The Income Equation: Why Value Matters, but Effort Alone Does Not Decide Your Pay

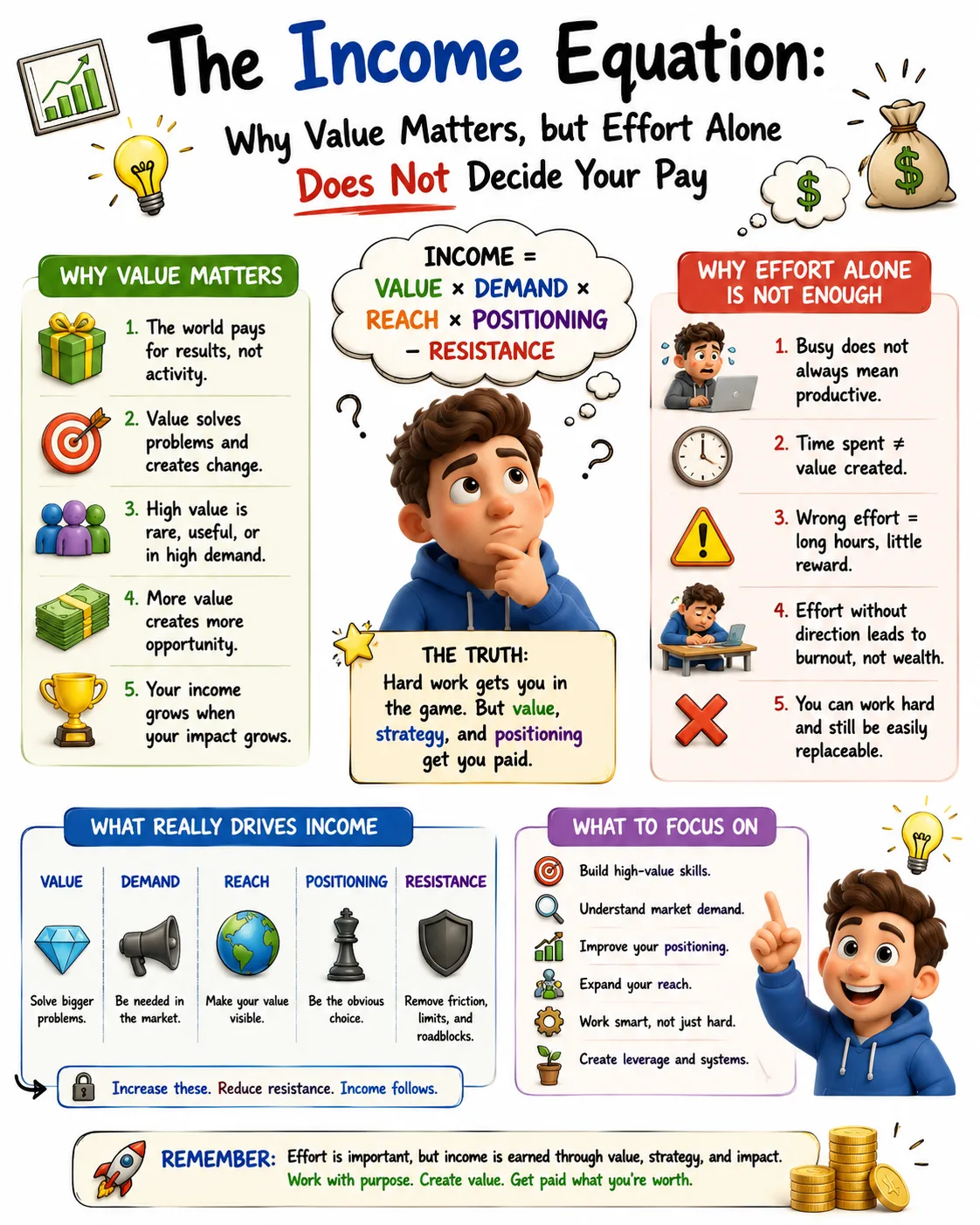

One of the most repeated ideas in personal development is that income reflects the value a person provides.

There is truth in that sentence. People are often paid more when they solve valuable problems, develop scarce skills, perform consistently, communicate well, negotiate effectively, and work in markets where their abilities are in demand. A surgeon, software engineer, electrician, sales leader, cybersecurity specialist, business owner, data scientist, attorney, skilled technician, or high-performing consultant may earn more because the problems they solve are difficult, urgent, profitable, or risky for customers and employers.

But the sentence is incomplete.

