The Monopoly Mindset: How Peter Thiel Thinks Wealth Is Built

Peter Thiel’s philosophy of wealth begins with a rejection of ordinary competition.

Most people are taught that competition is healthy. Businesses compete for customers. Workers compete for jobs. Investors compete for returns. Students compete for grades. Founders compete for market share. The language of modern economic life often assumes that competition is the natural path to excellence.

Thiel argues that this belief can be financially dangerous. Competition may produce better outcomes for consumers, but it often destroys profits for producers. When many companies sell similar products to similar customers with similar business models, margins shrink. Prices fall. Advertising costs rise. Talent becomes expensive. Differentiation disappears. The customer benefits, but the business owner struggles.

In Thiel’s view, exceptional wealth is usually not created by competing harder in crowded markets. It is created by building something so unique, valuable, and difficult to copy that competition becomes less relevant.

This is the foundation of the philosophy he popularized in Zero to One: great fortunes are built by creating new value, not merely replicating what already exists. The richest companies do not simply do the same thing slightly better. They open new markets, develop proprietary technology, build networks that become more valuable with scale, and create advantages that allow them to earn profits for long periods.

Thiel’s career reflects this worldview. He co-founded PayPal, became the first outside investor in Facebook, co-founded Palantir Technologies, and helped build Founders Fund. His wealth philosophy comes from startup formation, venture capital, technology investing, and a deep belief that technological progress is the engine of long-term economic growth.

His framework is not a conventional personal finance plan. It does not begin with budgeting, emergency funds, index funds, or retirement accounts. It begins with a more ambitious question: what important company, technology, or market can you help create that does not yet exist?

That question is not suitable for everyone in the same way. Most startups fail. Venture investing is illiquid and risky. Concentrated ownership can create extraordinary wealth or painful losses. Many people are better served by diversified investing and steady wealth accumulation. But Thiel’s ideas matter because they explain how extreme wealth is often created at the frontier of innovation.

