The Ownership Divide: How Assets, Liabilities, and Compounding Shape Wealth

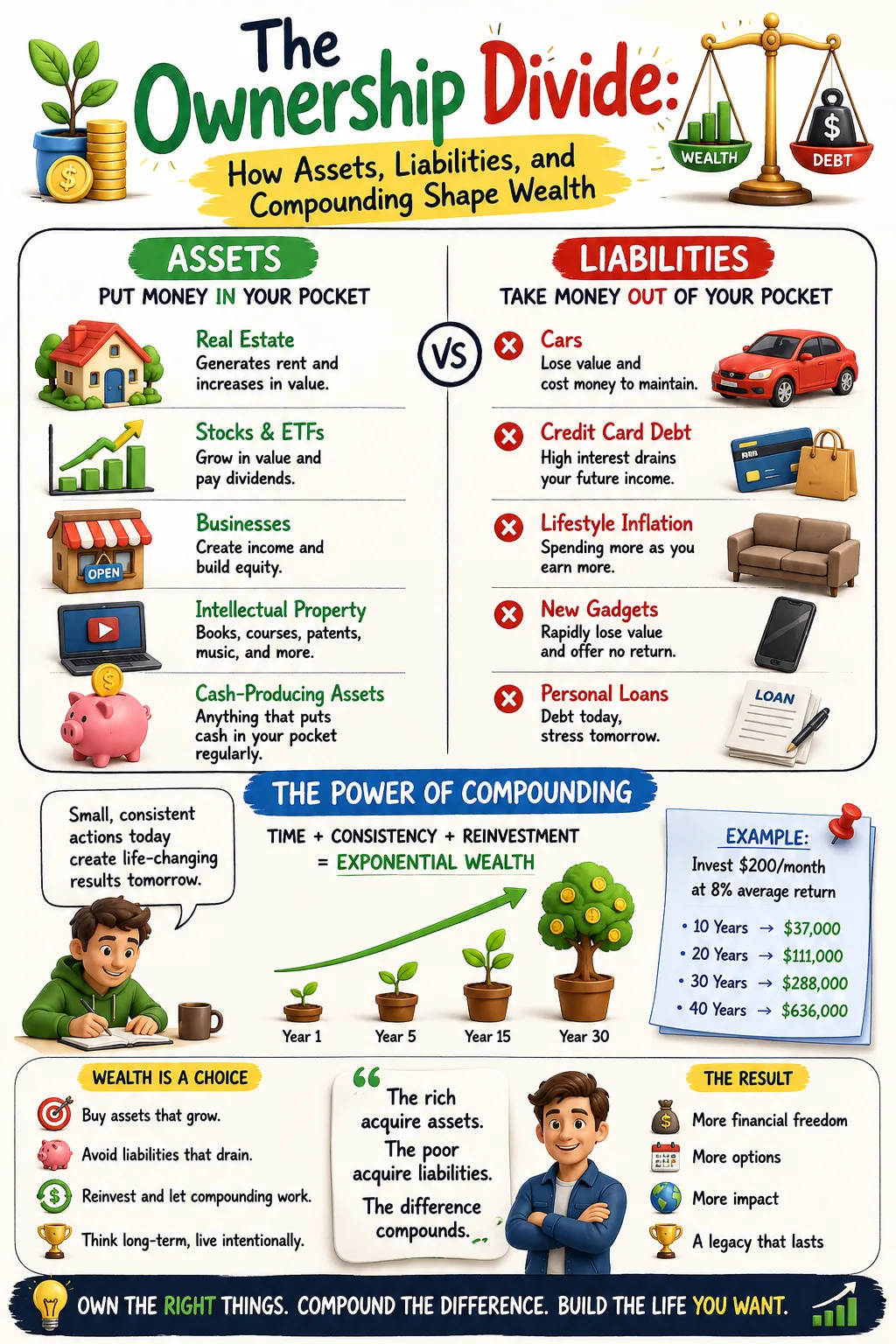

Few personal finance statements are as memorable as the claim that rich people buy assets, poor people buy liabilities, and the difference compounds.

It is sharp. It is simple. It sounds like a complete explanation of wealth. It suggests that the financial world can be divided into two groups: those who buy things that pay them and those who buy things that cost them. Over time, the first group becomes freer while the second becomes more trapped.