Income does not reflect value in a pure moral or mathematical sense. It reflects market value under specific conditions. Those conditions include education, credentials, geography, bargaining power, industry structure, labor market demand, social networks, discrimination, family support, economic cycles, immigration rules, health, caregiving responsibilities, access to capital, and luck. A nurse may create enormous human value and still earn less than a financial professional whose work is more highly rewarded by the market. A teacher may shape hundreds of lives and earn less than someone optimizing advertising funnels. A caregiver may provide indispensable value and receive little or no pay. A person may work hard in a low-wage labor market and remain financially stretched.

So the better claim is this: income often grows when a person consistently solves problems that a market has the willingness and ability to pay for.

That distinction matters because it preserves the useful lesson without turning income into a judgment of human worth. Personal development matters. Skills matter. Discipline matters. Pricing matters. Confidence matters. But income is not a complete measure of character, intelligence, effort, or social contribution.

Labor economists often describe skills, education, health, and experience as forms of human capital. The World Bank’s human capital work emphasizes that homes, neighborhoods, workplaces, and societies all help shape how skills develop and how people participate in economic life. ([worldbank.org](https://www.worldbank.org/en/publication/human-capital-report?utm_source=chatgpt.com)) The OECD has also warned that digital and environmental transformations are moving faster than many education and skills systems, which means workers and countries must keep adapting as technology changes the value of different capabilities. ([oecd.org](https://www.oecd.org/content/dam/oecd/en/publications/reports/2023/11/oecd-skills-outlook-2023_df859811/27452f29-en.pdf?utm_source=chatgpt.com))

That is the income equation in modern life: human capital multiplied by market demand, filtered through opportunity, bargaining power, execution, and context.

This article examines 10 popular claims about income, value, discipline, and success. Some are broadly supported. Some are useful but oversimplified. Some are motivating in the right context but damaging when presented as universal truth. The goal is not to weaken ambition. It is to make ambition more accurate.

1. Low Skills Can Limit Income

Skills are one of the clearest drivers of earning power. People who can solve complex, high-demand problems tend to have more income opportunities than people whose skills are common, easily replaced, or weakly connected to market demand.

But the phrase “low skills limit income” needs careful handling. It should not be used as an insult. A person may have valuable abilities that are not well paid in their local economy. They may have skills that are socially essential but not financially rewarded. They may lack access to education, training, childcare, transportation, healthcare, or professional networks. They may be skilled in one country or industry but unable to transfer credentials elsewhere. They may be early in a career and still building experience.

The income-relevant question is not simply, “Do I have skills?” It is, “Do I have skills that a market currently rewards, and can I prove, package, and apply them?”

That distinction is crucial. A skill has economic power when it intersects with demand. A person can become highly competent at something that few employers or customers are willing to pay for. Another person can become moderately competent in a high-demand area and earn more because the market urgently needs that capability. This is why income growth often requires studying both ability and demand.

Current labor market trends show how quickly demand can shift. The U.S. Bureau of Labor Statistics projects strong demand in computer and information technology occupations, with about 317,700 openings each year on average over the 2024 to 2034 period due to growth and replacement needs. ([bls.gov](https://www.bls.gov/ooh/computer-and-information-technology/?utm_source=chatgpt.com)) The BLS also lists fast-growing occupations across clean energy, healthcare, technology, and related fields, with wind turbine service technicians and solar photovoltaic installers among the fastest-growing occupations in its 2024 to 2034 projections. ([bls.gov](https://www.bls.gov/ooh/fastest-growing.htm?utm_source=chatgpt.com)) These examples do not mean every person should enter technology or clean energy. They show that market demand changes, and income strategy should respond to those changes.

Skill development should be treated as investment. Like any investment, it has a cost, a time horizon, and a potential return. A degree, certification, apprenticeship, portfolio, sales skill, technical skill, language, professional license, or management capability can increase income if it connects to real demand. But not every course pays off. Not every credential improves bargaining power. Not every training program leads to better work.

The practical approach is to investigate before investing. Look at job postings. Speak with people doing the work. Compare wages. Understand credential requirements. Study promotion paths. Ask what employers actually value. Build evidence through projects, results, references, or measurable outcomes.

Skills increase income most reliably when they are specific enough to be valuable, transferable enough to survive change, and visible enough for the market to recognize.

2. Complaining Changes Nothing, Unless It Becomes Action

“Complaining changes nothing” is motivational language with a partial truth inside it.

Complaining alone rarely improves income. A person can complain about low pay, unfair managers, poor opportunities, weak customers, difficult markets, and rising costs without taking any action that changes their situation. Repeated complaint can become a substitute for strategy. It may provide emotional release while leaving the underlying problem untouched.

But not all complaint is useless. Constructive complaint can become feedback, negotiation, advocacy, whistleblowing, union activity, policy reform, workplace improvement, or customer insight. Many social and workplace gains began with people naming a problem that others preferred to ignore. Workers who raise safety concerns, challenge discrimination, organize for better conditions, or negotiate compensation are not merely “complaining.” They are converting dissatisfaction into action.

