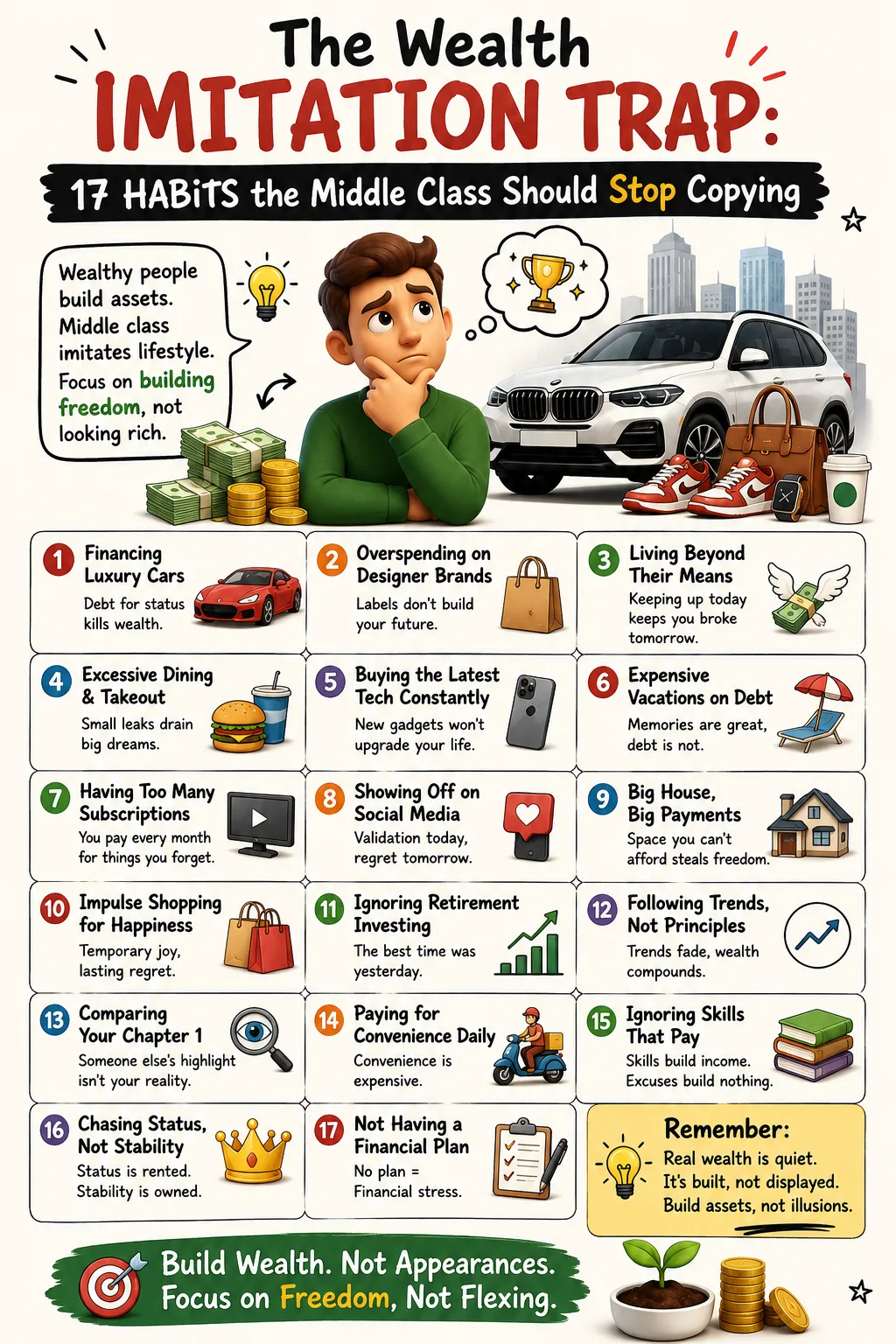

The Wealth Imitation Trap: 17 Habits the Middle Class Should Stop Copying

Most people do not see how wealth is built. They see how wealth is spent.

They see the car, not the balance sheet. They see the holiday, not the cash reserves. They see the house, not the property tax bill. They see the founder on stage, not the years of failed prototypes, unpaid invoices, personal guarantees, and investor dilution. They see the celebrity endorsing an investment, not the financial adviser, legal team, and diversified portfolio sitting behind the endorsement.

