The Science of Compounding: How Time Turns Consistency Into Wealth

Compounding is one of the few financial ideas that sounds simple and remains profound after decades of study.

At its core, compounding means growth building on previous growth. An investment earns a return. That return remains invested. Future returns are then earned not only on the original amount, but also on the earlier gains. Over time, the process can turn modest contributions into meaningful wealth, provided the money remains invested, costs are controlled, risk is managed, and the investor avoids self-defeating behavior.

The mathematics is clean. The human behavior is not.

Most people understand compounding in theory. Fewer people give it enough time to work. They start late. They stop during market declines. They withdraw gains. They chase trends. They increase spending faster than contributions. They search for perfect timing. They underestimate fees. They panic when volatility appears. They forget that compounding rewards patience more than excitement.

This is why compounding is not only a mathematical principle. It is a behavioral test.

The U.S. Securities and Exchange Commission’s Investor.gov compound interest calculator describes compound interest as a way to estimate how money can grow when earnings are reinvested, and Investor.gov’s educational materials emphasize starting to save and invest early because compound interest applies to both the initial principal and accumulated interest. ([investor.gov](https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator?utm_source=chatgpt.com)) ([investor.gov](https://www.investor.gov/additional-resources/information/military/getting-started?utm_source=chatgpt.com)) Vanguard’s investment principles reinforce the behavioral side of this process: set clear goals, keep a balanced and diversified investment mix, minimize costs, and maintain long-term discipline. ([corporate.vanguard.com](https://corporate.vanguard.com/content/dam/corp/research/pdf/vanguards_principles_for_investing_success.pdf?utm_source=chatgpt.com))

The phrase “science of compounding” should be understood carefully. Compounding is grounded in mathematics, investment theory, and historical market evidence. It is not a guarantee. Investments fluctuate. Inflation reduces purchasing power. Market downturns can last longer than expected. Past returns do not promise future returns. A concentrated investment can fail permanently. High costs can weaken results. Poor investor behavior can interrupt the process.

Still, when used wisely, compounding is one of the most accessible wealth-building forces available to ordinary households. It does not require fame, inheritance, genius, or constant trading. It requires time, consistency, reinvestment, patience, discipline, and a portfolio suited to the investor’s goals and risk tolerance.

The science is simple. The challenge is staying with it long enough for the numbers to become powerful.