The difference is agency.

Unproductive complaint says, “This is unfair,” and stops there. Productive complaint asks, “What can be changed, who has the power to change it, what evidence supports the case, and what action should follow?”

For income growth, this distinction matters. A person who feels underpaid can complain indefinitely. Or they can gather market data, document achievements, improve skills, apply elsewhere, negotiate, freelance, change industries, build a portfolio, or seek mentorship. The complaint may be valid, but validity alone does not create leverage.

At the same time, the advice should not imply that every person can simply act their way out of poor conditions. Some workers face limited local opportunities, caregiving obligations, visa restrictions, discrimination, health constraints, or economic downturns. The appropriate action may be gradual, collective, or strategic rather than immediate and individual.

The income lesson is not “never complain.” It is “do not let complaint become the end of analysis.”

Complaint identifies pain. Strategy turns pain into movement.

3. Many People Undercharge Themselves, but Not Everyone Sets Their Own Price

The idea that most people undercharge themselves is especially relevant for freelancers, consultants, creators, coaches, tradespeople, agencies, and entrepreneurs. When individuals set their own prices, psychology can become a major income constraint.

People undercharge for many reasons. They fear rejection. They confuse affordability with value. They compare themselves with low-cost competitors. They lack confidence. They do not understand the client’s economics. They price based on hours instead of outcomes. They fail to account for taxes, unpaid time, marketing, software, insurance, revision work, and business risk. They raise prices too slowly because they are afraid existing customers will leave.

Undercharging can create a trap. Low prices attract price-sensitive customers. Price-sensitive customers may demand more while paying less. The business owner becomes busy but not profitable. Because they are busy, they have less time to improve skills, market to better clients, build systems, or reposition their offer. Low pricing then becomes a ceiling on growth.

For independent workers, pricing should be connected to value, positioning, cost structure, demand, proof, and alternatives. A consultant who helps a company save $500,000 should not price only by the number of hours spent preparing the report. A designer whose work increases conversion rates should understand the economic value of better performance. A tradesperson who is reliable, insured, skilled, and punctual may be worth more than a cheaper competitor who creates risk.

But this claim is less applicable to salaried employees. A salaried employee does not usually “charge” directly. Their income is shaped by job market conditions, employer budgets, pay bands, credentials, negotiation, performance evaluation, industry norms, and bargaining power. They can still underprice themselves by accepting low offers, failing to negotiate, staying too long in low-growth roles, or not communicating impact. But the mechanism is different.

For employees, the equivalent of pricing is positioning. What roles are you applying for? What problems are you associated with solving? Can you document outcomes? Are you in an industry that pays for your strengths? Do decision-makers know your contribution? Are you negotiating from evidence or hope? Have you built alternatives?

Income often rises when people stop thinking only as labor sellers and begin thinking as value translators. The market does not automatically reward quiet contribution. Value must often be made visible, measured, communicated, and negotiated.

4. Fear Can Kill Opportunities, but Caution Can Save You

Fear is one of the most powerful forces in financial life. It prevents people from applying for better jobs, negotiating salaries, raising prices, starting businesses, investing, learning new skills, changing industries, asking for mentorship, or leaving unhealthy work environments.

Some fear is protective. A person should be cautious before taking on debt, quitting stable income, making a speculative investment, signing a lease, hiring employees, or entering an unfamiliar market. Risk is real. Optimism does not repay loans. Confidence does not guarantee customers. Ambition does not eliminate uncertainty.

The problem is not fear itself. The problem is unmanaged fear.

Unmanaged fear treats discomfort as danger. It says, “Do not apply because rejection will hurt.” “Do not negotiate because the employer might say no.” “Do not invest because markets can fall.” “Do not start because you might fail.” “Do not learn because you might be behind.” In this way, fear protects the present at the expense of the future.

Prudent caution asks better questions. What is the downside? Can I afford it? What evidence do I need? Can I test this on a small scale? Can I build a cash reserve first? Can I reduce fixed expenses? Can I learn before committing? Can I create a backup plan? Can I take the risk in stages?

This is the difference between gambling and calculated risk. A person who quits a job with no savings, no customers, no plan, and high debt may be reckless. A person who builds a business on the side, validates demand, saves a runway, and then transitions is taking a risk with structure. A person who puts all savings into one speculative asset is gambling. A person who invests regularly in a diversified portfolio aligned with long-term goals is taking market risk in a controlled way.

Fear kills opportunities when it becomes permanent avoidance. Caution protects opportunities when it helps a person prepare.

The income lesson is to respect risk without worshiping safety. Staying in the same place can also be risky if skills decay, wages stagnate, inflation rises, or industries change. Sometimes the greater risk is never acting.