There is a powerful lesson inside that statement. Wealth is often built by acquiring productive assets: investments, businesses, real estate, intellectual property, and other forms of ownership that can generate income or appreciate over time. Financial fragility is often worsened by liabilities: debts, payment obligations, and consumption habits that pull future income backward into the past. The difference does compound. Assets can produce returns. Debt can produce interest costs. Reinvested gains can multiply. Repeated borrowing can snowball.

But the statement is also incomplete. It can become unfair when it turns structural financial difficulty into a moral judgment. Many lower-income households are not buying luxury liabilities; they are paying for rent, food, childcare, transportation, healthcare, utilities, and survival. Many people do not lack wealth because they misunderstand assets. They lack wealth because income is too low, expenses are unavoidable, access to capital is limited, wages are unstable, emergencies are frequent, or one medical, family, or employment shock absorbs years of progress.

The better lesson is not that rich people are virtuous and poor people are careless. The better lesson is this: people who consistently direct surplus income toward productive assets instead of unnecessary consumption are generally more likely to build wealth over time.

That version is less provocative, but far more useful. It keeps the core financial principle while respecting reality. Wealth building depends on savings rate, income growth, investment returns, asset ownership, debt management, time, discipline, and risk protection. It also depends on conditions that are not evenly distributed: education, family support, health, geography, employment opportunity, tax systems, housing affordability, and access to financial tools.

Assets matter. Liabilities matter. But context matters too.

What an Asset Really Is

An asset is something with economic value. In wealth-building terms, the most important assets are those that can generate income, appreciate over time, preserve purchasing power, or improve future financial security.

Examples include diversified stock investments, bonds, retirement accounts, rental real estate, profitable businesses, certificates of deposit, cash reserves, intellectual property, royalties, ownership stakes, and certain forms of land or productive equipment. Some assets produce current income. Some primarily grow in value. Some provide liquidity. Some protect against emergencies. Some create business or career opportunity.

The key is that an asset strengthens the financial position over time.

A dividend-paying stock may distribute income. A broad stock fund may appreciate as companies grow. A bond may pay interest. A rental property may provide rent and potential appreciation. A business may generate profit and eventually sale value. A patent, book, software product, or licensed design may produce royalties. A cash reserve may not create high returns, but it prevents small emergencies from becoming high-interest debt.

Assets are not automatically safe. Stocks can decline. Bonds can lose value. Businesses can fail. Properties can sit vacant. Intellectual property may not sell. Cash can lose purchasing power to inflation. An asset is not good merely because it is called an asset. Its quality depends on price, risk, liquidity, return potential, cash flow, management, taxes, and suitability.

This is one of the first marks of financial maturity: understanding that asset ownership is essential, but asset selection still requires judgment.

What a Liability Really Is

A liability is a financial obligation. It is money owed, usually requiring future payments. Credit card balances, personal loans, auto loans, mortgages, student loans, business loans, unpaid taxes, and other debts are liabilities.

Liabilities are not all the same. Some finance consumption. Some finance assets. Some are expensive. Some are manageable. Some create opportunity. Some destroy flexibility.

A credit card balance used to finance lifestyle spending at high interest is usually destructive. It turns past consumption into a claim on future income. A car loan on an overpriced vehicle may reduce monthly flexibility for years while the vehicle declines in value. A personal loan used for nonessential spending can create pressure without creating future benefit.

But not every liability is bad. A mortgage on a reasonably priced home can help a household secure shelter and build equity, although it still carries risk and cost. Student loans may increase lifetime earning power if the education is useful, affordable, and connected to realistic income prospects. A business loan may help expand profitable operations if cash flow can support repayment. Debt used carefully to acquire productive assets can support wealth building.

The question is not simply, “Is this debt?” The question is, “What does this debt make possible, what does it cost, and what risks does it create?”

A liability becomes dangerous when it finances consumption that does not improve future income, asset ownership, or essential stability. It becomes especially dangerous when the interest rate is high, the repayment period is long, and the borrower has little margin for emergencies.

The Compounding Difference

The most important word in the statement is not rich, poor, assets, or liabilities. It is compounds.

Compounding is what turns small differences into large outcomes over time. When an investment earns a return and that return is reinvested, future returns are earned on a larger base. The process can begin slowly, almost invisibly. But given enough time, reinvested returns can become more powerful than the original contributions.