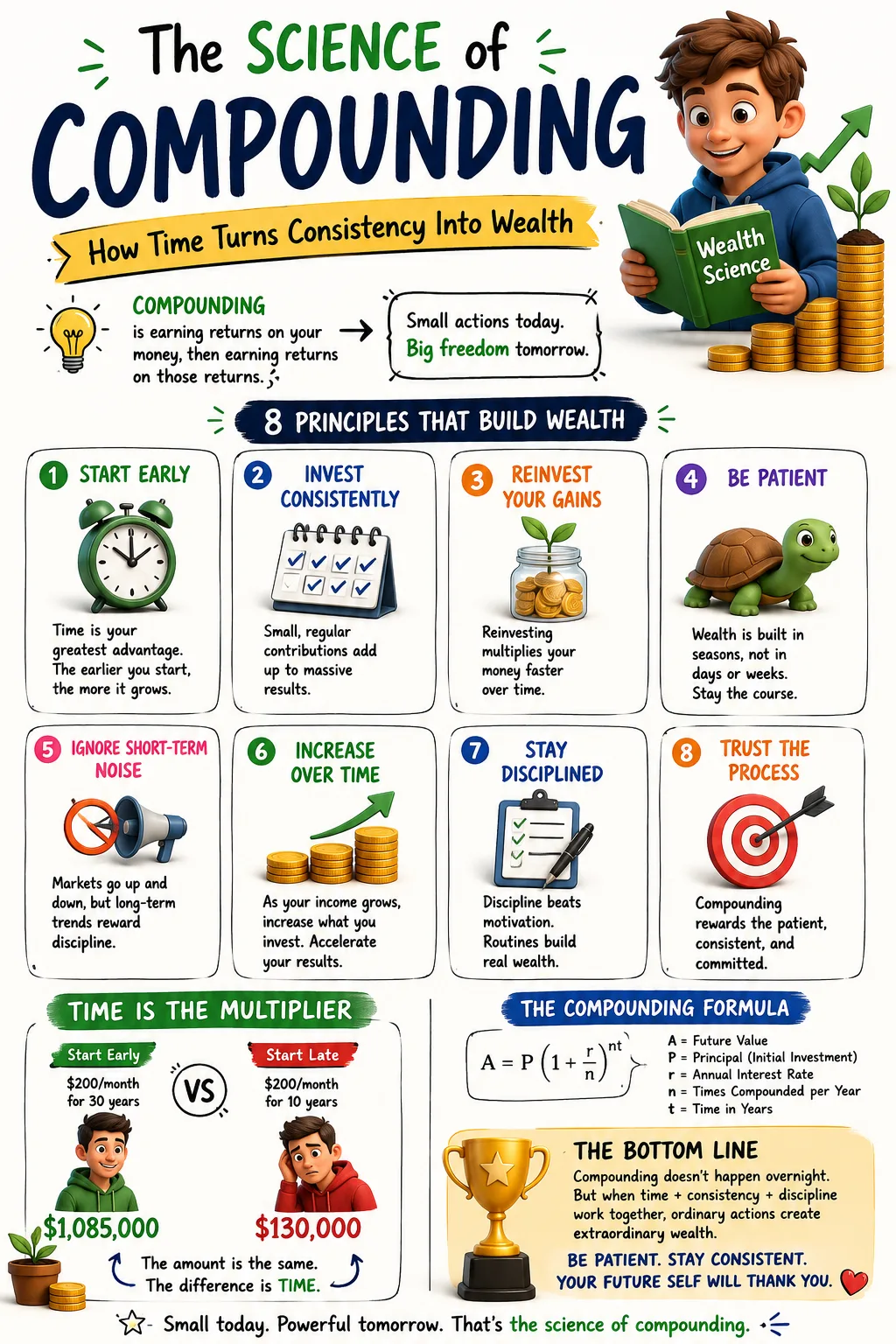

1. Start Now: Time Matters More Than Perfect Timing

The first rule of compounding is to begin early enough for time to matter.

Many people delay investing because they are waiting for the perfect moment. They want markets to feel safer, income to feel larger, debts to feel smaller, or knowledge to feel complete. Some of these concerns are valid. A person should not invest rent money, emergency cash, or money needed immediately for essential obligations. High-interest debt may deserve urgent attention before aggressive investing. Financial education matters.

But waiting for perfect conditions can become a permanent habit. Markets are rarely calm. Personal finances are rarely effortless. There is always a reason to delay. The cost of delay is time, and time is the ingredient compounding needs most.

Starting early gives every dollar more years to work. This is why small early contributions can compete with much larger later contributions. The early investor does not need each dollar to be large; they need each dollar to be patient. A dollar invested at 25 has more compounding runway than a dollar first invested at 45.

Time also reduces the pressure to chase extraordinary returns. A late starter may feel tempted to compensate through speculation, leverage, concentrated bets, or unrealistic assumptions. An early starter can rely more heavily on steady contributions and broad market exposure. This does not eliminate risk, but it can reduce the need for desperation.

The phrase “time in the market beats timing the market” captures a useful principle, though it should not be treated as a magic rule. No one can guarantee market outcomes over any specific period. But for long-term investors, repeatedly waiting for perfect entry points can be damaging because some of the best market periods are difficult to predict in advance. Missing strong days can reduce long-term results, and those gains then fail to compound.

The practical lesson is not to invest blindly at any moment with no regard for risk. The lesson is to build a process that does not depend on perfect prediction. Automatic contributions, diversified portfolios, and long-term plans allow investors to participate without needing to know exactly what markets will do next month.

Starting now may mean starting small. A person can begin with a retirement plan contribution, an index fund, an employer-sponsored account, or a modest automatic transfer. The first contribution is not only financial. It is psychological. It shifts identity from consumer only to owner.

Compounding begins with money, but it is sustained by the decision to stop waiting for a perfect future self.

2. Invest Consistently: Regular Contributions Create Momentum

Compounding becomes stronger when contributions are repeated.

Investing once is useful. Investing regularly is transformative. Regular contributions create momentum because they turn wealth building into a system rather than an event. Money enters the household, a portion is assigned to the future, and the process repeats before emotion can interfere.

This is why automatic investing is so powerful. It reduces reliance on mood, memory, and market opinion. The investor does not need to feel inspired every month. The system acts. Over years, those repeated actions can become a substantial portfolio.

