The Value Builder: How Mark Cuban Thinks About Getting Rich

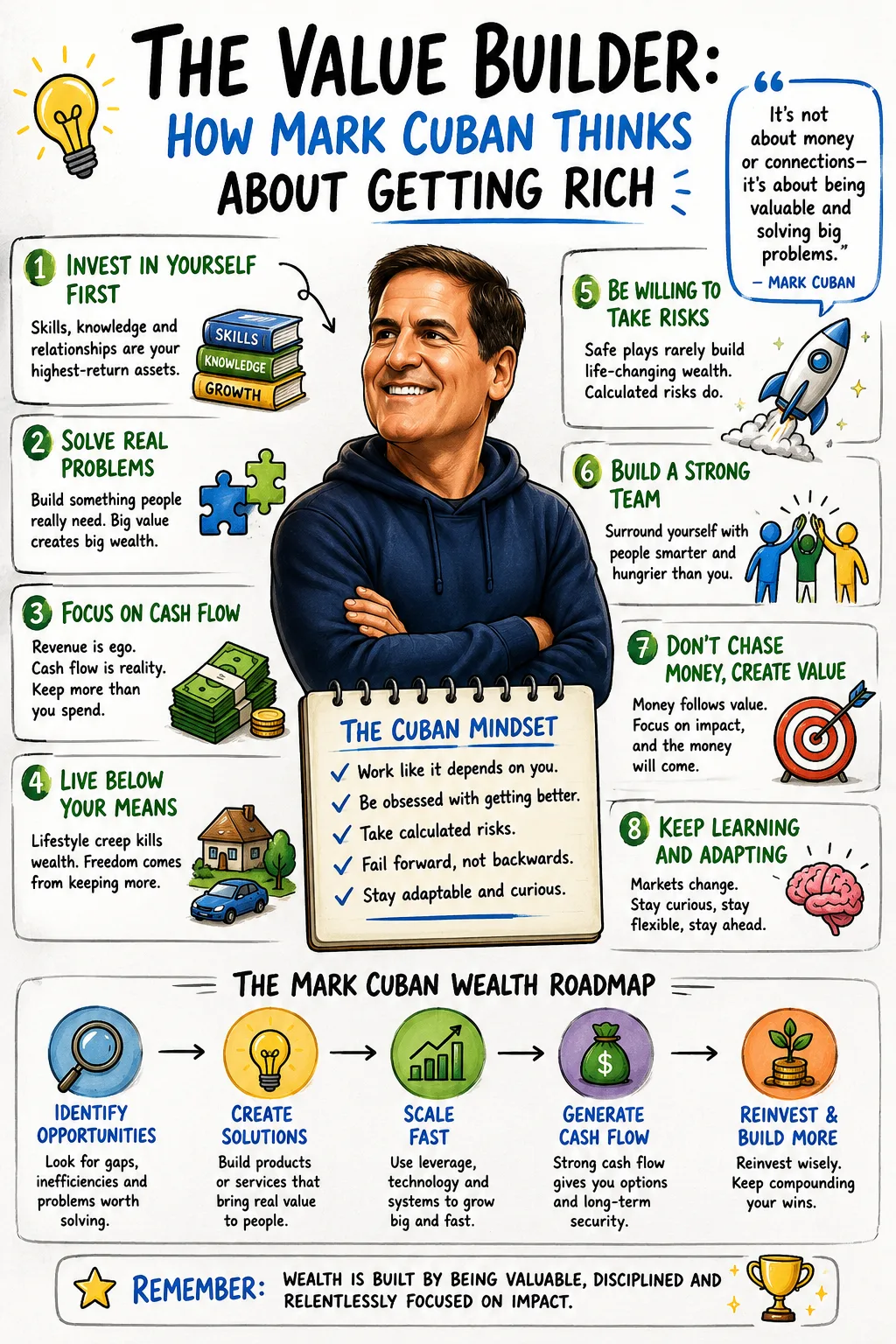

Mark Cuban’s philosophy on getting rich begins with a blunt idea: before you try to make your money work harder, make yourself more valuable. Cuban is not primarily known for preaching portfolio theory, elegant asset allocation, or quiet index-fund discipline. Those things can matter, but they are not the center of his message. His wealth philosophy starts closer to the ground: learn skills, sell something useful, avoid dumb debt, control expenses, understand technology, and build or own businesses that solve real problems.