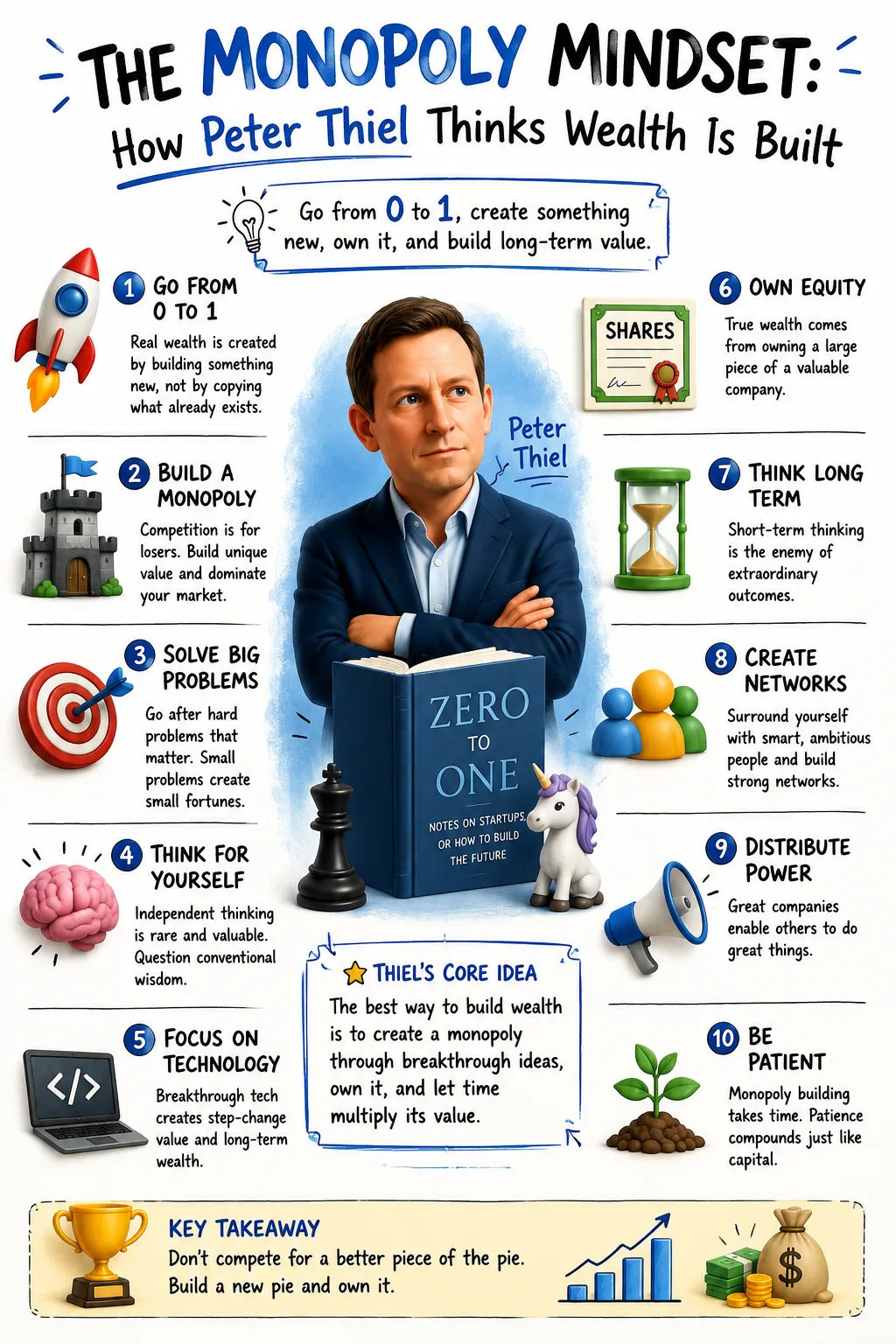

To understand how to get rich according to Peter Thiel, the key is to understand his operating principles: go from zero to one, avoid commoditized competition, build monopoly-like advantages, think independently, own equity, seek power-law outcomes, and work on difficult problems that can shape the future.

Zero to One: Creating What Did Not Exist Before

The central idea in Thiel’s philosophy is the distinction between horizontal progress and vertical progress.

Horizontal progress means copying or expanding what already works. If one company opens a successful restaurant concept and another person opens a similar restaurant in a different city, that is horizontal progress. If one factory produces a product and another factory produces more of the same product, that is horizontal progress. Thiel often describes this as going from one to many.

Vertical progress means creating something fundamentally new. It is the move from zero to one. It happens when a company invents a new technology, creates a new category, solves a problem in a way that was previously impossible, or opens a market that did not meaningfully exist before.

Thiel believes the greatest wealth is created through vertical progress because new value has less immediate competition. A company that creates a breakthrough product does not begin by fighting over an existing profit pool. It creates a new one.

This is why he places such importance on technology. Technology allows human beings to do more with less. It turns impossibility into possibility. It creates new productivity, new markets, new behaviors, and new business models. A software company can serve millions of users at relatively low marginal cost. A biotechnology breakthrough can create a treatment where none existed. A financial technology company can change how money moves. An aerospace company can expand the boundaries of transportation and defense.

Zero-to-one thinking asks founders and investors to look for non-obvious creation. What is missing from the world? What important problem remains unsolved? What technology is now possible that was impossible a decade ago? What does society need but has not yet built? What valuable truth is hidden because most people are looking elsewhere?

This approach differs sharply from trend-following entrepreneurship. Many founders look at what is already popular and try to build a slightly different version. A new delivery app. A new social network. A new productivity tool. A new marketplace. Some of these businesses may succeed, but Thiel would ask whether they are truly creating new value or merely entering a crowded field.

His philosophy rewards originality, but not originality for its own sake. A zero-to-one company must solve a real problem. Novelty without demand is not innovation; it is invention without a market. The goal is to build something both new and valuable.

This is a demanding standard. It requires insight, technical ability, timing, courage, and often years of uncertainty. But when it works, the outcome can be extraordinary. A company that creates a new category may define the rules before others arrive. It may shape customer expectations, attract talent, build infrastructure, accumulate data, and become the default choice in a market that later appears obvious.

