The Scalable Mind: How Bill Gates Thinks Wealth Is Built

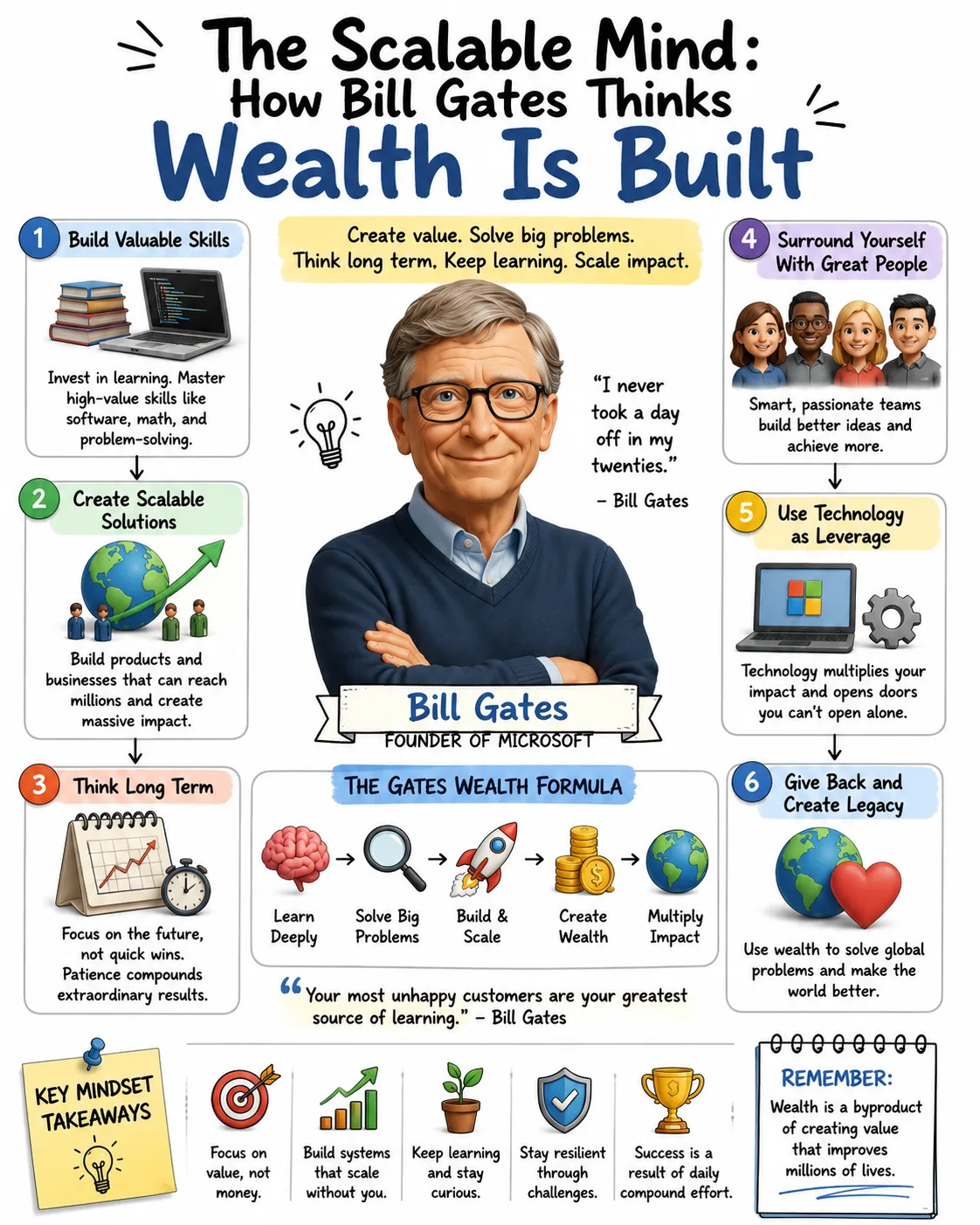

Bill Gates’ philosophy of wealth begins with an unusual kind of asset: the ability to learn faster than the world changes.

Before Microsoft became one of the most valuable companies in history, before personal computers became ordinary household tools, before software became the operating layer of modern business, Gates saw that code could scale in a way few physical products could. A program could be written once, improved repeatedly, distributed widely, and embedded into the daily work of millions of people. That insight turned technical skill into business leverage.

