The Millionaire Mindset: What Wealth Builders Think Differently About Money

The phrase “millionaire mindset” is everywhere. It appears in books, podcasts, short videos, coaching programs, motivational speeches, and social media captions. Sometimes it is useful. More often, it is reduced to a slogan: think rich, act rich, manifest abundance, reject average thinking, and wealth will follow.

That version is attractive because it makes wealth feel entirely controllable. It suggests that the distance between financial struggle and financial success is mainly a matter of attitude. Change the mind, and the money will arrive.

Reality is more serious than that.

Mindset matters, but it does not operate in a vacuum. A person’s financial outcome is shaped by income, education, health, family obligations, inheritance, geography, access to capital, tax systems, inflation, labor markets, housing costs, discrimination, economic cycles, and luck. A disciplined person can still face hardship. A careless person can still inherit wealth. A talented entrepreneur can fail because the timing was wrong. A moderate earner can become wealthy through decades of saving and investing. A high earner can stay financially fragile because every dollar is consumed.

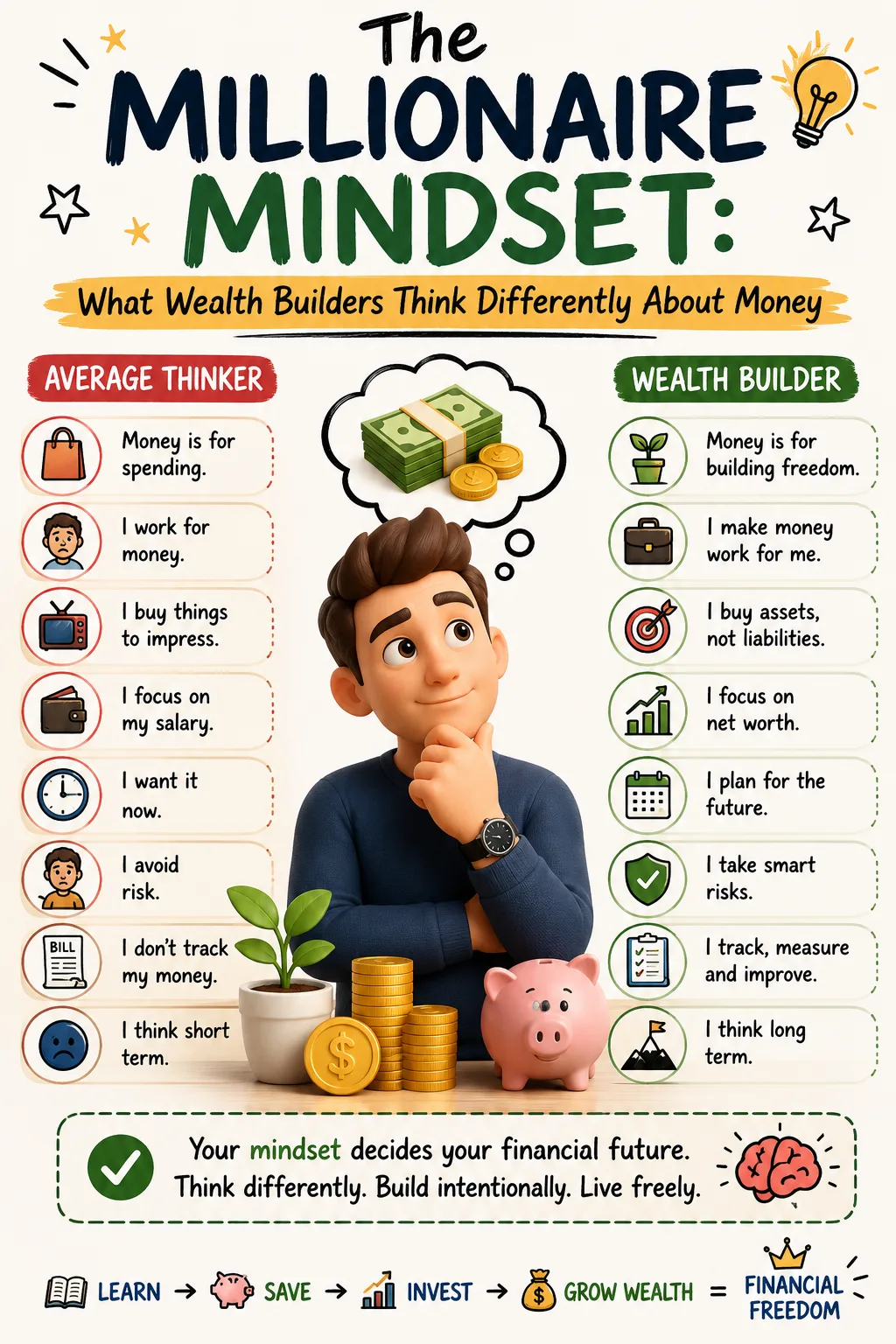

The most useful way to understand the millionaire mindset is not as a mystical belief system. It is a pattern of financial thinking. People who build durable wealth often think differently about time, ownership, risk, learning, spending, failure, and value creation. They do not always have the same personality. They do not all wake up at the same hour, read the same books, buy the same assets, or follow the same routines. But many share an orientation toward assets, patience, discipline, and calculated risk.

The Federal Reserve’s Survey of Consumer Finances is useful here because it examines household balance sheets, assets, debts, pensions, income, and demographic characteristics rather than only visible lifestyle. The 2022 SCF remains the most recent completed survey listed by the Federal Reserve. That distinction matters because millionaire status is about net worth, not salary. Net worth is assets minus liabilities. A person can earn a large income and still have low net worth if the money is spent, borrowed against, or lost. A person can earn steadily, live below their means, invest consistently, and become a millionaire without ever appearing rich.

Global wealth data also shows that millionaire status is highly uneven across countries and households. UBS’s Global Wealth Report 2024 noted that the United States had the highest number of U.S.-dollar millionaires in 2023. Reports like this are useful, but they should be read carefully. A millionaire in one country may have a very different lifestyle, tax situation, purchasing power, and housing market from a millionaire elsewhere. A million dollars of net worth also means something different at age 35 than at age 75, and it means something different when it is liquid than when most of it sits in a primary residence.

So the question is not, “What do millionaires believe that ordinary people do not?” The better question is, “What mental models and behaviors help people convert income, opportunity, and time into lasting net worth?”

