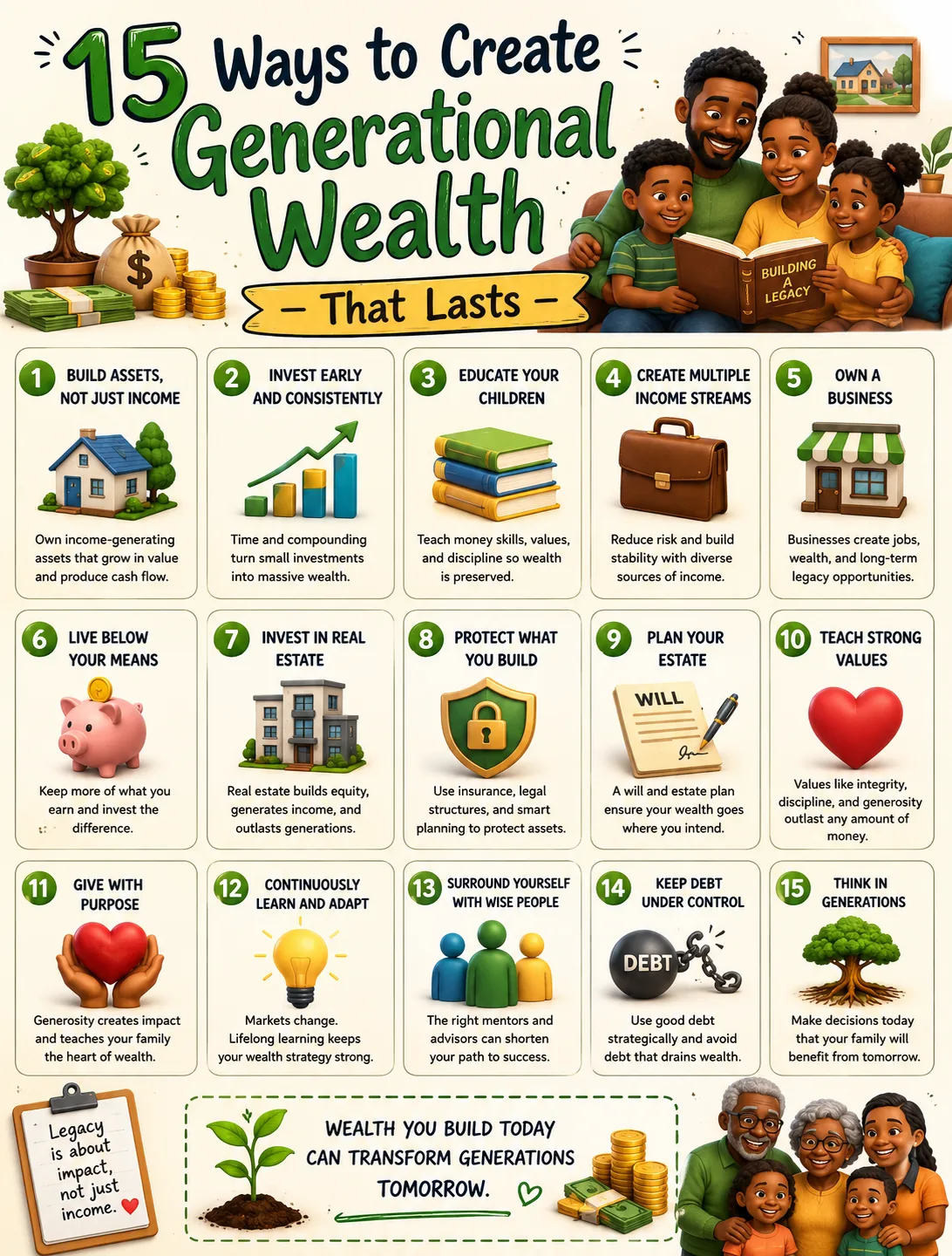

The Family Wealth System: How Assets Become a Multigenerational Legacy

Generational wealth is often imagined as a dramatic inheritance: a mansion, a family business, a portfolio of properties, a trust fund, or a large investment account quietly transferred from one generation to the next.

That image is incomplete.

Generational wealth is not merely the presence of assets. It is the presence of a system. A family can inherit money and lose it quickly. Another family can begin with modest income and, over decades, build education, habits, ownership, legal structure, insurance, investment discipline, and family values that change the financial path of children and grandchildren.

The difference is not luck alone. It is design.

A true family wealth system contains several parts. It increases earning power. It spends less than it earns. It protects against emergencies. It avoids destructive debt. It invests consistently. It diversifies. It owns productive assets. It plans for taxes and inheritance. It documents ownership. It insures against catastrophic loss. It teaches heirs how money works. It creates decision rules so that wealth is not destroyed by conflict, confusion, or entitlement.

Assets matter. But assets alone are not enough.

A house can become a blessing or a burden. A business can become an engine of opportunity or a source of lawsuits and family division. An investment account can compound for decades or be drained in a few years. A life insurance policy can protect dependants or become an expensive product no one understands. A trust can preserve wealth or fail because beneficiaries were never prepared to manage responsibility.

The most durable family wealth is built when financial capital and human capital grow together. Financial capital is money, property, investments, businesses, and other assets. Human capital is skill, education, judgment, health, discipline, networks, and the ability to create economic value. Families that transfer money without judgment often transfer fragility. Families that transfer judgment without capital may still leave the next generation struggling for opportunity. The goal is to build both.