Regular investing is often associated with dollar-cost averaging, which means investing a fixed amount at regular intervals regardless of market conditions. Dollar-cost averaging does not guarantee profit or prevent loss. It can underperform lump-sum investing in rising markets because money held back waits on the sidelines. But for many households, regular investing matches how income arrives and helps reduce emotional decision-making.

The behavioral benefit is significant. A person who invests only when they feel confident may buy after markets have already risen. A person who stops investing during downturns may miss lower prices and later recoveries. Regular contributions remove some of that timing pressure. They make investing ordinary.

Consistency also creates financial awareness. A household that invests every month begins to notice contribution rates, account balances, asset allocation, fees, taxes, and long-term goals. The habit builds knowledge through repetition.

There is another benefit: consistency turns modest income into progress. Many people delay investing because they believe the amount is too small to matter. But small amounts invested consistently can matter over long periods. The account balance may grow slowly at first, but the habit is doing invisible work. It is building discipline, financial identity, and a base that future contributions can expand.

The danger is stopping too often. Pausing contributions for true emergencies may be necessary. But stopping because markets are frightening, because lifestyle spending increased, or because the process feels slow can interrupt compounding. Wealth building is often less about dramatic financial intelligence and more about refusing to break the chain.

Consistency beats intensity because compounding rewards repetition.

3. Reinvest Gains: Growth Builds Upon Growth

Reinvestment is the engine inside compounding.

If an investment pays dividends, interest, or distributions and those payments are spent immediately, the investor receives income but reduces the compounding effect. If those gains are reinvested, they buy additional assets, which can then produce their own future returns. Growth begins to build upon growth.

This is the difference between harvesting and compounding. Harvesting takes the fruit now. Compounding plants the seeds again.

Reinvesting gains is especially powerful over long horizons because it increases the base on which future returns are calculated. At first, the change may feel minor. A small dividend reinvested into more shares does not look life-changing. But over decades, reinvestment can become a major contributor to total return.

Reinvestment applies beyond public markets. A business owner reinvests profits into better equipment, technology, staff, marketing, or product development. A real estate investor reinvests cash flow into maintenance, debt reduction, or additional property. A professional reinvests income into skills that raise earning power. A household reinvests savings from paid-off debt into retirement accounts.

The common principle is allowing returns to create more future returns instead of consuming every gain immediately.

There are times when reinvestment may not be appropriate. Retirees may need portfolio income for living expenses. A household may need to redirect gains toward emergency reserves, taxes, or debt reduction. An investor may choose not to reinvest in an asset that has become too concentrated or no longer fits the plan. Reinvestment should be intentional, not automatic without thought.

But for investors in the accumulation phase, reinvesting dividends and gains can be one of the simplest ways to accelerate compounding. It removes the temptation to treat every distribution as spendable income. It also keeps the portfolio aligned with growth unless rebalancing or cash needs require otherwise.

Compounding is often described as money working for you. Reinvestment is how you keep the workers on the job.

4. Stay Patient: Compounding Requires Years

Compounding is most disappointing at the beginning.

This is one of its great psychological challenges. The early years of investing often feel slow because contributions do most of the work. The balance rises, but not dramatically. A person may save and invest faithfully for several years and feel unimpressed. They may compare their progress with stories of sudden wealth from business exits, property booms, cryptocurrency surges, or individual stocks.

That comparison can be dangerous. Compounding does not usually announce itself early. It becomes powerful after the base has grown large enough for returns to matter. In the early stage, a 7 percent return on $5,000 is $350. In a later stage, a 7 percent return on $500,000 is $35,000. The percentage is the same. The lived experience is different.

Patience is therefore not passive. It is the discipline of staying invested during the period when the reward does not yet feel proportional to the effort.

Patience is also required because markets do not rise smoothly. Broad diversified investments can decline sharply. They can move sideways. They can test conviction. A long-term investor should expect volatility rather than treat it as evidence that the plan has failed.

This is where time horizon matters. Money needed in the next few months or years should not usually be exposed to the same volatility as money intended for retirement decades away. A patient investor is not someone who ignores risk. A patient investor matches the investment to the time horizon so that patience is possible.

The impatience problem often leads people into speculation. They become frustrated by slow compounding and start looking for shortcuts. Some shortcuts work for a few people. Many destroy capital. A person who abandons a sound long-term plan for a concentrated bet may lose not only money but compounding time that cannot be recovered.