That is the millionaire mindset worth studying.

1. Millionaires Think Long-Term

One of the clearest differences between wealth builders and wealth consumers is time horizon.

Many financial mistakes come from short-term thinking. A person buys the car because the monthly payment fits, not because the total cost strengthens their future. They take the holiday because they feel they deserve it, not because they have already funded their obligations. They sell investments during a decline because the pain is immediate, not because the long-term thesis has changed. They chase a speculative asset because someone else became wealthy quickly, not because the risk fits their plan.

Long-term thinking does not mean ignoring the present. People need housing, food, transport, rest, relationships, and joy. A financial life built only around future sacrifice can become emotionally brittle. But millionaires who build and keep wealth often make present decisions through the lens of future value.

They ask different questions. What will this decision cost over five years? Does this purchase create an asset or only a memory? Will this debt increase my options or reduce them? Is this investment aligned with a long-term plan or only a reaction to recent performance? Will this income stream last? What skill, asset, or relationship am I building that future me can benefit from?

The power of long-term thinking is most visible in compounding. Compound growth rewards time, but time rewards only those who remain invested, continue contributing, and avoid ruin. A person who starts investing early does not need to produce extraordinary annual returns to build meaningful wealth. They need consistent contributions, reasonable costs, diversification, patience, and the emotional ability to endure inevitable market declines.

Vanguard’s investing principles emphasize clear goals, a balanced and diversified investment mix, low costs, and long-term discipline. None of these principles sounds dramatic. That is part of their strength. Wealth building is often less about finding a dramatic secret and more about following simple principles long enough for them to matter.

Long-term thinkers also understand that career decisions compound. Skills compound. Reputation compounds. Networks compound. Health compounds. A person who invests in high-demand skills may increase earning power for decades. A business owner who builds systems and customer trust may create an asset that outlives their direct labor. A professional who maintains integrity may be offered opportunities years later because people remember reliability.

Short-term thinking asks, “What can I get now?” Long-term thinking asks, “What can this become?”

That question is central to the millionaire mindset.

2. They Prioritize Asset Ownership

Millionaires are usually not defined by what they earn. They are defined by what they own.

This is the difference between income and wealth. Income is money received from work, business, investments, pensions, rents, royalties, or other sources. Wealth is the value of assets after subtracting liabilities. A high income can help create wealth, but only if some of that income is converted into assets.