Generational wealth is not reserved for dynasties. It can begin with a household budget, a debt-repayment plan, an emergency fund, a retirement account, a small business, a rental property, a professional skill, a life insurance policy, a will, or a conversation with a child about saving. It grows through ordinary decisions repeated with uncommon consistency.

The work is slower than fantasy. It is also more powerful.

1. Increase the Family’s Earning Power

The first source of investable capital is usually earned income.

Before a family can buy assets, it must create surplus. Surplus comes from the gap between what the family earns and what it consumes. The larger and more stable that gap becomes, the more capital can be directed toward savings, debt reduction, investment, business formation, insurance, education, and property ownership.

This is why earning power is the first pillar of generational wealth.

Earning power is not only salary. It includes professional skill, technical ability, trade expertise, entrepreneurship, sales ability, leadership, negotiation, career mobility, and the capacity to adapt when industries change. A family’s wealth often begins not with an investment account but with one person acquiring a skill the market values.

Education can play a major role, though it should be understood broadly. University degrees, apprenticeships, professional certifications, technical training, coding boot camps, licenses, language skills, financial education, management training, and practical business experience can all increase earning capacity. The point is not prestige. The point is economic usefulness.

Families that build generational wealth often treat skill development as an asset class. They invest in education not as consumption but as productive capacity. They help children avoid unnecessary educational debt where possible. They encourage career paths that combine interest with market demand. They teach negotiation, communication, reliability, and problem-solving. They build professional networks. They understand that a person who can earn well has more options than a person who depends entirely on inherited assets.

Human capital is especially important for families starting without wealth. A high-income skill can create the first stream of surplus. A trade can fund a property. A profession can fund retirement accounts. A business skill can create equity. A technical skill can open global labor markets. A sales skill can raise income across industries. A management skill can turn a small enterprise into a transferable company.

But income alone is not wealth. Many high earners remain financially fragile because spending rises at the same pace as income. Earning power creates the opportunity. Discipline converts the opportunity into assets.

The family that wants generational wealth should ask: What skills are we building? Which careers are becoming more valuable? Which abilities can survive technological change? Which family members need training, mentorship, or credentials? Which children are being taught not only to get good grades, but to understand how value is created in the economy?

The first inheritance a family can provide is not money. It is capability.

2. Spend Less Than the Family Earns

Wealth cannot accumulate if every increase in income becomes an increase in consumption.

This is one of the simplest financial truths and one of the hardest to live by. A family may earn more over time, but if housing, vehicles, holidays, dining, subscriptions, gifts, clothing, school fees, and social expectations rise just as quickly, the household remains trapped. The lifestyle improves, but ownership does not.

Generational wealth requires margin.

Margin is the space between income and spending. It is the money that can be redirected toward assets instead of being absorbed by lifestyle. Without margin, there is no emergency fund. No investment account. No debt reduction. No business capital. No property down payment. No insurance buffer. No education fund. No estate-planning budget. The family may look successful but have no financial engine.

Spending less than the family earns does not require misery. It requires intentionality. A family wealth plan should define essential spending, savings targets, investment contributions, debt-reduction goals, and limits on lifestyle inflation. The goal is not to eliminate pleasure. The goal is to prevent consumption from quietly stealing the future.

Lifestyle inflation is especially dangerous because it feels normal. A raise becomes a larger apartment. A bonus becomes a car upgrade. A promotion becomes private clubs, expensive trips, and higher recurring obligations. Over time, the family becomes dependent on a high income just to maintain its lifestyle. If income falls, the household is exposed.

Generational wealth often grows in families that learn to delay visible status. They may drive modest cars while buying assets. They may live below what lenders would approve. They may automate investments before discretionary spending. They may celebrate milestones without turning every improvement into a permanent monthly cost. Their wealth grows because their surplus is protected.

Budgeting is not a low-income habit. It is a visibility tool. Wealthy families, successful businesses, and institutions all track cash flow because what is not measured is easily wasted. A family budget does not need to be complex. It needs to answer four questions: What comes in? What goes out? What must be protected? What can be invested?

Children learn from this. If they grow up seeing every dollar used for consumption, they inherit appetite. If they see money divided into giving, saving, investing, learning, and spending, they inherit a system.

Spending less than you earn is not the entire wealth plan. But it is the gate through which every other strategy must pass.

3. Build an Emergency Fund

An emergency fund is the family’s first defense against financial reversal.

It is safe, accessible money reserved for unplanned expenses and income disruptions. Medical bills, job loss, property repairs, urgent travel, family emergencies, business slowdowns, legal costs, and economic shocks can arrive without warning. Without emergency savings, the family may be forced to borrow at high interest, sell investments at the wrong time, delay important repairs, or rely on relatives.

Emergency reserves protect long-term wealth because they prevent short-term crises from damaging productive assets.

A family that has invested for decades should not have to sell shares during a market decline because the roof leaks. A business owner should not have to take desperate financing because sales slow for two months. A parent should not have to use a credit card at high interest because a child needs medical care. A property owner should not miss a mortgage payment because a tenant leaves unexpectedly.

Cash reserves are often criticized for earning low returns. That criticism misunderstands their role. The emergency fund is not designed to outperform the stock market. It is designed to stop the family from interrupting compounding. The return on an emergency fund is the crisis that does not become permanent.