Debt can compound too, but in the opposite direction. Interest charges increase what is owed. Missed payments can trigger fees. High-interest balances can grow faster than the borrower can reduce them. A household paying large interest costs has less surplus available for saving and investing. The debt does not merely cost money today; it blocks the future wealth that money could have built.

This is the ownership divide. One household directs surplus income into assets that may compound upward. Another directs future income toward payments on past consumption. At first, the difference may be hard to see. Both households may have similar incomes. Both may live in similar neighborhoods. Both may drive cars, take vacations, and appear financially normal.

Years later, the difference becomes visible. The asset buyer owns investments, equity, cash reserves, business interests, or property. The liability buyer owns obligations. One balance sheet has been quietly strengthened by time. The other has been quietly drained by it.

Compounding rewards direction. Money moving into productive assets can compound for the owner. Money moving into high-cost debt can compound against the borrower.

Why the “Rich People Buy Assets” Framing Is Partly True

High-net-worth households often own a larger share of productive assets. Their wealth may be held in businesses, equities, real estate, private investments, bonds, funds, intellectual property, or other forms of ownership. This is not accidental. Large fortunes are rarely built from wages alone. They are usually built from ownership.

Ownership allows people to participate in value created by assets. A business owner may benefit from profits and appreciation in enterprise value. A shareholder may benefit as companies grow. A landlord may receive rent and property appreciation. A founder may own equity that becomes valuable as the company scales. An investor may own a diversified portfolio that compounds over decades.

Income can make ownership easier. A high-income person who lives below their means can buy assets faster. A business owner with strong profits can reinvest. A family with inherited capital can begin the compounding process earlier. A professional with equity compensation can benefit from ownership alongside salary.

Over time, assets can begin producing income themselves. Dividends, interest, rents, royalties, distributions, and business profits may supplement labor income. Eventually, for some households, asset income can reduce dependence on work. That is the path toward financial independence.

This is why the asset lesson matters. A person who wants wealth must eventually own something that grows or pays. Income alone is not enough if all of it is consumed.

Why the “Poor People Buy Liabilities” Framing Is Misleading

The second half of the phrase is weaker because it generalizes too broadly. It implies that poverty is mainly the result of buying the wrong things. Sometimes poor financial decisions do contribute to hardship. High-interest debt, status spending, gambling, unnecessary car loans, and lifestyle inflation can damage households at any income level.

But many lower-income households do not have enough surplus to buy assets consistently. Their money goes to essentials. Rent may consume a large share of income. Transportation may be necessary for work. Childcare may be unavoidable. Healthcare costs may be unpredictable. Food, utilities, school expenses, family obligations, and debt from prior emergencies may leave little room for investing.

A household cannot invest money it does not have. Advice about buying assets becomes incomplete if it ignores the first requirement: a positive gap between income and expenses.

There is also the issue of access. Higher-income households often have better access to employer retirement plans, matching contributions, affordable credit, tax advisers, stable housing, financial education, professional networks, and family support. Lower-income households may face higher borrowing costs, unstable schedules, limited benefits, predatory financial products, and fewer safety nets.

None of this means financial behavior is irrelevant. Behavior matters enormously. But behavior operates inside constraints. A fair financial education framework teaches personal agency without pretending that every household starts from the same position.

The goal is not to shame people for lacking assets. The goal is to help people move, wherever possible, from consumption pressure toward ownership capacity.

The First Asset Is Often a Gap

Before a person can buy investments, property, or businesses, they need a surplus. The first asset is often not a stock or a rental unit. It is the gap between income and expenses.

This gap is what makes every other wealth decision possible. It funds emergency savings. It pays down debt. It buys investments. It covers insurance. It supports education. It creates options.

The gap can be created in two ways: increase income or reduce expenses. Both matter. Expense control is powerful because it can produce immediate results. Cutting unused subscriptions, reducing impulse purchases, refinancing expensive debt where appropriate, cooking more meals at home, or avoiding unnecessary upgrades can free cash flow.

But expenses can only be cut so far. Income growth is often essential. Skills, education, certifications, negotiation, job changes, entrepreneurship, freelance work, sales ability, leadership, and specialization can all increase earning power. For many people, the strongest wealth-building move is not finding a secret investment. It is increasing income while preventing lifestyle inflation.