5. Comfort Does Not Always Destroy Ambition

“Comfort destroys ambition” is a popular phrase because it sounds tough. It suggests that growth requires discomfort and that ease makes people weak.

There is a truth here. Many forms of progress require leaving familiar routines. Learning a new skill can feel uncomfortable. Negotiating can feel uncomfortable. Starting a business can feel uncomfortable. Networking, public speaking, investing, applying for better roles, asking for feedback, and changing habits can all create discomfort.

But the claim becomes harmful when it implies that comfort is always the enemy.

Sustainable success requires some forms of comfort: sleep, health, emotional stability, supportive relationships, psychological safety, and enough financial margin to think clearly. A person living in constant stress may not become more ambitious. They may become exhausted. Scarcity can narrow attention and reduce the capacity for long-term planning. Burnout can damage performance, judgment, and health.

Comfort becomes dangerous when it turns into complacency. Stability becomes powerful when it creates a platform for growth.

A stable job can fund education, investing, debt repayment, and business experiments. A peaceful home can support focus. A cash reserve can make career risk more rational. A supportive relationship can help someone pursue difficult goals. These are not ambition killers. They are ambition infrastructure.

The healthier principle is this: growth requires deliberate challenge, not permanent distress.

People should leave comfort zones strategically. Take on projects that stretch skills. Seek feedback. Build public evidence of competence. Apply for roles slightly beyond current confidence. Raise prices where value supports it. Learn technologies that may affect the industry. But do not confuse chronic instability with progress.

The goal is not to be uncomfortable all the time. The goal is to avoid becoming so comfortable that learning stops.

6. High Earners and Wealth Builders Often Learn Continuously

Continuous learning is one of the strongest ideas in the income-growth conversation.

Skills lose value when industries change. Technology reshapes tasks. Customer expectations evolve. Regulations change. Tools improve. Business models shift. A person who stops learning may not notice that the market has moved until their income options narrow.

The OECD has emphasized that skills are vital for resilient economies and societies, especially as digital and environmental transformations accelerate. ([oecd.org](https://www.oecd.org/en/publications/2023/11/oecd-skills-outlook-2023_df859811.html?utm_source=chatgpt.com)) This is not only a national policy issue. It is a household income issue. Workers who adapt are often better positioned than workers who rely only on past credentials.

Continuous learning does not always mean formal degrees. It may mean certifications, apprenticeships, online courses, books, mentorship, deliberate practice, industry events, project work, technical documentation, professional communities, or learning by building. The form matters less than the outcome: can the person solve more valuable problems after the learning?

Learning should also be strategic. Consuming endless content is not the same as increasing earning power. Watching videos about business is not building a business. Reading about negotiation is not negotiating. Taking courses without applying the material can become productive procrastination.

The highest-return learning often connects directly to market opportunities. A data analyst learning machine learning may increase options. A nurse developing specialist credentials may access higher-paid roles. An electrician learning solar installation or industrial systems may move into growing demand. A manager learning financial analysis may become more valuable in strategic roles. A freelancer learning sales may earn more from existing technical ability.

Learning also includes financial literacy. A person who earns more but does not understand taxes, debt, cash flow, investing, or risk may fail to convert income into wealth. Financial literacy research has repeatedly connected knowledge with better financial behaviors and outcomes. A 2024 NBER overview reviewed evidence on financial literacy, financial education, and their relationship to financial decisions. ([nber.org](https://www.nber.org/papers/w32355?utm_source=chatgpt.com))

The income lesson is simple: the market pays for usefulness, and usefulness must be renewed.

7. High Income Requires Discipline

High income is not only earned through ambition. It is usually maintained through discipline.

At higher levels of responsibility, the demands increase. Professionals must deliver results consistently. Entrepreneurs must manage customers, cash flow, hiring, operations, competition, taxes, and strategy. Executives must make decisions under uncertainty. Specialists must keep their expertise current. Salespeople must maintain pipelines. Investors must manage risk and emotion. Creators must produce even when attention fluctuates.

Discipline matters because motivation is inconsistent. People may feel energized when starting a new role, launching a business, receiving praise, or seeing early results. But high income often requires performance after the excitement fades. It requires showing up when the work is repetitive, difficult, stressful, or invisible.

Discipline also separates high income from high net worth. A person can earn a lot and still remain financially fragile if they lack spending discipline. Lifestyle inflation can consume raises. Poor debt decisions can absorb bonuses. Speculation can erase savings. Lack of tax planning can reduce retained wealth. High income gives more room to build wealth, but it also gives more room to make expensive mistakes.

This is why discipline must operate in two places: earning and keeping.

Earning discipline includes skill development, reliability, execution, relationship management, and performance. Keeping discipline includes saving, investing, tax awareness, insurance, debt control, and lifestyle management. A person who excels at earning but fails at keeping may look successful while building little wealth.