The right size depends on the family’s situation. A dual-income household with stable jobs, low debt, strong insurance, and no dependants may need a smaller reserve than a single-income family with children, elderly parents, irregular income, a business, or multiple properties. Entrepreneurs often need larger reserves because business income can be uneven. Retirees may need reserves to avoid selling investments during downturns.

The emergency fund should be separate from investment capital. It should not be placed in speculative assets. It should not depend on selling cryptocurrency, private investments, collectibles, or property. It should be liquid enough to use when life becomes inconvenient.

Families building generational wealth should also teach younger members the purpose of liquidity. Cash is not a failure of ambition. It is a form of resilience. The family with reserves has choices. It can wait, negotiate, recover, and avoid panic. The family without reserves may be forced to accept whatever terms the crisis offers.

The first layer of wealth is not return. It is stability.

4. Eliminate Destructive Debt

Debt can either accelerate wealth or destroy it.

The difference lies in cost, purpose, structure, and cash flow. Productive debt may help acquire an asset that generates income or appreciates over time, such as a carefully financed rental property, business equipment, or expansion capital. Destructive debt finances consumption at high interest, compounds against the borrower, and leaves no asset strong enough to justify the burden.

Credit-card balances, payday loans, high-cost personal loans, tax arrears, debt in default, and unnecessary consumer financing can quietly drain a family’s future. Every interest payment sent to a lender is money that cannot be invested. When the interest rate is high, the family’s income is being used to enrich someone else’s balance sheet.

Generational wealth requires reversing the direction of compounding. Instead of interest compounding against the family, assets must compound for it.

Debt repayment should be prioritized by danger. Debts in default, tax debts, and obligations that threaten housing, employment, legal standing, or essential assets deserve urgent attention. High-interest consumer debt should usually be eliminated before speculative investing. Variable-rate debt should be reviewed carefully because rising rates can increase payments. Secured debt should be respected because failure can mean losing the asset attached to it.

Low-cost debt is more nuanced. A fixed-rate mortgage on a reasonable home may not need to be paid off immediately if the family has adequate reserves and can invest elsewhere. A business loan may be appropriate if cash flow supports it and the return on capital is strong. But even productive debt must be managed conservatively. Leverage turns mistakes into larger mistakes.

Families should also be cautious about informal debt between relatives. Loans to family members can become emotionally complicated, especially if repayment is uncertain. If the money is truly a gift, call it a gift. If it is a loan, document it properly. Ambiguity damages both finances and relationships.

One of the most powerful gifts a generation can give the next is freedom from financial habits that normalize destructive borrowing. Children who grow up seeing credit used to fund lifestyle may repeat the pattern. Children who learn that debt must be evaluated by cost, purpose, and risk inherit a stronger framework.

Debt is not automatically immoral. But debt without discipline is anti-wealth. It claims tomorrow’s income before tomorrow arrives.

5. Invest Consistently for Decades

Generational wealth is often less dramatic than people imagine. It is frequently built through ordinary investing repeated for extraordinary lengths of time.

Consistent investing works because it combines surplus, ownership, and compounding. A family that invests regularly in diversified assets gives time the opportunity to do what time does best: turn small repeated contributions into meaningful capital.

Compounding means earnings can generate additional earnings. A portfolio that produces returns can reinvest those returns, increasing the base on which future returns are earned. Over decades, this process can become powerful. The earlier the family begins, the less it must rely on heroic contributions later.

Potential vehicles may include broad stock-market funds, bond funds, retirement accounts, pension plans, regulated mutual funds, and exchange-traded funds. The right structure depends on jurisdiction, taxes, employer benefits, income level, risk tolerance, and time horizon. The deeper principle is that investment should become a family habit, not an occasional event driven by excitement.

Automatic contributions can help. When money moves into investments before discretionary spending, the family reduces the temptation to invest only what is left. Regular investment also reduces the pressure to perfectly time markets. No family can know in advance which month will be ideal. Consistency creates participation.

Long-term investing is not the same as ignoring risk. Asset allocation matters. Fees matter. Taxes matter. Diversification matters. Time horizon matters. A portfolio for a child’s education in three years should not be invested the same way as a portfolio for retirement in thirty years. But the principle remains: wealth grows when capital is put to work patiently.

The family should avoid confusing investing with trading. Trading seeks short-term advantage. Investing seeks ownership and compounding. Some people can trade successfully, but for most families, frequent speculation increases costs, taxes, stress, and the likelihood of mistakes. Generational wealth is rarely built by chasing every market trend.

Consistent investing also teaches heirs a crucial lesson: wealth is not magic. It is behavior repeated across time. A child who watches parents invest every month learns that ownership is normal. A young adult who starts investing early learns that small amounts matter. A family that discusses compounding teaches patience in a culture of immediacy.

Decades are an underrated asset. Families that use them well can turn modest beginnings into durable financial strength.

6. Diversify the Family’s Investments

Concentrated wealth is vulnerable wealth.

A family may become wealthy through concentration: one business, one property, one employer, one stock, one industry, one currency, or one fortunate investment. But the strategy that creates wealth is not always the strategy that preserves it.

Diversification means spreading exposure across different assets so that the failure of one does not determine the fate of the family. It cannot eliminate loss. It cannot prevent market declines. It does not guarantee success. But it can reduce the damage caused by a single point of failure.