A household with no gap is financially trapped. A household with a small gap has a beginning. A household with a growing gap has momentum.

The Second Asset Is Liquidity

Cash reserves are often underrated because they do not look like exciting assets. But liquidity is one of the most important assets a household can own. An emergency fund prevents ordinary problems from becoming debt spirals.

Without cash, a car repair may become a credit card balance. A medical bill may become a personal loan. A job loss may force early retirement withdrawals. A home repair may lead to borrowing at unfavorable terms. A small emergency becomes expensive because there is no buffer.

Cash does not compound like equities over the long term, but it protects compounding from interruption. It prevents forced selling. It gives a person time to make decisions. It reduces reliance on lenders. It creates psychological stability.

For many households, building emergency savings is the first practical step toward the asset mindset. It may not feel like wealth, but it is the beginning of control.

The Third Asset Is Earning Power

Human capital is one of the largest assets most people possess. Skills, education, credentials, reputation, experience, communication, and professional networks can increase income over a lifetime.

A person who improves earning power can create more surplus. More surplus can buy more assets. More assets can produce more income. This is how human capital becomes financial capital.

Investing in skills may include formal education, trade training, technical certifications, sales training, leadership development, writing ability, financial literacy, coding, data analysis, design, project management, healthcare expertise, entrepreneurship, or any capability that solves valuable problems. The best skill investments are not always the most expensive. They are the ones that increase a person’s ability to earn, adapt, and create value.

For someone with limited income, the most important asset purchase may not be a stock. It may be a skill that raises income. For someone with strong income but poor habits, the most important move may be directing that income into investments. For someone with assets but no protection, the priority may be insurance and estate planning.

The asset mindset should fit the stage of life.

Good Debt, Bad Debt, and Dangerous Debt

The asset-versus-liability conversation often becomes too simplistic about debt. Debt is not automatically evil. It is a tool. But like any powerful tool, it can help build or help destroy.

Good debt is sometimes described as debt used to acquire something that increases future value. A mortgage may help buy a home. A student loan may help fund education. A business loan may help purchase equipment or inventory. But even good debt can become bad if the price is too high, the income assumptions are wrong, or the payments are unaffordable.

Bad debt usually funds consumption without creating future economic benefit. Credit card debt for lifestyle spending, high-interest personal loans, expensive auto loans, and buy-now-pay-later habits can weaken wealth building. The borrower receives the benefit immediately but pays for it over time, often with interest.

Dangerous debt is debt that can cause financial ruin under stress. It may involve variable rates, high leverage, weak cash flow, poor collateral, uncertain income, or assets that can decline sharply. Borrowing to invest can be especially dangerous when the investor assumes prices will only rise.

The debt test is practical. Does this debt help acquire or protect something valuable? Is the interest rate reasonable? Can payments be made if income falls? Is there a clear repayment plan? What happens if the asset declines in value? Does the debt increase freedom over time, or does it reduce it?

Debt should not be judged only by what it buys. It should be judged by what it does to the future.

When a Home Is Both Asset and Liability

A primary residence is one of the most debated examples in personal finance. Some people call a home an asset because it can appreciate and build equity. Others call it a liability because it requires mortgage payments, taxes, insurance, repairs, and maintenance while producing no direct income unless rented or sold.

Both views contain truth. A home is an asset in the sense that it has value and can build equity. It can also provide stability, control, and protection from rent increases in some markets. But a home is also a major expense. It can consume cash flow, reduce flexibility, and require large ongoing costs.

The wealth impact of homeownership depends on price, location, financing terms, maintenance, taxes, insurance, opportunity cost, time horizon, and whether the household can comfortably afford it. A reasonably priced home purchased with manageable debt may support long-term stability. An oversized home bought to signal success may become a financial burden.

The asset mindset does not ask, “Is homeownership always good or bad?” It asks, “Does this housing decision strengthen or weaken the household’s financial position?”

Cars, Status, and Depreciation

Vehicles are often where the asset-versus-liability lesson becomes visible. A car may be necessary for work, family, and daily life. In that sense, it supports income and function. But most cars depreciate. They also require fuel, insurance, repairs, registration, parking, and sometimes interest payments.

The financial danger is not owning a car. The danger is overbuying a car. An expensive vehicle financed over many years can turn transportation into a wealth leak. The monthly payment may appear manageable, but the opportunity cost can be large. Money going to car debt cannot go to investments, emergency savings, or debt reduction.