Patience is easier when expectations are realistic. Compounding over decades can be powerful. Compounding over months is usually unimpressive. The investor who expects wealth to appear quickly may sabotage the process. The investor who expects the early years to feel ordinary is more likely to endure.

Wealth often grows quietly before it grows visibly.

5. Ignore Short-Term Market Noise Without Ignoring Your Plan

Short-term market noise is constant.

Every day brings headlines: inflation, interest rates, elections, earnings reports, recessions, wars, technology shifts, analyst forecasts, central bank decisions, currency movements, commodity prices, and market predictions. Some of these events matter. Many are impossible to translate into useful personal investment decisions.

The danger is that noise creates the illusion of necessary action. A headline appears, and the investor feels they must respond. Markets fall, and they consider selling. Markets rise, and they consider buying more aggressively. A sector becomes popular, and they wonder whether their diversified portfolio is too boring. A commentator sounds confident, and they question their plan.

Frequent reaction can damage compounding because it turns investing into emotional interruption. Morningstar’s Mind the Gap research focuses on the difference between fund returns and the returns investors actually experience, emphasizing that cash-flow timing and investor behavior can affect outcomes. ([morningstar.com](https://www.morningstar.com/business/insights/research/mind-the-gap?utm_source=chatgpt.com)) This matters because an investment can perform well while the average investor in it earns less due to poor timing decisions.

Ignoring noise does not mean ignoring reality. Investors should review portfolios periodically. Goals change. Risk tolerance changes. Time horizons shorten. Asset allocations drift. Fees can be reduced. Tax situations evolve. A person approaching retirement should not invest exactly like someone starting their first job. A household expecting a major expense should adjust liquidity.

The distinction is between review and reaction.

Review is scheduled, calm, and connected to goals. Reaction is emotional, urgent, and driven by headlines. Review asks whether the plan still fits. Reaction asks how to escape discomfort. Review considers allocation, costs, contributions, taxes, and risk capacity. Reaction often chases what just happened.

A practical approach is to create a written investment policy. It can define goals, time horizon, contribution rate, target allocation, rebalancing rules, liquidity needs, and conditions for making changes. The policy becomes a defense against short-term noise.

Compounding needs time. Noise constantly asks for interruption. The investor’s job is to know when action is necessary and when patience is the action.

6. Increase Contributions Over Time

Compounding is powered by both returns and contributions.

Many discussions of investing focus heavily on returns. People ask what the market will do, which fund will outperform, or which asset class will lead. These questions matter, but they can distract from one of the most controllable variables: the amount invested.

Increasing contributions over time can have a major effect on future wealth. A person who raises their savings rate with each raise, bonus, promotion, or debt payoff can accelerate compounding without needing to predict markets perfectly. The investor controls the contribution even when they cannot control the return.

This is also how households fight lifestyle inflation. When income rises, spending tends to rise unless a plan prevents it. A raise can become a larger apartment, better car, more restaurants, more travel, and more subscriptions. None of those choices may be wrong individually, but if every increase in income is absorbed by lifestyle, wealth accumulation remains slow.

A better habit is to assign a portion of every income increase to the future before lifestyle adjusts. If income rises by 10 percent, perhaps half of the increase goes to savings and investing. If a debt is paid off, the old payment can be redirected to retirement accounts or brokerage investments. If a bonus arrives, a percentage can be invested before discretionary spending begins.

Fidelity has argued that contributing even 1 percent more of salary to a tax-advantaged retirement account can make a meaningful difference over time, and it also suggests that savers who cannot immediately reach a 15 percent target can start with what they can afford and increase contributions after raises or promotions. ([fidelity.com](https://www.fidelity.com/viewpoints/retirement/save-more?utm_source=chatgpt.com)) ([fidelity.com](https://www.fidelity.com/learning-center/personal-finance/retirement/how-to-max-out-your-retirement-vp?utm_source=chatgpt.com)) The precise target depends on country, age, retirement system, income, employer benefits, and goals, but the principle is universal: contribution increases matter.

Increasing contributions also changes identity. The investor begins to see rising income not merely as permission to consume, but as a chance to buy more future freedom. This is one of the most important mindset shifts in personal finance.

The market may not cooperate every year. Contributions can.

7. Stay Disciplined: Consistency Beats Perfection

Perfect investing is impossible.

No investor knows the future with certainty. No one buys at every bottom, sells at every top, avoids every bad investment, chooses the best fund every year, and reacts perfectly to every economic change. The pursuit of perfection can become a trap. It encourages overthinking, delay, trading, and regret.

