The Psychology of Wealth: 8 Mental Habits That Shape Financial Success

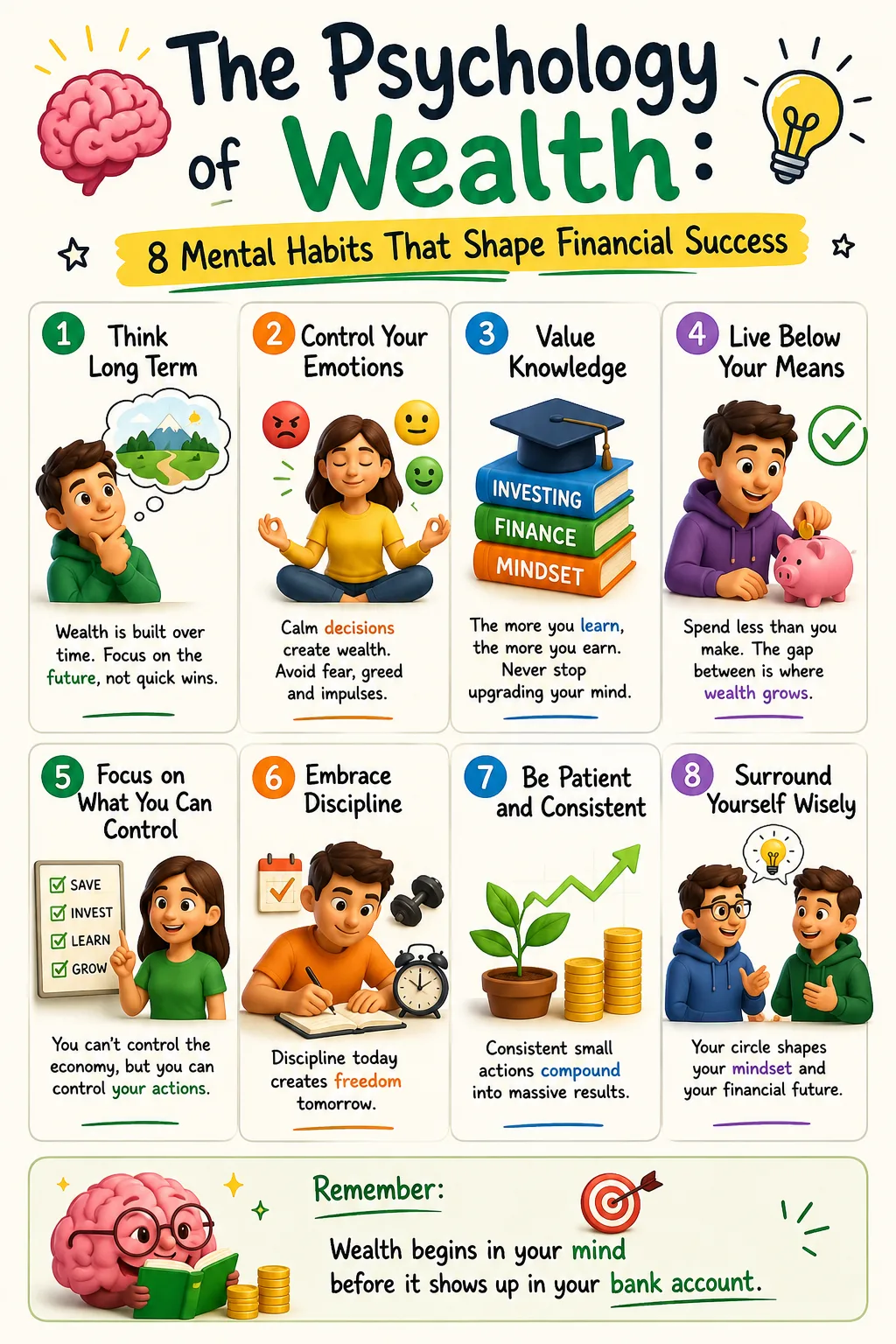

Wealth begins in the mind long before it appears on a balance sheet.

This does not mean positive thinking creates money by itself. It does not mean a person can visualize their way into financial security while ignoring income, debt, taxes, inflation, health, opportunity, or economic reality. Wealth is not magic. It is built through resources, choices, systems, time, and often circumstances that are not equally distributed.

