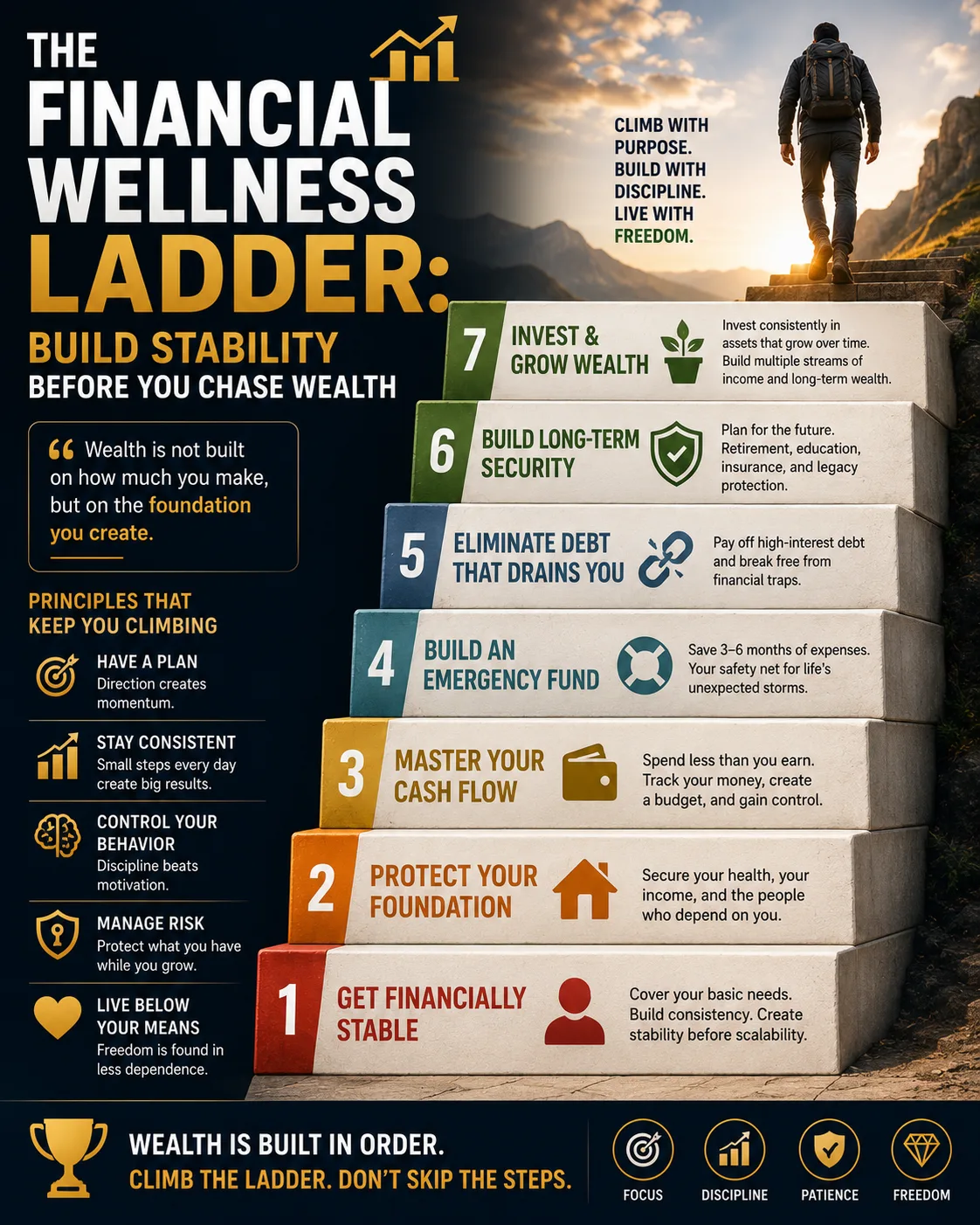

The Financial Wellness Ladder: Build Stability Before You Chase Wealth

Financial wellness is often mistaken for wealth. The two are connected, but they are not the same. A person can earn a high income and still feel financially anxious. A household can own assets and still be one emergency away from distress. An investor can hold shares, bonds, land, or retirement savings and still lack the basic structure needed to protect those assets from life’s disruptions.