Discipline is more useful than perfection because discipline is repeatable.

Disciplined investors set goals, choose an appropriate strategy, invest regularly, control costs, diversify, rebalance when necessary, and avoid emotional overreaction. They understand that every year will not feel successful. Some years will be negative. Some years will produce modest returns. Some years will make other strategies look better. Discipline keeps the investor from abandoning the plan simply because another approach is temporarily more exciting.

Discipline is also required in household finance. A person must protect the contribution rate from lifestyle demands. They must avoid high-interest debt that competes with investing. They must keep emergency reserves so investments are not raided for ordinary surprises. They must review insurance, taxes, and financial goals. Compounding can be interrupted by poor financial structure outside the portfolio.

Behavioral finance matters because investors often damage their own outcomes. They chase performance, sell after losses, buy after hype, hold concentrated positions too long, or confuse recent luck with skill. Morningstar’s research on investor return gaps exists because what investors earn can differ from what investments report, depending on timing and behavior. ([morningstar.com](https://www.morningstar.com/en-gb/business/insights/research/mind-the-gap?utm_source=chatgpt.com))

Discipline can be engineered through systems. Automatic contributions reduce the need for monthly decisions. Target-date funds or diversified portfolios can reduce overtrading for some investors. Rebalancing rules reduce emotional allocation shifts. Separate accounts keep emergency money away from investments. Written plans prevent headlines from becoming strategy.

The disciplined investor does not need to be brilliant every month. They need to avoid repeated mistakes that stop compounding.

8. Trust the Process, With Caveats

“Trust the process” is useful if the process is sound.

It is dangerous if the process is vague, reckless, or misunderstood. A person should not trust a process that involves concentrated speculation, excessive leverage, high fees, no emergency fund, no diversification, and no understanding of risk. Blind faith is not financial discipline.

A process worth trusting has structure. It begins with clear goals. It matches investments to time horizon and risk tolerance. It uses diversification. It controls costs. It automates contributions where possible. It maintains liquidity. It reviews periodically. It avoids emotional decisions. It recognizes taxes and inflation. It adjusts when life changes.

Trusting that kind of process means accepting that every period will not feel good. Markets may decline. Some years may disappoint. Other investors may appear to get rich faster. Headlines may create fear. The process is not designed to eliminate discomfort. It is designed to keep discomfort from controlling behavior.

There must also be humility. Historical market returns are not guarantees. Diversified equities have historically rewarded long-term investors more than cash over long horizons, but they also bring volatility and periods of loss. Bonds carry interest-rate and credit risk. Real estate carries liquidity, maintenance, financing, and local-market risk. Cash carries inflation risk. Every asset has risk.

Trusting the process means trusting a risk-aware structure, not believing nothing can go wrong.

It also means knowing when to change the process. A change in goals, age, income stability, family obligations, tax situation, or time horizon may justify adjustment. A person approaching retirement may need a different allocation from the one they held at 30. A household expecting a home purchase may need more cash and less market exposure for that goal. A business owner with variable income may need larger reserves.

The process should be disciplined, not frozen.

Wealth rewards patience when patience is attached to a sound plan.

Why Compounding Feels Slow Before It Feels Powerful

Compounding is often misunderstood because its results are uneven over time.

In the beginning, most portfolio growth comes from contributions. This can feel discouraging because the account balance depends heavily on the investor’s own effort. The portfolio is not yet large enough for returns to do much visible work. A market decline can erase months of contributions, making the process feel pointless.

But this early stage is essential. It builds the base. Without the base, later compounding cannot occur. The investor who quits during the slow stage never reaches the powerful stage.

As the portfolio grows, returns begin to matter more. A 5 percent return on $10,000 is $500. A 5 percent return on $200,000 is $10,000. A 5 percent return on $1 million is $50,000. The same percentage becomes more meaningful as the base grows. This is why compounding can look like it accelerates later, even though the mathematics were operating all along.

This also explains why early withdrawals can be so damaging. Removing money from an investment account does not only reduce the current balance. It removes the future returns that money might have generated. Spending investment gains during the accumulation phase can feel harmless, but it reduces the snowball.

The emotional challenge is to respect the early stage. The investor must continue contributing when the visible reward is modest. They must allow time to transform effort into momentum.

Compounding is not linear in how it feels. It is often boring, then surprising.