Status spending compounds in the wrong direction because it often creates recurring obligations. A person may buy a car to feel successful, then work harder to afford the payment, insurance, maintenance, and lifestyle expectations attached to it. The appearance of wealth can quietly delay actual wealth.

The asset-minded approach is not to avoid all comfort. It is to avoid letting depreciating purchases dominate the balance sheet.

Productive Assets That Build Wealth

Productive assets are assets that can generate income or long-term growth. They are central to wealth building because they allow money to work beyond the owner’s direct labor.

Diversified stock investments allow households to own shares of businesses. Over long periods, broad equity ownership can participate in economic growth, though values fluctuate and losses are possible. Bonds can provide income and stability, but they carry interest-rate, inflation, and credit risk. Rental real estate can produce rent and appreciation, but it requires management, capital, and local market knowledge. Businesses can create profit and equity value, but they carry operational risk. Intellectual property can generate royalties, but success depends on demand and distribution.

There is no single best asset for everyone. The right asset depends on time horizon, risk tolerance, income stability, tax situation, knowledge, liquidity needs, and goals. A simple diversified portfolio may be better for one person than direct real estate. A business may be appropriate for someone with expertise and risk tolerance. Bonds may matter more for someone nearing retirement. Cash may be essential for someone with unstable income.

The principle is not to buy every possible asset. The principle is to own productive assets in a way that fits the plan.

The Role of Diversification

Asset ownership builds wealth, but concentrated ownership can create danger. A person whose wealth depends entirely on one company, one property, one industry, one business, or one market is exposed to specific risks.

Diversification spreads risk across assets. A diversified investor does not need every company to succeed. A household with multiple income sources is less dependent on one paycheck. A business owner who invests outside the business reduces dependence on one enterprise. A property investor with reserves and careful financing is less vulnerable to one vacancy or repair.

Diversification can feel less exciting than concentration. Concentrated bets create the most dramatic success stories. But they also create many failures. Wealth preservation often requires resisting the temptation to place everything on one idea.

The goal is not merely to become wealthy. The goal is to remain financially resilient while wealth grows.

How Liabilities Compound Against You

Liabilities compound against a household in three ways.

First, interest costs consume cash flow. A credit card charging high interest turns every unpaid balance into a growing obligation. The borrower pays not only for the original purchase but also for the cost of delaying payment.

Second, payments reduce investment capacity. A household sending hundreds or thousands each month to lenders has less money available to buy assets. Even if the debt balance is not growing, the opportunity cost is real.

Third, liabilities reduce flexibility. High fixed payments make job loss, illness, relocation, entrepreneurship, or family changes more difficult. The borrower must keep earning enough to satisfy the obligations.

This is why bad debt is so damaging. It does not only reduce today’s comfort. It claims tomorrow’s choices.

How Assets Compound for You

Assets compound in the opposite direction. Investments can generate returns. Businesses can reinvest profits. Rental properties can build equity. Dividends and interest can be reinvested. Skills can increase income. Reputation can create opportunities. Each gain can become the base for the next gain.

The process is slow at first. A small investment account may not feel meaningful. A first dividend may be tiny. A small emergency fund may not feel like wealth. A young business may produce modest profit. But compounding rewards time and repetition.

The asset buyer’s advantage is not always visible in the early years. The liability buyer may appear to enjoy life more because consumption is visible. The asset buyer may seem ordinary because wealth is often hidden in accounts, equity, and ownership claims. Over time, the hidden advantage becomes more visible.

Assets create options. Liabilities create obligations.

The Behavioral Challenge

If buying assets is so powerful, why do many people struggle to do it? The answer is not only math. It is behavior.

Consumption provides immediate reward. Assets provide delayed reward. Debt makes consumption immediate. Investing requires patience. Status spending is visible. Asset accumulation is often invisible. Social pressure rewards appearance. Compounding rewards restraint.

Humans are not naturally designed to optimize thirty-year financial outcomes. We respond to emotion, comparison, fear, desire, convenience, and habit. This is why systems matter. Automatic saving, automatic investing, spending limits, debt repayment plans, separate accounts, emergency funds, and scheduled financial reviews help protect people from short-term impulses.