Financial wellness is the condition of having control over your money, resilience against shocks, a clear plan for the future, and enough flexibility to live meaningfully along the way. It is not built by one investment, one salary increase, one side hustle, or one lucky financial decision. It is built through sequence.

The order matters. Many people try to invest before they can budget. They chase returns before they have emergency savings. They buy assets while carrying expensive debt. They pursue financial freedom while ignoring insurance. They think about retirement only after lifestyle has absorbed every raise. This is like building the upper floors of a house before the foundation has set.

A strong financial life is built in layers. First, you learn to manage money. Then you create a surplus. Then you protect yourself from emergencies. Then you insure against risks that could wipe out years of progress. Then you reduce destructive debt. Then you build larger reserves and plan for predictable expenses. Then you invest. Then you diversify. Then you invest consistently. Then you allow money to support a meaningful life. Then you prepare for retirement, tax efficiency, and the transfer of wealth.

This is the financial wellness ladder. It does not promise instant riches. It offers something better: a durable path from financial stress to financial strength.

Step One: Master Money Management Before You Try to Build Wealth

The first step in financial wellness is not investing. It is knowing where your money goes.

This sounds basic, but it is where many financial plans fail. People often underestimate spending, overestimate discipline, and assume that income alone will solve problems. Yet money that is not tracked tends to disappear. A salary can feel sufficient on payday and inadequate two weeks later. Business income can look impressive until expenses, taxes, school fees, rent, transport, and family obligations are counted honestly.

Money management begins with visibility. You need to know your income, fixed expenses, variable expenses, debt obligations, irregular costs, and savings rate. Without this information, every decision is guesswork. You cannot know whether you can invest more, save more, repay debt faster, or afford a major purchase if you do not understand your monthly cash flow.

A budget is not a punishment. It is a map. It tells you what your money is already doing and gives you the power to redirect it. The goal is not to remove all enjoyment from life. The goal is to ensure that your spending reflects your priorities rather than your impulses.

A good budget separates needs, obligations, future goals, and discretionary spending. Needs include food, housing, transport, utilities, medical expenses, and essential family responsibilities. Obligations include debt repayments, insurance premiums, taxes, rent, school fees, and contractual commitments. Future goals include savings, investments, emergency reserves, retirement contributions, and sinking funds. Discretionary spending includes entertainment, eating out, upgrades, subscriptions, travel, celebrations, and lifestyle choices.

Many people resist budgeting because they fear what it will reveal. But avoiding the truth does not improve the numbers. If money is leaking through small daily choices, the leak continues whether it is measured or not. If debt repayments are consuming too much income, ignoring them only delays the reckoning. If lifestyle spending has quietly expanded, a budget makes the pattern visible.

The first practical act of financial wellness is to track spending for at least one full month. Not from memory. Not roughly. Track actual spending. Mobile money, bank statements, cash withdrawals, card payments, subscriptions, informal lending, family support, and impulse purchases should all be included. The exercise may be uncomfortable, but it is often transformative.

Once the numbers are visible, the next question is simple: what must change? Some expenses may be reduced. Some may be eliminated. Some may be renegotiated. Some may be accepted because they support health, family, or long-term goals. The point is not to spend as little as possible. The point is to spend intentionally.

Financial wellness begins when money stops moving unconsciously.

Step Two: Create a Consistent Savings Habit

After money becomes visible, the next step is saving. Saving is the act of keeping part of today’s income for tomorrow’s needs. It is the bridge between earning and wealth creation.

A person who cannot save consistently will struggle to invest consistently. Investing requires surplus money. It also requires delayed gratification, emotional control, and the ability to let money serve the future instead of immediate consumption. Saving builds those muscles.