This is how the middle class often falls into the wealth imitation trap. Instead of studying the quiet mechanics of wealth, people copy the visible behaviors associated with affluence. They finance cars, stretch for houses, chase premium products, trade risky assets, start side businesses, copy portfolios, and assume debt is sophisticated simply because wealthy people use it.

The problem is not ambition. Ambition is useful. The problem is copying strategies without copying the context that makes those strategies survivable.

A wealthy person may finance a car because their money is invested elsewhere, their cash flow is abundant, and the vehicle serves a business purpose. A middle-income household may finance the same kind of car and lose the ability to save. A wealthy investor may take concentrated risk because 90 percent of their life is already financially secure. A middle-class investor may copy the same risk and put their entire future in danger. A business owner may quit a job because they have capital, clients, experience, and a spouse with stable income. Another person may quit because entrepreneurship sounds glamorous online.

The same behavior can be wise or reckless depending on the financial foundation underneath it.

That is why wealth should not be studied through appearances. It should be studied through ownership, cash flow, risk management, tax efficiency, time, and discipline. The Federal Reserve’s Survey of Consumer Finances tracks household balance sheets, income, pensions, assets, and liabilities, which is why it is more useful than lifestyle observation for understanding wealth. Research from the Richmond Fed also shows that households in the middle of the wealth distribution tend to hold more of their wealth in real estate and physical assets, while wealthier households are more heavily invested in stocks and, especially at the top, private business equity.

That distinction matters. Wealth is not primarily built by looking rich. Wealth is built by owning assets that can appreciate, produce income, reduce future costs, or give the owner more control. The danger for the middle class is that visible wealth habits often consume the very capital needed to build invisible wealth.

This article examines 17 habits the middle class should stop copying blindly. The goal is not to condemn every luxury purchase, every loan, every business idea, or every investment risk. The goal is to separate financial strategy from financial theater.

1. Financing Luxury Cars Before Building Financial Resilience

A luxury car is one of the easiest ways to feel wealthy without becoming wealthy. It is visible, emotional, and socially legible. People understand the signal immediately. A retirement account does not turn heads at a traffic light. A paid-off credit card balance does not photograph well. A diversified index fund will not impress neighbors. A luxury car can do all of that in seconds.

That is why it is so dangerous for people who are still building their first layer of financial security.

There are circumstances where a high-income or high-net-worth person may finance a vehicle without damaging their financial life. They may preserve liquidity, use the vehicle for legitimate business purposes, or choose financing because the interest rate is attractive relative to other uses of cash. They may also have enough assets that the car payment represents a tiny fraction of monthly income.

For a middle-class household, the same payment can be a financial anchor. The damage is not limited to the monthly loan. There is insurance, maintenance, fuel, registration, depreciation, repairs, and the opportunity cost of the money that could have gone toward savings or investments.

The most expensive part of the luxury car habit is often what it prevents. A $900 monthly vehicle payment is not only $900. It may be the missing emergency fund. It may be the retirement contribution never made. It may be the credit card balance that cannot be paid down. It may be the down payment delayed for years. It may be the reason a household earns more but never feels ahead.

A car is transportation first. It can be comfort, enjoyment, and identity after the basics are secure. But when a vehicle payment competes with an emergency fund, retirement savings, high-interest debt repayment, or housing stability, the car is no longer a symbol of progress. It is a claim on future freedom.

2. Buying a Large Home Too Early

Homeownership can be one of the most powerful wealth-building tools available to ordinary households. It can create forced savings through mortgage principal repayment. It can provide stability. It can protect against some forms of rent inflation. Over long periods, it may build equity and become a major part of net worth.

But buying too much house too early can turn a wealth-building asset into a financial trap.

The middle class often sees wealthy households living in large homes and assumes the house itself is the wealth strategy. Sometimes it is. Often, it is the result of wealth that already exists. A large home is affordable to a wealthy family because it is supported by assets, income, reserves, and flexibility. For a household still building financial stability, the same home can absorb every dollar of surplus.

The mortgage is only the cover charge. Bigger homes usually mean higher property taxes, higher insurance, higher utilities, more furniture, more repairs, more maintenance, more cleaning, more landscaping, and more pressure to maintain a certain lifestyle. A larger home also increases the cost of mistakes. A roof, plumbing issue, heating system, or structural repair can become a major financial event.