Behavioral systems help. Automatic investing, separate savings accounts, scheduled reviews, written goals, spending rules, and debt limits can make discipline less dependent on mood. The goal is to design a financial life where good decisions happen by default.

High income can be a powerful tool. Discipline determines whether it becomes freedom or simply a more expensive lifestyle.

8. Laziness Has Financial Consequences, but the Word Can Hide Too Much

The claim that laziness has financial consequences is true in a narrow sense and dangerous in a broad one.

In a narrow sense, effort matters. A person who refuses to learn, avoids responsibility, misses deadlines, ignores feedback, performs poorly, wastes opportunities, or consistently does less than the role requires may damage their income prospects. Employers and customers usually reward reliability, competence, initiative, and problem-solving more than indifference.

But the word “laziness” is often used too casually. It can mislabel people who are exhausted, depressed, ill, underpaid, burned out, caregiving, disabled, discouraged, poorly managed, or trapped in labor markets with limited upside. It can also ignore unequal starting points. A person working two low-wage jobs may have less time for professional development than someone with family support and a flexible schedule. A parent caring for children or relatives may appear less career-focused while doing enormous unpaid labor.

Income analysis becomes shallow when every outcome is reduced to effort. Effort matters, but effort is not the only variable. Productivity depends on health, tools, training, management, incentives, autonomy, sleep, nutrition, safety, transportation, childcare, and emotional bandwidth.

A more useful question than “Am I lazy?” is “What is reducing my productive capacity?”

Sometimes the answer is avoidance. Sometimes it is fear. Sometimes it is poor habits. Sometimes it is a lack of skill. Sometimes it is a toxic workplace. Sometimes it is burnout. Sometimes it is untreated health issues. Sometimes it is unclear goals. Sometimes it is an economic environment where hard work is not enough to produce mobility.

The solution depends on the cause. Avoidance may require accountability. Burnout may require rest and boundaries. Low skill may require training. Poor health may require care. Low opportunity may require relocation, networking, credentialing, or collective advocacy. A bad job may require an exit plan.

The wealth-building mindset does not use shame as the main tool. Shame may create temporary urgency, but it often damages clarity. Serious income growth requires honest diagnosis.

9. Consistency Beats Motivation

Consistency is one of the most reliable forces in income growth and wealth building.

Motivation is emotional. It rises after inspiration and falls after difficulty. Consistency is structural. It continues because the behavior has become scheduled, automatic, or identity-based. This is why consistent learning, saving, investing, prospecting, practicing, publishing, selling, networking, or improving often beats occasional bursts of intensity.

In careers, consistency builds trust. A person who performs reliably becomes easier to promote, recommend, hire, or refer. In freelancing, consistency builds reputation. In business, consistency builds customer confidence. In investing, consistency allows time and compounding to work. In personal finance, consistency turns modest actions into meaningful results.

The problem is that consistency looks unimpressive in the beginning. Saving a small amount every week does not feel life-changing. Practicing a skill for 30 minutes daily does not look dramatic. Applying for better roles over months can feel slow. Building a client pipeline one conversation at a time lacks glamour. But repeated actions create accumulation.

Consistency also protects against the self-help trap of emotional dependency. If someone acts only when motivated, progress depends on mood. A serious person designs routines that operate even when motivation is absent.

The key is to make consistency sustainable. Many people fail because they design habits that require too much willpower. They try to transform everything at once. They commit to unrealistic schedules. They burn out and then conclude they lack discipline.

Better systems start smaller. Save automatically. Study at the same time each day. Apply to a fixed number of roles weekly. Review finances monthly. Contact a certain number of prospects. Practice a skill repeatedly. Increase difficulty gradually. Track actions, not only outcomes.

Consistency is not about perfection. Missing one day is not failure. The danger is allowing one missed day to become identity collapse. Wealth builders return to the system quickly.

Motivation starts. Consistency compounds.

10. Income Often Grows With Value Provided, but Value Must Be Marketed and Negotiated

The claim that income grows with value provided is broadly useful. People who solve valuable problems, produce measurable outcomes, and serve markets with willingness to pay often increase earning power.

But value alone does not guarantee income. Value must be recognized, priced, communicated, negotiated, and captured.

This is where many capable people struggle. They create value but do not document it. They help employers save money, improve systems, retain customers, reduce risk, train staff, or generate revenue, but they cannot translate those contributions into evidence. When compensation discussions arise, they rely on effort rather than outcomes.

Markets rarely reward invisible value automatically. Employers may underpay loyal workers who do not negotiate. Clients may accept low prices from skilled freelancers who lack confidence. Industries may undervalue socially important labor. Intermediaries may capture much of the value created by workers. Geographic labor markets may limit pay. Discrimination may reduce compensation despite performance.