A useful target is to save at least 20% of income where possible. This number will not fit every household at every stage. Someone with a low income, dependents, high rent, medical obligations, or temporary hardship may need to start lower. Someone with strong income and modest expenses may be able to save far more. The exact percentage is less important than the direction: the savings rate should be intentional, measurable, and improving over time.

The phrase “save as much as possible whenever you can” sounds flexible, but it is often too vague. Most people need a defined system. A better approach is to decide on a savings percentage or amount before spending begins. When income arrives, savings should move first. This is the principle behind paying yourself first.

Automation helps. If savings depend on monthly motivation, they are vulnerable to mood, fatigue, pressure, and temptation. Automatic transfers to a savings account, Money Market Fund, SACCO account, retirement plan, or investment account turn saving into a default behavior. The less negotiation required, the more likely the habit will survive.

Income growth should also increase savings. One of the most common financial traps is lifestyle inflation. A person earns more, then immediately upgrades housing, transport, entertainment, clothes, gadgets, restaurants, and social spending. Their income rises, but their savings rate remains weak. They look more successful but remain financially fragile.

A stronger rule is to save a portion of every income increase before upgrading lifestyle. If income rises by 30%, the household might assign half of that increase to savings, debt reduction, or investments. Lifestyle can improve, but the future improves too.

Saving is not only about sacrifice. It is about options. Savings allow you to handle emergencies, leave toxic work, negotiate better, invest when opportunities appear, avoid bad debt, and sleep better during uncertainty. The person with savings has choices that the person living from payday to payday does not.

Step Three: Build the First One-Month Emergency Fund

The full emergency fund may eventually need to cover six months or more of expenses, but the first milestone should be smaller: one month of essential living costs.

This starter emergency fund matters because large financial goals can feel discouraging. If a household spends 100,000 per month, a six-month reserve requires 600,000. For many people, that number feels distant. A one-month target is more achievable and creates immediate protection.

The one-month emergency fund is not complete financial security, but it is the first wall between inconvenience and crisis. It can handle a delayed salary, a minor medical expense, a small repair, a temporary cash-flow gap, or an urgent family need without immediately turning to debt.

This fund should be separate from daily spending money. If it sits in the same account used for groceries, transport, entertainment, and bills, it will likely be spent. Separation creates respect. The account should be accessible but not too convenient. The goal is to make emergency money available for real emergencies and slightly inconvenient for casual use.

Many people ask whether they should save a starter emergency fund while carrying debt. In most cases, yes. Clearing debt is important, but using every spare shilling for debt repayment while holding no emergency cash can backfire. A small emergency then forces the person to borrow again, often at high interest. The debt cycle continues.

A starter emergency fund interrupts that cycle. It gives the household breathing room while debt reduction continues. Once one month of expenses is saved, the household can pursue debt repayment more aggressively while still maintaining a basic buffer.

Step Four: Protect Against Medical Risk

Health insurance is not a luxury in a financial wellness plan. It is a protection against one of the most common ways wealth is destroyed: illness.

Medical emergencies can consume savings quickly. A family may spend years building reserves only to lose them to one hospitalization, surgery, chronic illness, accident, or specialist treatment. In countries where out-of-pocket medical costs can be significant, health insurance is a core part of financial planning.

The purpose of health insurance is not to make illness painless. It is to prevent illness from becoming a financial catastrophe. A good cover can protect emergency funds, preserve investments, reduce borrowing, and protect dependents from sudden financial strain.

The right health insurance depends on income, age, dependents, medical history, employer benefits, public schemes, private options, hospital networks, exclusions, waiting periods, outpatient needs, maternity needs, chronic illness coverage, and claim procedures. The cheapest cover is not always the best. A policy that excludes likely risks or has weak hospital access may fail when needed.

Every household should understand what is covered, what is excluded, what limits apply, which hospitals are included, how preauthorization works, what documents are required, and whether dependents are covered. Insurance should not be purchased and forgotten. It should be reviewed annually because family needs change.

Health insurance is only one part of the protection layer. A broader wellness plan may also require life insurance, disability cover, property insurance, motor insurance, and business insurance depending on circumstances.