That makes Cuban’s approach different from investors who begin with capital markets. Warren Buffett tells people to think like business owners when buying stocks. Ray Dalio asks investors to understand economic cycles and balance risk. John Bogle tells ordinary investors to own broad markets cheaply and patiently. Cuban’s advice often begins earlier in the wealth journey. He asks how a person can increase earning power in the first place.

His own career helps explain the emphasis. Cuban’s official biography describes a long entrepreneurial arc: selling and trading as a young person, working in software after moving to Dallas, being fired, founding MicroSolutions, selling it to CompuServe for $6 million, co-founding AudioNet, growing it into Broadcast.com, and selling Broadcast.com to Yahoo for $5.7 billion in stock. It also notes that he purchased the Dallas Mavericks for $285 million, later sold majority control in 2023, and continued to be involved with the team.

Those facts matter because Cuban’s wealth did not come mainly from clipping coupons or earning a high salary. It came from recognizing technological shifts, building businesses inside those shifts, selling when the economics were favorable, protecting capital, and repeatedly moving into new industries. His official biography also describes his later work in media, entertainment, “Shark Tank,” and the 2019 co-founding of Cost Plus Drugs, whose January 2022 launch used transparent pricing and a limited markup model to challenge prescription drug pricing.

Cuban’s philosophy is practical, aggressive, and grounded in execution. He is not anti-investing. He is not anti-markets. But he often argues that the average person’s highest-return early investment is not a stock, fund, or crypto token. It is the development of skills that can increase income, create business opportunities, and make the person useful in a changing economy.

That message is especially relevant now. Artificial intelligence, software automation, digital distribution, healthcare innovation, and small-business technology are changing how value is created. Cuban has recently argued that AI can help small businesses become more competitive and that people with AI skills may find opportunities by helping smaller firms adopt new tools.

To get rich according to Mark Cuban is not to wait for a perfect market entry point. It is to become valuable, stay liquid, avoid financial traps, build cash-flowing businesses, own equity, and keep learning before the world forces you to catch up.

Invest in Yourself Before You Invest Like a Professional

Cuban’s first wealth principle is that the best early investment is often self-improvement. Not vague self-improvement. Marketable self-improvement. Skills that make a person more useful, more employable, more persuasive, more technically capable, or more able to build something customers will buy.

This is a crucial distinction. Many people ask where to invest $500, $1,000, or $5,000 as if the right fund or stock will transform their financial life. Cuban’s answer would likely be less glamorous: use early money and time to increase your earning power. Learn sales. Learn software. Learn artificial intelligence. Learn how an industry actually works. Learn communication. Learn how to read financial statements. Learn how to solve a problem that businesses or consumers will pay to fix.

The logic is simple. A small portfolio can compound, but a small income has limited fuel. A person earning $35,000 a year and saving very little may not be transformed by a slightly better investment return. But if that person develops a valuable skill and raises income to $70,000, $100,000, or more, the entire financial equation changes. More income can fund debt repayment, emergency savings, business experiments, investment contributions, and personal freedom.

Skill development also compounds. A person who learns sales can use that skill in every job, business, negotiation, and investor conversation. A person who learns technology can spot opportunities before others do. A person who learns communication can lead teams, attract customers, raise capital, and build trust. A person who understands finance can avoid bad deals and recognize good ones.

Cuban’s biography illustrates this pattern. His early work in a Dallas software store gave him exposure to coding, installation, customer support, and business software. That experience became a bridge to MicroSolutions, which grew into a national systems integration company before being sold. The lesson is not that everyone should copy Cuban’s career path. The lesson is that expertise can become the seed of ownership.

Many people separate learning from earning. Cuban’s worldview connects them. The right learning increases earning power. The right earning power creates capital. Capital creates options. Options create the ability to take calculated risks. This is why investing in yourself is not motivational decoration. It is financial strategy.