There is also a liquidity problem. Home equity is real wealth, but it is not the same as cash. A household may technically own an appreciating asset while still struggling to pay bills. This is why being “house rich and cash poor” is so uncomfortable. The asset exists, but the household cannot easily use it without borrowing, refinancing, downsizing, or selling.

The better question is not, “What is the largest house the bank will approve?” It is, “What home allows us to build wealth while still saving, investing, insuring, and living with margin?”

A home should support a financial life, not consume it.

3. Chasing Status Purchases

Status spending is one of the oldest financial traps. Every generation has its version: designer clothing, luxury watches, premium electronics, exclusive memberships, private clubs, expensive handbags, rare sneakers, high-end restaurants, curated travel, and the constant upgrading of visible goods.

The middle class often copies these purchases because status goods appear to offer membership in a higher economic class. They create the feeling of arrival. They suggest success before the balance sheet confirms it.

The danger is that status purchases usually depreciate financially while appreciating emotionally. They feel meaningful at the moment of purchase, then quickly become normal. The first luxury item feels like a milestone. The second feels like a standard. The third becomes expected. This is how lifestyle inflation quietly rewrites the definition of “enough.”

Wealthy households can also waste money on status. Not all rich people are financially wise. But when a person with millions in assets buys a luxury watch, the purchase may represent a tiny percentage of net worth. When a middle-income household buys the same item on credit, the purchase may delay savings, increase debt, and create pressure to maintain an image that has not been financially earned.

The practical test is simple: does the purchase make you poorer in order to make you look richer?

There is nothing wrong with beauty, craftsmanship, or enjoyment. Money should improve life. But status spending becomes dangerous when the purchase is mainly designed to communicate wealth to others. The strongest financial position is often the opposite: looking normal while quietly becoming financially stronger.

4. Assuming All Debt Is “Good Debt”

Wealthy people often use debt. Businesses borrow to expand. Real estate investors use mortgages. Private equity firms use leverage. High-net-worth households may borrow against investment portfolios instead of selling assets. This leads many people to conclude that debt is inherently sophisticated.

That is a dangerous half-truth.

Debt is not good because wealthy people use it. Debt is useful when it finances productive assets, improves long-term earning power, or creates a favorable risk-adjusted return. Debt is dangerous when it funds consumption, hides unaffordability, or magnifies losses that the borrower cannot absorb.

A mortgage on an affordable home may help build equity. A student loan for a high-return field may increase lifetime earnings. A business loan may be productive if the business has customers, margins, and a realistic repayment plan. But credit card debt for lifestyle spending is not good debt. A large car loan that prevents investing is not good debt. A personal loan used to fund appearances is not good debt. Borrowing to speculate in assets one does not understand is not good debt.

Leverage has two faces. It can accelerate wealth when asset values rise and cash flow is sufficient. It can destroy wealth when income falls, rates rise, asset prices decline, or repayment terms tighten. Wealthy borrowers may survive those conditions because they have liquidity and diversified assets. Middle-class borrowers may not.

The right question is not, “Can I borrow?” It is, “What does this debt produce, what can go wrong, and can I survive the downside?”

5. Investing Without Understanding Risk

Many people begin investing by copying. They copy a friend, influencer, colleague, celebrity, business channel, online forum, or wealthy investor. Copying feels efficient because it avoids the discomfort of learning. But investing without understanding risk can turn confidence into expensive tuition.

Risk is not only volatility. Risk is the chance that money will not be available when needed. Risk is concentration. Risk is illiquidity. Risk is paying too high a price. Risk is misunderstanding tax consequences. Risk is owning an asset that can fall 60 percent while believing it can only rise. Risk is using borrowed money. Risk is confusing a bull market with personal skill.

A wealthy investor may hold complex assets because they understand the role those assets play in a broader portfolio. They may own private equity, hedge funds, real estate partnerships, concentrated founder shares, options, or alternative assets. They may also have advisers helping them assess liquidity, taxes, estate planning, and downside exposure.

A middle-class investor who copies the asset without the planning may be taking risk without understanding it. That is not investing. It is financial mimicry.

Vanguard’s investing principles emphasize goals, balance, cost, and discipline, including the importance of maintaining perspective and sticking with a plan over time. Those principles are not glamorous, but they are powerful because they match the real problem most investors face: not finding the most exciting asset, but building a portfolio they can hold through uncertainty.

The best investment is not the one that sounds smartest at dinner. It is the one that fits the investor’s goals, time horizon, liquidity needs, temperament, and risk capacity.