Gates did not build wealth by chasing short-term speculation. He built it by developing rare skills, applying those skills to a rapidly expanding technology market, surrounding himself with exceptional people, and creating software products that became essential infrastructure. His fortune was not the product of one lucky idea alone. It came from the intersection of timing, technical ability, strategic execution, platform economics, long-term thinking, and ownership.

His philosophy differs from purely investment-driven wealth advice. Gates’ path was not primarily about buying assets created by others. It was about building an asset so valuable that others organized their work around it. Microsoft’s rise showed the power of scalable technology: once software becomes a platform, every additional user, developer, business customer, and complementary product can strengthen the system.

At the same time, Gates’ later life adds another dimension to his wealth philosophy. Through philanthropy, global health work, climate writing, and public commentary, he has repeatedly emphasized that wealth is not only a private achievement. It creates responsibility. Capital can be used to fund research, improve health, expand education, reduce poverty, and solve problems markets may neglect.

To understand how to get rich according to Bill Gates, the starting point is not glamour. It is competence. Learn deeply. Build useful technology. Think in decades. Hire extraordinary people. Reinvest in innovation. Protect capital. Read constantly. Focus on problems large enough to matter.

His approach is less dramatic than the mythology of overnight success. It is a philosophy of compounding: skills compound into judgment, judgment compounds into better decisions, products compound into platforms, platforms compound into competitive advantages, and capital compounds when reinvested wisely.

Wealth Begins With Rare Skills

Gates’ wealth philosophy starts with human capital. Early in life, before a person owns substantial financial assets, their most valuable asset is often their ability to learn, solve problems, and create value others cannot easily replicate.

Gates developed deep technical skill at a time when software was still emerging as a major commercial force. That combination mattered. Skill alone is not enough if it is applied to a stagnant field. A growing field alone is not enough if a person has no meaningful ability. Wealth emerges when rare capability meets expanding demand.

This is one of the most practical lessons in Gates’ philosophy. People who can solve difficult problems create disproportionate value. Software engineering, artificial intelligence, mathematics, data analysis, science, biotechnology, cybersecurity, engineering, product management, and technical communication all represent areas where skill can translate into economic leverage.

Rare skills do not have to be purely technical, but Gates’ life demonstrates the financial power of technical fluency. Software allows a small team to affect millions of users. A single improvement in code can be distributed globally. A productivity tool can become part of how companies operate. A platform can become the foundation for thousands of other businesses.

For an individual wealth builder, the lesson is clear: income potential improves when your skills become more valuable, more scarce, and more connected to important problems. A person who develops general ability may find work. A person who develops scarce ability in a growing market can create leverage.

This is why learning is not a phase of life in the Gates framework. It is the engine. The world changes too quickly for early education to remain sufficient. Technologies mature. Industries shift. New tools appear. Old advantages decay. The person who keeps learning can reposition before the market forces them to.

There is also a discipline to skill-building. Gates’ example is not casual curiosity alone. It is deep concentration. Serious skill requires long hours of study, practice, experimentation, feedback, and problem-solving. In fields like software and science, superficial knowledge is not enough. The market rewards people who can build, debug, reason, improve, and deliver.

Wealth, in this view, is not first a money problem. It is a capability problem. Before capital can compound, competence must be created.

Technology That Scales

Microsoft’s success illustrates one of Gates’ central business insights: scalable technology can create extraordinary wealth because revenue can grow much faster than costs.

A traditional business often requires substantial incremental cost for each additional customer. A restaurant needs more ingredients, staff, space, and equipment as it serves more people. A consulting firm needs more professional hours. A manufacturing business needs materials, logistics, and production capacity.

Software behaves differently. Once a software product is created, the cost of distributing it to one additional user can be relatively low. The company still has expenses: engineering, support, security, sales, infrastructure, research, compliance, and administration. But the marginal economics can be powerful. A product that serves one thousand customers may be adapted to serve one million. A digital tool can cross borders faster than a physical operation.

This scalability is central to Gates’ wealth philosophy. Build something useful once, improve it constantly, and distribute it widely. If the product becomes essential, the business can generate significant profits because the value delivered increases across a large customer base.

Scalability also changes ambition. A local service business may be excellent but limited by geography and labor capacity. A software platform can become global. It can serve individuals, companies, governments, schools, and developers. It can become part of the operating system of work itself.