To increase income, people must learn not only how to create value but how to capture a fair share of it.

For employees, this may mean documenting achievements, understanding market salaries, applying externally, negotiating offers, moving to higher-value roles, managing relationships with decision-makers, and aligning work with revenue, cost reduction, risk reduction, or strategic priorities. For freelancers and entrepreneurs, it may mean clearer positioning, stronger proof, better pricing, client selection, recurring revenue, and offers tied to outcomes. For investors, it may mean allocating capital to assets that can create or capture economic value over time.

The value equation has several parts: problem severity, buyer ability to pay, scarcity of solution, proof of competence, trust, timing, competition, and negotiation. A person may be highly skilled but operate in a low-paying market. Another may be moderately skilled but positioned in a high-demand niche with strong buyers. Income reflects the whole equation, not skill alone.

The most practical question is: “What problem can I solve that is urgent, valuable, and recognized by people or organizations with resources?”

That question moves income strategy from vague self-improvement to market-aware value creation.

Human Capital: The Foundation of Earning Power

Human capital is the knowledge, skills, health, habits, experience, relationships, and judgment that increase a person’s productive capacity. For most people, human capital is the first wealth-building asset. Before they own substantial investments or businesses, they own their ability to earn.

Increasing human capital can be one of the highest-return financial decisions available. A skill that raises annual income by $10,000 may be worth far more over a career than a one-time investment gain. A credential that opens a higher-paying profession can reshape a household’s financial future. A sales skill, coding skill, management ability, language, technical license, or healthcare specialization can create compounding career benefits.

But human capital is not built only through formal education. It is built through deliberate practice, feedback, difficult projects, mentorship, professional networks, industry knowledge, communication, and reputation. It is also maintained through health, rest, and adaptability.

The modern labor market rewards combinations of skills. Technical ability plus communication. Healthcare knowledge plus management. Data analysis plus business judgment. Trade skill plus reliability and customer service. Creative ability plus marketing. Finance knowledge plus technology. The more valuable combinations a person can offer, the more income paths may open.

Human capital is also perishable. Skills can become outdated. Industries can shrink. Tools can change. This is why continuous learning is not a luxury. It is risk management.

The income strategy for a serious wealth builder begins with this question: “What abilities would make my time more valuable three years from now?”

Market Demand: The Missing Half of the Value Conversation

Many people are told to “follow your passion.” Passion can provide energy, but demand determines whether the market pays. The ideal is to find the overlap between interest, ability, and market need.

Market demand explains why two equally hardworking people can earn very different incomes. A skill in short supply and high demand tends to command more. A skill in abundant supply or low demand commands less. An industry with high profit margins may pay more than an equally difficult industry with tight margins. A job connected to revenue, risk, regulation, or technical scarcity may pay more than a job that is emotionally valuable but budget-constrained.

This can feel unfair because market pay and human importance are not the same. Society may deeply need caregivers, teachers, sanitation workers, and food workers, yet many such roles are not paid in proportion to their social value. Understanding market demand is not the same as endorsing every outcome as just. It is recognizing the system in which income decisions occur.

For individuals, market awareness helps direct effort. If an industry is declining, skill-building may need to focus on transferable abilities. If a field is growing, credentials and experience may produce strong returns. If a role is underpaid locally, remote work, relocation, unionization, entrepreneurship, or specialization may change the equation.

Market demand also affects entrepreneurs. A business idea is not valuable because the founder loves it. It is valuable if customers care enough to pay at prices that exceed costs. The market does not pay for effort alone. It pays for solved problems.

The income lesson is not to abandon meaning. It is to connect meaning with demand where possible.

Bargaining Power: Why Value Does Not Automatically Become Income

Bargaining power determines how much of created value a person can keep.

A worker may create substantial value but lack bargaining power because they have few alternatives, weak labor protections, limited credentials, visa restrictions, caregiving constraints, or poor information about market pay. An employer may capture more of the value because it controls access to customers, capital, systems, and brand. A freelancer may create value but undercharge because they fear losing clients. A business may create value but lack pricing power because competitors can easily copy the service.

Bargaining power improves when alternatives improve. This is why job offers matter. This is why savings matter. A person with an emergency fund can negotiate differently from someone who cannot miss a paycheck. This is why networks matter. Information about opportunities increases leverage. This is why specialization matters. Scarce skills improve pricing power.

Negotiation is often misunderstood as aggression. It is better understood as evidence-based communication about value, alternatives, and terms. A strong negotiator knows the market, documents results, understands the other party’s needs, and asks clearly.

For employees, negotiation may include salary, bonus, equity, flexibility, title, training, relocation support, retirement contributions, or promotion path. For freelancers, it may include scope, price, timeline, revisions, payment terms, retainers, and cancellation clauses. For business owners, it may include contracts, margins, distribution, financing, and supplier terms.