6. Quitting Stable Income Too Quickly

Entrepreneurship has produced enormous wealth. Many of the world’s richest people built or owned businesses. That fact has inspired millions of middle-class workers to see employment as a limitation and business ownership as the path to freedom.

The aspiration is valid. The execution is where people get hurt.

There is a major difference between building a business while managing risk and quitting stable income because employment feels ordinary. A job may not be glamorous, but it can be a powerful financial platform. It provides cash flow, benefits, borrowing capacity, retirement contributions, health coverage, professional experience, and time to build assets.

Quitting too quickly can turn a promising business idea into a survival crisis. When personal bills depend immediately on a young business, the founder may be forced into desperate decisions. They may underprice work, borrow too much, accept bad clients, skip insurance, drain retirement savings, or abandon a good idea because the runway was too short.

Wealthy entrepreneurs often appear fearless in hindsight, but many had advantages that are not visible in the heroic version of the story: family capital, elite networks, a spouse with income, previous exits, investors, industry experience, or the ability to fail without homelessness.

The middle class should not avoid entrepreneurship. It should de-risk it. Build savings. Test demand. Find paying customers. Understand margins. Keep fixed expenses low. Maintain health coverage where possible. Build the business before depending entirely on it.

The goal is not to worship stable income forever. The goal is to use stable income as a bridge to ownership, not burn the bridge before the other side exists.

7. Overconcentrating Investments

Concentration can create wealth. Many fortunes began with concentrated ownership in one business, one stock, one property portfolio, or one industry. But concentration is also how many fortunes disappear.

The middle class often hears the success stories and misses the survivorship bias. People talk about the founder whose company became worth billions. They talk less about the thousands of founders whose equity became worthless. They celebrate the investor who bought one stock early and held it. They ignore the investors who concentrated in companies that collapsed. They admire the crypto millionaire and forget the people who bought near the top.

Concentration is powerful because it amplifies outcomes. That is the point. But amplification works both ways. A portfolio dominated by one stock, one cryptocurrency, one employer, one rental property, or one business is not merely an investment strategy. It is a dependency.

This is especially dangerous when income is also concentrated. An employee who holds most of their investments in their employer’s stock is exposed to the same company twice. If the company struggles, the person may lose income and wealth at the same time. A small business owner whose entire net worth sits inside the business faces a similar risk.

Diversification does not guarantee profit, and it does not eliminate losses. Morningstar has noted that diversification is more nuanced than simply assuming every asset will move in opposite directions, especially during periods when many assets become positively correlated. Still, diversification remains one of the most important defenses against life-changing concentration errors.

Wealthy people may accept concentration because they have already secured enough elsewhere. The middle class should be careful about concentrating before the foundation is built.

8. Using Credit to Maintain a Lifestyle

Credit can disguise a financial gap for a long time. It allows a household to live as though income is higher than it really is. The danger is that the gap does not disappear. It accumulates.

Using credit for lifestyle spending is different from using credit for convenience and paying it off in full. The problem begins when borrowed money funds restaurants, travel, clothing, electronics, gifts, celebrations, furniture, subscriptions, and social expectations that ordinary income cannot support.

At first, the household may feel in control. Minimum payments are manageable. The lifestyle continues. No one else knows. But interest begins to claim future income. A portion of every paycheck now belongs to past consumption. The household becomes less able to save, invest, or handle emergencies. Eventually, credit that once created flexibility becomes a cage.

This habit is often copied from visible wealth. People see affluent lifestyles and imitate the spending pattern without the asset base behind it. But wealthy consumption funded by income from assets is different from middle-class consumption funded by revolving debt.

The healthiest use of credit is strategic, temporary, and affordable. It should not be the bridge between desired identity and actual cash flow.

9. Treating Every Hobby as an Investment

There is a modern habit of rebranding consumption as investing. Sneakers become an alternative asset class. Handbags become stores of value. Trading cards become portfolio holdings. Watches become inflation hedges. Wine, art, toys, collectibles, and memorabilia are described in the language of wealth.

Some collectibles do rise in value. Some rare items have produced extraordinary returns. But the existence of profitable examples does not make every hobby an investment strategy.

Collectibles have several problems for ordinary households. They can be illiquid, meaning they may not sell quickly when cash is needed. Their value can depend on condition, authenticity, fashion, scarcity, platform fees, buyer sentiment, and expert appraisal. Markets can be thin. Storage and insurance can matter. The resale price seen online is not always the price an ordinary seller will receive.