Thiel’s wealth philosophy therefore begins with creation. Not consumption. Not imitation. Not optimization around the edges. Creation.

Why Thiel Believes Competition Can Be a Trap

One of Thiel’s most provocative arguments is that competition is overrated.

This does not mean competition is bad for society. Competitive markets can lower prices, improve service, and force companies to become more efficient. But for the business owner, intense competition often means weak profits. If customers can easily switch among similar providers, the seller has little pricing power. If competitors can copy the product quickly, advantages disappear. If everyone is fighting for the same customer, marketing costs rise and margins fall.

Thiel’s point is that capitalism and competition are not the same thing. Capitalism, in the sense of wealth creation, depends on accumulating profits. Competition tends to erode profits. The more perfectly competitive a market becomes, the harder it is for any participant to earn exceptional returns.

Consider a commodity business. If many sellers offer nearly identical products, the customer chooses primarily on price. The producer with the lowest cost may survive, but most competitors struggle to earn high margins. The business may work hard and still create little wealth for owners.

Now compare that with a company that offers a product no one else can easily match. It may have proprietary technology, a strong network, a trusted brand, regulatory advantages, unique data, high switching costs, or economies of scale. Customers do not see it as interchangeable. The company can earn stronger margins because it provides differentiated value.

Thiel wants founders to escape the commodity trap. Instead of asking how to win a crowded race, he asks how to find or create a race that others are not yet running.

This is difficult because competition feels validating. If many companies are entering a market, it seems to prove demand. Investors may feel safer funding a company in a hot category. Founders may feel reassured when competitors exist because the market is visible. But a crowded market can also signal that profits will be competed away.

By contrast, a truly original idea may look strange at first. It may lack obvious comparisons. Customers may need education. Investors may misunderstand it. Analysts may doubt it. The founder may feel lonely. Yet if the insight is right, the lack of competition can become the opportunity.

Thiel’s view does not mean founders should ignore competitors. It means they should avoid defining success as beating similar companies at the same game. The better strategy is to build something with a structural advantage.

Competition asks, “How can we be better than them?” Monopoly thinking asks, “How can we become the only company that does this particular thing in this particular way for this particular market?”

Monopoly in Thiel’s Sense

When Thiel praises monopoly, he is not necessarily referring to illegal or abusive market power. He is using the term in a strategic sense: a company with a durable competitive advantage that allows it to earn above-average profits over time.

In this usage, a monopoly is not simply a large company. It is a company that is meaningfully different from competitors and protected by advantages that are hard to replicate.

Thiel identifies several sources of monopoly-like strength. The first is proprietary technology. If a company’s technology is significantly better than alternatives, it can create a powerful advantage. The improvement must be substantial, not marginal. A product that is 10 percent better may not be enough to change behavior. A product that is dramatically better can create a new market.

The second source is network effects. A product has network effects when it becomes more valuable as more people use it. Social networks, marketplaces, payment systems, communication platforms, and developer ecosystems can benefit from this dynamic. Once a network becomes dominant, new competitors face a difficult challenge because users want to be where other users already are.

The third source is economies of scale. Some businesses become more efficient as they grow. Software is a classic example because the cost of serving an additional user may be low once the product is built. Large-scale companies can spread fixed costs across a bigger customer base, invest more in infrastructure, and lower unit economics in ways smaller competitors cannot match.

The fourth source is brand. A strong brand can create trust, reduce customer uncertainty, and support pricing power. But Thiel is skeptical of brand without substance. Brand is strongest when it reflects a real underlying advantage.

The fifth source is switching costs. If customers face significant inconvenience, expense, data loss, retraining, integration challenges, or operational risk when changing providers, they are less likely to leave. Enterprise software companies often benefit from this once their systems become embedded in customer workflows.

A strong company may combine several of these advantages. A software platform may have proprietary technology, network effects, scale, brand recognition, and switching costs. That combination can produce durable profitability.

Thiel’s monopoly concept is important because it shifts the investor’s attention from growth alone to defensibility. A company can grow quickly and still be fragile if competitors can copy it easily. A defensible company can grow more slowly at first but become more valuable over time because its profits are protected.