Improving bargaining power may be one of the most direct ways to increase income without changing core skills. The same person can earn more in a better-paying industry, with better negotiation, in a stronger market, or with clearer proof of results.

Financial Discipline: Turning Income Into Wealth

Income growth is valuable, but it is not the same as wealth building.

Wealth is built when income is converted into assets and protected from unnecessary leakage. A person can increase income and still remain financially fragile if spending rises at the same pace. This is why high earners can live paycheck to paycheck and moderate earners can build strong net worth over time.

The Federal Reserve’s Survey of Consumer Finances tracks household assets, liabilities, income, and net worth, making it useful for understanding the difference between earning and owning. ([federalreserve.gov](https://www.federalreserve.gov/econres/scfindex.htm?utm_source=chatgpt.com)) A household’s financial health is not fully described by salary. It depends on savings, debt, investments, insurance, housing costs, retirement assets, and liquidity.

Financial discipline turns income into freedom. It includes saving a portion of income, avoiding destructive debt, investing consistently, managing taxes, maintaining emergency reserves, and controlling lifestyle inflation. Without these habits, higher income can simply fund higher obligations.

The ideal pattern is to increase income and capture part of every increase for wealth building. If a raise arrives, savings and investments should rise before lifestyle absorbs the entire amount. If debt is paid off, the old payment can be redirected toward assets. If a side income develops, part of it can fund emergency savings or retirement contributions.

Income is the raw material. Discipline is the conversion process.

External Factors: The Reality Ambition Must Face

A serious income philosophy must acknowledge external factors.

Geography matters. A skill that pays well in one city may pay less in another. Remote work has changed some opportunities, but not all jobs can be done remotely. Industry matters. Similar roles can pay differently depending on margins, regulation, capital intensity, unionization, and competition. Economic cycles matter. A person graduating into a recession may face different opportunities from someone graduating into a strong labor market.

Family background matters. People raised with financial stability, professional networks, tutoring, safe housing, and career guidance often have advantages that compound quietly. Health matters. Chronic illness, disability, mental health, and caregiving responsibilities shape work capacity. Discrimination matters. Race, gender, class, disability, age, and other factors can influence hiring, pay, promotion, and access to capital.

Luck matters too. Meeting the right mentor, joining a company before rapid growth, buying a home before a housing boom, avoiding illness, or entering an industry at the right time can significantly affect outcomes.

Acknowledging these factors does not eliminate personal responsibility. It makes responsibility more intelligent. A person cannot control every condition, but they can better choose where to focus effort. They can build skills, seek information, improve negotiation, move toward stronger markets, reduce debt, protect health, develop networks, and create options where possible.

The most useful mindset is neither fatalism nor fantasy. Fatalism says nothing can be changed. Fantasy says everything depends only on attitude. Financial maturity says: understand reality clearly, then act where action has leverage.

A Practical Framework for Growing Income

The first step is to identify your current income engine. Are you paid for time, results, credentials, risk, relationships, ownership, or capital? Employees, freelancers, business owners, and investors earn differently. The strategy must match the income model.

The second step is to measure your market. What do people with your skills earn in stronger roles, industries, or locations? What credentials are repeatedly requested? What problems are employers or customers willing to pay more to solve? What trends are increasing demand?

The third step is to build high-return skills. Choose skills that are connected to real opportunities, not only personal interest. Combine technical ability with communication, sales, management, or business judgment where possible. Skill combinations often create more differentiation than isolated skills.

The fourth step is to create proof. Employers and clients pay more when they trust results. Build a portfolio, case studies, metrics, references, certifications, completed projects, testimonials, or documented achievements. Proof reduces perceived risk for the buyer.

The fifth step is to improve bargaining power. Build savings, alternatives, networks, and market information. Apply for roles before desperation. Negotiate from evidence. Raise prices when demand and results support it. Avoid relying on one employer or client without a backup path.

The sixth step is to convert higher income into wealth. Increase savings and investments as income rises. Avoid lifestyle inflation. Pay down high-interest debt. Build emergency reserves. Invest according to a long-term plan. Use income growth to buy future options, not only present comfort.

The seventh step is to review annually. Skills, markets, and goals change. A strategy that worked five years ago may not work today. Income growth requires adaptation without chasing every trend.

How Employees Can Apply the Income Equation

Employees should focus on becoming more valuable and more visible.

More valuable means solving problems that matter to the organization. These may involve revenue growth, cost reduction, risk management, customer retention, operational efficiency, compliance, leadership, technical expertise, or strategic execution. The closer work is to measurable outcomes, the easier it becomes to argue for higher compensation.