Compounding Works Against Borrowers Too

Compounding is not always friendly.

The same principle that helps investors can hurt borrowers when interest accumulates on debt. High-interest debt can grow quickly because interest charges create larger balances, which then generate more interest. Credit card debt, payday loans, and other expensive borrowing can become the negative version of compounding.

This is why debt management is part of any serious compounding discussion. A person investing at a reasonable expected return while carrying high-interest consumer debt may be fighting themselves. The investment account grows on one side while debt compounds against them on the other.

Not all debt is harmful. A mortgage, education loan, or business loan may be productive if the cost is reasonable and the asset or opportunity is sound. But high-interest consumer debt is often a wealth destroyer because it claims future income without creating a productive asset.

The practical lesson is to compare interest rates, risk, and financial priorities. Paying down expensive debt can be one of the most powerful guaranteed improvements to a household’s financial position. Reducing a 20 percent credit card balance is not as glamorous as buying an investment, but it may be more urgent and more certain.

Compounding rewards ownership and punishes expensive dependency. The household must decide which side of the formula it wants to be on.

Inflation and the Real Value of Compounding

Investment growth must be understood after inflation.

A portfolio may grow in nominal terms while purchasing power grows less than expected. If an account rises by 6 percent and inflation is 3 percent, the real increase in purchasing power is much smaller than the account statement suggests. Over long periods, inflation can meaningfully erode cash and low-return assets.

This is one reason long-term investors often need exposure to growth assets. Cash is useful for emergencies and short-term goals, but holding too much long-term money in cash may expose the household to purchasing-power risk. A diversified portfolio can help address this risk, though it introduces market volatility.

The right balance depends on time horizon. Money needed soon should prioritize stability and liquidity. Money intended for decades from now may need growth to maintain and increase purchasing power. Confusing these purposes can create problems. Investing short-term cash too aggressively can force selling during downturns. Holding long-term money too conservatively can weaken future buying power.

Compounding should always be judged in real-life terms. The goal is not merely a larger number. The goal is greater future purchasing power, security, and choice.

Diversification: The Risk Control Behind Compounding

Compounding requires survival. Diversification supports survival.

A concentrated investment can compound spectacularly if it succeeds. It can also fail permanently. The danger of putting too much money into one company, one property, one cryptocurrency, one business, or one sector is that the investor’s future becomes tied to one outcome.

Diversification spreads risk across different assets, sectors, companies, geographies, or income sources. It does not guarantee profit. It does not prevent loss. In severe downturns, many assets can fall together. But diversification reduces the chance that one failure destroys the entire plan.

Vanguard’s principles explicitly include maintaining a balanced and diversified mix of investments. ([corporate.vanguard.com](https://corporate.vanguard.com/content/dam/corp/research/pdf/vanguards_principles_for_investing_success.pdf?utm_source=chatgpt.com)) This is central to compounding because the investor must remain invested long enough to benefit. A portfolio that is too concentrated may produce emotional or financial damage that causes the investor to quit.

Diversification should reflect goals. A young investor saving for retirement may hold a different mix from a retiree drawing income. A household with unstable employment may need more cash. A business owner with most wealth tied to a company may need outside investments for balance. A person with stock compensation from an employer may need to avoid overconcentration in that same company.

Compounding is powerful, but it needs a vehicle that can endure the road.

Costs: The Quiet Enemy of Compounding

Fees matter because they compound too.

An investment cost may look small as a percentage, but over decades it can reduce wealth meaningfully. Fund expense ratios, advisory fees, trading costs, commissions, tax inefficiency, account fees, and hidden product costs all reduce the amount that remains invested and available to compound.

This does not mean every paid service is bad. Good advice can be valuable, especially for tax planning, retirement decisions, estate planning, business owners, complex compensation, or behavioral coaching. The issue is whether the cost is transparent, reasonable, and justified by value.

Low-cost investing has become more accessible through index funds, exchange-traded funds, and retirement plan options. The growth of passive investing reflects, in part, investor awareness that costs are one of the variables they can control.

A high-cost investment must overcome its fees before the investor benefits. A low-cost investment allows more of the market return to remain with the investor. Over long horizons, that difference can compound.

Compounding rewards what stays invested. Costs remove fuel from the engine.

Investor Behavior: The Human Side of Compounding

The greatest threat to compounding is often not the market. It is the investor.