Assets are financial engines. Some appreciate. Some produce income. Some reduce future expenses. Some create strategic control. Stocks, bonds, retirement accounts, real estate, private businesses, intellectual property, professional practices, cash reserves, and diversified funds can all play roles in a wealth-building structure. Not every asset is appropriate for every person, and not every asset rises in value. But the ownership principle matters.

Many people focus mainly on earning. Wealth builders focus on converting earnings into ownership.

This is why two households with the same income can look similar for years and end up in very different places. One household upgrades lifestyle every time income rises. The other captures part of each raise and buys assets. At first, the difference may be invisible. Both households live in similar neighborhoods, attend similar events, and earn similar salaries. After 20 years, one has a lifestyle history. The other has a lifestyle and a balance sheet.

Ownership changes the direction of money. A consumer sends money outward. An owner sends money into assets that may send money back. A worker earns from labor. An investor earns from capital. A business owner may earn from systems, people, products, intellectual property, and customer relationships. The most durable wealth often comes from combining labor income with asset ownership over time.

This does not mean everyone must become a full-time entrepreneur or real estate investor. Many millionaires are employees who accumulated wealth gradually through retirement accounts, diversified investments, home equity, and disciplined saving. The point is not that one path is superior for everyone. The point is that wealth requires ownership of something beyond current consumption.

The middle-class trap is confusing the visible lifestyle of wealth with the invisible machinery of wealth. A luxury car is visible. A diversified portfolio is invisible. A paid-off mortgage is invisible. A growing retirement account is invisible. A private business balance sheet is invisible. Yet the invisible assets often matter more.

The millionaire mindset asks: “How can I own more of what grows, produces, or protects value?”

3. They Keep Learning

Wealth builders tend to be students long after formal education ends.

This does not mean every millionaire reads the same books or studies finance obsessively. Some build wealth through technical expertise, sales ability, medical careers, law, engineering, construction, logistics, design, software, real estate, or business operations. But many have a habit of learning that improves their economic usefulness.

Learning increases human capital. Human capital is the present value of a person’s future earning ability. It includes skills, judgment, credibility, relationships, adaptability, and problem-solving ability. For most people, human capital is their first major asset. Before they have investment portfolios, properties, or businesses, they have the ability to earn.

This is why continuous learning matters. A person who keeps improving can move into better roles, negotiate more effectively, start businesses, understand investments, avoid scams, and adapt when industries change. A person who stops learning becomes more vulnerable to economic shifts.

The learning habits of wealth builders often include finance, but not only finance. They study markets, taxes, negotiation, leadership, technology, customer behavior, industry trends, communication, operations, and decision-making. They ask how value is created, captured, protected, and scaled.

Financial literacy is especially important because money decisions affect every stage of wealth building. Research by Olivia Mitchell and Annamaria Lusardi has linked financial literacy to economic decision-making and reviewed evidence that many people lack basic knowledge of interest, inflation, and risk diversification. Related global work has found that only about one in three adults worldwide are financially literate when tested on core concepts such as interest rates, compounding, inflation, and diversification.

These concepts are not academic decorations. A person who does not understand compound interest may underestimate both investment growth and debt costs. A person who does not understand inflation may keep too much long-term money in cash. A person who does not understand diversification may put too much of their future into one asset. A person who does not understand taxes may earn well and keep less than necessary.

Learning also protects against fraud. Scams often rely on urgency, complexity, social proof, and promised certainty. A financially literate person is more likely to ask basic protective questions: How does this investment make money? Who is on the other side? What are the fees? Can I exit? What are the risks? Why is this opportunity being offered to me? What happens if assumptions fail?

The millionaire mindset treats learning as maintenance. Just as a business must maintain equipment and a property owner must maintain a building, a wealth builder must maintain judgment.

4. They Manage Risk Rather Than Avoid It

Millionaires are often described as risk takers. That phrase is incomplete. Durable wealth builders are usually risk managers.

There is a major difference between calculated risk and reckless risk. Calculated risk has research behind it. It has position sizing. It has downside planning. It has a reason. It has a recovery path if things go wrong. Reckless risk relies on excitement, borrowed confidence, excessive leverage, concentration, and the belief that a good story is the same as a good investment.