Sales Is a Wealth Skill

Cuban often emphasizes sales because sales is the bridge between value and money. A person may have intelligence, ideas, or technical ability, but wealth requires convincing other people to exchange money, attention, trust, or opportunity. Sales is not merely persuasion. At its best, it is understanding a problem so clearly that the customer feels understood before being asked to buy.

This matters for employees as much as entrepreneurs. A worker who can sell ideas internally gains influence. A manager who can sell a vision can recruit talent. A founder who can sell customers can survive. A job candidate who can sell their value can negotiate better compensation. An investor who can sell a thesis can raise capital. A leader who can sell change can move an organization.

Cuban’s business career shows the importance of execution over ideas. AudioNet and Broadcast.com were not merely concepts about internet broadcasting. They required technology, customer development, deals, timing, and the ability to convince the market that streaming media would matter. His biography states that AudioNet became Broadcast.com, went public in 1998, and was later sold to Yahoo for $5.7 billion in stock. The idea mattered, but execution turned the idea into wealth.

This is one of Cuban’s most practical lessons for ordinary people: do not hide behind ideas. Ideas are abundant. Execution is scarce. Customers do not pay for what a founder imagines. They pay for something delivered, improved, supported, and trusted. The entrepreneur who cannot sell usually cannot learn fast enough from the market. The employee who cannot communicate value may remain underpaid even when competent.

Sales also teaches humility. The market does not care how much effort went into a product if customers do not want it. Rejection becomes information. Questions reveal objections. Objections reveal gaps. Gaps reveal what must be improved. This feedback loop is one of the fastest forms of business education.

For a Wealth Insights reader, the practical application is direct. Learn how to explain value clearly. Learn how to ask better questions. Learn how to identify pain points. Learn how to follow up. Learn how to negotiate without desperation. Learn how to close without deception. Ethical sales is not manipulation. It is the disciplined matching of a real problem with a credible solution.

Build Businesses That Solve Real Problems

Cuban’s entrepreneurship philosophy is grounded in utility. A business should solve a problem customers recognize and are willing to pay to fix. This sounds obvious, but many aspiring entrepreneurs start with what they want to build rather than what the market needs.

A real problem has urgency. It costs money, time, energy, status, safety, convenience, or opportunity. The customer feels it. The customer has tried to solve it. The customer understands why a better solution matters. When a business solves that kind of problem, marketing becomes easier because the offer meets existing demand.

By contrast, weak businesses often sell novelty without necessity. They require customers to be educated into caring. They depend on hype, discounts, or investor money rather than clear value. They may grow attention without durable cash flow. Cuban’s approach tends to favor businesses with practical economics: customers, revenue, margins, service quality, and cash flow.

His own career includes examples of problem-solving at different levels. MicroSolutions served business software and networking needs at a time when companies were adopting new computing infrastructure. Broadcast.com made internet streaming commercially meaningful before streaming became ordinary. Cost Plus Drugs addresses a visible problem in American healthcare: opaque and expensive prescription drug pricing. Cuban’s official biography describes Cost Plus Drugs as using transparent pricing and a limited markup model after its 2022 launch.

The deeper lesson is that wealth follows value creation. Not always immediately. Not always fairly. Not without risk. But over time, businesses that solve expensive problems have more room to grow than businesses built only on enthusiasm.

For aspiring entrepreneurs, this means the first question is not “What is my passion?” It is “Whose problem can I solve better than the alternatives?” Passion may help sustain effort, but customers buy solutions. A founder who loves coffee must still solve a location, quality, convenience, community, or pricing problem. A software founder must reduce friction, increase revenue, save labor, improve compliance, or create measurable benefit. A consultant must help clients make money, save money, reduce risk, or make better decisions.

Cuban’s philosophy rewards market contact. Talk to customers. Sell before building too much. Watch what people actually pay for. Study complaints. Study inefficiencies. Study industries where customers feel trapped. Wealth is often created by making a painful process simpler, cheaper, faster, or more trustworthy.