This is especially important for families whose identity and finances are tied to one asset. A business owner may have most of the family’s net worth in the company. A property-owning family may depend entirely on one neighborhood or one type of tenant. An employee may hold employer stock while also relying on the same employer for salary. A farmer may depend on land, weather, commodity prices, and local policy. A founder may have enormous paper wealth but little liquidity.

Diversification is not betrayal of the asset that created wealth. It is respect for uncertainty.

A diversified family balance sheet may include cash reserves, bonds, domestic and international equities, property, business ownership, retirement accounts, and other carefully assessed assets. The exact mix should match goals, taxes, liquidity needs, and risk tolerance. The objective is to make the family resilient across economic conditions.

Diversification also includes income diversification. A household dependent on one salary is more fragile than one with two incomes, investment income, rental income, business income, or royalties. A business dependent on one customer is fragile. A portfolio dependent on one market is fragile. A family whose wealth can survive multiple shocks is stronger than a family that appears richer but is concentrated.

There is a balance. Over-diversification into poorly understood assets can create confusion. Buying many investments without strategy is not wisdom. The family should understand what each asset does, how it behaves, and why it belongs in the plan.

Still, the principle is clear: no single asset should have the power to ruin the family.

7. Own a Sustainable Business

Business ownership can be one of the strongest engines of generational wealth.

A successful business can produce income, employment, intellectual property, brand value, strategic control, tax planning opportunities, transferable equity, and a saleable asset. Unlike wages, business ownership can separate income from one person’s hours. Unlike passive investments, it can allow direct influence over growth.

But a business is not automatically generational wealth.

Many businesses are really demanding jobs owned by the founder. If customers depend entirely on one person, accounts are disorganized, systems are undocumented, employees cannot make decisions, and no successor exists, the business may generate income but have limited transferable value. When the founder becomes ill, retires, or dies, the family may discover that the “asset” was largely the founder’s personal effort.

To become generational, a business needs structure.

It needs clean financial statements. It needs separation between business and personal expenses. It needs documented processes. It needs legal ownership records. It needs management depth. It needs customer relationships that do not depend solely on one individual. It needs contracts, compliance, insurance, tax planning, and succession. It needs a strategy for whether future generations will operate it, own it passively, sell it, or hire professional managers.

Family businesses are especially sensitive because they combine money, identity, control, and emotion. A child who works in the company may expect leadership. A child who does not work in the company may expect equal ownership. A spouse may depend on dividends. Siblings may disagree about whether to reinvest profits or distribute cash. Without governance, the business can become the battlefield on which family tensions are fought.

Business succession should begin long before the founder is ready to leave. Future leaders need training, accountability, and real experience. Ownership rules should be documented. Voting rights, compensation, employment standards, buyout provisions, and dispute-resolution processes should be clear. A family should decide whether ownership is a birthright, a responsibility, or both.

A sustainable business can change a family’s trajectory for generations. It can fund education, create jobs, support philanthropy, and build identity around enterprise. But it must be professionalized. The goal is not merely to keep the business in the family. The goal is to make sure the family does not destroy the business.

8. Acquire Income-Producing Real Estate Carefully

Real estate has built many family fortunes because it combines utility, income, leverage, inflation sensitivity, and long-term ownership.

Property can contribute to generational wealth through rental income, appreciation, debt repayment by tenants, business premises, farmland, development rights, or productive land. A family that buys well, finances prudently, maintains properly, and holds patiently may create assets that support future generations.

But real estate is often romanticized.

A property is not profitable merely because it is tangible. The investment must be evaluated after mortgage payments, interest rates, taxes, insurance, maintenance, vacancies, repairs, management, legal obligations, tenant risk, transaction costs, and local market conditions. A building with poor cash flow can drain a family. A property bought at the wrong price can underperform for years. A highly leveraged portfolio can become dangerous when interest rates rise or tenants leave.

The primary residence deserves special care in family wealth discussions. Owning a home can provide stability, control, and equity. It can protect a family from rent inflation and create a forced-saving effect through mortgage repayment. But it should not automatically be treated as a high-return investment. A large home can also create high taxes, maintenance costs, insurance costs, and illiquidity. The family home may be emotionally valuable while financially inefficient.

Rental real estate is different. It should be analyzed like a business. What is the expected rent? What are realistic vacancy assumptions? What repairs are likely? Who manages the property? What does insurance cost? Are there legal restrictions? What happens if the tenant stops paying? How much debt is being used? Is there a reserve fund for capital expenses?

Families that build wealth through property usually respect maintenance and records. They keep titles clear. They document leases. They maintain insurance. They track expenses. They plan for repairs before emergencies. They avoid treating rental income as fully spendable because buildings age and capital needs return.

Real estate can also create inheritance complexity. Multiple heirs may disagree about whether to sell or keep a property. One child may live in the home. Another may need cash. A rental portfolio may require management. A farm may carry identity as well as economic value. Estate documents should explain ownership, decision rights, and succession intentions.

Property can be a pillar of generational wealth. But it rewards families that treat it with arithmetic, not mythology.

9. Create Intellectual Property

Intellectual property can turn ideas into assets.

Books, music, patents, trademarks, software, educational programs, designs, licensing rights, proprietary processes, media libraries, and creative works can produce income beyond the creator’s direct labor. This makes intellectual property especially powerful in a family wealth system. It can scale, travel, and sometimes continue earning after the original creator is no longer working.