But psychology matters because money is not only a mathematical subject. It is emotional, social, behavioral, and deeply personal. People do not simply earn, save, invest, and spend like machines. They compare themselves with others. They panic during market declines. They chase recent winners. They delay difficult decisions. They confuse luck with skill. They increase spending when income rises. They avoid looking at debt because it feels painful. They sell long-term investments because short-term fear becomes unbearable.

The technical side of finance asks, “What is the optimal decision?” The psychological side asks, “Can a real human being actually follow it?”

That second question explains why wealth is often less about discovering secret information and more about behaving consistently with ordinary truths. Spend less than you earn. Invest for long periods. Diversify. Control costs. Avoid ruin. Build liquidity. Increase income without surrendering every raise to lifestyle. Stay humble when things go well. Stay disciplined when things go badly.

These ideas are simple to understand and difficult to live.

Vanguard’s long-standing investing framework emphasizes four principles: set clear goals, maintain balance through diversification, minimize costs, and stay disciplined over time. The Federal Reserve’s Survey of Consumer Finances also reminds us that wealth is not merely income; it is reflected in household balance sheets, pensions, assets, debts, and other financial characteristics. Those two points together reveal the heart of wealth psychology: financial success depends on both structure and behavior.

This article explores eight psychological habits that shape wealth. They are not guarantees. They do not erase structural inequality, low wages, illness, family obligations, unstable work, or bad luck. But they help explain why some people convert income into assets while others convert income into lifestyle. They explain why some investors endure volatility while others sabotage their returns. They explain why humility, patience, and self-control can be more valuable than intelligence alone.

Wealth is built with money. But money must be guided by a mind that can wait, measure risk, resist pressure, and keep acting when the rewards are invisible.

1. Time Is Your Greatest Asset

Time is the quiet force behind nearly every durable fortune.

People often talk about money as if the amount invested matters most. The amount does matter. A person who can invest $2,000 a month has an obvious advantage over someone who can invest $100. But time changes the equation because it allows returns to build on previous returns. It allows small habits to become large outcomes. It allows assets to mature, debts to shrink, skills to compound, and knowledge to deepen.

Time is powerful because it does not require drama. A person does not need to predict every market movement, buy the perfect stock, or build a billion-dollar company to benefit from time. They need to begin, remain consistent, and avoid the kind of mistakes that interrupt compounding.

Compounding is often described mathematically, but its psychological requirement is patience. The early years can feel unrewarding. A person invests regularly and sees only modest progress. The balance grows, then falls during a market decline. The effort feels large and the result feels small. This is when many people lose interest. They want wealth to feel visible. They want evidence now.

But time rarely rewards impatience. It rewards endurance.

Consider a person who invests consistently for 30 or 40 years. The first decade may appear slow because contributions do most of the work. The second decade becomes more interesting because returns begin to contribute meaningfully. The third and fourth decades can become transformative because the accumulated base is finally large enough for growth to feel powerful.

This is why the late stages of compounding often look miraculous to people who did not witness the early stages. They see the final number and assume brilliance. In many cases, the real secret was simply that the investor did not stop.

Time also matters outside investment portfolios. A career compounds when skills, reputation, relationships, and judgment accumulate. A business compounds when systems, customer trust, brand recognition, and operational knowledge improve. A financial life compounds when small decisions are repeated for years: avoiding unnecessary debt, saving a percentage of income, insuring major risks, and increasing assets faster than liabilities.

The tragedy is that time is most valuable when people feel they have the least money. A young investor may believe there is no point in starting with small amounts. But small amounts invested early can matter more than larger amounts invested late. The early dollars have more years to work. The habit also has more years to mature.

Time is not only an asset because it allows money to grow. It is an asset because it allows mistakes to be corrected. A 25-year-old who learns from overspending, debt, or poor investment decisions has decades to recover. A 55-year-old making the same mistake has fewer years to rebuild. This does not mean older investors are doomed. It means delay carries a cost.

The psychological lesson is clear: respect time before it becomes scarce.

2. Start Investing Early

Starting early is one of the few financial advantages available to ordinary people without special access, elite networks, or inherited capital. It does not require knowing the future. It requires giving the future a claim on today’s income.

