling that “this time is different” deserves examination. Sometimes conditions genuinely change. But often the phrase is a signal that investors are rationalizing behavior they would reject in calmer moments.

Dalio’s solution is systematic thinking. Predefined rules reduce dependence on mood. Rebalancing forces investors to trim what has risen and add to what has fallen, if the long-term allocation still makes sense. Position limits prevent enthusiasm from becoming concentration. Liquidity reserves prevent panic selling. Diversification reduces the emotional burden of any single outcome. Written principles create distance between impulse and action.

This is not easy. Emotional discipline is not achieved by reading one book or repeating a slogan. It is built through preparation, experience, and humility. An investor who has already imagined downturns is less shocked when they arrive. A household with cash reserves is less likely to sell investments at the wrong time. A person who understands market history is less likely to believe every crisis is unprecedented.

Emotional control also applies during success. Wealth can make people careless. A rising portfolio can create the illusion of genius. A successful business can encourage overexpansion. A promotion can justify lifestyle inflation. A lucky investment can lead to larger and more reckless bets. Dalio’s principles-based thinking protects against both panic and arrogance.

The goal is not to become emotionless. Money is tied to safety, identity, family, status, and dreams. Emotion is unavoidable. The goal is to prevent emotion from making final decisions without evidence and structure.

Think in Probabilities, Not Certainties

Dalio’s worldview is probabilistic. Instead of asking, “Will this happen?” a better investor asks, “What is the probability, what are the consequences, and how should I position myself?” This shift is subtle but powerful.

Certainty is seductive. People want clear answers: recession or no recession, inflation or deflation, bull market or bear market, soft landing or crisis. But markets rarely provide certainty in advance. Even when an investor correctly identifies a risk, timing and magnitude remain difficult. A good thesis can lose money if expressed too early, sized too large, or held with too much leverage.

Probabilistic thinking encourages humility. An investor might believe there is a 60 percent chance of one outcome and a 40 percent chance of another. That belief should produce a different portfolio than a 100 percent conviction. It should also invite updating as evidence changes.

This mindset is useful beyond investing. A person considering a career move can estimate probabilities: chance of higher income, chance of stress, chance of learning, chance of regret, chance of reversibility. A business owner can assess scenarios: base case, upside case, downside case, liquidity stress case. A household can evaluate debt: what happens if income falls, rates rise, or expenses increase?

Probabilistic thinking also reduces shame around being wrong. If you believe an outcome has a 70 percent probability, the 30 percent outcome can still happen. Being wrong does not automatically mean the decision was bad. A decision is bad if the probabilities, consequences, and sizing were poorly considered. A good decision can have a bad outcome. A bad decision can have a lucky outcome.

This distinction is essential for wealth building. Without it, people learn the wrong lessons. They may repeat reckless behavior because it worked once. Or they may abandon sound behavior because it failed temporarily. Dalio’s framework asks investors to judge process, not just outcome.

Meaningful Work and Meaningful Relationships

Dalio’s definition of success is not limited to money. His principles emphasize meaningful work and meaningful relationships, especially when supported by radical truth and transparency. Principles.com states that meaningful relationships and meaningful work are mutually reinforcing.

This matters because wealth can become distorted when money is separated from life quality. A person can accumulate assets while damaging health, relationships, curiosity, and purpose. Dalio’s philosophy does not romanticize poverty or dismiss financial success. He built extraordinary wealth. But his broader framework suggests that money is not the highest form of achievement by itself.

Meaningful work creates energy, learning, and contribution. It does not always mean glamorous work. It means work connected to values, strengths, and growth. A craftsperson, physician, teacher, investor, founder, engineer, farmer, or manager can all experience meaningful work if the work challenges them and serves something beyond vanity.

Meaningful relationships provide feedback, belonging, trust, and perspective. They also protect against the isolation that can come with ambition. Wealth without trusted relationships can become lonely and fragile. A person surrounded only by flatterers, dependents, or transactional contacts may lack the honest feedback needed to make wise decisions.

Dalio’s emphasis on truth connects these ideas. Meaningful relationships require honesty. Meaningful work requires reality-based improvement. In both cases, comfort is less important than growth.