Execution Beats the Romance of Ideas

One reason Cuban resonates with entrepreneurs is that he strips away the romance of the “big idea.” Many people believe they are one idea away from wealth. Cuban’s career suggests something different: the idea is the opening move, not the game.

Execution includes product quality, hiring, timing, pricing, customer support, operations, cash management, sales discipline, and the willingness to keep improving after the excitement fades. It includes doing unglamorous work when nobody is applauding. It includes answering customer complaints, fixing broken processes, studying competitors, and understanding unit economics.

This is why entrepreneurship is both powerful and dangerous. It can create wealth faster than salaried employment because ownership captures upside. But it can also destroy savings, time, confidence, and relationships when handled carelessly. Cuban’s philosophy is not that everyone should quit a job tomorrow. It is that significant wealth often comes from ownership and problem-solving, but ownership must be earned through execution.

The modern economy makes starting easier than succeeding. A person can launch a website, open a store, create a product, publish content, or advertise globally with little upfront infrastructure. But low barriers create crowded markets. Customers have more options. Attention is expensive. Trust is hard to build. Technology can help small businesses, but it does not eliminate the need for a strong offer.

Execution also requires speed. Markets move. Technology changes. Competitors copy. Customer expectations rise. A founder who waits for perfect certainty may lose the moment. But speed without learning becomes recklessness. Cuban’s approach favors informed action: learn enough, test quickly, listen carefully, improve constantly.

This is where many people misunderstand entrepreneurial risk. The risky part is not merely starting. The risky part is starting without customer understanding, financial discipline, or adaptability. A calculated risk has a reason, a downside limit, and a learning loop. A reckless gamble has only hope.

Live Below Your Means So You Can Take Better Risks

Cuban’s wealth philosophy includes old-fashioned financial discipline. Spend less than you earn. Avoid unnecessary debt. Do not let lifestyle inflation consume future freedom. Save aggressively enough to create flexibility.

This advice may sound ordinary, but it is the foundation that makes Cuban-style risk possible. A person living paycheck to paycheck cannot easily walk away from a bad job, invest in skills, start a business, move for opportunity, or survive a failed experiment. High fixed expenses turn ambition into fragility.

Living below your means is not about worshiping austerity. It is about maintaining control. The person with low expenses and cash reserves can choose. The person with expensive obligations must obey. A larger house, luxury car, and status lifestyle may feel like success, but if they require constant high income, they reduce freedom.

Cuban’s own public advice on debt and spending has been unusually direct. In a 2009 blog post, he wrote that people should pay off debt by the best means available, not live beyond their means, put credit cards away if they do not need something, and forget about purchases they cannot pay for with cash. That is not sophisticated financial engineering. It is behavioral discipline.

The reason this matters is that wealth is built not only by making good investments, but by avoiding bad constraints. Lifestyle inflation is one of the most common bad constraints. Income rises, spending rises, and the person remains financially stressed at a higher standard of living. They appear more successful but have not become more free.

For high earners, this problem can be severe. A person earning $300,000 a year may still accumulate little wealth if the money disappears into housing, cars, private schools, travel, restaurants, subscriptions, and taxes. Another person earning less but saving and investing consistently may build more durable security. Cuban’s framework pushes people to value flexibility over display.

Living below your means also creates psychological strength. Cash in the bank changes how you negotiate. It reduces panic. It allows patience. It lets you say no to bad deals. It lets you wait for good opportunities. In Cuban’s world, financial discipline is not a conservative alternative to ambition. It is what makes ambition survivable.

High-Interest Debt Is an Emergency

Cuban is especially forceful about consumer debt. In a 2010 Blog Maverick post titled “The Best Investment Advice You Will Ever Get,” he wrote that if someone has credit card or other consumer debt at 5 percent interest or more, they should pay it off because compound interest becomes the enemy and the odds of earning more than the consumer interest rate are slim.

This advice is mathematically powerful. Paying off a credit card charging 20 percent interest is economically similar to earning a guaranteed 20 percent return before considering taxes and risk. Very few investments can promise that. The stock market may offer attractive long-term returns, but not guaranteed returns at credit card interest levels. A speculative investment might double, but it might also collapse. Debt repayment removes a certain cost.