The strongest scalable businesses often share several traits. They solve frequent problems. They improve productivity. They become embedded in workflows. They benefit from user familiarity. They can be updated over time. They attract complementary products or developers. They create switching costs because customers build habits, files, processes, and systems around them.

Microsoft’s history reflects these dynamics. Operating systems, productivity software, developer tools, and enterprise platforms do not merely sell once; they become part of how people work. Once a tool becomes a standard, it gains advantages that competitors must overcome.

For entrepreneurs, the Gates lesson is not simply “build software.” It is to look for business models where value can expand without costs rising at the same speed. That can include software, digital education, cloud services, data products, platforms, intellectual property, automated services, and certain forms of media or infrastructure.

Scalability should not be confused with ease. Building a scalable product is difficult. Technology markets are competitive. Customers have high expectations. Security and reliability matter. Distribution can be expensive. Large incumbents can respond aggressively. But when scalability works, it creates a form of business leverage that few traditional models can match.

Build Products That Become Platforms

Gates’ wealth was not created by a single product in isolation. Microsoft became powerful because its products became platforms. A platform is more than a tool. It is an environment others depend on, build upon, or integrate into their own work.

This distinction is critical. A product solves a problem for a customer. A platform becomes part of the customer’s operating system. It attracts developers, partners, training, documentation, complementary products, integrations, and institutional habits. The more people use it, the more valuable it can become.

Platform businesses can create durable wealth because they sit at the center of ecosystems. A company that controls an important platform may benefit from network effects, switching costs, standards, developer loyalty, and recurring demand. Customers do not leave easily because their work, data, employees, and processes become connected to the system.

Gates understood that software ecosystems matter. Developers want to build where users are. Users want access to the applications and tools they need. Businesses want compatibility. Training programs and IT departments prefer standards. Each part reinforces the others.

This creates a compounding advantage. A platform with more users attracts more developers. More developers create more applications. More applications attract more users. More users encourage more training and institutional adoption. Over time, the platform can become difficult to displace even when alternatives exist.

The platform lesson applies beyond Microsoft. Many of the most valuable modern technology companies operate platform models: cloud computing ecosystems, app stores, marketplaces, payment networks, enterprise software suites, operating systems, developer platforms, and data networks.

For wealth builders, the lesson is to seek positions where value compounds through connection. A business that sells one-time products must continually replace demand. A platform can become stronger as more participants join. A professional can apply the same principle by building a network, body of expertise, community, or toolset that others rely on.

Platform thinking also requires responsibility. Once people depend on a system, reliability, security, governance, and trust become essential. A platform that abuses its position can face customer backlash, regulatory scrutiny, and reputational damage. Durable wealth requires maintaining the ecosystem, not merely extracting from it.

Think in Decades

Gates’ approach to wealth is fundamentally long term. Microsoft was not built for a quick exit. It was built through years of product development, strategic partnerships, hiring, competition, reinvestment, and adaptation.

Long-term thinking matters because meaningful companies take time to build. Products must improve. Customers must be earned. Talent must be recruited. Systems must mature. Competitive advantages must be defended. Capital must be allocated wisely across cycles.

Short-term thinking can damage a company that should be compounding. A business obsessed with immediate profit may underinvest in research, product quality, customer trust, and talent. It may cut the very capabilities that would make it stronger later. Gates’ philosophy emphasizes sustained value creation, not temporary financial appearance.

This does not mean ignoring current performance. A company must survive the present to reach the future. Cash flow, execution, customer satisfaction, and competitive positioning matter every day. But short-term decisions should serve long-term strategy.

Long-term thinking is also crucial for investors. Markets can be noisy. Prices move for reasons unrelated to long-term value. Economic cycles, interest rates, sentiment, regulation, and fear can distort judgment. Gates’ broader public posture, especially through his relationship with long-term investors such as Warren Buffett, reflects respect for patient capital and disciplined decision-making.

For individuals, thinking in decades changes behavior. A person choosing a career asks not only what pays today, but what skills will matter in ten years. An entrepreneur asks whether the business can remain relevant as technology changes. An investor asks whether the asset can compound across cycles. A student asks which fields are expanding, not merely which credentials are fashionable.

Patience is not passivity. It is commitment to a compounding process. Gates’ philosophy asks people to become serious enough about the future to invest in it before the rewards are visible.