A professional may create a training program. A musician may own royalties. A software developer may build code that is licensed. A writer may own publishing rights. A designer may create patterns or trademarks. A business may develop proprietary processes, customer data, brand assets, or technology. A teacher may build a course. A family may own rights that can be renewed, licensed, sold, or inherited.

The key is ownership.

An idea is not enough. The rights must be documented. Contracts must clarify who owns the work. Trademarks, copyrights, patents, licensing agreements, royalties, and usage rights need proper records. If intellectual property is created inside a business, ownership should be assigned correctly. If a creator dies, heirs need to know what exists, where revenue comes from, and who can administer the rights.

Intellectual property is often neglected in estate planning because it does not look like traditional wealth. A bank account is obvious. A house is obvious. A royalty stream, domain name, software repository, online course, manuscript, brand asset, or licensing contract may be overlooked. Yet these assets can be valuable and difficult to reconstruct after death.

Families should create an intellectual-property inventory. It should list registered rights, contracts, platforms, passwords, royalty accounts, renewal deadlines, business entities, collaborators, and revenue history. It should identify who has the skill to manage or monetize the assets.

Intellectual property can also teach younger generations a powerful lesson: ownership can come from creativity, not only capital. A family does not need to begin rich to build assets. Knowledge, art, technology, design, teaching, and invention can become economic property when protected and distributed properly.

Still, not all intellectual property becomes valuable. Creation must meet demand. Rights must be enforceable. Distribution matters. A book no one reads, software no one uses, or a patent no one licenses may have little economic value. IP becomes wealth when it is connected to markets.

The family that owns ideas and understands how to monetize them adds a modern layer to generational wealth.

10. Use Tax-Advantaged Structures Legally

Taxes can quietly determine how much wealth survives.

A family that earns, invests, sells, gifts, inherits, and transfers assets without tax awareness may lose more capital than necessary. A family that uses lawful structures wisely may preserve more for reinvestment, education, retirement, philanthropy, and heirs.

Tax-advantaged structures vary by country. Depending on the jurisdiction, families may use retirement accounts, pension schemes, education savings plans, tax-efficient investment accounts, family businesses, trusts, charitable structures, insurance arrangements, or estate-planning tools. The details matter enormously. What is beneficial in one country may be irrelevant or harmful in another.

The principle is not to avoid taxes at any cost. The principle is to avoid unnecessary tax drag while remaining compliant.

There is a major difference between lawful tax planning and aggressive schemes. Lawful planning uses established rules, proper documentation, qualified advice, and transparent reporting. Aggressive schemes often rely on secrecy, artificial transactions, unrealistic promises, offshore confusion, social media promoters, or pressure to act quickly. Families building multigenerational wealth should avoid strategies they cannot explain and professionals who discourage independent review.

Tax planning affects many decisions. Which account should hold which investment? When should assets be sold? Should appreciated assets be gifted or inherited? How should a business be owned? How should retirement accounts name beneficiaries? Should charitable giving occur during life or at death? How should property be titled? What records are needed to establish cost basis? What happens when heirs live in different jurisdictions?

Small tax efficiencies can compound. So can tax mistakes.

Families should work with qualified tax professionals who understand their assets, country, residency, business interests, and estate goals. Advice should be written, current, and coordinated with legal and investment planning. Tax rules change. A structure that worked ten years ago may no longer be ideal.

Taxes should not be allowed to dominate every decision. Sometimes paying tax is the result of making money. Sometimes simplicity is worth more than a complex structure. Sometimes liquidity, family harmony, or investment quality matters more than minimizing tax. But no family wealth system is complete if taxes are ignored.

Generational wealth is not only about earning returns. It is about keeping enough of those returns in the family system to keep compounding.

11. Create a Will and Estate Plan

Without an estate plan, the law may make decisions the family never intended.

An estate plan is a coordinated set of instructions for managing and transferring assets during incapacity and after death. It may include a will, beneficiary designations, powers of attorney, medical directives, guardianship instructions, trust arrangements, business-succession documents, and an inventory of assets and liabilities.

Many people delay estate planning because they believe it is only for the old or the very rich. That delay can be costly. A young parent needs guardianship instructions. A business owner needs succession documents. A property owner needs clear title planning. A person with retirement accounts needs beneficiary designations. A person with digital assets needs access instructions. A blended family needs clarity. A wealthy household needs tax and trust coordination.

A will is important, but it is not always enough. Some assets pass outside the will through beneficiary forms, joint ownership, payable-on-death designations, trust ownership, or corporate agreements. If these documents conflict, the result may surprise the family. A carefully written will cannot always override an outdated beneficiary form.

Estate planning also addresses incapacity. If a parent, founder, investor, or property owner becomes unable to act, who can pay bills, manage accounts, operate the business, sign documents, or make medical decisions? Without powers of attorney and medical directives, the family may face delays, court processes, and conflict during an already painful time.

For families with businesses, estate planning should connect to succession planning. Who owns the shares? Who votes? Who manages? Can heirs sell? Must the business buy back ownership? How will estate taxes or inheritance obligations be funded? Is there insurance to provide liquidity? What happens if one child works in the business and another does not?

Estate planning is not a one-time event. It should be reviewed after marriage, divorce, births, deaths, business sales, property purchases, relocation, major tax changes, and significant wealth changes. An outdated estate plan can create false confidence.