The asset mindset must be designed into daily life. Otherwise, the consumption environment will usually win.

Building an Asset-First Financial System

An asset-first system does not rely on leftover money. It assigns income before lifestyle absorbs it.

The system begins with essential expenses: housing, food, utilities, transportation, healthcare, insurance, childcare, and minimum debt obligations. Then it directs money to emergency savings, high-interest debt repayment, retirement contributions, investments, and other asset-building goals. Lifestyle spending is planned around what remains.

This order matters. Many households reverse it. They spend first, then save what is left. But what is left is often nothing. Asset-first planning makes wealth building a priority rather than a hope.

Automation can help. Retirement contributions can come directly from pay. Transfers to savings can happen after income arrives. Investment purchases can be scheduled. Debt payments can be automated. The less the system depends on monthly motivation, the better.

Asset-first does not mean joyless. It means intentional. A person can spend on enjoyment while still protecting the future. The problem is not spending. The problem is spending that permanently prevents ownership.

The Role of Income Growth

Asset building becomes easier when income grows faster than expenses. This is why increasing skills and earning power is part of the asset conversation.

A person can cut spending to create a gap, but income growth can expand the gap. Higher income can fund emergency savings, debt repayment, retirement contributions, investments, business capital, education, and insurance. The danger is lifestyle inflation. If every raise is consumed, the gap does not grow.

The strongest wealth pattern is to raise income, control fixed expenses, and direct a meaningful share of increases toward assets. A raise can become a larger car payment, or it can become a larger investment contribution. A bonus can become a vacation, or it can eliminate debt. Business profit can become lifestyle inflation, or it can become retained capital.

The decision determines whether higher income becomes higher wealth.

Asset Buying at Different Income Levels

The asset strategy looks different depending on income and stability.

For someone with very limited income, the first step may be survival and stabilization. That may include accessing benefits, reducing immediate debt pressure, finding stable housing, improving employment, using community resources, or building a small emergency fund. The advice to buy investments may be premature if essentials are not secure.

For someone with modest but stable income, the focus may be building a small cash reserve, avoiding high-interest debt, contributing to employer retirement plans where available, and investing small amounts consistently. Small amounts matter because they build the habit and begin the compounding process.

For a middle-income household, asset building may include retirement accounts, diversified taxable investments, home equity, education savings, insurance, and debt management. The key challenge is often lifestyle inflation and large fixed costs.

For high-income households, the challenge may be preserving the gap between income and expenses, managing taxes, diversifying concentrated equity or business wealth, protecting assets, and planning for estate transfer. High income creates opportunity, but it also enables expensive mistakes.

The principle is the same at every level: convert available surplus into assets. The implementation changes with circumstances.

Not Every Asset Should Be Bought Immediately

The desire to buy assets can lead to mistakes. Some people invest before building an emergency fund. Some buy rental property without understanding expenses. Some purchase individual stocks based on hype. Some borrow heavily to invest. Some buy businesses without reviewing financials. Some chase high-yield products without understanding risk.

Asset buying should follow due diligence. What is the expected return? What are the risks? How liquid is the asset? What taxes apply? What fees exist? What could cause loss? How does this asset fit the broader plan? Is the buyer financially prepared to hold through volatility or setbacks?

Sometimes the best asset purchase is not a new investment. It may be paying off high-interest debt. It may be building cash reserves. It may be buying insurance. It may be investing in a skill. It may be improving a business. It may be creating an estate plan.

The asset mindset is not about rushing into ownership. It is about allocating capital wisely.

The Social Side of Asset Ownership

Asset ownership is not only a personal finance issue. It has social consequences. Families that own assets can pass advantages to the next generation: education funding, housing support, business capital, inheritance, financial knowledge, and safety nets. Families without assets may have to start over every generation.

This is one reason the difference compounds. Asset ownership can create multi-generational momentum. A parent with investments may help a child avoid student debt. A family with property may provide housing stability. A business may employ relatives or be transferred. Financial knowledge may be taught early. Emergency support may prevent a crisis from becoming permanent.

The absence of assets compounds too. Without reserves, emergencies become debt. Without inheritance, each generation begins with fewer cushions. Without investment accounts, market growth benefits others. Without ownership, income must come primarily from labor.

This does not mean wealth is destiny. Families can change their trajectory. But it does show why asset ownership matters beyond individual choices. It shapes opportunity over time.