The greatest danger is psychological. Calling a purchase an investment can give permission to overspend. A person who would hesitate to buy a luxury item for pleasure may feel justified buying it “as an asset.” But if the item does not produce income, has uncertain resale demand, and represents money that should have gone to savings, it is not functioning like a core wealth asset.

Hobbies are allowed. Enjoyment matters. But hobbies should be funded from discretionary money after the financial foundation is protected. An investment should be judged by expected return, risk, liquidity, costs, taxes, and role in the portfolio. A hobby should be judged by joy. Confusing the two can be expensive.

10. Ignoring Emergency Savings Because “Cash Is Lazy”

Some wealthy investors dislike holding excess cash because they have access to credit, liquid assets, and multiple sources of income. They may view cash as inefficient because it can lose purchasing power to inflation and may earn less than long-term investments.

That logic can be dangerous when copied too early.

For a household without substantial assets, cash is not lazy. Cash is protective. It prevents a temporary problem from becoming expensive debt. It allows a person to leave a bad job, repair a car, handle a medical bill, support family, move for opportunity, or survive a delayed paycheck.

The Federal Reserve reported that in 2024, 63 percent of adults said they would cover a hypothetical $400 emergency expense exclusively with cash or its equivalent, leaving a significant share who would need another method. This is why emergency savings remain central to financial resilience. Without cash, even small disruptions can force borrowing or asset sales at bad times.

The middle class should not copy the idea that every dollar must be aggressively invested. Investing is essential for long-term wealth, but cash reserves protect the investment plan from being interrupted. A person who has to sell investments during a downturn to pay rent may discover that being fully invested was not sophisticated. It was fragile.

The right amount of cash depends on income stability, household size, health risks, employment security, insurance coverage, and fixed expenses. But the principle is universal: before chasing maximum return, secure survival.

11. Following Celebrity Investment Trends

Celebrity investment culture is seductive because it combines fame, wealth, and urgency. A famous person promotes a cryptocurrency, startup, app, real estate trend, private fund, product, or trading strategy. The audience assumes the celebrity has access to superior information. Sometimes they do. Often, they are being paid, receiving equity, following advisers, or taking a small risk relative to their net worth.

A celebrity can lose money on a speculative investment and remain wealthy. A middle-class household may not have that luxury.

The deeper problem is that endorsements replace due diligence. People stop asking basic questions. What is the asset worth? How does it produce cash flow? What are the risks? Who is selling? What are the fees? Is there liquidity? What happens if the price falls? How does this fit into the rest of the portfolio?

Social proof is not analysis. Fame is not a valuation method. Confidence is not a margin of safety.

The middle class should be especially cautious when an investment is marketed with urgency, exclusivity, lifestyle imagery, or promises of easy wealth. Serious investing is usually less theatrical. It involves reading, comparing, understanding costs, assessing risk, and deciding how much exposure is appropriate.

The best response to a celebrity investment trend is not automatic rejection. It is disciplined skepticism. If the investment cannot survive ordinary questions, it does not deserve extraordinary trust.

12. Equating High Income With Wealth

High income helps. It can make wealth building easier because there is more potential surplus after essential expenses. But income is not wealth. Income is flow. Wealth is stock. Income is what comes in. Wealth is what remains and grows.

This distinction is one of the most important financial lessons for the middle class. A person earning a large salary can still have low net worth if spending, taxes, debt, housing, private school, luxury consumption, and lifestyle inflation consume everything. A person with a moderate income can build meaningful wealth over time if they save consistently, avoid destructive debt, invest, and own appreciating assets.

The Federal Reserve’s Survey of Consumer Finances is useful because it distinguishes balance sheets from income, showing that household financial condition depends on assets and liabilities as well as earnings. The Richmond Fed’s discussion of portfolios across the wealth distribution reinforces this point: wealthier households tend to own more financial and business assets, not merely higher monthly consumption.

High earners can be especially vulnerable to the income illusion. Because money arrives frequently and in large amounts, they may assume they are financially secure. But if the income stops and there are few assets, the lifestyle collapses quickly.

The middle class should measure progress through net worth, savings rate, debt reduction, investment balances, insurance coverage, and income resilience. Salary matters. But the balance sheet tells the truth.