The purpose of estate planning is not only asset transfer. It is family protection. It reduces ambiguity. It lowers administrative burden. It helps prevent disputes. It gives wealth a legal path to the people and purposes the owner intended.

Love is not a substitute for documentation.

12. Review Beneficiaries and Asset Ownership

Beneficiary designations and ownership records are the hidden wiring of wealth transfer.

A family may spend months writing a will while ignoring the forms that actually control major assets. Retirement accounts, insurance policies, jointly owned property, bank accounts, payable-on-death accounts, investment accounts, trust assets, corporate shares, and digital platforms may transfer according to documents outside the will.

This is why regular beneficiary reviews are essential.

Outdated forms can redirect wealth to the wrong person. A former spouse may remain named on an insurance policy. A deceased parent may still be listed. A minor child may be named directly without a trust or guardian structure. A new spouse may be omitted. A business partner may have unclear rights. A property may be jointly titled in a way that conflicts with the broader plan.

Asset ownership must also be reviewed. Who legally owns the house? Who owns the rental property? Are business shares held personally, through a company, or through a trust? Are investment accounts individual, joint, corporate, or custodial? Are intellectual-property rights assigned correctly? Are digital assets accessible? Are titles consistent with tax and estate-planning goals?

The legal owner is not always who the family assumes it is.

Families should maintain a wealth map that lists every major asset, owner, beneficiary, account, policy, debt, title, and governing document. This map should be reviewed periodically and after major life events. It should be stored securely but be accessible to the appropriate people if needed.

Ownership mistakes can be especially costly for blended families, unmarried partners, family businesses, and assets in multiple jurisdictions. Informal promises may not hold. Verbal agreements may be forgotten or disputed. Documents decide.

This is one of the least glamorous parts of generational wealth, yet it is one of the most important. Families do not lose wealth only through bad investments. They lose it through paperwork errors, outdated forms, unclear ownership, and assets that never reach the intended heirs.

Generational wealth requires legal accuracy. The family must know not only what it owns, but who owns it and where it goes next.

13. Protect the Family With Appropriate Insurance

Insurance is the defensive wall around a family wealth system.

Unexpected death, disability, illness, property loss, lawsuits, business interruption, or professional liability can destroy decades of savings and investment. A family may build assets carefully, only to lose them because a major risk was uninsured or underinsured.

The purpose of insurance is not to buy every policy available. It is to transfer risks that the family cannot afford to carry alone.

Life insurance may protect dependants if an income earner dies prematurely. Disability insurance may protect income if a worker cannot continue. Health insurance may reduce the financial impact of illness. Property insurance may protect homes, rental properties, or business premises. Business interruption insurance may help if operations are disrupted. Professional liability coverage may protect against claims. Umbrella liability insurance may provide additional protection above standard policies.

Insurance needs change over time. A young parent with dependants may need substantial life insurance. A retiree with grown children and sufficient assets may need less. A landlord needs different coverage from a renter. A business owner needs different protection from a salaried employee. A high-net-worth family may need liability coverage that reflects its asset base.

Complex policies that combine insurance and investment require careful review. Some may be appropriate in specific circumstances, but they can also carry high fees, surrender charges, opaque returns, and sales incentives. Families should understand what portion of the policy is protection, what portion is investment, what fees apply, and what alternatives exist.

Insurance also supports estate and succession planning. A family business may need insurance to fund a buyout or provide liquidity after the death of an owner. Parents may use insurance to provide for children while illiquid assets pass through legal processes. Property owners may need coverage that protects rental income and liability. Families with significant wealth may use insurance as part of broader planning, but only with qualified advice.

The emotional value of insurance is peace. It allows the family to build aggressively in some areas because catastrophic risks are addressed elsewhere. It prevents one tragedy from forcing asset sales at the worst possible time.

Generational wealth is not only about what the family builds. It is about what the family survives.

14. Teach Financial Capability to the Next Generation

An inheritance without financial competence can disappear quickly.

This is why financial education is not optional. It is part of the wealth transfer. A family that passes down assets but not judgment has completed only half the task.

Children and younger family members should gradually learn budgeting, saving, investing, taxes, credit, debt, insurance, business economics, fraud detection, giving, and estate responsibilities. The lessons should be age-appropriate and practical. A young child can learn the difference between spending and saving. A teenager can learn budgeting and compound growth. A young adult can learn credit, investing, taxes, and employment benefits. A future heir can learn trust responsibility, business governance, philanthropy, and asset stewardship.

Financial education should be lived, not merely lectured.

A family might review a simple household budget together. Parents might explain why they invest automatically. A teenager might manage a small investment account under supervision. Young adults might participate in charitable decisions. Future business heirs might attend meetings, read financial statements, or work outside the family company before entering it. Family members might discuss mistakes as well as successes.

One of the most valuable lessons is the difference between income and wealth. A person can earn a lot and own little. Another can earn moderately and build assets steadily. Children who understand this are less likely to confuse spending with success.

Another lesson is fraud awareness. Families with assets become targets. Younger heirs may be approached by scammers, manipulative friends, romantic partners, speculative promoters, or people offering guaranteed returns. Teaching skepticism is an act of protection.

Financial capability also includes emotional maturity. Heirs need to understand that wealth brings responsibility, not just consumption. They need to learn how to say no, how to evaluate requests, how to work with advisers, how to read documents, how to ask questions, and how to live with privilege without losing purpose.