Early investing works because it combines habit formation with compounding. The first benefit is behavioral. A person who begins investing early learns to treat investing as normal. Money comes in, a portion goes out to future ownership, and the remainder funds current life. This rhythm matters. People who wait until they “feel ready” often discover that readiness keeps moving. There is always a bill, a purchase, a desire, a fear, or an excuse.

The second benefit is mathematical. Long investment horizons allow market volatility to be endured more comfortably. A young investor has time to survive recessions, bear markets, inflationary periods, interest-rate cycles, and economic surprises. Long horizons do not eliminate risk, but they change how risk can be managed.

The third benefit is educational. Investing early teaches lessons while the stakes are smaller. A young person who experiences a market decline with a modest portfolio learns emotional discipline. They discover what volatility feels like. They learn whether they are tempted to sell in panic or chase trends. These lessons are far cheaper when the account is small than when retirement depends on it.

Many people delay investing because they believe they do not know enough. This concern is understandable, but it can become a trap. Financial education is important, yet one does not need to master every advanced concept before beginning with simple, diversified, low-cost investments appropriate to their goals and risk tolerance. In fact, overcomplication can be its own form of procrastination.

A person might spend years searching for the perfect investment while missing the benefit of ordinary investing. They read about private equity, tax shelters, options strategies, cryptocurrency cycles, real estate syndications, and macro forecasts. Meanwhile, they have no emergency fund, no retirement contributions, and no automatic investment plan. Knowledge becomes entertainment rather than action.

Starting early does not mean investing recklessly. A person should first protect essentials, understand high-interest debt, build some liquidity, and avoid investing money needed immediately for rent, food, medical care, or urgent bills. But once basic stability exists, early investing should become a priority.

The phrase “small amounts can become large fortunes” is true only under certain conditions. The money must be invested productively. Costs must be controlled. The investor must avoid repeated panic selling. Time must be long enough. Contributions must continue. There is no guarantee of a fortune. But the principle remains: early ownership gives ordinary savings extraordinary room to grow.

Starting early also changes identity. A person who invests becomes not only a worker or consumer but an owner. They begin to participate in economic growth instead of only paying for the products and services that growth creates. This psychological shift is powerful. Owners think differently. They ask where cash flow comes from. They care about assets. They think beyond the next paycheck.

The earlier that identity forms, the more natural wealth building becomes.

3. Stay Humble

Humility may be the most underrated financial virtue.

Money can make people overconfident when things go well. A rising market can make investors feel brilliant. A business success can make founders believe every future decision will work. A few profitable trades can convince someone they have discovered a repeatable edge. A high salary can make a professional believe their income is permanent. A hot property market can make homeowners mistake broad appreciation for personal genius.

Success often includes skill. It may reflect discipline, intelligence, persistence, courage, and good judgment. But it also includes factors beyond personal control: economic cycles, interest rates, timing, geography, health, family support, market conditions, government policy, technological change, and plain luck.

Humility does not mean denying effort. It means refusing to confuse favorable circumstances with invincibility.

This matters because arrogance changes risk behavior. A humble person asks, “What could go wrong?” An arrogant person asks, “How much can I make?” A humble investor diversifies because they know the future is uncertain. An arrogant investor concentrates because they believe uncertainty applies mainly to other people. A humble household maintains emergency savings. An arrogant household assumes income will continue uninterrupted. A humble business owner protects against downside. An arrogant one overexpands.

Financial history is full of people who were right long enough to become dangerous to themselves. They made money in one environment and assumed the same strategy would work in every environment. They forgot that leverage feels intelligent when asset prices rise and brutal when they fall. They forgot that liquidity is invisible until it is needed. They forgot that customers, employers, lenders, markets, and governments can change.

Humility protects wealth because it keeps people teachable. A humble investor can admit they do not know which asset class will lead next year. A humble professional can keep improving skills even while income is strong. A humble entrepreneur can listen to customers instead of falling in love with a product. A humble family can live below its means because it understands that the future may not resemble the present.