13. Believing Every Side Hustle Will Scale

The modern economy has made side hustles more accessible than ever. Freelancing, content creation, e-commerce, coaching, tutoring, delivery platforms, digital products, affiliate marketing, consulting, and creator businesses can all generate supplemental income. Some become major enterprises.

But many side hustles remain small. That does not make them failures. A modest side income can pay down debt, build savings, fund investments, or create breathing room. The problem begins when people copy the exceptional success stories and assume every side hustle will become a scalable business.

Scaling requires more than effort. It requires demand, distribution, systems, pricing power, margins, repeat customers, technology, capital, management, and often luck. A person can work extremely hard and still build something that remains limited by time, geography, competition, or low margins.

This matters because people sometimes spend too much money trying to look like entrepreneurs before the business model is proven. They buy courses, branding packages, equipment, inventory, software, websites, ads, coaching, and office space before validating demand. The side hustle becomes another form of consumption, dressed in business language.

The middle-class approach should be practical. Start small. Validate with paying customers. Track profit, not just revenue. Protect the main income source until the business is stable. Avoid confusing audience attention with cash flow. Use side income to strengthen the balance sheet.

A side hustle does not need to become an empire to be valuable. But it should not become a financial leak in the name of ambition.

14. Constantly Upgrading Lifestyle as Income Rises

Lifestyle inflation is one of the most common reasons people earn more without becoming wealthier. Every raise creates a new normal. A better apartment. A newer car. More restaurants. Better holidays. Higher-end clothing. More convenience. More subscriptions. More expensive hobbies. More social obligations.

The process is subtle because each upgrade feels reasonable. The person is not being reckless in one dramatic moment. They are simply allowing spending to rise with income until the surplus disappears.

This habit is often copied from wealthier circles. As income rises, people spend more time around colleagues, friends, or neighbors with higher consumption patterns. The reference group changes. What once felt expensive begins to feel standard. The household may still be middle class financially, but its lifestyle expectations have moved upward.

The danger is that lifestyle inflation steals the most powerful wealth-building moment: the gap between rising income and old expenses. If a person receives a raise and keeps living mostly the same way, the difference can be invested, saved, or used to reduce debt. If every raise is absorbed, income growth produces comfort but not freedom.

The solution is not permanent deprivation. It is intentional upgrade sequencing. Increase savings first, then upgrade lifestyle from what remains. Capture a portion of every raise for wealth building before lifestyle claims it.

A higher income should widen the distance between survival and stress. If it only raises the cost of being you, it has not created wealth.

15. Ignoring Tax Planning Until Wealth Arrives

Many middle-class households assume tax planning is only for the rich. This belief can be costly. While advanced tax strategies may require specialized advice and significant assets, basic tax awareness matters long before someone becomes wealthy.

Tax-efficient retirement accounts, employer plans, health savings accounts where available, education accounts, capital gains rules, business expense documentation, charitable giving, asset location, and withdrawal planning can all affect long-term wealth. The exact tools vary by country and personal situation, but the principle is consistent: what matters is not only what you earn, but what you keep and compound.

Wealthy households often pay professionals to coordinate taxes, investments, estates, businesses, insurance, and charitable planning. The middle class may not need a full advisory team, but ignoring taxes entirely means missing opportunities that can compound over decades.

The mistake is copying wealthy consumption while ignoring wealthy administration. Many affluent households are organized. They track documents. They plan before year-end. They understand deductions, contributions, tax brackets, and asset sales. They coordinate major decisions with tax consequences in mind.

Tax planning should be ethical, legal, and tailored. It is not about evasion. It is about structure. A household that invests tax-efficiently and avoids unnecessary tax drag may accumulate significantly more wealth over time than one that treats taxes as an afterthought.

16. Copying High-Risk Investment Portfolios

Some wealthy investors hold portfolios that would be inappropriate for the average household. They may invest in startups, private funds, concentrated stocks, speculative real estate, cryptocurrency, commodities, venture capital, distressed debt, options, or highly illiquid assets. These investments can make sense within a larger financial structure.

The key phrase is “within a larger financial structure.”

A wealthy investor may allocate 5 percent of net worth to a speculative opportunity. If it fails, their home, retirement, healthcare, children’s education, and basic lifestyle remain intact. A middle-class investor may put 50 percent of savings into the same opportunity and call it bold. The asset is the same. The risk is not.

High-risk portfolios are especially dangerous when investors focus on upside stories and ignore position sizing. Risk is not only about what you buy. It is about how much you buy, how it is funded, when you need the money, and what happens if it falls sharply.