For founders, the lesson is to build protection into the business model. For investors, the lesson is to look for advantages that can persist.

Start Small, Dominate, Then Expand

Thiel advises founders to begin with a small market they can dominate. This may sound counterintuitive because entrepreneurs often want to describe enormous markets. Large markets attract attention. They sound ambitious. They make financial projections look exciting.

But large markets also attract competition. A startup entering a huge market without a clear wedge may be crushed by incumbents or lost among rivals. Thiel prefers a narrow starting point where the company can become the clear leader.

A small market allows focus. The company can understand a specific customer deeply, tailor the product, build loyalty, and establish dominance before expanding. Once it controls the initial niche, it can move into adjacent markets from a position of strength.

This strategy reflects how many successful technology companies have grown. They begin with a concentrated use case, community, geography, customer type, or workflow. They solve one problem extremely well. Then they expand.

The discipline is choosing the right small market. It must be small enough to dominate but important enough to serve as a foundation. A market that is too small may never support a significant company. A market that is too broad may prevent early dominance. The founder’s job is to find the narrow opening that can lead to a much larger opportunity.

This approach also helps with product development. A company serving everyone often serves no one deeply. A company serving a specific group can build sharper features, clearer messaging, and stronger customer love. Early users become advocates. Their feedback improves the product. Their concentration may produce network effects faster.

Dominating a small market also creates proof. Investors, employees, partners, and customers can see traction. The company is not merely claiming a large theoretical opportunity; it is winning a real segment.

From there, expansion must be logical. The next market should be adjacent enough that the company’s capabilities transfer. A business that dominates one niche but expands randomly may lose focus. Thiel’s strategy is not small thinking. It is sequenced ambition.

Start where victory is possible. Build strength. Then widen the circle.

The Contrarian Question

Thiel is famous for asking: “What important truth do very few people agree with you on?”

This question reveals the heart of his independent-thinking philosophy. Exceptional wealth often comes from seeing something true before it becomes consensus. If everyone already agrees that an opportunity is valuable, the price may already reflect it. If everyone already understands a market, competition may already be intense. If everyone already sees the future clearly, the easy gains may be gone.

Contrarian thinking does not mean disagreeing for attention. It does not mean being provocative, cynical, or reflexively opposed to mainstream views. A contrarian truth must be both unpopular and correct. That is a much higher standard.

The question forces intellectual discipline. What do you believe that others reject? Why do they reject it? What evidence do you have? What would prove you wrong? Are you seeing something real, or are you merely attracted to being different?

In entrepreneurship, a contrarian truth might be that a market dismissed as too small is actually the beginning of a much larger shift. It might be that customers are dissatisfied with a solution that outsiders assume is good enough. It might be that a technology is improving faster than incumbents realize. It might be that regulation, culture, or cost curves are about to change.

In investing, contrarian thinking means identifying mispriced opportunities. But this is difficult because markets often appear wrong to people who simply do not understand them. A falling stock is not necessarily cheap. A hated industry is not necessarily attractive. A popular company is not necessarily overvalued. The investor must distinguish between genuine insight and personal opinion.

Thiel’s question is especially useful because it connects truth with importance. Many obscure beliefs do not matter financially. The goal is not to find any unusual opinion. The goal is to identify a hidden truth that can support a valuable business or investment.

Independent thinking also requires courage. A founder pursuing a non-consensus idea may face skepticism from investors, friends, employees, customers, and the media. An investor making a concentrated bet may look foolish before looking right. A technologist working on a difficult problem may spend years without recognition.

But the reward for being right before consensus can be extraordinary. When the world eventually agrees, the company or investor who acted early may already own the advantage.

Equity Over Wages

Thiel’s wealth philosophy strongly favors ownership over wages. Salaries provide income. Equity provides upside.

An employee who earns a wage is paid for labor. That income may be high, stable, and valuable. But the upside is usually limited. The employee may receive raises, bonuses, or promotions, yet most of the enterprise value created by a successful company accrues to owners.

Founders, early employees with meaningful equity, and investors participate differently. If the company becomes much more valuable, their ownership can appreciate dramatically. This is one reason technology startups have produced substantial wealth for founders and early shareholders.