Life insurance is important when other people depend on your income. If a parent, spouse, or breadwinner dies, the emotional loss is already severe. The financial loss should not force dependents into crisis. Life cover can provide money for living expenses, education, debt repayment, or estate settlement.

Disability insurance is often overlooked, yet the risk is serious. Death ends income permanently, but disability can end or reduce income while expenses continue and medical costs rise. A household that depends heavily on one person’s ability to work should consider how it would survive if that ability were interrupted.

Property and motor insurance protect valuable assets from damage, theft, accidents, and liability. For business owners, insurance may also protect inventory, equipment, premises, employees, and professional risks. The right insurance plan depends on what could financially damage the household if left uncovered.

Insurance is not an investment. It is a shield. Its value is seen most clearly when something goes wrong.

Step Five: Eliminate Debt Strategically

Debt is not always bad. Some debt finances productive assets, education, business expansion, or housing under reasonable terms. But high-interest consumer debt is one of the greatest obstacles to financial wellness.

Expensive debt drains future income. Credit card balances, mobile loans, salary advances, payday-style borrowing, informal high-interest loans, and unnecessary personal loans can create a cycle where today’s spending becomes tomorrow’s pressure. The borrower works, earns, and immediately sends a large portion of income to lenders.

Debt repayment should be strategic. The goal is not only to reduce balances but to reduce financial leakage. High-interest debt usually deserves priority because it compounds against the borrower. Paying off a loan charging a high rate can produce a guaranteed improvement in financial position. It is difficult for most investments to reliably outperform expensive debt after risk and tax.

There are two common debt repayment methods. The avalanche method prioritizes the highest-interest debt first while maintaining minimum payments on the rest. This is mathematically efficient because it reduces total interest paid. The snowball method prioritizes the smallest debt first, regardless of interest rate, to create psychological momentum. This can help people who need early wins to stay motivated.

The best method is the one that the borrower will actually follow, though high-interest debt should never be ignored for too long. A practical plan may combine both approaches: clear a few small balances to create momentum, then attack the highest-cost debts aggressively.

Debt repayment should happen alongside basic emergency savings. Using every available shilling to repay debt while leaving no cash buffer can lead to repeated borrowing. A stronger sequence is to build a one-month emergency fund, pay down destructive debt aggressively, then expand the emergency fund once debt pressure eases.

Borrowers should also address the behavior that created the debt. If debt arose from a medical emergency, the solution may be insurance and emergency savings. If it arose from lifestyle spending, the solution is budgeting and discipline. If it arose from income instability, the solution may include cash reserves, income diversification, and more conservative spending. Debt repayment without behavior change often becomes temporary.

Debt freedom is not only about having no loans. It is about no longer depending on debt to manage ordinary life.

Step Six: Expand the Emergency Fund and Build Sinking Funds

After the starter emergency fund and debt strategy are in place, the next step is to build a deeper safety net.

A full emergency fund typically targets three to six months of essential living expenses. For households with irregular income, dependents, single-income reliance, business volatility, or weak job security, nine to twelve months may be more appropriate. The fund should reflect real risk, not just a textbook number.

This money is for unexpected events: job loss, medical gaps not covered by insurance, urgent repairs, temporary income disruption, or family emergencies. It should not be used for holidays, school fees, planned purchases, weddings, insurance premiums, or car servicing. Those belong in sinking funds.

A sinking fund is money saved for a known future expense. It turns large irregular costs into manageable monthly contributions. If school fees are due in four months, the amount should be divided across those months. If annual insurance is due in twelve months, divide the premium by twelve. If a holiday is planned for December, start saving early. If a car will need maintenance, build a fund before the mechanic calls.

Sinking funds prevent predictable costs from becoming fake emergencies. They also protect investments. Without sinking funds, people often sell investments or borrow for expenses they knew were coming. This interrupts compounding and creates stress.

Emergency funds and sinking funds should be separate. Combining them creates confusion. A household may think it has a healthy emergency reserve, but part of that money may already be needed for school fees, insurance, or rent deposits. When the planned expense is paid, the emergency fund shrinks. Then a true emergency arrives, and the household is exposed.