People buy after excitement. They sell after fear. They compare themselves with recent winners. They change strategies too often. They hold too much cash after downturns. They take risks they do not understand. They abandon boring plans because speculation looks more impressive.

This is why investor behavior has become such an important part of financial research. Morningstar’s Mind the Gap work examines how investor timing can cause experienced returns to differ from reported fund returns. ([morningstar.com](https://www.morningstar.com/business/insights/research/mind-the-gap?utm_source=chatgpt.com)) The lesson is direct: what you own matters, but how you behave with what you own also matters.

Good behavior can be supported by systems. Automate contributions. Avoid checking long-term accounts too frequently. Use a written plan. Keep emergency cash separate. Rebalance on a schedule. Limit speculative positions. Avoid investing based on social media urgency. Discuss major changes with a qualified adviser or a trusted financially literate person before acting.

The aim is not to remove emotion. That is impossible. The aim is to prevent emotion from making irreversible decisions during temporary stress.

Compounding is mathematical, but it depends on emotional endurance.

A Practical Compounding Framework

The first step is to stabilize the foundation. Pay attention to essential expenses, high-interest debt, emergency savings, insurance, and income stability. Investing without a basic financial buffer may lead to forced withdrawals later.

The second step is to define goals. Retirement, home purchase, education, business capital, financial independence, and emergency reserves all have different time horizons and risk requirements. Money should be invested according to purpose.

The third step is to automate contributions. Decide how much will be invested each month and make it automatic where possible. The goal is to remove the need for repeated willpower.

The fourth step is to choose diversified investments suited to the time horizon and risk tolerance. Many investors may use broad funds, retirement accounts, or professionally managed allocations. The specific choice depends on country, taxes, fees, employer plans, and personal circumstances.

The fifth step is to reinvest gains during the accumulation phase unless there is a clear reason not to. Let growth build on growth.

The sixth step is to increase contributions over time. Use raises, bonuses, debt payoff, and income growth as opportunities to raise the savings rate.

The seventh step is to review periodically. Check whether the portfolio still fits goals, risk tolerance, time horizon, and tax situation. Rebalance if necessary. Review costs. Avoid making changes only because of headlines.

The eighth step is to stay humble. Compounding is powerful, but markets are uncertain. Maintain diversification, liquidity, and realistic expectations.

What Compounding Teaches About Wealth

Compounding teaches that wealth is often less about brilliance than behavior.

The investor who starts early, contributes regularly, reinvests gains, increases contributions, controls costs, diversifies, and stays disciplined may outperform someone who constantly searches for the perfect opportunity but cannot act consistently. The simple plan held for decades can beat the sophisticated plan abandoned during stress.

Compounding also teaches that time has economic value. The earlier a person begins, the less pressure they may feel to chase extreme returns. The longer money remains invested, the more opportunity it has to grow. This is why delay can be costly even when no money is visibly lost. The lost asset is time.

It also teaches that small habits matter. A 1 percent increase in contributions, a reinvested dividend, a reduced fee, an avoided panic sale, or a skipped high-interest debt balance may seem minor. Over time, such decisions can produce meaningful differences.

Finally, compounding teaches humility. The investor does not control market returns. They control contributions, costs, diversification, behavior, and time in the plan. That is enough to matter, but not enough to guarantee perfection.

Final Thought: Compounding Rewards the Patient Owner

The science of compounding is not a promise of easy wealth. It is a framework for understanding how wealth can grow when time, money, and discipline work together.

Start now because time is the most valuable ingredient. Invest consistently because repeated contributions create momentum. Reinvest gains because growth builds on growth. Stay patient because compounding takes years before it becomes impressive. Ignore short-term noise because constant reaction interrupts the process. Increase contributions because savings rate is one of the most controllable drivers of future wealth. Stay disciplined because consistency beats perfection. Trust the process only when the process is sound, diversified, cost-aware, and aligned with your goals.

The limitations matter. Returns are not guaranteed. Inflation reduces purchasing power. Markets can decline. Diversification is essential. Asset allocation should match the time horizon. High-interest debt can compound against you. Investor behavior can damage results.

But the central lesson remains powerful: wealth does not always require dramatic moves. Often, it requires giving ordinary decisions enough time to become extraordinary.

Compounding is the quiet reward for patient ownership. It turns consistency into capital, capital into growth, and growth into future options. The process may look slow at first. That is not evidence it is failing. It is evidence that the most important work is still happening beneath the surface.