Morningstar’s investor behavior research, including its Mind the Gap work, focuses on the difference between reported investment returns and the returns investors actually experience because of timing decisions and behavior. This is relevant because high-risk assets often produce emotional decisions. People buy after excitement and sell after pain.

The middle class should not avoid all risk. Risk is necessary for growth. But risk should be intentional, diversified, sized appropriately, and connected to a plan. The goal is not to become rich quickly at the cost of possibly starting over. The goal is to become financially stronger without making one mistake that destroys years of progress.

17. Measuring Success by Visible Wealth

The final habit is the root of many others: measuring success by what can be seen.

Visible wealth is easy to understand. It includes cars, homes, clothes, restaurants, holidays, watches, jewelry, schools, neighborhoods, and social circles. These things may reflect wealth, but they can also reflect debt, high income without savings, family support, business write-offs, or simple prioritization of consumption.

Invisible wealth is harder to admire because it is quiet. It includes a paid-off loan, six months of emergency savings, a growing retirement account, diversified investments, insurance coverage, a strong credit profile, a profitable business, low fixed expenses, and the ability to make decisions without panic.

The middle class often underestimates invisible wealth because it does not provide immediate social reward. No one applauds an automatic investment contribution. No one compliments a lower debt-to-income ratio at dinner. No one sees the household that chose a smaller home and gained the ability to sleep well.

But invisible wealth is the foundation of freedom. It gives people choices. It allows career changes, family support, generosity, retirement, resilience, and dignity under pressure. Visible wealth asks to be noticed. Invisible wealth works whether anyone notices or not.

The better scorecard is net worth, savings rate, debt quality, asset ownership, income durability, liquidity, and peace of mind. A person who improves those measures is becoming wealthier even if their lifestyle looks unchanged.

What the Middle Class Should Copy Instead

The lesson is not that wealthy people have nothing to teach. Many wealthy households do practice habits worth studying. The middle class should copy the principles beneath wealth, not the surface signals around it.

Copy ownership. Wealthy households often own businesses, stocks, real estate, retirement assets, intellectual property, or other claims on future income. Ownership allows money to work beyond labor. The middle class can begin with accessible forms of ownership, such as retirement accounts, diversified funds, small business equity, or affordable real estate when appropriate.

Copy discipline. Wealth is often built through repeated boring actions: saving, investing, reviewing expenses, maintaining insurance, avoiding destructive debt, and staying invested through volatility. Vanguard’s principles of goals, balance, cost, and discipline capture this less glamorous but more durable side of investing.

Copy risk management. Many wealthy people protect the downside carefully. They insure major risks, diversify, maintain liquidity, use legal structures, and avoid putting their entire life at risk for one opportunity. The middle class should do the same at an appropriate scale.

Copy tax awareness. Wealthy households often plan before acting. They consider the tax effects of selling, buying, contributing, borrowing, gifting, and investing. Middle-class households can benefit from understanding available tax-advantaged accounts and planning tools in their jurisdiction.

Copy patience. Real wealth often grows slowly before it grows visibly. The early years of saving and investing can feel unimpressive. Then compounding begins to matter. Time is not a decorative part of wealth building. It is one of the main ingredients.

The Middle-Class Wealth Framework

A stronger middle-class wealth strategy begins with financial order. Before copying advanced strategies, a household should know its income, expenses, assets, liabilities, interest rates, insurance coverage, and savings rate. Confusion is expensive. Clarity is a financial asset.

The next step is liquidity. A starter emergency fund can prevent small shocks from becoming debt. Over time, that fund should grow based on household risk. A single-income family with children and a mortgage needs more protection than a dual-income household with low fixed costs.

After liquidity comes debt quality. High-interest consumer debt should be reduced aggressively because it competes directly with wealth building. Lower-cost debt tied to productive assets may be manageable, but it still needs discipline and monitoring.

Then comes consistent investing. For many households, diversified low-cost funds, retirement accounts, and automatic contributions provide a practical foundation. The specific investment choices depend on country, tax rules, age, risk tolerance, and goals. But the general principle is broad ownership rather than constant speculation.

Next is income growth. The middle class should not rely only on cutting expenses. Earning power matters. Skills, credentials, negotiation, career moves, business ownership, and selective side income can all expand the financial gap available for saving and investing.

Finally, the household should protect progress. Insurance, estate documents, tax planning, diversification, and prudent cash reserves keep one event from undoing years of work.