Humility is also useful after failure. People who believe success is entirely personal may interpret failure as total personal defeat. That can lead to shame, denial, and paralysis. A more humble view recognizes that outcomes are mixed. Some losses reflect mistakes. Some reflect bad luck. Some reflect forces that could not have been predicted. The goal is to learn without being destroyed by self-blame.

Staying humble is not passive. It is not timid. It does not mean avoiding ambition or refusing opportunity. It means ambition with a margin of safety. It means confidence without delusion. It means understanding that the world owes no investor a smooth path.

In personal finance, humility often looks boring. It looks like diversification, insurance, cash reserves, written plans, modest assumptions, and refusal to bet the family’s future on one idea. These habits do not create exciting stories at dinner. They create durability.

4. Understand Risk

Risk is one of the most commonly used and least understood words in finance.

Many people think risk means the possibility of losing money this month. That is one form of risk, but it is not the only one. Risk can mean permanent loss of capital. It can mean volatility. It can mean inflation eroding purchasing power. It can mean illiquidity. It can mean being forced to sell at a bad time. It can mean concentration in one employer, one industry, one asset, or one country. It can mean borrowing too much. It can mean investing too conservatively for a long-term goal.

The right strategy depends on the individual because risk is personal.

A 28-year-old with stable income, no dependents, low debt, and a 35-year investment horizon can usually accept more investment volatility than a 62-year-old preparing to retire next year. A household with one income, three children, and a large mortgage needs a different cash reserve from a dual-income household with low fixed costs. A business owner with unpredictable income may need more liquidity than an employee with secure wages. A person with high-interest debt faces a different risk profile from someone with no debt and substantial savings.

This is why copying portfolios is dangerous. Two people can own the same investment and face different risks because their lives are different.

An asset that is appropriate inside one financial structure may be reckless inside another. A wealthy investor may hold private investments that cannot be sold easily because they have other liquid assets. A middle-class investor may buy the same illiquid asset and discover that paper wealth cannot pay an emergency bill. A young investor may tolerate a severe market decline because retirement is decades away. A retiree withdrawing from the portfolio may face sequence-of-returns risk if losses occur early in retirement.

Understanding risk also means understanding temperament. Some investors believe they are aggressive until the first large decline. They discover that a risk-tolerance questionnaire is easier than watching years of savings fall in value. The emotional experience of loss is different from the theoretical acceptance of volatility.

This is where planning matters. A written investment plan can reduce emotional decision-making by defining the purpose of each account, target allocation, rebalancing rules, liquidity needs, and circumstances that would justify a change. Without a plan, every market movement becomes an invitation to improvise.

Risk cannot be eliminated. It can only be managed, transferred, reduced, accepted, or misunderstood. Holding cash avoids market volatility but creates inflation risk. Investing in stocks creates volatility but may support long-term growth. Buying a home creates housing stability but introduces maintenance, concentration, and liquidity risk. Starting a business creates upside but also income uncertainty. Every path contains trade-offs.

Financial maturity is not the avoidance of risk. It is knowing which risks are worth taking, which risks are unnecessary, and which risks could ruin you.

5. Master Self-Control

Self-control is where financial knowledge becomes financial behavior.

Many people know what they should do. They know they should save more, spend less impulsively, avoid high-interest debt, invest consistently, compare prices, read contracts, and stop chasing status. Knowing is not the hard part. Repeating the right behavior under emotional pressure is the hard part.

Money decisions happen in moments of temptation, fear, fatigue, stress, pride, comparison, and desire. A person may have a sound financial plan on Monday morning and abandon it by Friday night after seeing friends at an expensive restaurant. They may intend to invest for decades and then sell during a market decline after reading alarming headlines. They may promise to avoid debt and then finance a lifestyle upgrade because they feel behind their peers.

Self-control is not merely personal toughness. It is also environmental design. The best financial systems reduce the number of times self-control must be heroic.

Automatic saving is one example. If money is transferred to savings or investments before it reaches everyday spending, the household is less dependent on willpower. Separate accounts help because money assigned to rent, taxes, emergency savings, or investing is less likely to be confused with discretionary money. Waiting periods help because many impulses fade after 24 or 48 hours. Written rules help because they move decisions from emotional moments into calmer planning sessions.