Separate accounts or clear tracking categories create discipline. The money should be named according to its purpose. “Emergency Fund.” “School Fees.” “Insurance.” “Car Maintenance.” “Medical Reserve.” “Holiday.” “House Deposit.” Named money is harder to misuse.

Many people find Money Market Funds useful for emergency and sinking funds because they may offer better returns than ordinary savings accounts while maintaining relatively high liquidity. They are often suitable for money that should earn modest returns but remain accessible. Still, they should be understood properly. Money Market Funds are investment products. Returns vary, fees matter, access rules differ, and lower risk does not mean no risk.

For immediate needs, a household may keep a small amount in a bank or mobile account and the larger emergency reserve in a liquid cash-management vehicle. Liquidity should match urgency.

Step Seven: Begin Investing After the Foundation Is Stable

Investing should begin once the household has enough stability to avoid turning every market fluctuation into a personal crisis. This does not require perfect finances. Waiting for perfection can delay investing for years. But it does require a basic foundation: controlled spending, a savings habit, basic emergency cash, insurance protection, and a debt strategy.

Investing is different from saving. Saving prioritizes safety and liquidity. Investing accepts risk in pursuit of growth, income, or inflation protection. The money invested should not be needed for immediate emergencies or predictable short-term expenses.

Beginners should start with clarity. What is the goal? Retirement? Education? Wealth accumulation? Financial independence? Home purchase? Passive income? The goal determines the time horizon, and the time horizon determines suitable risk.

Money needed in one year should not be invested like money needed in twenty years. Short-term goals require stability. Long-term goals can usually tolerate more volatility because time allows markets and assets to recover from temporary declines.

Common investment options may include Money Market Funds, Treasury bills, Treasury bonds, SACCO shares and deposits, unit trusts, exchange-traded funds, retirement schemes, equities, real estate, and business interests. Each has different risks. They should not be treated as interchangeable.

Money Market Funds may be useful for liquidity and capital preservation but are not long-term growth engines. Treasury bonds can provide income and relative security, but they carry interest-rate risk, inflation risk, and reinvestment risk. SACCOs can offer useful savings and credit benefits, but their strength depends on governance, regulation, liquidity, and asset quality. ETFs and equity funds can provide diversified growth exposure, but market values fluctuate. Real estate can create income and appreciation, but it is illiquid and costly to transact. Businesses can build wealth, but they carry operational risk.

The investor’s task is not to choose the most exciting option. It is to match each asset to a purpose.

Step Eight: Diversify Through Asset Allocation

Once investing begins, diversification becomes essential. Asset allocation is the process of dividing investments across different asset classes to balance risk and return. It is one of the most important decisions an investor makes.

A person who places all wealth in one asset is exposed to one story. If that story fails, the financial plan suffers. Concentrating everything in property, one SACCO, one employer’s shares, one business, one currency, or one fund can create hidden fragility.

Diversification spreads risk. It may include cash for liquidity, fixed income for stability and income, equities for growth, real estate for long-term value and income, retirement accounts for future security, and business interests for entrepreneurial upside. The exact mix depends on age, income stability, goals, risk tolerance, tax position, and time horizon.

Younger investors with long horizons may hold more growth assets because they have time to recover from volatility. Older investors or those nearing retirement may need more income, stability, and liquidity. A business owner whose income is already volatile may need a more conservative investment portfolio than a salaried employee with predictable income. A household with dependents may need stronger cash reserves and insurance before increasing risk.

Diversification should be real, not cosmetic. Owning several funds that all invest in the same assets may not diversify much. Owning multiple properties in the same neighborhood may still depend on one local market. Owning shares in several banks may still expose the investor to one sector. True diversification asks whether the assets respond differently to economic conditions.

Asset allocation should also consider inflation. Cash protects liquidity but may lose purchasing power over time. Fixed income provides income but can be hurt by rising inflation and interest rates. Equities and real assets may offer long-term inflation protection, but they fluctuate. A balanced portfolio recognizes that every asset has strengths and weaknesses.