More visible means decision-makers understand the contribution. This does not require bragging. It requires documentation and communication. Track achievements. Quantify results. Share progress. Ask managers what outcomes matter most. Build relationships across the organization. Understand how promotions are decided.

Employees should also manage career risk. Staying too long in a low-growth role can reduce lifetime earnings. Loyalty is valuable when it is reciprocated with development, fair pay, and opportunity. When it is not, the market may be a better judge of value than the current employer.

Negotiation should be prepared before it is needed. Research salary ranges. Document outcomes. Understand the employer’s constraints. Practice the conversation. Consider total compensation, not salary alone. Benefits, retirement contributions, equity, flexibility, training, and career path can all carry value.

How Freelancers and Entrepreneurs Can Apply the Income Equation

Freelancers and entrepreneurs must learn pricing, positioning, and profitability.

Many independent workers focus on skill and neglect business mechanics. They become excellent at the service but weak at attracting clients, qualifying buyers, setting prices, managing scope, collecting payment, and building recurring revenue. Income suffers not because the skill lacks value, but because the value is poorly packaged.

A strong offer answers clear questions. Who is the customer? What problem is being solved? Why is it urgent? What result is expected? Why are you credible? What does it cost? What is included? What is excluded? What happens next?

Pricing should reflect more than hours. It should account for expertise, results, demand, risk, taxes, overhead, unpaid time, and opportunity cost. Underpricing may win work but damage the business. Overpricing without proof may reduce trust. The goal is alignment between value, market, and positioning.

Entrepreneurs should also distinguish revenue from profit. A business can look busy and still be financially weak. Profitability, cash flow, customer acquisition cost, retention, margins, and working capital matter. The business owner who ignores these variables may earn less than an employee while taking more risk.

How Investors Should Think About Income and Value

Investors also participate in the income equation. They allocate capital to assets that may create or capture value. Stocks, bonds, real estate, businesses, and other investments all involve expectations about future cash flows, growth, risk, and price.

The investor’s income growth comes not only from labor but from ownership. Dividends, interest, rents, business profits, and capital gains can eventually supplement or replace earned income. But investment income requires capital, and capital usually begins with saved income.

This is why earning power and investing are connected. Higher income can accelerate investing if spending is controlled. Investing can later reduce dependence on labor income. The path from worker to owner begins when surplus income is converted into assets.

Investors must still understand risk. Chasing high returns without diversification, liquidity, or knowledge can destroy capital. The goal is not merely to earn more income from assets. It is to build durable, risk-aware ownership over time.

The Ethical Dimension of Value and Income

It is tempting to treat market income as the ultimate proof of value. That is a mistake.

Markets are powerful but imperfect. They reward scarcity, bargaining power, ownership, and willingness to pay. They do not always reward social importance. A society may pay speculative activities more than caregiving, entertainment more than teaching, or financial engineering more than essential public service. Market income is information, but it is not moral truth.

This matters because people should not measure their worth only by income. A parent raising children, a caregiver supporting an elderly relative, a teacher shaping students, or a community worker helping vulnerable people may create enormous value that is not fully captured in pay.

At the same time, people who need higher income must understand market reality. Moral value and market value are different. A person can honor the social importance of work while still seeking better compensation, stronger bargaining power, or a more sustainable path.

The goal is not to worship the market. It is to understand it well enough to navigate it.

Final Thought: Income Rewards Value, but Only When Value Meets a Market

Your income does not reveal your human worth. It does not measure your kindness, courage, intelligence, sacrifice, or importance to the people who depend on you. But income does reveal something about the market conditions around your skills, your bargaining power, your positioning, your consistency, and the economic value others are willing and able to pay for.

The most useful income mindset is both ambitious and honest.

Low skills can limit income, but skills must be connected to demand. Complaining changes little unless it becomes action. Many people undercharge, especially when they control their own pricing, but salaried workers face different constraints. Fear can kill opportunities, but caution can prevent ruin. Comfort can create complacency, but stability can also support growth. Wealth builders learn continuously because markets change. High income requires discipline to earn and even more discipline to keep. Laziness can have consequences, but the word often hides health, caregiving, burnout, and structural barriers. Consistency beats motivation because repeated behavior compounds. Income often grows with value provided, but value must be visible, marketable, negotiated, and captured.

The path forward is not to blame yourself for every financial limitation. Nor is it to deny the role of personal agency. The path is to study the income equation clearly: skills, demand, proof, bargaining power, consistency, discipline, and context.

Improve what you can. Understand what you cannot fully control. Move toward markets that reward your strengths. Build skills that increase your usefulness. Communicate your value clearly. Negotiate from evidence. Convert income into assets. Keep learning as the economy changes.

Income is not destiny. It is a signal. Read it carefully, then use it to build a stronger financial future.