Read Constantly, Learn Relentlessly

Gates is widely known for his reading habits. Reading is not a decorative part of his public image; it is central to how he gathers information, tests assumptions, and expands judgment.

In his philosophy, reading is a way to borrow the expertise of others. A well-chosen book can compress years of research, experience, history, or scientific discovery into a form that improves decision-making. For a business leader, investor, technologist, or philanthropist, that matters.

Continuous learning helps identify emerging opportunities. A person who reads deeply across technology, economics, history, science, climate, health, and policy can make connections that others miss. Gates’ later work in global health and climate reflects this interdisciplinary learning style. Wealth creation and problem solving often happen at the intersection of fields.

Reading also slows down thinking in a useful way. In a business culture dominated by speed, headlines, and short-form commentary, books and long-form analysis provide context. They help distinguish durable trends from temporary noise. They reveal how systems work beneath surface events.

For wealth builders, the practical lesson is not merely to read more, but to read better. Choose material that improves judgment. Study fields connected to your work. Learn from history. Understand technology shifts. Read opposing views. Take notes. Revisit important ideas. Turn knowledge into decisions.

Learning becomes financially valuable when it changes behavior. Reading about software is useful if it helps a founder build better products. Reading about climate is useful if it helps an investor understand energy transitions. Reading about management is useful if it helps a leader hire and delegate better. Reading about economics is useful if it improves capital allocation.

Gates’ reading habit reflects a broader principle: ignorance compounds negatively, but knowledge compounds positively. The person who stops learning makes decisions with an aging map. The person who keeps learning updates the map as the terrain changes.

Solve Important Problems

Gates’ philosophy emphasizes working on problems large enough to matter. This applies to business, technology, and philanthropy.

Microsoft’s early opportunity was tied to a major shift: personal computing. As computers moved from specialized institutional tools toward widespread business and household use, software became essential. The problem was not small. People needed operating systems, productivity tools, programming environments, and digital infrastructure.

Large problems create large opportunities because many people or institutions need better solutions. Productivity, healthcare, climate, education, agriculture, cybersecurity, artificial intelligence, and digital infrastructure all represent areas where successful solutions can produce significant economic and social value.

Gates’ later focus on global health and climate reinforces the idea that important problems require systems thinking. A disease problem may involve science, logistics, funding, behavior, governments, and infrastructure. A climate problem may involve energy production, industrial processes, agriculture, policy, innovation, and consumer adoption. These are not simple markets; they are complex systems.

For entrepreneurs, solving important problems does not always mean starting with a grand global mission. It can begin with a specific bottleneck inside a large system. A software tool that saves companies hours of work, a medical device that improves diagnosis, an education platform that helps students learn, or a cybersecurity service that protects small businesses can all address meaningful needs.

The key is seriousness. Trend chasing often leads entrepreneurs toward crowded markets with shallow demand. Problem solving leads them toward durable value. If the problem is real, frequent, expensive, or painful, customers have a reason to care.

Important problems also attract talent. Skilled people want to work on things that matter. A company with a meaningful mission can recruit people motivated by more than compensation. That becomes a competitive advantage when combined with strong execution.

There is a danger, however, in confusing importance with business viability. A problem can be socially important and still difficult to solve profitably. Clean energy, healthcare, and education often involve regulation, long sales cycles, entrenched systems, and complex incentives. Gates’ approach would not ignore these realities. It would study them deeply.

The wealth lesson is to look for problems where impact, technical feasibility, customer demand, and scalable economics can meet.

Hire Outstanding People

Gates has consistently emphasized the importance of hiring exceptional talent. In technology businesses, the difference between average and outstanding talent can be enormous. A great engineer, product leader, scientist, designer, or manager may not be slightly better than average; they may produce outcomes that reshape the company.

This belief reflects a broader principle: wealth creation is often a team achievement. Even visionary founders need people who can build, sell, operate, improve, defend, and scale the business. A company’s quality eventually reflects the quality of its people and the standards they maintain.

Hiring outstanding people is not only about intelligence. It includes judgment, work ethic, curiosity, collaboration, integrity, resilience, and ability to learn. A company filled with brilliant but misaligned people can still fail. Talent must be organized around a mission, culture, and operating system.

Gates’ Microsoft was known for high standards and intense technical culture. That intensity helped the company compete in a fast-moving market. High standards can create excellence, but they must be managed carefully. A demanding culture can produce innovation when paired with clarity and purpose. It can become destructive if it creates fear, politics, or burnout.