A person cannot build wealth without taking some risk. Holding all money in cash creates inflation risk. Investing in stocks creates market risk. Buying property creates liquidity, maintenance, financing, and tenant risk. Starting a business creates income and execution risk. Changing careers creates uncertainty. Even staying in the same job carries the risk that the job, company, or industry changes around you.

The question is not whether to take risk. The question is which risks are worth taking and which risks can destroy the plan.

Millionaires who keep wealth tend to respect downside. They may invest aggressively in areas they understand, but they usually care about survival. They diversify where appropriate. They maintain liquidity. They insure major risks. They avoid borrowing so much that one downturn can force liquidation. They learn from losses. They do not assume that a rising market proves their intelligence.

Risk capacity also varies by person. A young investor with stable income, no dependents, and a long time horizon can usually tolerate more portfolio volatility than someone about to retire. A business owner with uneven income may need more cash than a salaried employee. A household with children and one main earner needs different protection from a dual-income household with low fixed costs. A wealthy investor may allocate a small portion of net worth to speculative opportunities and remain secure if they fail. A middle-income household putting most savings into the same opportunity is not taking the same risk, even if the asset is identical.

This is why blindly copying millionaire investments can be dangerous. The wealthy investor’s visible decision may be only one piece of a much larger financial structure. What looks bold from the outside may be small relative to their net worth. What looks simple may have legal, tax, liquidity, and advisory support behind it.

The millionaire mindset does not worship risk. It prices risk. It studies risk. It sizes risk. It asks whether the reward justifies the exposure and whether failure is survivable.

5. Discipline Matters More Than Motivation

Motivation is useful, but it is unreliable. Discipline is the system that keeps working after motivation fades.

Most people feel motivated after reading a financial book, watching an inspiring video, receiving a raise, paying off a debt, or seeing someone else succeed. Motivation can start change. It rarely sustains it for decades. Wealth building requires repeated behavior through boredom, market declines, family obligations, job stress, inflation, unexpected bills, and social pressure.

Discipline appears in ordinary acts. Saving automatically. Investing monthly. Paying bills on time. Avoiding high-interest debt. Reviewing accounts. Increasing contributions when income rises. Keeping insurance current. Saying no to purchases that conflict with goals. Rebalancing a portfolio. Reading before investing. Waiting before making large decisions.

These habits are not glamorous. They are powerful because they reduce dependence on emotional intensity.

The most disciplined wealth builders often design systems. They do not rely on remembering to save what is left at the end of the month. They automate transfers. They do not keep all money in one account where every dollar looks spendable. They separate bills, savings, investments, taxes, and discretionary spending. They do not make investment decisions based on headlines. They use written plans. They do not negotiate with themselves every payday. The decision has already been made.

Discipline also protects against lifestyle inflation. When income rises, many people allow spending to rise automatically. The disciplined person captures part of the increase first. A raise becomes higher retirement contributions, faster debt repayment, a larger emergency fund, or new investment capital before lifestyle absorbs it.

This is not deprivation. It is sequencing. Enjoyment has a place. Wealth builders are not required to live joyless lives. But they understand that every dollar has a job, and if they do not assign the job, impulse and comparison will assign it for them.

Discipline is often confused with personality. People say, “I’m just not disciplined.” But discipline can be engineered. Make the desired behavior automatic. Make the damaging behavior harder. Remove triggers. Create waiting periods. Use accountability. Track progress. Build routines. Start small enough to repeat.

The millionaire mindset knows that wealth is not built by occasional intensity. It is built by consistent execution.

6. They Focus on Value Creation

Many people want to earn more. Millionaires often ask a deeper question: what value can I create, control, or scale?

Income follows value in many forms. An employee earns more by solving more important problems, developing scarce skills, managing complexity, leading people, selling effectively, or producing measurable results. An entrepreneur earns by creating products or services people want enough to pay for. An investor earns by allocating capital to assets that create or capture value. A professional earns by applying expertise to problems clients cannot solve alone.

Value creation is not always glamorous. It may involve improving a supply chain, building software, managing rental property, providing healthcare, designing systems, teaching, manufacturing, repairing, consulting, farming, writing, financing, or organizing people. The common feature is usefulness.

The millionaire mindset is less obsessed with appearing successful and more interested in becoming economically useful. It asks: what problem can I solve? Who has that problem? How painful is it? How much would they pay for a solution? Can the solution be delivered profitably? Can it scale? Can it be protected? Can it be repeated?