The purpose of diversification is not to avoid all losses. That is impossible. The purpose is to avoid one mistake, one market, one institution, or one cycle destroying the entire plan.

Step Nine: Invest Consistently and Keep Buying

After the right investment structure is created, consistency becomes the main discipline.

Many investors spend too much energy trying to time the market. They want to buy at the bottom and avoid every decline. This is emotionally appealing but difficult in practice. Markets are uncertain. Good news and bad news are priced quickly. Waiting for perfect conditions often means remaining in cash while long-term opportunities pass.

Consistent investing shifts the focus from prediction to participation. The investor contributes regularly, whether monthly, quarterly, or according to income cycles. This approach builds ownership over time and reduces the pressure to find the perfect entry point.

Regular investing also creates discipline during downturns. When markets fall, fear encourages people to stop. Yet if the investor is buying diversified long-term assets, lower prices can improve future returns. Continuing to invest through weak markets is emotionally difficult but financially powerful.

This does not mean buying anything blindly. The investment plan must still be suitable, diversified, and aligned with goals. Consistency should support a good plan, not excuse a bad one.

Investors should increase contributions as income rises. Raises, bonuses, commissions, business profits, and side income should not disappear entirely into lifestyle. A portion should be directed toward investments before spending expands. This is how income growth becomes wealth growth.

Compounding rewards consistency. At first, investment returns may feel small because the portfolio is small. Over time, contributions accumulate, returns generate returns, and the portfolio begins to carry more of the load. The early years require patience. The later years reveal the power of repetition.

Step Ten: Leave Room for Life Experiences

Financial wellness is not the same as extreme deprivation. A plan that ignores joy, rest, family, travel, celebration, generosity, and meaningful experiences may look efficient on paper but fail in real life.

Money is a tool. It should protect the future, but it should also support a life worth living today. The key is intentionality. Experiences should be planned, funded, and aligned with values rather than financed through guilt, pressure, or debt.

This is where sinking funds become useful again. A holiday fund allows travel without damaging emergency savings. A celebration fund allows weddings, birthdays, or family events without borrowing. A generosity fund allows support for relatives or community needs without disrupting the entire budget. When experiences are funded intentionally, they become part of the plan rather than threats to the plan.

Some people delay all enjoyment until retirement. This can be a mistake. Health, relationships, children’s ages, friendships, and opportunities change. The goal is not to spend recklessly, but to recognize that life is not lived only in the future.

A financially well person can say yes to meaningful experiences because the essentials are protected. They can also say no to performative spending because their values are clear. This balance matters. Wealth without enjoyment can become fear. Enjoyment without discipline can become regret.

Step Eleven: Plan for Retirement Before It Becomes Urgent

Retirement planning should begin long before retirement feels close. The earlier it starts, the more time compounding has to work and the less pressure future income must carry.

Retirement is not only an age. It is the point at which work income reduces or stops and accumulated assets must support living expenses. That requires capital. The required capital depends on expected expenses, inflation, health needs, dependents, lifestyle, housing, life expectancy, and desired legacy.

Many people underestimate retirement because they focus only on current expenses. But retirement can last decades. Medical costs may rise. Inflation can reduce purchasing power. Family obligations may continue. Housing may need maintenance. A person who retires without adequate planning may become dependent on children, relatives, government support, or forced asset sales.

Retirement planning should include pension contributions, employer retirement schemes, individual retirement plans, long-term investment portfolios, income-generating assets, and debt reduction before retirement. Entering retirement with high-interest debt or no liquidity can create serious stress.

Tax treatment matters. Retirement contributions may offer tax advantages depending on the jurisdiction and structure. Tax-efficient investing can improve long-term outcomes because the amount kept after tax is what funds the future. Investors should understand contribution limits, withdrawal rules, tax reliefs, and the tax treatment of pension income, dividends, interest, capital gains, and rental income.

Retirement planning should also consider inflation. A retirement income that looks adequate today may be insufficient twenty years from now. Investments should be chosen not only for safety but for the ability to preserve purchasing power over time.