Self-control also requires knowing one’s weaknesses. Some people overspend socially. Some overspend online at night. Some overspend after stress. Some are vulnerable to sales. Some chase market trends. Some avoid financial tasks until they become emergencies. The goal is not to pretend these patterns do not exist. The goal is to design around them.

Behavioral finance is important because investors often experience a gap between investment returns and investor returns. Morningstar’s Mind the Gap research focuses on how timing decisions and investor behavior can affect the returns investors actually experience. This is a reminder that the investment one owns is only part of the outcome. The investor’s behavior around that investment also matters.

Self-control is especially important during rising income years. A raise creates opportunity, but it also creates temptation. Without discipline, higher income becomes higher spending. With discipline, higher income becomes higher savings, faster debt repayment, better insurance, and more ownership.

Self-control should not be confused with misery. A healthy financial life includes enjoyment. The problem is not spending. The problem is spending that steals from priorities the person claims to value more. A budget is not a punishment when it reflects genuine goals. It is a protection against the version of ourselves that trades tomorrow for a momentary feeling.

Mastering self-control means learning to create distance between desire and decision. That distance is where wealth is often saved.

6. Study Financial History

Financial history does not repeat perfectly, but it teaches patterns of human behavior.

Markets change. Products change. Technology changes. Regulations change. The names of the assets change. But fear, greed, leverage, overconfidence, panic, speculation, fraud, and herd behavior appear again and again. The details evolve; the psychology remains familiar.

Studying financial history helps investors avoid believing that the present moment is entirely new. Every boom produces arguments for why old rules no longer apply. Every bubble has a story. Every crisis feels unprecedented while it is happening. Every generation believes it has discovered innovations that eliminate risk. Sometimes there truly are major innovations. But even real innovation can be overpriced when enthusiasm becomes detached from cash flows, affordability, and risk.

History teaches humility because it shows how often smart people were surprised. It teaches patience because it shows that markets have endured wars, recessions, inflation, political crises, banking panics, technological shifts, and policy mistakes. It teaches caution because it shows that leverage and euphoria can destroy wealth quickly. It teaches perspective because it reminds investors that declines are part of long-term markets, not evidence that the future has ended.

Studying history also helps people understand the difference between temporary loss and permanent impairment. A diversified market portfolio may decline sharply and later recover, though recovery is never guaranteed on a specific timetable. A fraudulent scheme, bankrupt company, or overleveraged speculation may never recover. History helps investors ask better questions about what they own and why it might survive.

The phrase “the past leaves clues for the future” must be handled carefully. History does not provide a script. It does not tell investors exactly when to buy, sell, borrow, or wait. It does not guarantee that future returns will match past returns. But it provides context. It shows ranges of outcomes. It reveals the emotional traps that appear when people forget that uncertainty is normal.

Historical perspective is especially valuable during extremes. In euphoric markets, history whispers that trees do not grow to the sky. In panicked markets, history reminds us that fear can overprice disaster. In quiet markets, history warns that calm can breed complacency.

A financially educated person does not study history to become a fortune teller. They study history to become less naive.

7. Avoid Lifestyle Inflation

Lifestyle inflation is the silent enemy of wealth building.

It happens when spending rises with income. A person receives a raise and upgrades the apartment. Another raise brings a nicer car. A bonus funds a holiday. A promotion justifies private memberships, expensive restaurants, premium devices, and more convenience. None of these choices may feel extreme. The household is simply adjusting to its new level.

The danger is that every income increase is immediately claimed by lifestyle. The person earns more but saves the same amount. Or worse, they earn more and take on larger obligations. Financial stress remains because the cost of life rises as fast as the income supporting it.

Lifestyle inflation is psychologically powerful because people adapt quickly. What once felt luxurious becomes normal. What once felt normal begins to feel inadequate. The reference group changes. A professional earning more money may spend more time around people who also spend more. The comparison baseline rises, and yesterday’s success becomes today’s expectation.

This is why avoiding lifestyle inflation does not mean refusing every upgrade. It means upgrading deliberately and in the right order. Higher income should first increase financial strength. Emergency savings should improve. High-interest debt should fall. Retirement contributions should rise. Investments should grow. Insurance should be reviewed. Only then should lifestyle expand from the remaining surplus.