For the individual wealth builder, this means financial goals should be integrated with life goals. What kind of work do you want wealth to make possible? Which relationships should money help protect? What kind of person are you becoming while pursuing wealth? Are you building assets at the expense of everything that makes those assets worth having?

Dalio’s philosophy gives permission to define success broadly. Getting rich is not merely about a number. It is about becoming more capable, more truthful, more resilient, and more useful while building financial security.

How Individual Investors Can Apply Dalio Without Becoming Macro Traders

The average investor should be careful when translating Dalio’s institutional methods into personal strategy. Bridgewater operates with resources, data, talent, tools, and risk systems far beyond what a household can replicate. An individual investor does not need to build a hedge fund in miniature.

What individuals can adopt are the principles beneath the machinery. First, build financial literacy around the economic forces that affect your life. Understand how interest rates influence mortgages, bonds, savings accounts, business valuations, and stock prices. Understand how inflation affects purchasing power. Understand how debt can amplify both gains and losses. Understand why liquidity matters during stress.

Second, create a diversified core portfolio. For many investors, broad-based, low-cost funds may be the most practical way to own productive assets across markets. The exact allocation depends on age, income stability, goals, risk tolerance, tax situation, and time horizon. Dalio’s lesson is not that everyone needs the same All Weather mix. The lesson is that portfolios should not depend entirely on one economic outcome.

Third, manage risk before chasing return. Ask what could force you to sell at the wrong time. Job loss? Medical expenses? Debt payments? Concentrated employer stock? Illiquid investments? Lack of cash? A portfolio that looks optimal on paper but fails under real-life stress is not truly optimal.

Fourth, write down investment principles. This can include target allocation, rebalancing rules, contribution schedule, emergency fund policy, debt limits, speculative investment limits, and criteria for changing strategy. The point is to reduce improvisation during emotional periods.

Fifth, review mistakes honestly. Every year, examine financial decisions without self-punishment. What worked? What failed? What was luck? What was skill? What risk was misunderstood? What assumption changed? Which principle needs updating?

Sixth, separate entertainment from investing. It is acceptable to follow markets, read macro commentary, and study investment ideas. But entertainment should not control the family balance sheet. A small experimental account is different from risking retirement security on a prediction.

Seventh, protect compounding. Avoid high-interest debt. Avoid excessive fees. Avoid unnecessary trading. Avoid panic selling. Avoid concentration you cannot emotionally or financially endure. The boring behaviors are often the ones that keep compounding alive.

The Limits of Dalio’s Approach

Dalio’s philosophy has limitations, especially for individual investors. The first is that macroeconomic understanding does not guarantee superior returns. Many intelligent investors correctly understand broad conditions and still fail to profit because timing, valuation, positioning, and market expectations are difficult. The economy and the market are related, but they are not the same thing.

The second limitation is that diversification can disappoint. A diversified portfolio may lag a concentrated stock portfolio during long equity booms. Investors may become impatient and abandon resilience at exactly the wrong time. Diversification is emotionally difficult because its benefits are often invisible until conditions change.

The third limitation is that risk parity and All Weather concepts can be complex. Institutional versions may use leverage or instruments that are inappropriate for many households. A simplified diversified portfolio may capture some of the spirit, but not the exact mechanics. Investors should avoid copying advanced strategies without understanding costs, taxes, liquidity, leverage, and implementation risk.

The fourth limitation is that principles can become rigid. A principle is useful when it reflects reality. It becomes dangerous when treated as sacred despite changing evidence. Dalio’s own framework emphasizes learning and updating. The point is not to freeze decisions forever, but to improve them through feedback.

The fifth limitation is cultural. Radical transparency may improve decision-making in some settings, but it can also be misapplied. Honesty without judgment can become cruelty. Transparency without boundaries can become dysfunction. In personal finance, the goal should be truth in service of better decisions, not bluntness for its own sake.

The mature reader should take Dalio seriously without turning him into a doctrine. His principles are tools. They must be adapted to personal circumstances, temperament, and goals.

Dalio Compared With Buffett, Bogle, and Howard Marks

Dalio’s philosophy overlaps with other great investment thinkers, but his emphasis is distinct. Warren Buffett focuses on buying high-quality businesses at sensible prices, understanding competitive advantage, and letting compounding work over long periods. John Bogle emphasized low costs, broad diversification, index funds, and staying the course. Howard Marks focuses deeply on risk, cycles, investor psychology, and second-level thinking. Dalio adds a global macro lens and a systematic culture of principles.