A useful retirement question is: how much monthly income will I need when I no longer rely on employment or active business income? From there, the investor can estimate the assets required to produce that income. The answer may be imperfect, but it creates direction.

The Missing Layer: Tax Planning

A complete financial wellness plan should include tax awareness. Tax is one of the largest financial costs many people face, yet it is often ignored until filing deadlines or penalties appear.

Tax planning does not mean tax evasion. It means arranging finances legally and intelligently so that obligations are met while available reliefs and efficient structures are used. This may include retirement contribution relief, proper business expense documentation, understanding withholding tax, planning for capital gains tax where applicable, reviewing rental income obligations, and keeping records.

For employees, tax planning may involve understanding payslips, benefits, pension contributions, insurance reliefs, and allowable deductions. For business owners and freelancers, it may involve separating personal and business finances, keeping receipts, planning for tax payments, and avoiding the mistake of treating gross revenue as personal income.

Investors should understand whether returns are taxed as interest, dividends, capital gains, rental income, or business income. Two investments with the same headline return may produce different after-tax results. The after-tax return is what matters.

Tax planning becomes more important as wealth grows. Property ownership, business profits, investment income, retirement withdrawals, and estate transfers all have tax implications. Ignoring tax can reduce wealth quietly and sometimes create legal problems.

Financial wellness requires not only earning and investing, but keeping records, understanding obligations, and planning ahead.

The Missing Layer: Estate Planning

Estate planning is often postponed because it feels uncomfortable. People do not like thinking about death, incapacity, succession, or family conflict. Yet avoiding the topic can leave dependents exposed and assets vulnerable.

An estate plan answers several questions. Who should receive your assets if you die? Who should manage affairs if you are incapacitated? Who are the beneficiaries of insurance policies, retirement accounts, SACCO deposits, bank accounts, and investments? Who will care for minor children? How will business interests be transferred or managed? How can disputes be minimized?

A will is one of the basic tools of estate planning. Beneficiary nominations are also important because certain assets may pass according to named beneficiaries rather than the will. These nominations should be reviewed after marriage, divorce, childbirth, death of a beneficiary, or major family changes.

Business owners need succession planning. If the owner dies or becomes incapacitated, who can access accounts, manage operations, pay staff, collect receivables, and make decisions? A profitable business can collapse if key knowledge and authority are locked inside one person’s head.

Estate planning is not only for the rich. Anyone with children, dependents, savings, land, insurance, retirement accounts, or business interests needs some form of plan. The more complex the family and asset base, the more important it becomes.

Financial wellness includes protecting the people and assets that outlive you.

Common Mistake: Delaying Investing Too Long

Because financial wellness emphasizes foundations, some people may delay investing excessively. They wait until the emergency fund is perfect, debt is completely gone, insurance is comprehensive, income is high, and every uncertainty is resolved. This can postpone wealth creation for years.

The better approach is staged progress. Build a starter emergency fund. Begin debt reduction. Get essential insurance. Start modest investing when the foundation is stable enough. Continue growing reserves and investments together. The sequence matters, but it does not require perfection before any investment begins.

For example, a person may contribute a small amount to retirement while still building emergency savings. A household may invest modestly while aggressively repaying high-interest debt, provided it has a basic buffer. The exact balance depends on interest rates, employer matching, tax benefits, job security, and risk tolerance.

The danger is extremes. Investing aggressively with no foundation is fragile. Waiting forever to invest is costly. Financial wellness lies between recklessness and paralysis.

Financial Wellness for Irregular Income

Many financial frameworks assume stable monthly income. But freelancers, entrepreneurs, commission earners, farmers, casual workers, consultants, and informal-sector workers often face irregular cash flow. Their financial wellness plan must be more conservative.

Irregular income requires a larger cash buffer. Instead of budgeting from average income alone, the household should identify the minimum monthly survival cost and build reserves for low-income months. A business owner may need both a personal emergency fund and a business emergency fund.