This way of thinking is especially important for entrepreneurs. Starting a business is not automatically wealth building. Many businesses fail, stall, or become low-wage jobs for their owners. A business becomes a wealth-building asset when it creates value beyond the owner’s direct labor, has customers, margins, systems, and some durability.

Value creation also applies to careers. An employee who wants higher income should not only ask for more money. They should ask how to become more valuable in the market. That may mean acquiring technical skills, improving communication, moving closer to revenue, managing larger responsibilities, changing industries, or building a reputation for rare reliability.

Wealth is often created at the intersection of skill and demand. Skill without demand can become frustration. Demand without skill can become missed opportunity. The wealth builder studies both.

This mindset also reduces envy. Instead of resenting what others earn, the value creator studies why money is flowing there. What problem is being solved? What asset is being owned? What risk is being taken? What system is being built? What market is being served?

That curiosity is more productive than comparison.

7. They View Failure as Feedback

Failure is unavoidable in wealth building. Investments decline. Businesses struggle. Career moves disappoint. Partnerships fail. Products do not sell. Markets change. Assumptions prove wrong. People make emotional decisions. Debt becomes heavier than expected. Opportunities are missed.

The millionaire mindset does not romanticize failure, but it does not waste it.

There is a difference between a loss and a lesson. A loss becomes a lesson only when it is examined honestly. What did I believe? What did I miss? Was the risk too large? Did I understand the investment? Did I rely on someone else’s confidence? Did I ignore warning signs? Did I use too much debt? Did I confuse luck with skill? Did I act from fear, greed, pride, or urgency? Was the decision bad, or was the outcome unfavorable despite a sound process?

That final question is essential. Not every bad outcome proves a bad decision. Investing involves uncertainty. Business involves uncertainty. A rational decision can still lose money. A foolish decision can still make money. The goal is not to judge decisions only by outcomes. The goal is to improve the process.

This is why resilient wealth builders keep records. Investors may track why they bought, what they expected, what would make them sell, and how the position fits the portfolio. Business owners track margins, customer acquisition, cash flow, and mistakes. Households review budgets, debt patterns, and spending triggers. Documentation turns vague regret into usable information.

Failure also tests identity. Some people interpret financial mistakes as proof that they are bad with money forever. That belief is destructive. Others refuse to admit mistakes because their ego cannot tolerate being wrong. That is also destructive. The healthier response is responsibility without self-destruction.

A person can say, “That decision was poor, and I can learn.” They can also say, “That outcome hurt, but the process was reasonable.” Both statements require maturity.

Millionaires who build through entrepreneurship often experience repeated setbacks. The public sees the successful company, not the rejected pitches, failed products, bad hires, cash shortages, legal disputes, or years of uncertainty. Investors who hold wealth also experience drawdowns and mistakes. The difference is not that they never lose. The difference is that they survive, learn, and adjust.

Failure becomes dangerous when it is denied, repeated, oversized, or financed with money one cannot afford to lose. Failure becomes useful when it is contained and studied.

8. Financial Literacy Is Common Among Wealth Builders

Financial literacy does not guarantee wealth, but financial ignorance makes wealth harder to build and easier to lose.

At a basic level, wealth builders tend to understand net worth, cash flow, compounding, debt, taxes, inflation, investment risk, diversification, liquidity, and insurance. They may not be experts in every area, but they know enough to ask better questions and avoid obvious traps.

Net worth tells whether the household is becoming wealthier. Cash flow tells whether the household can sustain its obligations. Compounding explains why time matters. Debt knowledge explains why interest can either work for or against the borrower. Tax awareness affects how much wealth is retained. Inflation explains why idle money can lose purchasing power. Diversification reduces concentration risk. Liquidity protects against forced selling. Insurance protects against catastrophic loss.

These concepts work together. A person who earns well but ignores taxes, debt, and spending may fail to build wealth. A person who invests but has no emergency fund may be forced to sell at the wrong time. A person who owns a business but ignores cash flow may fail despite profitability on paper. A person who buys property but underestimates maintenance, vacancy, financing, and taxes may discover that ownership is more complicated than appreciation charts suggest.