This framework is not flashy. That is why it works. It is built around resilience before status, ownership before consumption, and systems before inspiration.

Why Context Matters More Than Imitation

Financial advice often fails because it ignores context. “Buy real estate” may be excellent advice for one person and terrible advice for another. “Start a business” may be liberating for one household and reckless for another. “Use debt strategically” may be appropriate for an experienced investor and disastrous for someone with unstable income. “Invest aggressively” may make sense for a young person with a long time horizon and no dependents, but not for someone who needs the money next year.

Context includes income stability, household obligations, debt levels, health, dependents, country, taxes, age, risk tolerance, skills, savings, insurance, and access to advice. Wealthy households often have a wider margin for error. Middle-class households must be more careful because one mistake can take years to repair.

This does not mean the middle class should be timid. Excessive fear can also be costly. Avoiding all investing, refusing every opportunity, and holding too much cash forever can limit wealth. The point is not to avoid risk. It is to take the right risks in the right order.

A person with no emergency fund should not copy an illiquid investment strategy. A person with high-interest debt should be cautious about speculative assets. A person with unstable income should value cash more than someone with multiple assets. A person with dependents should think differently about insurance than a single person with few obligations.

Good financial strategy is personal without being random. It is built from principles, then adjusted to reality.

The Quiet Advantage of Not Looking Rich

One of the most underrated middle-class advantages is the ability to avoid lifestyle pressure. A household that does not need to appear wealthy can redirect money toward becoming wealthy.

This is harder than it sounds. Social comparison is powerful. People want to feel respected. They want their children to feel included. They want to reward themselves for hard work. They want their lifestyle to reflect progress. None of that is wrong. But if every sign of progress must be visible, wealth building becomes slow.

The quiet path is different. It allows income to rise faster than spending. It allows an older car to coexist with a growing portfolio. It allows a modest home to fund better sleep. It allows a family to take fewer status holidays and more strategic steps. It allows a person to be underestimated while their balance sheet strengthens.

This is not about pretending money does not matter. It is about understanding what money is for. Money is not only for display. It is for security, time, opportunity, generosity, ownership, and independence.

When the middle class stops copying visible wealth, it can begin building durable wealth.

The Real Wealth Habits Worth Keeping

The habits worth keeping are rarely the ones that trend online. Spend less than you earn. Increase the gap between income and expenses. Build liquidity. Avoid high-interest debt. Invest consistently. Diversify. Keep costs reasonable. Protect against major risks. Improve earning power. Understand taxes. Track net worth. Buy assets before luxuries. Be patient.

These ideas sound simple because the words are simple. The execution is not. It takes discipline to resist lifestyle inflation. It takes humility to buy a less impressive car. It takes patience to invest when results are not immediate. It takes courage to ignore friends, influencers, and social pressure. It takes maturity to choose invisible wealth over visible applause.

The middle class does not need to reject wealth. It needs to reject imitation without understanding. The goal is not to live small forever. The goal is to build a foundation strong enough that future choices are funded by assets, not anxiety.

Copying the rich can be expensive when you copy the spending first. Studying the wealthy can be valuable when you study the structure beneath the spending: ownership, liquidity, risk control, tax awareness, patience, and disciplined capital allocation.

The difference between those two approaches may determine whether rising income becomes lasting wealth or merely a more expensive lifestyle.

Final Thought: Wealth Is Built Below the Surface

Most of the habits that create wealth are not immediately visible. No one can see your savings rate from across a room. No one knows your net worth from your shoes. No one can tell whether your car is paid off by hearing the engine. No one sees the automatic investment that posts every month. No one sees the insurance policy that protects your family from catastrophe. No one sees the debt you chose not to take.

That invisibility is exactly why real wealth requires independence of mind. You must be willing to make decisions that may not impress anyone today so that your future self has more freedom tomorrow.

The middle class should stop copying habits that consume capital before capital has had a chance to grow. Stop copying the financed luxury car, the oversized house, the status purchase, the careless leverage, the celebrity investment, the concentrated bet, the lifestyle funded by credit, and the belief that looking successful is the same as being secure.

Copy the deeper habits instead. Own assets. Build cash reserves. Control debt. Invest with discipline. Diversify. Learn before risking. Protect against disaster. Increase income without surrendering every raise to lifestyle. Measure success by net worth, not applause.

Visible wealth can be rented. Real wealth must be built.