For entrepreneurs, the hiring lesson is that early team decisions are among the most important capital allocation choices a company makes. Payroll is not merely an expense. It is an investment in capability. Hiring weak people because they are convenient can be more expensive than hiring strong people who raise the company’s ceiling.

Outstanding people also attract other outstanding people. Talent density compounds. Strong teams create better products, make better decisions, and recruit from stronger networks. They raise expectations. They notice problems earlier. They challenge weak thinking.

For individual wealth builders, this principle applies personally. Surround yourself with people who improve your standards. Partners, mentors, colleagues, investors, and advisors shape decisions. A person’s network can either expand or limit ambition.

Gates’ philosophy makes hiring a core wealth-building function because no scalable company is built by one person alone.

Build Competitive Advantages

Creating wealth is not only about launching a successful product. It is about defending the value created. Gates understood that technology markets can change quickly. A company that leads today may fall behind if it stops improving.

Competitive advantage is what allows a company to earn attractive returns despite rivals. In software, advantages may include platform adoption, developer ecosystems, switching costs, data, brand, distribution, enterprise relationships, integration, intellectual property, and continuous innovation.

Microsoft’s strength came partly from ecosystem power. When customers, businesses, developers, and hardware partners organize around a platform, the platform gains resilience. Competitors must not only build a better product; they must persuade an entire ecosystem to move.

Switching costs are especially important. Once a company trains employees on software, stores files in certain formats, builds workflows around tools, and integrates systems, changing providers becomes expensive and risky. The incumbent gains time to improve and defend its position.

But competitive advantages are not permanent by default. Technology history is full of once-dominant companies that missed transitions. Gates’ own career includes moments where Microsoft had to respond to major shifts, from the internet to cloud computing to mobile computing to artificial intelligence. The lesson is that advantages must be renewed.

A company with a strong market position can become complacent. Customers may tolerate it for a while, but if innovation stops, vulnerability grows. Gates’ philosophy emphasizes ongoing investment because leadership is not a trophy; it is a responsibility to keep improving.

For investors, competitive advantage is one of the most important questions. Does the company have pricing power? Can competitors copy it easily? Are customers locked in by value or merely habit? Is the market growing? Does scale strengthen the business? Is management reinvesting wisely?

For entrepreneurs, the question is equally direct: if your product works, why will you still win five years from now?

Innovation as a Discipline

Gates’ philosophy treats innovation as essential for long-term success. But innovation is not only a flash of inspiration. It is a discipline involving research, experimentation, product development, feedback, and repeated improvement.

Technology companies must innovate because their markets evolve. Customer expectations rise. Competitors improve. New platforms emerge. Security threats change. Hardware capabilities expand. Regulation shifts. A product that feels advanced today may feel outdated in a few years.

Innovation requires investment before returns are certain. Research and development can be expensive. Many experiments fail. Some products never become commercial successes. But a company that refuses to invest in innovation may protect short-term margins while weakening its future.

Gates’ interest in areas such as artificial intelligence, climate technology, digital health, and scientific research reflects a belief that breakthrough innovation can address both economic and social challenges. AI may change how people work and learn. Clean technologies may reshape energy and industry. Biotechnology may improve health outcomes. Digital tools may expand access to services.

The wealth opportunity lies in combining innovation with execution. A good idea is not enough. The company must turn invention into a reliable product, distribute it, support it, price it, protect it, and improve it. Many technically impressive innovations fail because they do not become usable businesses.

For individual entrepreneurs, innovation can begin with practical improvement. Not every business must invent a new operating system or climate technology. Innovation may mean automating a painful workflow, simplifying a professional service, applying AI to a narrow industry problem, improving logistics, or designing a better customer interface.

The Gates lesson is that wealth favors people and companies that keep asking: what can technology now make possible that was not possible before?

Capital Allocation and Reinvestment

Gates’ wealth philosophy includes disciplined capital allocation. Building a great company requires deciding where money, talent, and time should go. Reinvesting profits wisely can strengthen competitive advantages, fund innovation, and extend the company’s future.

Capital allocation is not only an investor’s concern. It is a founder’s daily responsibility. Should the company hire more engineers or expand sales? Invest in research or improve support? Acquire a competitor or build internally? Return capital or reinvest? Enter a new market or deepen the existing one?