A useful rule is to save a portion of every raise before experiencing it as spendable income. If a person receives a 10 percent raise and automatically directs half of it toward savings or investing, lifestyle can still improve while wealth building accelerates. This protects progress without demanding permanent austerity.

Lifestyle inflation is most dangerous for high earners because it hides behind abundance. A person with a large income may assume they are doing well because bills are paid and purchases are possible. But if assets are not accumulating, the high income is only financing an expensive present.

The goal of earning more is not merely to spend more beautifully. It is to increase options. A larger income should buy lower stress, greater resilience, more ownership, and eventually more freedom. If it only buys a larger cage, the income has been underused.

8. Control What You Can

Much of finance is uncontrollable.

No individual controls market returns, inflation, interest rates, recessions, tax law, political events, currency movements, employer decisions, housing cycles, technological disruption, or global shocks. A person can study these forces, but they cannot command them. Obsessing over what cannot be controlled can create anxiety without improving outcomes.

The most productive financial minds focus on controllable variables: savings rate, spending behavior, debt management, diversification, costs, tax awareness, insurance, career development, emergency reserves, investment discipline, and time horizon.

This is not glamorous. Predicting markets feels more exciting than increasing a savings rate. Debating economic forecasts feels more intellectual than reducing high-interest debt. Chasing hot investments feels more active than making automatic contributions to a diversified portfolio. But controllable actions often matter more to real households than sophisticated predictions.

The Federal Reserve’s 2025 report on household well-being noted that 63 percent of adults said they would cover a hypothetical $400 emergency expense exclusively with cash, savings, or a credit card paid off at the next statement. That statistic is a reminder that basic resilience still matters. Before a household worries about complex market forecasts, it must ask whether it has enough liquidity to handle ordinary life.

Control also means building systems that function during stress. A household cannot control job loss, but it can reduce fixed expenses, build emergency savings, maintain professional skills, and avoid unnecessary debt. An investor cannot control market downturns, but they can diversify, maintain an appropriate allocation, avoid panic selling, and avoid investing money needed soon. A family cannot control every medical event, but it can evaluate insurance and avoid being underprotected against catastrophic risks.

Control is liberating because it narrows attention. Instead of trying to solve the entire financial universe, a person asks, “What action is available to me this month?” That action might be tracking expenses, increasing contributions by 1 percent, refinancing expensive debt, reviewing insurance, applying for a better job, building a starter emergency fund, or writing an investment policy statement.

Small controllable actions compound because they are repeatable. Forecasts may be wrong. Systems can keep working anyway.

The Wealth Mindset Is Not Blind Optimism

The phrase “wealth mindset” is often misused. It can become a vague promise that thoughts alone produce prosperity. That is not serious financial education. A real wealth mindset is not blind optimism. It is disciplined realism.

Disciplined realism sees opportunities without denying risks. It believes improvement is possible but does not pretend that every starting point is equal. It values ambition but respects arithmetic. It understands that income matters, but so do savings, debt, behavior, taxes, inflation, and time. It studies success without ignoring luck. It studies failure without surrendering to cynicism.

A healthy wealth psychology does not shame people for being poor or financially stretched. Many households face constraints that cannot be solved by mindset alone. Low wages, high rent, medical expenses, caregiving duties, unstable work, discrimination, weak local economies, and family emergencies can overwhelm even disciplined people. Financial advice becomes cruel when it ignores these realities.

At the same time, external realities do not eliminate the importance of behavior. Two households with similar incomes can end up in different positions because one controls debt, saves consistently, invests, protects against risk, and avoids lifestyle inflation while the other does not. Personal decisions matter most when they are repeated over years.

The wealth mindset worth having is not, “I will be rich because I think rich.” It is, “I will make decisions that increase resilience, ownership, and freedom within the reality I face.”

How These Principles Work Together

The eight principles are connected. Time rewards early investing. Early investing requires self-control. Self-control is strengthened by focusing on what can be controlled. Understanding risk helps investors remain disciplined. Studying history creates humility. Humility prevents overconfidence. Avoiding lifestyle inflation creates the surplus that allows investing to happen. Every habit supports the others.

A person who understands time but lacks self-control may still fail to invest consistently. A person who invests early but does not understand risk may panic during volatility. A person who earns more but cannot avoid lifestyle inflation may never create surplus. A person who studies history but refuses humility may believe they are the exception to every past mistake.