Financial literacy also changes behavior because it changes what feels normal. Someone who understands compounding may value early investing more. Someone who understands amortization may think differently about long loans. Someone who understands opportunity cost may see a luxury purchase not only as a price but as the future assets it replaces. Someone who understands inflation may realize that cash safety is not the same as long-term purchasing-power safety.

The purpose of financial literacy is not to turn everyone into a professional investor. It is to help people become competent stewards of their own lives. Even people who hire advisers need enough knowledge to evaluate advice, understand incentives, and ask informed questions.

The millionaire mindset treats financial education as a lifelong practice because money decisions do not stop. A person must decide how much to save, where to invest, how to manage debt, when to buy property, how to insure risk, how to support family, how to plan retirement, how to handle inheritance, and how to give. Each stage requires judgment.

Financial literacy is not a luxury topic. It is a defense system.

The Myth of the Self-Made Millionaire

The phrase “self-made millionaire” can be useful, but it can also be misleading.

It usually means the person did not simply inherit a complete fortune. They built wealth through work, business, investing, or professional success. That distinction matters. Many people do create wealth through effort, discipline, risk-taking, and intelligent decisions.

But “self-made” can obscure the support systems and advantages that help wealth accumulate. A person may not inherit millions but may inherit stability, education, confidence, networks, unpaid internships, a safe neighborhood, family housing, healthcare, business advice, or the ability to take risks without immediate catastrophe. Another person may begin with debt, family obligations, unstable housing, medical needs, or limited access to capital.

Humility requires acknowledging both effort and context.

This does not mean individual choices do not matter. They matter greatly. But the millionaire mindset becomes shallow when it pretends that mindset alone explains wealth. A more honest view says that wealth often emerges when personal behavior meets opportunity, time, institutions, and sometimes luck.

Recognizing context should not create helplessness. It should create accuracy. If someone lacks inherited capital, they may need to build more slowly. If income is low, the first wealth move may be skill development rather than investing. If debt is expensive, debt repayment may be the highest-return action. If housing costs are overwhelming, relocation or income growth may matter more than budgeting apps. If access to quality financial advice is limited, simple diversified strategies may be safer than complex products.

The real millionaire mindset is not denial of obstacles. It is disciplined adaptation to reality.

Entrepreneurship, Investing, and Career: Three Paths to Millionaire Status

There is no single millionaire path.

Some become millionaires through entrepreneurship. They build companies, retain equity, create jobs, solve problems, and eventually own an asset worth far more than their original labor. Entrepreneurship can create wealth because business equity can scale. A company can serve many customers, employ people, build systems, and produce profits beyond the founder’s direct hours.

But entrepreneurship is risky. Many businesses fail. Others survive but never create significant wealth. Some become stressful jobs with less security than employment. The millionaire mindset does not worship entrepreneurship blindly. It studies demand, margins, cash flow, financing, customer acquisition, competition, and execution risk.

Others become millionaires through investing. They save consistently, buy diversified assets, use retirement accounts, keep costs low, stay invested, and allow compounding to work over decades. This path is less dramatic than entrepreneurship but more accessible to many households. It requires income surplus, discipline, time, and emotional resilience.

Still others become millionaires through careers. Professionals, managers, skilled tradespeople, executives, engineers, healthcare workers, lawyers, pilots, salespeople, and public-sector employees can build wealth by earning steadily, avoiding lifestyle inflation, and investing over long periods. Their primary asset is human capital, gradually converted into financial capital.

Many people combine paths. An employee invests. An investor starts a side business. A business owner buys real estate. A professional builds intellectual property. A retiree owns a portfolio and a paid-off home. Wealth is often built through overlapping layers rather than one heroic move.

The right path depends on temperament, skills, opportunities, risk tolerance, family situation, geography, and time horizon. A person who hates business operations may not need to force entrepreneurship. A person with unstable income may need liquidity before aggressive investing. A person with strong career prospects may build wealth faster by increasing earning power than by chasing speculative side hustles.

The millionaire mindset is strategic. It does not ask, “Which path sounds most impressive?” It asks, “Which path fits my strengths and can convert effort into assets?”

Why High Income Does Not Guarantee Wealth

One of the most important millionaire mindset lessons is that income is not the finish line.

High income can create a powerful opportunity. It can accelerate saving, investing, debt repayment, education, business formation, and property ownership. But it can also fund larger mistakes. A high-income household can borrow more, buy more, waste more, and appear richer while remaining financially fragile.