Thiel’s own career demonstrates the power of equity. PayPal, Facebook, Palantir, and venture investments created wealth not through wages but through ownership stakes in companies whose value increased substantially.

This principle applies beyond Silicon Valley, though the magnitude varies. A small business owner builds equity in a company. A real estate investor owns property equity. A shareholder owns part of a public company. An inventor may own intellectual property. A creator may own a media asset or product line. A professional may accept equity in a startup rather than only cash compensation.

The central lesson is that wealth usually belongs to those who own productive assets. Labor can generate income, but ownership captures compounding value.

However, equity is not automatically superior to wages. Startup equity can become worthless. Private company shares may be illiquid for years. Employees may accept lower salaries for options that never pay off. Founders may own large percentages of companies that fail. Public stocks can decline. Intellectual property may never produce income.

The quality of the equity matters. Ownership in a weak business is not wealth; it is risk. Ownership in a strong, growing, defensible business can be transformative.

For individuals, the practical question is how to increase ownership intelligently. That may mean founding a company, joining an early-stage business with strong prospects, buying public equities, investing in private businesses, building intellectual property, or acquiring assets. The right path depends on skill, risk tolerance, capital, time horizon, and access.

Thiel’s philosophy does not say wages are useless. Wages can fund survival and investment. But wages alone rarely create extreme wealth unless they are converted into ownership. The wealth builder uses income as a bridge to equity.

The Power Law: Why a Few Outcomes Matter So Much

Thiel’s venture-capital worldview is shaped by the power law. In many domains, outcomes are not evenly distributed. A small number of results account for a disproportionate share of the total.

In venture capital, this means a few investments often generate most of the returns. Many startups fail. Some return modest amounts. A small number become enormous winners. The best investment in a venture portfolio may outperform all the others combined.

This has major implications for how Thiel thinks about wealth. If returns follow a power law, then investors and founders should not treat opportunities as interchangeable. They should search for exceptional upside. A company that can become one of the defining businesses in a market is fundamentally different from a company that may produce a modest return.

This contrasts with traditional diversification logic. In public market investing, diversification can reduce company-specific risk and produce broad exposure to economic growth. In venture capital, excessive diversification into mediocre companies may dilute attention and capital away from the few opportunities that matter most.

Thiel’s power-law thinking encourages concentration, but concentration increases risk. If the chosen company fails, losses can be severe. This is why venture investing requires a different mindset from ordinary saving. The investor must be prepared for illiquidity, failure, long holding periods, and extreme uncertainty.

For founders, power-law thinking means choosing an idea with the potential to become very large. A startup is too difficult and risky to justify if the best-case outcome is small. Thiel would argue that founders should work on ideas with asymmetric upside: limited enough to begin, but large enough to matter if successful.

For employees, the power law suggests that joining the right company early can matter more than receiving small equity stakes in many ordinary companies. But identifying the right company is hard. Many startups sound promising. Few become exceptional.

For individual investors, the lesson should be applied carefully. Most people should not imitate venture capital concentration with money they cannot afford to lose. But they can learn from the principle. Not all opportunities deserve equal effort. Not all skills have equal upside. Not all companies have equal compounding potential. Not all markets are worth entering.

Power-law thinking asks: where can a small number of excellent decisions produce most of the result?

Technology as the Engine of Wealth Creation

Thiel believes technological progress is central to long-term prosperity. Without technology, economic growth becomes limited. Societies can redistribute wealth, optimize processes, or globalize production, but genuine progress requires new capabilities.

This belief explains why he emphasizes industries such as software, artificial intelligence, biotechnology, aerospace, financial technology, cybersecurity, defense technology, and other deep technology sectors. These fields have the potential to create products and systems that change what humanity can do.

Technology businesses can be powerful wealth engines because they often scale differently from traditional businesses. A software company may build a product once and sell it globally. A platform may become more valuable as more users join. A data advantage may improve with scale. A breakthrough technology may open an entirely new market.

Low marginal cost is especially important. If the cost of serving each additional customer is low, revenue growth can eventually produce high margins. This is one reason successful software companies can become extraordinarily profitable.