Good capital allocation compounds. Money invested in the right product, team, or infrastructure can produce returns for years. Poor allocation can waste resources and distract the company. Even successful businesses can decline if management deploys capital badly.

Gates’ broader philosophy favors maintaining financial flexibility. Companies that overextend themselves may lose strategic control. A strong balance sheet allows a business to invest during downturns, fund long-term research, and survive competitive pressure. Financial discipline is not the opposite of innovation; it is what makes sustained innovation possible.

For individuals, capital allocation begins with how income is used. High earnings do not automatically become wealth. Money can be spent, wasted, saved, invested, or reinvested in capability. Gates’ path reminds readers that capital should be directed toward assets, skills, businesses, and opportunities that can create long-term value.

Reinvestment is especially important in scalable businesses. Profits can fund better products, stronger teams, broader distribution, security, infrastructure, and new research. The company becomes stronger because yesterday’s success finances tomorrow’s advantage.

But reinvestment must be disciplined. Not every project deserves funding. Not every acquisition creates value. Not every research effort will pay off. Capital allocation requires judgment, measurement, and willingness to stop funding weak ideas.

Wealth grows when capital is protected from waste and deployed toward compounding advantage.

Artificial Intelligence and the Next Wave of Opportunity

Artificial intelligence fits naturally within Gates’ wealth philosophy because it combines technical complexity, broad usefulness, scalability, and the potential to reshape many industries. AI can improve productivity, accelerate research, personalize education, support healthcare, automate routine work, and create new software categories.

The opportunity is large because AI is not one product. It is a general-purpose technology that can be applied across sectors. Companies may use it to write code, analyze data, support customers, generate content, discover drugs, improve logistics, detect fraud, manage energy, and enhance decision-making.

But the Gates framework would treat AI with seriousness rather than hype. Large opportunities attract intense competition. Many AI tools may become commoditized. Durable wealth will likely accrue to companies that combine AI capability with proprietary data, distribution, workflow integration, trust, domain expertise, infrastructure, or platform control.

For individuals, AI reinforces the importance of lifelong learning. Some tasks will be automated. Other tasks will become more valuable when paired with AI tools. The workers who adapt may become more productive. The workers who ignore the shift may find their skills losing market value.

A Gates-inspired approach to AI would ask practical questions. What problems can AI solve better than existing methods? Which industries have inefficient workflows? Where is data available and useful? Where do customers need reliability and trust? What skills will remain scarce? How can AI increase human capability rather than merely reduce labor cost?

The wealth opportunity is not limited to building foundational AI models. Many successful businesses may be created by applying AI to narrow, valuable problems: legal workflows, medical administration, industrial maintenance, cybersecurity, education, accounting, scientific research, logistics, and enterprise productivity.

As with earlier software waves, the winners will not be those who merely use fashionable language. They will be those who build products customers depend on.

Measure Success Beyond Wealth

Gates’ later career makes it impossible to discuss his wealth philosophy without discussing responsibility. After stepping away from Microsoft’s day-to-day leadership, he devoted enormous attention and resources to philanthropy, especially global health, education, poverty reduction, and climate innovation.

This reflects a broader view: wealth creates optionality, but also obligation. Once personal financial needs are far exceeded, capital can be directed toward problems that markets and governments have not solved adequately.

Philanthropy is not separate from Gates’ analytical mindset. His approach often emphasizes measurement, evidence, scale, and systems. Which interventions save the most lives? Which technologies can reduce emissions? Which education reforms improve outcomes? Which health systems fail because of logistics rather than science?

This is consistent with his business philosophy. Solve important problems. Use data. Think long term. Invest in innovation. Measure results. Improve systems.

For ordinary wealth builders, the philanthropic scale may differ, but the principle still applies. Wealth is not only a scorecard. It is a tool. It can support family security, community institutions, education, medical care, scientific progress, entrepreneurship, and social improvement.

Thinking beyond wealth can also improve how wealth is built. A founder working on a meaningful problem may recruit better people and persist longer. An investor with values may avoid opportunities that create harmful externalities. A professional who sees money as a tool may make more balanced decisions.

Gates’ philosophy suggests that the final purpose of wealth is not endless accumulation. It is increased capacity to act.

Where Gates’ Approach Can Go Wrong

Gates’ philosophy is powerful, but it can be misapplied.