This is the income illusion. People assume that earning more automatically means becoming wealthy. It does not. Wealth requires retention. Money must be kept, invested, protected, and allowed to grow.

Lifestyle inflation is the enemy here. A raise becomes a larger apartment. A bonus becomes a luxury trip. A promotion becomes a more expensive car. A business win becomes a bigger house. Each upgrade may feel justified. The person works hard. They want to enjoy success. Yet if every increase in income is matched by an increase in spending, net worth may barely move.

High income also creates social pressure. People earning more may move in circles where expensive lifestyles seem normal. The reference group changes. What once looked luxurious begins to look standard. The household may feel behind even while earning more than most.

Millionaire thinking separates income from identity. It does not ask, “What lifestyle should someone with my income display?” It asks, “How much of this income can become lasting freedom?”

A person who earns $250,000 and saves nothing is financially weaker than a person who earns $90,000 and builds assets steadily, assuming both can meet basic needs. The high earner has more potential, but potential is not wealth until it is converted.

The balance sheet tells the truth that income alone can hide.

The Role of Index Investing and Modern Financial Tools

One current trend supporting ordinary wealth building is the growth of low-cost index investing. Index funds and exchange-traded funds allow investors to own broad baskets of securities at relatively low cost. They do not eliminate risk, and they do not guarantee returns, but they make diversification more accessible than it was for earlier generations.

This matters because many people do not have the time, interest, or expertise to select individual stocks. A disciplined, diversified investment strategy can be more practical than trying to identify winners. Costs also matter. High fees reduce the portion of returns that investors keep. Vanguard’s investing framework explicitly includes minimizing costs as one of its core principles.

Financial tools have also improved access to budgeting, automation, retirement planning, brokerage accounts, and education. A person can automate savings, track spending, invest monthly, compare fees, and learn basic concepts more easily than in the past.

But easier access creates new risks. Online financial education varies widely in quality. Some content teaches disciplined investing. Some sells speculation. Some encourages entrepreneurship. Some encourages gambling disguised as trading. Some provides genuine education. Some monetizes insecurity.

The millionaire mindset uses tools without surrendering judgment to them. A budgeting app does not create discipline by itself. A brokerage account does not create investment wisdom. A podcast does not replace due diligence. An online course does not guarantee business success. Artificial intelligence can support research and productivity, but it does not remove the need for judgment, ethics, and risk management.

Technology can amplify good habits or bad habits. It can automate investing, or it can make impulsive trading easier. It can expand learning, or it can accelerate misinformation. The tool is not the mindset. The mindset determines how the tool is used.

Millionaire Habits That Are Often Misunderstood

Many popular millionaire habits are true only in context.

“Millionaires take risks” is true, but the best ones manage risk rather than gamble recklessly. “Millionaires use debt” is true, but productive leverage differs from consumer debt. “Millionaires own businesses” is often true, but not every business is a wealth-building asset. “Millionaires invest aggressively” may be true for some, but asset allocation depends on age, liquidity, goals, and risk capacity. “Millionaires think big” can be useful, but thinking big without execution is fantasy.

Even frugality can be misunderstood. Many millionaires live below their means, but frugality alone rarely creates significant wealth without income, assets, or investment. Cutting small expenses can help, especially when money is tight, but the larger goal is to increase the gap between income and spending and direct that gap into assets.

Another misunderstood habit is networking. Wealthy people often build networks, but networking is not merely attending events or collecting contacts. Valuable networks are built through competence, trust, generosity, and repeated usefulness. A person who wants access to opportunity should focus on becoming someone others trust with opportunity.

The popular version of millionaire thinking often highlights confidence. Confidence matters, but unearned confidence is dangerous. The more useful trait is calibrated confidence: enough belief to act, enough humility to prepare, and enough self-awareness to change course when evidence demands it.

Millionaire habits should not be copied as rituals. They should be understood as principles.

A Practical Millionaire Mindset Framework

The first principle is clarity. Know your net worth, income, expenses, debts, savings rate, investment accounts, insurance coverage, and financial goals. Wealth cannot be managed if it is not measured.

The second principle is surplus. Create a gap between income and expenses. This may require spending control, but it may also require income growth. A household cannot always budget its way into wealth if income is too low for basic needs. The millionaire mindset addresses both sides: earn more where possible and spend intentionally.