But technology alone is not enough. Many technically impressive products fail commercially. The business must solve a real problem, reach customers, create a defensible position, and build a viable economic model. Thiel’s framework combines technology with monopoly strategy. The question is not simply, “Is this innovative?” It is, “Can this innovation become the foundation of a durable, valuable company?”

Artificial intelligence is a useful example. AI may create enormous opportunities, but many AI businesses may become commoditized if they lack proprietary data, distribution, workflow integration, brand, or technical differentiation. A company using AI is not automatically a monopoly. The advantage must be specific and defensible.

Biotechnology offers another example. A breakthrough therapy can create immense value, but development risk, regulation, clinical trials, capital intensity, and scientific uncertainty are significant. The upside can be large, but so can the failure rate.

Thiel’s technology optimism is therefore not a call to chase every trend. It is a call to work on hard problems where success would matter greatly and where a company can build lasting advantage.

Long-Term Thinking and Durable Value

Thiel encourages founders and investors to think in decades. A great company is not merely one that grows quickly for a few quarters. It is one that can remain valuable far into the future.

This long-term orientation changes how a business is evaluated. Short-term revenue growth may be exciting, but the deeper question is whether profits can endure. What will the company look like ten years from now? Will customers still need it? Will competitors copy it? Will technology make it obsolete? Will regulation restrict it? Will the market expand? Will its advantages strengthen or decay?

Thiel argues that much of a company’s value lies in its future cash flows. If a business cannot plausibly generate profits years into the future, its present value is limited. This is particularly important for startups, where current profits may be small or nonexistent. The valuation depends on the possibility of future dominance.

Long-term thinking also affects strategy. A founder building for durability may invest more in technology, culture, hiring, product quality, customer trust, and defensibility. A founder chasing short-term metrics may over-optimize for growth that cannot last.

Durable value requires patience. Monopoly-like advantages are rarely built overnight. Network effects take time. Proprietary technology takes research and development. Brand trust accumulates slowly. Enterprise relationships require credibility. Regulatory expertise develops over years.

This is one reason Thiel is skeptical of purely incremental companies. A business that depends on being slightly better today may be vulnerable tomorrow. A business that builds structural advantages can become stronger with time.

Long-term thinking does not mean ignoring the present. Startups must survive before they can dominate. Cash, product-market fit, customer adoption, and execution matter immediately. But short-term action should serve a long-term thesis.

The wealth builder asks not only, “Can this make money now?” but “Can this become more valuable over time because its advantages compound?”

Building for the Future

Thiel’s philosophy is deeply connected to the idea of building the future. He has often argued that society needs ambitious technological progress rather than mere financial engineering, globalization, or incremental improvement.

This matters for wealth because the largest opportunities often arise when the future is genuinely different from the present. If the world of tomorrow looks almost exactly like today, then most businesses will compete within existing categories. If new technologies reshape industries, the companies that create or control those technologies may become extremely valuable.

Building for the future requires imagination, but also specificity. Vague optimism is not enough. A founder must have a definite view of what should exist and how to build it. Thiel prefers definite optimism over indefinite optimism. The definite optimist believes the future can be better and has a plan to make it so.

This is a demanding mindset because it rejects passive trend participation. It asks founders to take responsibility for a specific future. Not “AI will change everything,” but “this particular AI system will solve this particular problem for this particular customer in a way competitors cannot easily copy.” Not “space will be important,” but “this technology can reduce launch costs, improve satellite capability, or enable a new market.” Not “healthcare is broken,” but “this product can improve diagnosis, treatment, workflow, or cost in a defensible way.”

The future rewards builders, not spectators. Thiel’s philosophy places the founder, engineer, scientist, investor, and operator at the center of progress. These people do not merely predict change. They create it.

For individuals outside startups, the same principle can be applied to career strategy. Work in fields where the future is expanding. Build skills tied to technological change. Develop judgment in industries where new value is being created. Seek ownership where possible. Avoid spending an entire career in markets being commoditized or automated unless you have a clear advantage.

Building for the future is not only about founding a company. It is about positioning one’s talent and capital where important change is happening.