The first risk is assuming every technology business will scale like Microsoft. Most software companies do not become dominant platforms. Many struggle with distribution, competition, churn, security, pricing, or weak demand. Scalability creates upside, but it does not guarantee success.

The second risk is underestimating competition. Technology markets evolve quickly. A company can be innovative and still lose if competitors move faster, build better products, control distribution, or capture developer mindshare. Technical excellence must be paired with strategy.

The third risk is ignoring regulation. Large platform businesses can face scrutiny over competition, privacy, security, labor, and market power. The stronger a company becomes, the more its social responsibilities increase.

The fourth risk is overinvesting in research without commercial discipline. Innovation matters, but businesses must eventually deliver products customers adopt. Research spending should connect to a credible path of value creation.

The fifth risk is believing learning alone is enough. Reading and studying are essential, but wealth requires application. Knowledge must become skill, product, strategy, investment, or decision. Information without execution does not compound financially.

The sixth risk is trying to imitate Gates without his context. He entered software at a historically important moment, had rare technical ability, worked intensely, found the right co-founder and market, and executed through a company that became central to personal computing. The lesson is not that everyone should copy his path exactly. The lesson is to understand the principles beneath it.

Those principles remain useful: build valuable skills, choose growing markets, create scalable products, hire exceptional people, think long term, and reinvest in durable advantages.

A Practical Gates-Inspired Wealth Strategy

A practical wealth strategy inspired by Bill Gates begins with skill selection. Choose an area where demand is likely to grow and expertise is difficult to fake. Artificial intelligence, software, cybersecurity, data, biotechnology, climate technology, robotics, cloud infrastructure, digital health, and technical product leadership are examples of fields where deep skill can create leverage.

Then study seriously. Build projects. Read widely. Learn from experts. Practice problem-solving. Develop the ability to explain complex ideas clearly. Technical skill becomes more valuable when paired with communication.

Next, place yourself near important problems. Work in industries where technology is changing the economics. Join companies that are building useful products. Start small projects that solve real pain points. Avoid spending years in roles that do not build transferable capability.

Seek ownership where appropriate. This may mean founding a company, joining a promising startup with equity, investing in public companies, building intellectual property, or creating digital assets. Gates’ wealth came from ownership of a company that scaled. Income matters, but ownership creates upside.

Build or invest in scalable models. Look for products or services that can serve many customers without costs rising proportionally. Software, data products, platforms, and digital infrastructure can offer this potential.

Surround yourself with strong people. Choose colleagues, partners, advisors, and mentors who raise standards. Great teams make better decisions than isolated individuals.

Think long term. Do not abandon a compounding path because early results are slow. Skills, products, companies, and investments often take years to mature. Patience is productive when paired with improvement.

Allocate capital carefully. Save, invest, reinvest, and maintain flexibility. Avoid unnecessary risks that could force you out of the game. Wealth is built by surviving long enough for good decisions to compound.

Finally, define what the wealth is for. Security, freedom, invention, philanthropy, family, community, and impact may all matter. Money becomes more meaningful when connected to purpose.

The Real Meaning of Getting Rich According to Bill Gates

Bill Gates’ philosophy of getting rich is not about shortcuts. It is about building capacity that scales.

Develop rare skills. Apply them to large problems. Build technology that can reach millions. Create products that become platforms. Hire outstanding people. Reinvest in innovation. Think in decades. Keep learning. Protect capital. Use wealth responsibly.

This philosophy is demanding because it requires depth. It does not reward shallow trend chasing. It rewards the person who can understand difficult systems, build useful tools, and stay committed long enough for value to compound.

For the modern wealth builder, Gates’ example is especially relevant because technology continues to reshape opportunity. Software, artificial intelligence, cloud computing, digital health, climate technology, and scientific innovation are still creating new markets. The people who learn deeply and build seriously can participate in that change.

But the lesson is broader than technology. Gates shows that wealth follows scalable value. A person becomes financially powerful when their knowledge, product, company, or capital can serve more people without being limited entirely by personal hours.

According to Bill Gates, getting rich is not mainly about predicting the next hot trend. It is about becoming capable enough to build something the world needs, patient enough to improve it over decades, and disciplined enough to turn success into lasting value.

That is the scalable mind: the ability to convert learning into technology, technology into platforms, platforms into wealth, and wealth into impact.