Financial success rarely comes from one trait. It comes from alignment. The mind, habits, income, spending, investments, and risk management must point in the same direction.

That alignment can begin modestly. A person does not need a large portfolio to practice patience. They do not need a high income to track spending. They do not need advanced knowledge to avoid high-interest debt. They do not need wealth to become humble, disciplined, or historically aware.

The first signs of progress may be invisible. A bill is paid on time. A transfer to savings happens automatically. A credit card balance falls. A purchase is delayed. A market decline is endured without panic. A raise is partly invested instead of fully spent. These moments may not impress anyone else, but they reshape the financial future.

A Practical Framework for Applying the Psychology of Wealth

The first step is to define the purpose of money. Without purpose, money is easily captured by impulse and comparison. Purpose might include security, homeownership, retirement, education, business ownership, family support, generosity, travel, independence, or freedom from toxic work. Clear purpose gives discipline a reason to exist.

The second step is to measure the present honestly. Calculate net worth. List debts, interest rates, assets, monthly income, fixed expenses, insurance coverage, and savings rate. Wealth psychology must be connected to facts. Motivation without measurement becomes fantasy.

The third step is to create liquidity. An emergency fund is psychological as much as financial. It reduces panic, prevents expensive borrowing, and gives the household room to think. The first target can be small. The point is to begin creating distance between life and crisis.

The fourth step is to automate wealth-building behavior. Automate savings. Automate investing. Automate debt repayment where appropriate. Automation turns intention into infrastructure. It also reduces the emotional negotiation that occurs every payday.

The fifth step is to invest according to a written plan. The plan should define goals, time horizon, target allocation, contribution schedule, rebalancing approach, and rules for changing strategy. The plan should be boring enough to follow during both excitement and fear.

The sixth step is to review lifestyle inflation before it becomes permanent. Every raise, bonus, promotion, or business improvement should be divided intentionally between present enjoyment and future strength. Money that is not assigned will usually be absorbed.

The seventh step is to study financial history and personal history. Market history teaches external patterns. Personal history teaches internal patterns. Where have you overspent? When have you panicked? Which environments trigger poor decisions? Which habits have worked before? Self-knowledge is a financial tool.

The eighth step is to keep humility as wealth grows. The larger the portfolio, the more important risk management becomes. Success should increase gratitude and caution, not recklessness. The goal is not only to become wealthy. It is to remain financially secure through changing conditions.

What Wealth Psychology Looks Like in Real Life

Imagine two professionals who earn similar incomes. One sees each raise as permission to upgrade. A better apartment, a larger car payment, premium travel, more subscriptions, and frequent status purchases become the new standard. They are not broke in the obvious sense. Bills are paid. The lifestyle looks successful. But the emergency fund remains thin, investments are inconsistent, and debt grows whenever life becomes inconvenient.

The other professional also enjoys life but captures part of every raise for wealth building. They maintain a modest car, automate investments, build cash reserves, avoid credit card balances, and upgrade slowly. Their lifestyle may look less impressive. But after ten years, the difference is substantial. One household has memories and payments. The other has memories and assets.

The gap did not come from intelligence alone. It came from psychology: patience, self-control, resistance to comparison, and the ability to value invisible progress.

Consider two investors during a market decline. One checks their account daily, reads alarming commentary, sells after losses, and waits for confidence to return. By the time confidence returns, prices may have already recovered. The other investor reviews their plan, confirms that their time horizon has not changed, continues automatic contributions, and rebalances if appropriate. Both investors experienced the same market. Their behavior produced different outcomes.

Consider two entrepreneurs. One quits a job immediately after having an idea because they believe boldness guarantees success. They have little savings, no customers, and high fixed expenses. The stress of survival forces rushed decisions. Another builds the business while employed, tests demand, saves a runway, tracks margins, and leaves only when the venture can support the risk. Both value entrepreneurship. One respects risk.

Wealth psychology is not abstract. It appears in ordinary decisions repeated under pressure.

The Role of Luck, Access, and Circumstance

No serious discussion of wealth psychology should ignore luck and access.