One useful method is to pay yourself a fixed monthly amount from business or irregular income, while surplus months refill reserves. This smooths consumption and prevents high-income months from creating false confidence.

Sinking funds are especially important for irregular earners because predictable expenses do not wait for good months. School fees, rent, insurance, and taxes arrive whether income was strong or weak. Planning must account for seasonality.

Irregular earners should also be cautious with debt. Fixed repayments can become stressful when income fluctuates. Before borrowing, they should stress-test repayments against weak months, not average months.

For such households, financial wellness is less about maximizing return and more about surviving volatility while still building long-term assets.

The Annual Financial Review

A financial wellness plan should be reviewed at least once a year. Life changes, and the plan must adapt.

The review should begin with income. Did income rise, fall, or become more volatile? Did new income streams appear? Did any disappear? Then expenses should be reviewed. Which costs increased? Which can be reduced? Are there subscriptions, habits, or obligations that no longer serve the household?

Next, review the emergency fund. Does it still cover the intended number of months? Have expenses risen? Has income become more or less stable? Are dependents increasing?

Review insurance. Is health cover adequate? Are dependents included? Is life cover needed or sufficient? Does disability risk require attention? Are property, motor, or business risks properly covered?

Review debt. Which debts remain? What interest rates apply? Can any be refinanced, accelerated, or eliminated? Is new debt being used productively or destructively?

Review investments. Does the asset allocation still match goals and risk tolerance? Are fees reasonable? Are contributions consistent? Is the portfolio diversified? Has any investment become too large a share of net worth?

Review taxes. Are records complete? Are retirement reliefs or other legal benefits being used? Are there upcoming tax obligations from business, property, investments, or capital gains?

Review estate planning. Are beneficiaries updated? Is there a will? Have family circumstances changed? Are dependents protected?

This annual review turns financial wellness into a living system rather than a one-time exercise.

The Financial Wellness Ladder in Practice

A person beginning from financial stress should not try to do everything at once. The ladder is climbed step by step.

First, track spending and build a realistic budget. Second, save a defined amount or percentage from every income payment. Third, build a one-month emergency fund. Fourth, secure essential health insurance and review other protection needs. Fifth, attack high-interest debt while avoiding new destructive borrowing. Sixth, expand the emergency fund and create sinking funds for predictable expenses. Seventh, begin investing with long-term money. Eighth, diversify through thoughtful asset allocation. Ninth, invest consistently and increase contributions as income rises. Tenth, fund meaningful life experiences intentionally. Eleventh, plan for retirement, tax efficiency, and estate transfer.

This order is powerful because each step supports the next. Budgeting creates surplus. Saving turns surplus into reserves. Reserves reduce crisis borrowing. Insurance protects savings. Debt reduction frees cash flow. Sinking funds stabilize the budget. Investing converts surplus into assets. Diversification manages risk. Consistency builds compounding. Life experiences make the journey sustainable. Retirement and estate planning protect the future.

Financial wellness is not one action. It is a sequence of protections and commitments that turn income into stability, and stability into wealth.

The Real Goal: Freedom With Resilience

The purpose of financial wellness is not to count money for its own sake. It is to create freedom with resilience.

Freedom means having choices. The choice to leave a bad job. The choice to handle emergencies without begging or borrowing. The choice to educate children without panic. The choice to invest patiently. The choice to support family without destroying your own finances. The choice to retire with dignity. The choice to enjoy life without guilt because the future is being funded.

Resilience means those choices do not disappear the moment life becomes difficult. A resilient household has cash reserves, insurance, manageable debt, diversified investments, and a plan. It can bend without breaking.

This is why the order matters so much. Wealth built on a weak foundation can collapse quickly. Wealth built on wellness is harder to shake.

Before chasing aggressive returns, build the system that allows you to keep them. Before comparing investment products, understand your cash flow. Before buying assets, protect against emergencies. Before dreaming of financial independence, create financial stability. Before retirement arrives, prepare for it.

The financial wellness ladder is not glamorous. It is better than glamorous. It is dependable. And dependability, repeated over years, is one of the most underrated paths to wealth.