Families sometimes hide all financial information from children to avoid entitlement. The concern is understandable. But total secrecy can create unprepared heirs. The better approach is progressive disclosure: teach principles early, reveal responsibilities gradually, and connect wealth to values, work, and stewardship.

The next generation does not need to know everything at once. But they should not inherit blindly.

15. Build Family Governance and a Succession System

As family wealth becomes larger or more complex, informal decision-making becomes risky.

Family governance is the system by which a family makes decisions about shared assets, businesses, investments, distributions, employment, philanthropy, conflict, and succession. It turns wealth from a collection of assets into a coordinated institution.

Governance may sound formal, but its purpose is practical. Who manages investments? Who may work in the family business? What qualifications are required for leadership? How are distributions approved? When can assets be sold? How are disputes resolved? Who communicates with advisers? How are younger members educated? What values guide investment and giving?

Without governance, families often rely on personality. The founder decides. The strongest sibling dominates. The loudest relative pressures. The most financially needy person receives attention. Decisions become reactive. Resentment grows. Wealth becomes emotional territory.

A governance system creates rules before conflict.

For a modest family, governance may be as simple as an annual family financial review, updated estate documents, a shared asset inventory, and clear beneficiary designations. For a family business, it may include employment policies, shareholder agreements, board structures, compensation rules, and succession plans. For larger wealth, it may include family councils, investment committees, trust governance, philanthropic boards, and formal education programs.

Succession is central. Every important role needs a future. Who succeeds the founder? Who manages the properties? Who administers intellectual property? Who speaks to the lawyer? Who understands the investment policy? Who can access documents? Who leads family meetings? Who has authority in an emergency?

Succession is not only about death. It is about continuity. A founder may become tired. A parent may become ill. A key adviser may retire. A child may prove capable. A business may outgrow family management. Governance allows the system to adapt.

Families should also define their values. Wealth without values becomes a prize to fight over. Wealth with values can become a mission. Education, enterprise, service, independence, philanthropy, faith, creativity, community, stewardship, or resilience may become guiding principles. Values do not eliminate financial disagreements, but they provide a language for resolving them.

Generational wealth survives when decision-making survives the original wealth creator.

The Assets Most Capable of Lasting

Not all assets are equally capable of carrying wealth across generations.

Some assets are liquid and easy to divide, such as diversified investment accounts. Some are tangible but management-intensive, such as real estate. Some are powerful but fragile, such as operating businesses. Some are scalable but legally complex, such as intellectual property. Some are protective rather than growth-oriented, such as insurance. Some are not assets in the traditional sense but may be the most important inheritance of all: education, health, habits, and networks.

The strongest family wealth systems often combine several asset types. Financial portfolios provide liquidity and diversification. Real estate may provide income and inflation sensitivity. Businesses may provide control and growth. Intellectual property may provide scalable recurring income. Insurance protects against shocks. Education and skills allow each generation to create value rather than merely consume assets.

Balance matters. A family with only property may be illiquid. A family with only a business may be concentrated. A family with only cash may lose purchasing power. A family with only inheritance and no education may lose discipline. A family with only professional income and no assets may remain dependent on labor.

The most resilient families build layers.

Layer one is stability: emergency reserves, insurance, debt control, and basic legal documents. Layer two is accumulation: consistent investing, retirement planning, and diversification. Layer three is productive ownership: real estate, business equity, intellectual property, and income-producing assets. Layer four is transfer: estate planning, tax planning, beneficiary accuracy, and succession. Layer five is stewardship: financial education, governance, values, and responsibility.

A family that builds all five layers has more than wealth. It has continuity.

Common Mistakes That Interrupt Generational Wealth

Generational wealth is often lost through predictable mistakes.

The first is lifestyle inflation. The family earns more, but spending rises faster. Visible success replaces invisible ownership. The next generation inherits habits, not assets.

The second is destructive debt. High-interest borrowing consumes surplus and reverses compounding. The family works for creditors instead of building capital.

The third is concentration. One business, one stock, one property, or one person carries too much responsibility. When that asset fails, the family has no protection.

The fourth is poor documentation. Missing wills, outdated beneficiaries, unclear titles, informal partnerships, and disorganized records can undo years of planning.

The fifth is underinsurance. A death, disability, lawsuit, illness, fire, or business interruption forces asset sales or creates debt.

The sixth is unprepared heirs. Children receive money without financial education, emotional maturity, or decision-making experience.

The seventh is family conflict. Siblings disagree. Second spouses and children clash. Business roles are unclear. Some heirs want income while others want growth. No process exists for resolving disputes.

The eighth is tax neglect. Assets are sold, gifted, transferred, or inherited without understanding the tax consequences.

The ninth is fraud. Families with money attract promoters, scammers, and advisers with conflicts. A single bad scheme can destroy trust as well as capital.

The tenth is assuming wealth will manage itself. It will not. Wealth requires administration. Accounts must be reviewed. Documents must be updated. Properties must be maintained. Businesses must be led. Heirs must be prepared.

These mistakes are common because they are human. They involve pride, avoidance, fear, secrecy, overconfidence, and emotion. A family wealth system exists to reduce the damage of human weakness.

The Family Wealth Map

One practical tool can reveal whether a family has a collection of assets or a true wealth system: the family wealth map.