Where Buffett studies businesses, Dalio studies economic machines. Where Bogle simplifies investing for the ordinary person, Dalio dissects the forces that make different assets behave differently. Where Marks emphasizes market cycles and risk awareness, Dalio adds debt cycles, policy, and macroeconomic regimes. All of them respect discipline, humility, and long-term thinking.

The ordinary investor can combine their lessons. From Buffett: own productive assets and be patient. From Bogle: keep costs low and avoid unnecessary complexity. From Marks: understand risk and cycles. From Dalio: diversify across environments, build principles, and study the economic forces that shape outcomes.

The best personal investment philosophy is rarely copied from one person. It is assembled from durable truths. Dalio’s contribution is especially valuable for investors who have never thought beyond stocks rising over time. He reminds them that the world changes, regimes shift, debt matters, inflation matters, and portfolios should be built for uncertainty.

The Dalio Wealth Checklist

A practical Dalio-inspired wealth plan begins with clarity. Know what you own, what you owe, what you earn, what you spend, and what risks you carry. Financial vagueness is the enemy of good decision-making.

Next, build a liquidity base. Cash may not be exciting, and inflation can erode its purchasing power, but liquidity prevents forced selling and creates flexibility. An emergency fund is not a failure to invest. It is part of the system that allows investments to remain invested.

Then invest consistently. Choose an allocation that reflects your goals and risk tolerance. Use broad diversification where appropriate. Reinvest returns. Keep costs reasonable. Avoid constantly changing strategy because of headlines.

Study economic basics. You do not need to predict the next central bank decision, but you should understand how inflation, rates, debt, and growth affect your life. This knowledge improves decisions around mortgages, career risk, savings, business investment, and asset allocation.

Balance risk. Look beyond account labels and identify true exposure. Are you overly dependent on one employer, industry, country, currency, property, or asset class? What would happen if that exposure suffered?

Write principles. Create rules for saving, investing, debt, speculation, rebalancing, and major financial decisions. Revisit those rules periodically as life changes.

Run scenario analysis. What happens if markets fall sharply? What happens if inflation persists? What happens if rates rise or stay high? What happens if you lose income for six months? What happens if a major expense appears? A plan that survives only the best case is not a plan.

Learn from mistakes. Keep a decision journal for major financial choices. Record why you made the decision, what you expected, what could go wrong, and how you will evaluate the outcome. This creates a feedback loop.

Protect meaningful work and relationships. Do not let wealth building become an excuse to neglect the life wealth is supposed to support. Money should increase freedom, resilience, and contribution.

The Final Measure of Getting Rich According to Ray Dalio

To get rich according to Ray Dalio is to become a better reader of reality. Wealth is not built by wishful thinking. It is built by understanding systems, respecting cycles, managing risk, and improving decisions through principles and feedback.

Dalio’s path is not the fastest-sounding path. It does not promise overnight transformation. It asks for patience, study, humility, and discipline. It asks investors to accept uncertainty rather than pretend it can be eliminated. It asks them to diversify because the future is unknowable, to compound because time is powerful, and to tell the truth because denial is expensive.

The central lesson is that sustainable wealth requires both capital and character. Capital compounds when protected and reinvested. Character compounds when mistakes become principles. A person who can do both becomes increasingly difficult to derail.

Dalio’s philosophy is especially valuable in uncertain times because it does not depend on a perfect forecast. It prepares for multiple outcomes. It treats risk as a first-class concern. It respects the economy’s cycles without surrendering to them. It reminds investors that the goal is not to be right about everything, but to build a system that can survive being wrong.

For the individual reader, the most useful takeaway is not to imitate Bridgewater. It is to think more clearly. Understand the machine you live in. Own assets that can compound. Diversify across possible futures. Write principles before emotion takes over. Learn from mistakes without ego. Seek meaningful work and meaningful relationships alongside financial security.

That is how Ray Dalio’s wealth philosophy becomes practical. It turns getting rich from a chase into a discipline. It replaces prediction with preparation. It replaces emotional reaction with thoughtful rules. It replaces financial noise with a long-term system for surviving, learning, and compounding.