How Thiel’s Ideas Apply to Individual Wealth Builders

Most people will not found the next PayPal, Facebook, or Palantir. That does not mean Thiel’s ideas are irrelevant. They can be translated into practical principles for careers, business ownership, and investing.

The first principle is to seek ownership. Even if a person remains employed, they can use income to acquire equity in public companies, private businesses, real estate, or their own ventures. Wealth comes from owning assets that appreciate or produce cash flow.

The second principle is to develop rare skills. In labor markets, competition is intense when many people can do the same work. A professional who develops scarce expertise, especially in a growing field, creates more pricing power. This is a personal version of monopoly strategy. The goal is not to become interchangeable.

The third principle is to choose markets carefully. A talented person in a declining or commoditized field may struggle more than a less talented person in an expanding market with strong demand. Industry selection matters. Thiel’s framework encourages people to ask where the future is being built and where their contribution can be valuable.

The fourth principle is to think independently. Do not choose a career, investment, or business simply because it is popular. Popularity can signal opportunity, but it can also signal crowding. Ask what others are missing. Ask whether the consensus is too optimistic or too pessimistic. Ask where your knowledge gives you an edge.

The fifth principle is to look for defensibility. If starting a business, ask what will prevent competitors from copying you. If investing, ask whether the company has durable advantages. If building a career, ask what makes your contribution hard to replace.

The sixth principle is to understand power laws. A few decisions may drive most of your financial outcome: the industry you enter, the company you join, the business you start, the equity you hold, the skill you master, the investment you make, the partner you choose. Treat these decisions with the seriousness they deserve.

The seventh principle is to respect risk. Thiel’s philosophy can inspire boldness, but boldness without risk management becomes gambling. Concentrated bets should be made only when the downside is survivable and the insight is strong. For most households, a stable financial base remains essential.

Where Thiel’s Philosophy Can Go Wrong

Thiel’s ideas are powerful, but they can be misapplied.

The first danger is romanticizing startups. Building a startup is not automatically a path to wealth. Most startups fail, and many founders earn less than they could have earned in employment for years. A company must have a real market, strong execution, capital discipline, and a defensible advantage. Ambition alone is not enough.

The second danger is misunderstanding monopoly. Some founders claim they have no competition because they define the market too narrowly or ignore substitutes. Customers always have alternatives, even if the alternative is doing nothing. A monopoly-like position must be earned through real advantage, not asserted in a pitch deck.

The third danger is contrarianism without truth. Being different is not the same as being right. Many unpopular ideas are unpopular because they are wrong. Independent thinking must be paired with evidence, humility, and willingness to revise.

The fourth danger is overconcentration. Thiel’s power-law worldview can justify large bets, but most individuals cannot absorb venture-style losses. Concentration can build wealth when correct and destroy it when wrong. People must distinguish between money allocated for high-risk opportunity and money needed for financial security.

The fifth danger is ignoring ethics and regulation. Companies that become dominant may attract scrutiny. Market power can create responsibilities. Data, privacy, labor practices, competition law, national security, and social impact matter. A business built for the future must consider the society it is helping create.

The sixth danger is dismissing ordinary wealth building. Not everyone needs to build a monopoly to become financially independent. Diversified investing, disciplined saving, career growth, entrepreneurship, and real estate can all build wealth. Thiel’s philosophy is most relevant to ambitious founders, venture investors, and people seeking asymmetric upside, but it should not make steady compounding seem inferior for those with different goals.

The strongest application of Thiel’s thinking combines ambition with discipline. Build something new, but validate demand. Seek monopoly-like advantages, but understand customers. Think independently, but test beliefs. Own equity, but manage risk. Pursue power-law upside, but protect the base.

Comparing Thiel With Traditional Financial Advice

Traditional personal finance often emphasizes diversification, steady saving, broad-market investing, debt control, and long-term compounding. Thiel’s philosophy emphasizes concentration, startups, technological innovation, monopoly strategy, and non-consensus thinking.

These approaches can appear contradictory, but they address different games.