A family wealth map lists every major asset, liability, income source, owner, beneficiary, insurance policy, legal document, tax exposure, and intended successor. It includes bank accounts, investment accounts, retirement plans, pensions, real estate, business interests, intellectual property, insurance policies, loans, credit cards, tax obligations, trusts, wills, powers of attorney, medical directives, digital assets, and key advisers.

For each asset, the map should answer: What is it? Who owns it? What is it worth? Does it produce income? Is there debt against it? Who inherits it? Where are the documents? What tax issues may apply? Who can manage it if the current owner cannot?

For each liability, it should answer: Who owes it? What is the interest rate? Is it secured? What is the repayment plan? What happens if the borrower dies or becomes disabled?

For each insurance policy, it should answer: What risk does it cover? Who is insured? Who is the beneficiary? Is the coverage still appropriate? When does it expire? What are the exclusions?

For each legal document, it should answer: When was it created? Where is it stored? Who prepared it? Does it reflect current family circumstances? Does it coordinate with beneficiary designations and ownership titles?

The family wealth map does not need to be shared with everyone in full detail. Privacy matters. But the right people should know that it exists and how to access it in an emergency. A beautifully designed plan that no one can find is not a plan.

Creating the map often reveals gaps immediately. A missing beneficiary. An old will. A forgotten retirement account. A rental property without adequate insurance. A business with no succession document. A valuable digital asset with no access instructions. A loan no one else knows about. These discoveries are not failures. They are opportunities to protect the family before a crisis exposes the weakness.

Generational wealth becomes real when it can be understood by someone other than the person who built it.

The Mindset of Stewardship

Generational wealth requires a different mindset from personal wealth.

Personal wealth asks, “What can this money do for me?” Generational wealth asks, “What should this money make possible after me?”

That question changes behavior. It encourages patience over display. Ownership over consumption. Education over entitlement. Protection over recklessness. Clarity over secrecy. Governance over personality. Long-term thinking over impulse.

Stewardship does not mean never enjoying money. A family that builds wealth can live well, travel, give, celebrate, and create comfort. But enjoyment must be integrated into the system rather than allowed to consume it. The family should know how much can be spent without weakening the foundation.

Stewardship also means each generation has responsibility. The first generation may create the surplus. The second may professionalize the assets. The third may need to preserve values while adapting to a new economy. No generation should see itself merely as a consumer of what came before.

This is where family stories matter. Children should know how the wealth was built. They should understand sacrifice, mistakes, discipline, and risk. A portfolio without a story can feel like free money. A portfolio connected to effort and values is more likely to be respected.

Families should also allow the next generation to create. Generational wealth should not trap heirs inside old identities. A child may not want to run the family business. A grandchild may create wealth through technology, art, science, investing, or public service. The system should preserve capital while allowing talent to evolve.

The best family wealth does not produce dependency. It produces capacity.

Building Generational Wealth Without Starting Rich

Many families assume generational wealth is impossible because they did not inherit any.

That belief is understandable but limiting. Starting without wealth makes the journey harder, not meaningless. The first generation may not create a dynasty. It may create stability. Stability may allow the next generation to avoid destructive debt. That generation may invest earlier. The next may inherit assets and financial education. Progress compounds socially as well as financially.

A family can begin with one emergency fund. One debt eliminated. One retirement account opened. One child taught to budget. One insurance policy purchased. One will written. One professional skill acquired. One small business started. One property bought carefully. One investment contribution automated. One family meeting held.

Small beginnings matter because they change direction.

The family that moves from debt to surplus has changed direction. The family that moves from renting out of instability to housing security has changed direction. The family that moves from no investments to monthly contributions has changed direction. The family that moves from secrecy to financial education has changed direction. The family that moves from undocumented wishes to legal clarity has changed direction.

Generational wealth is not created only when millions are transferred. It is created whenever the next generation receives more stability, knowledge, and opportunity than the last.

The early work may feel slow. But slow does not mean small. A family that changes its financial operating system changes the probabilities for everyone who follows.

The Legacy Is the System

Generational wealth is not a single account, property, policy, company, or inheritance. It is the system that connects them.

Income creates surplus. Surplus funds savings and investment. Investments create ownership. Ownership creates income and appreciation. Insurance protects against catastrophe. Legal planning transfers assets correctly. Tax planning preserves capital. Beneficiary reviews prevent misdirection. Education prepares heirs. Governance prevents conflict. Values give the money purpose.

When these pieces work together, wealth becomes more durable. When they are missing, even large fortunes can become fragile.

The family that wants to create generational wealth should begin with a clear question: Are we merely collecting assets, or are we building a system?

A collection of assets may look impressive but remain vulnerable. A system can survive change. It can adapt when markets fall, when a founder retires, when children grow, when laws change, when properties need repair, when businesses face competition, when families disagree, and when life becomes uncertain.

The work requires discipline. It requires honest conversations. It requires professional advice. It requires documentation. It requires patience. It requires teaching. It requires the humility to admit that wealth can be lost and the wisdom to build protections before they are needed.

But the reward is profound.

Generational wealth gives families more than comfort. It gives them resilience, education, mobility, choice, dignity, and the ability to contribute beyond survival. It allows one generation’s discipline to become another generation’s opportunity.

The goal is not simply to leave money behind. The goal is to leave behind people capable of using wealth well.

That is the real inheritance.