The third principle is ownership. Convert surplus into assets. That may mean retirement accounts, diversified funds, business equity, real estate, cash reserves, education, or other productive assets. The specific mix depends on goals and circumstances.

The fourth principle is protection. Maintain emergency savings, insurance, diversification, and manageable debt. Wealth that is not protected can disappear quickly.

The fifth principle is learning. Improve financial literacy and earning power continuously. Study compounding, taxes, risk, debt, investing, business, and career strategy. Learn enough to avoid being dependent on hype.

The sixth principle is patience. Give assets time to work. Avoid interrupting compounding through panic, impatience, lifestyle inflation, or speculation.

The seventh principle is review. Revisit the plan as life changes. A strategy for a single 25-year-old may not fit a 45-year-old with children, a business, aging parents, and a mortgage. Wealth building requires adaptation without constant emotional reaction.

The eighth principle is humility. Respect luck, uncertainty, and context. Do not confuse a good outcome with a perfect process. Do not confuse a bad year with permanent failure. Do not assume that past success guarantees future success.

This framework is not glamorous. It does not promise overnight wealth. It is designed for durability.

What Ordinary Investors Can Learn from Millionaires

The most useful lesson is not to copy the millionaire lifestyle. It is to copy the asset orientation.

Many people spend their working lives trying to afford the appearance of wealth. The better approach is to build the substance of wealth. That means owning assets before overbuying luxuries, funding retirement before financing status, maintaining liquidity before chasing speculation, and measuring progress by net worth rather than applause.

Ordinary investors can also learn patience. Wealth often accumulates slowly, then suddenly appears impressive after years of invisible progress. The early years of investing can feel underwhelming because contributions do most of the work. Later, the portfolio itself begins to contribute more meaningfully. But that later stage arrives only if the early stage is respected.

They can learn risk discipline. Do not put the entire future into one asset. Do not borrow heavily for uncertain returns. Do not invest money needed for near-term obligations. Do not confuse popularity with safety. Do not assume that a wealthy person’s investment is suitable for your life.

They can learn the importance of financial literacy. A person does not need to become an expert in everything, but they should understand enough to make informed decisions. The cost of ignorance is too high.

They can learn to focus on value creation. Whether through employment, business, investing, or professional expertise, money follows usefulness over time. The more valuable the problems a person can solve, the more opportunities they are likely to see.

Most of all, they can learn that wealth is not an identity to perform. It is a structure to build.

The Millionaire Mindset Is Not a Guarantee

It is important to say this clearly: the millionaire mindset does not guarantee millionaire status.

A person can think long-term, work hard, save, invest, learn, and still face setbacks. Markets can disappoint over certain periods. Health can fail. Families can need support. Jobs can disappear. Businesses can struggle. Inflation can reduce purchasing power. Housing can become unaffordable. Life can interrupt even the best plan.

But the absence of a guarantee does not mean the habits are meaningless. Good habits improve odds. They increase resilience. They create more options. They reduce avoidable mistakes. They allow opportunity to be used when it appears.

The millionaire mindset should never be used to blame people for poverty or hardship. Nor should it be dismissed because luck and structure matter. The mature view holds both truths: circumstances shape outcomes, and behavior still matters.

Financial education is most powerful when it respects reality and still points toward agency.

Final Thought: Millionaires Build Systems Around Their Ambition

The millionaire mindset is not simply wanting more money. Nearly everyone wants more money. The difference is in how desire is organized.

Wealth builders turn ambition into systems. They think long-term. They buy assets. They keep learning. They manage risk. They rely on discipline more than motivation. They create value. They learn from failure. They understand the basic mechanics of money. They measure net worth instead of confusing income with wealth. They know that looking rich and becoming rich are often opposite behaviors.

They also understand that money is not only about accumulation. Wealth can buy security, time, generosity, mobility, healthcare, education, independence, and the ability to make decisions without constant financial fear. That is why the mindset matters. It is not about worshiping millionaires. It is about learning how durable financial freedom is built.

The most important millionaire habit may be the quietest one: converting today’s resources into tomorrow’s options.

Every automatic investment, every avoided bad debt, every skill learned, every risk studied, every expense controlled, every asset purchased, and every mistake examined adds to those options. The process may not look dramatic from the outside. It may not impress anyone this month. But over years, it can change the shape of a life.

Millionaire thinking is not magic. It is disciplined ownership of the future.