Traditional financial advice is designed for resilience and broad applicability. It helps households avoid ruin, build retirement assets, and participate in economic growth without needing to identify exceptional companies early. It is useful because most people do not have access to venture deals, startup equity, or proprietary insight.

Thiel’s philosophy is designed for exceptional wealth creation. It explains how outlier companies and investors generate extraordinary returns. It is less diversified, more uncertain, and more dependent on rare insight and execution.

A person can use both. They can maintain diversified investments while building a startup. They can work in technology and own public equities. They can keep emergency reserves while taking calculated entrepreneurial risk. They can invest most assets prudently while allocating a smaller portion to asymmetric opportunities.

The key is not to confuse the safety portfolio with the ambition portfolio. Money needed for stability should not be treated like venture capital. Money allocated to high-upside bets should be understood as risky and illiquid.

Thiel’s contribution is not that everyone should abandon diversification. It is that diversification alone rarely creates extreme wealth. Extreme wealth usually requires concentrated ownership in something that becomes far more valuable. The challenge is that concentrated ownership is easy to admire after success and hard to survive before success.

The Practical Path: Building a Thiel-Inspired Wealth Strategy

A practical Thiel-inspired strategy begins with asking where you have or can build an edge. This may be technical expertise, industry knowledge, customer insight, distribution capability, capital access, operational skill, or a unique network. Without an edge, bold bets are usually speculation.

Next, identify a market where change is possible. Look for technological shifts, regulatory changes, customer dissatisfaction, cost declines, new infrastructure, or cultural movement. A good opportunity often appears where the old solution is accepted as normal despite being inefficient, expensive, slow, or inadequate.

Then search for a narrow starting point. Who is the first customer? What small market can be served better than anyone else? What segment is overlooked by incumbents? What problem is painful enough that customers will adopt a new solution?

After that, define the defensibility. What will make the business hard to copy if it works? Proprietary technology? Data? Network effects? Scale? Brand? Distribution? Switching costs? Regulatory expertise? Operational excellence? A startup without a path to defensibility may become a feature, not a company.

Then decide how to gain ownership. Found the company, join early with equity, invest where legally and financially appropriate, build intellectual property, or acquire ownership in public companies with durable advantages. The form of ownership matters less than the quality of the asset.

Finally, balance ambition with survival. Keep enough liquidity to avoid forced decisions. Avoid risking essential capital on uncertain outcomes. Learn continuously. Seek disagreement from intelligent people. Update beliefs when evidence changes.

This approach does not guarantee wealth. Nothing in entrepreneurship or investing does. But it creates a framework for pursuing high-upside opportunities with more discipline than simple optimism.

The Real Meaning of Getting Rich According to Peter Thiel

Peter Thiel’s philosophy of getting rich is not about working slightly harder than competitors in a crowded field. It is about escaping the crowd altogether.

He asks wealth builders to search for hidden truths, build new things, own equity, create defensible businesses, and think in terms of power-law outcomes. He wants founders to stop copying and start inventing. He wants investors to understand that a few exceptional companies may matter more than many average ones. He wants ambitious people to work on the future rather than compete over the present.

The monopoly mindset is not about avoiding effort. It is about directing effort toward a position where effort can compound. A company with no defensibility must keep fighting every day for every dollar. A company with structural advantages can turn innovation, scale, network effects, and brand into enduring value.

For the individual wealth builder, the lesson is clear. Do not become interchangeable. Do not assume the most crowded opportunity is the best one. Do not confuse consensus with truth. Do not rely only on wages if ownership is available. Do not pursue novelty without value. Do not take concentrated risk without understanding the downside.

Thiel’s philosophy is demanding because it offers no easy formula. It requires independent thought, courage, patience, technical or strategic insight, and a willingness to be misunderstood. It also requires humility because many bold ideas fail.

But the central insight is powerful: extraordinary wealth often comes from creating or owning something the world eventually cannot ignore.

That may be a company, a technology, a platform, a patent, a network, a brand, or a body of scarce expertise. The form can vary. The principle remains the same. Build or own something rare, valuable, and difficult to copy.

According to Peter Thiel, getting rich is not about winning the competition. It is about creating the kind of value that makes competition less important.