Some people begin with family wealth, elite education, stable housing, strong networks, good health, safe neighborhoods, and early exposure to financial knowledge. Others begin with debt, instability, medical challenges, family obligations, underfunded schools, discrimination, or local economies with limited opportunity. The same habit can produce different outcomes depending on the starting point.

Starting early is easier when there is surplus income. Self-control is easier when basic needs are met. Risk-taking is easier when failure is survivable. Investing is easier when financial systems are accessible and trusted. Humility includes recognizing these differences.

This does not make the eight principles useless. It makes them more grounded. A person facing hardship may apply them differently. “Start investing early” may first mean building a $500 emergency fund. “Control what you can” may mean applying for public benefits, renegotiating debt, finding more stable work, or protecting housing. “Avoid lifestyle inflation” may be irrelevant to someone who cannot yet cover essentials. Financial advice must meet reality before it can improve reality.

The psychology of wealth should empower people, not blame them. It should show what is possible while respecting what is difficult.

The Difference Between Being Rich and Being Financially Mature

Being rich and being financially mature are not the same.

A rich person has money. A financially mature person understands money. A rich person can still overspend, overborrow, speculate, ignore taxes, neglect insurance, and confuse luck with skill. A person of modest means can be financially mature by managing risk, saving consistently, investing patiently, and making thoughtful trade-offs.

Financial maturity is visible in behavior. It is the ability to delay gratification without becoming joyless. It is the ability to take risk without gambling. It is the ability to enjoy success without assuming it will last forever. It is the ability to learn from failure without being consumed by shame. It is the ability to ignore social pressure when the balance sheet says no.

Many people want wealth because they want freedom. But freedom requires maturity. Without maturity, more money may simply create larger mistakes. Higher income can fund larger debts. Bigger bonuses can fund bigger lifestyle inflation. Access to credit can fund larger speculation. Social status can create pressure to spend even more.

The psychology of wealth is therefore not only about getting money. It is about becoming the kind of person who can use money well.

Building a Personal Wealth Philosophy

A personal wealth philosophy is a set of rules that guides financial decisions before emotions take over. It does not need to be complicated. In fact, the best philosophy is often simple enough to remember under stress.

One person’s philosophy might be: “I invest automatically, avoid high-interest debt, keep six months of expenses in cash, and never buy luxury goods with borrowed money.” Another might be: “I increase my savings rate with every raise, maintain diversified investments, and make major financial decisions only after sleeping on them.” Another might be: “I protect my family first, invest for decades, and do not risk money I need within three years.”

The exact rules vary. The point is to decide in advance what kind of financial life you are building.

A strong philosophy should include a view on time, risk, debt, spending, saving, investing, giving, insurance, and lifestyle. It should be realistic enough to follow and strong enough to resist pressure. It should allow enjoyment but prevent self-sabotage. It should evolve as life changes, but not shift with every headline.

Writing these rules down matters. A rule kept only in the mind can be rewritten by fear or desire. A written rule creates accountability. It reminds the future self what the calm self believed.

Final Thought: Wealth Rewards the Mind That Can Wait

The psychology of wealth is not about secret tricks. It is about becoming steady in a world designed to make people restless.

Markets move. Friends upgrade. Advertisers tempt. Headlines frighten. Social media compares. Economic conditions change. Life interrupts. The person trying to build wealth must operate inside all of this without surrendering every decision to the emotion of the moment.

Time is your greatest asset because it allows money and behavior to compound. Starting early matters because small actions need years to reveal their power. Humility matters because success is never entirely self-made. Risk awareness matters because every strategy belongs to a person, not a slogan. Self-control matters because knowledge without discipline does not build wealth. Financial history matters because human behavior repeats even when technology changes. Avoiding lifestyle inflation matters because surplus is the raw material of ownership. Controlling what you can matters because attention is too valuable to waste on the uncontrollable.

None of these principles guarantees wealth. But together, they create a financial character capable of building it.

The world often celebrates the visible signs of success. The psychology of wealth is quieter. It is found in the automatic contribution, the resisted impulse, the diversified portfolio, the emergency fund, the studied mistake, the patient plan, the humble assumption, and the decision to let time work.

Wealth is not only what you own. It is how you think while you are building, protecting, and using what you own.