The Estate Planning Connection

Owning assets creates another responsibility: deciding what happens to them during incapacity or after death. Asset building without estate planning is incomplete.

A will, beneficiary designations, powers of attorney, healthcare directives, trusts where appropriate, and an asset inventory can protect the wealth that has been built. Without planning, assets may be delayed, misdirected, taxed inefficiently, or disputed. Beneficiary designations should be reviewed regularly because certain accounts may pass outside a will.

Estate planning is not only for the wealthy. Anyone with children, financial accounts, property, business interests, life insurance, retirement accounts, or healthcare preferences needs some level of planning. The more assets a person builds, the more important organization becomes.

Wealth is not only about acquiring assets. It is about protecting and transferring them with intention.

A Better Version of the Statement

The original statement is memorable because it creates contrast. But a more accurate and useful version would be:

People who consistently use surplus income to buy productive assets, while limiting unnecessary liabilities, are more likely to build wealth over time.

This version avoids judging people by income level. It recognizes that surplus matters. It distinguishes necessary liabilities from unnecessary ones. It focuses on repeated behavior. It includes time.

It also makes the principle actionable. The question becomes: How can I increase surplus? Which liabilities are weakening my future? Which assets should I acquire first? How can I protect the assets I already own? How can I keep the process going long enough for compounding to matter?

Practical Steps to Shift From Liabilities to Assets

Begin with a balance sheet. List what you own and what you owe. Include cash, investments, retirement accounts, property, vehicles, business interests, credit card debt, loans, mortgages, and other obligations. Net worth is not a measure of personal worth. It is a financial map.

Next, review cash flow. How much income comes in each month? How much goes out? Which expenses are essential? Which are flexible? Which debts carry the highest interest rates? How much surplus exists?

Then build a small emergency fund. This protects against new debt. After that, attack high-interest debt while maintaining essential reserves. If an employer offers retirement benefits or matching contributions, evaluate how to use them. Begin investing consistently in diversified assets suited to your time horizon and risk tolerance. Increase contributions as income rises.

Review major purchases carefully. Before taking on a new payment, ask what it will do to the freedom gap. Before buying a depreciating item, consider the opportunity cost. Before borrowing, understand the total cost. Before investing, understand the risk.

Finally, protect progress. Use insurance appropriately. Diversify. Keep records. Update beneficiaries. Avoid scams. Continue learning. Revisit the plan after major life changes.

What to Avoid

Avoid using debt to create the appearance of wealth. Avoid assuming every asset is a good investment. Avoid buying liabilities because monthly payments seem manageable. Avoid carrying high-interest consumer debt while trying to build wealth. Avoid lifestyle inflation that absorbs every raise. Avoid blaming individuals for every financial hardship while ignoring real constraints. Avoid waiting until you feel wealthy to start building assets.

Avoid financial shame. Shame rarely improves decision-making. Clarity does. The question is not how past choices look. The question is what the next dollar can do.

What to Do

Create a gap between income and expenses. Build liquidity. Reduce expensive debt. Increase earning power. Buy productive assets consistently. Reinvest returns. Diversify. Protect against major risks. Use debt carefully and only when the expected benefit justifies the cost and risk. Turn income into ownership before lifestyle consumes it.

Teach the asset mindset without contempt. The goal is not to divide people into rich and poor categories. The goal is to help more people understand how ownership, debt, and time interact.

The Difference That Compounds

The difference between assets and liabilities may begin as a small monthly choice. Invest or spend. Save or borrow. Buy for use or buy for status. Build reserves or depend on credit. Increase skills or stay economically exposed. Reinvest returns or consume them. Keep the car longer or upgrade early. Buy diversified assets or chase appearances.

One choice rarely determines a life. Repeated choices do.

Assets are claims on future value. Liabilities are claims against future income. The household that steadily increases assets while controlling liabilities becomes stronger over time. The household that accumulates obligations while neglecting ownership becomes more fragile. That is the compounding difference.

The lesson is not that rich people are good and poor people are bad. The lesson is that wealth follows ownership, surplus, discipline, and time. When money is consistently directed toward productive assets, the future begins to work for the owner. When money is consistently directed toward unnecessary liabilities, the future becomes more expensive.

Financial progress begins when the next dollar is given a better job.