High-interest debt also weakens decision-making. It creates stress, reduces cash flow, and limits options. A person carrying expensive debt may feel pressure to chase risky returns because normal progress seems too slow. That desperation can lead to worse decisions: speculative trading, predatory loans, get-rich-quick schemes, or business risks taken without adequate reserves.

Cuban’s view is useful because it restores order. Before trying to look clever, stop the financial bleeding. Pay off high-interest consumer debt. Build a cash cushion. Learn skills. Then invest and take risks from a position of strength.

This does not mean all debt is identical. A fixed-rate mortgage, a business loan used responsibly, or education debt tied to strong earning power is different from revolving credit card debt used to finance consumption. The key distinction is whether the debt supports future productive capacity or merely pulls consumption forward at a punishing cost.

For households, the first step is inventory. List every debt, interest rate, minimum payment, and payoff balance. Then prioritize high-interest obligations. Some people prefer the avalanche method, paying the highest rate first. Others prefer the snowball method, paying smaller balances first for psychological momentum. The best method is the one that gets expensive debt eliminated and prevents it from returning.

Cuban’s debt advice is not glamorous because the best financial moves often are not glamorous. Paying off a card does not create a social media-worthy investment story. But it improves net worth, cash flow, and peace of mind. That is real wealth building.

Cash Is Not Laziness; Cash Is Optionality

Cuban’s philosophy values cash because cash creates flexibility. Investors sometimes mock cash as unproductive, especially during bull markets. But cash has a strategic role. It covers emergencies, reduces forced selling, supports business starts, allows negotiation, and lets a person act when opportunities appear.

The value of cash is easiest to see during stress. A household with cash can handle job loss without immediately liquidating investments. A founder with cash can survive a slow sales month. An investor with cash can buy when others are forced to sell. An employee with cash can leave a toxic workplace or negotiate without fear. A family with cash can absorb medical, housing, or vehicle shocks without turning to high-interest debt.

Cuban’s career also shows the value of protecting capital after a major win. His official biography says that after Broadcast.com was sold to Yahoo, he became concerned that the internet stock boom could become a bust and hedged his stock through a collar that became famous as one of the great protective trades of the era. That move reflects a broader principle: getting rich is not enough. Wealth must be protected from concentration, timing, and overconfidence.

For ordinary people, the equivalent is less dramatic but just as important. Build an emergency fund. Avoid investing money needed for near-term obligations in volatile assets. Keep enough liquidity to avoid desperation. Do not treat every dollar as if it must chase return at all times.

Cash is also valuable in entrepreneurship. Many businesses fail not because the idea is worthless, but because cash runs out before the model works. Owners underestimate working capital, customer acquisition costs, delayed payments, inventory needs, taxes, and slow seasons. Positive cash reserves give the entrepreneur room to learn.

The opportunity cost of cash is real. Over long periods, excessive cash can trail productive assets. Inflation can erode purchasing power. But Cuban’s philosophy is not to hold all wealth in cash forever. It is to hold enough cash to remain flexible, resilient, and ready. Cash is not the destination. It is the oxygen that lets the wealth builder keep moving.

Cash Flow Is the Business Reality Check

Cuban often evaluates businesses through practical economics. Revenue is not enough. Growth is not enough. Attention is not enough. A business must eventually produce cash or have a credible path to doing so. Cash flow is the movement of money into and out of a business. Without it, even impressive companies can become fragile.

Cash flow matters because bills are paid in cash, not headlines. Payroll, rent, inventory, software, debt service, taxes, advertising, and suppliers require money. A company can be “growing” and still be in danger if it consumes more cash than it can raise or generate. During easy funding environments, businesses can hide weak economics behind investor capital. When conditions tighten, cash flow becomes the test.

Cuban’s preference for execution and sustainability is especially relevant to small business owners. A founder should know gross margin, customer acquisition cost, repeat purchase behavior, churn, working capital needs, payment cycles, and breakeven points. These are not accounting details reserved for finance teams. They are survival facts.

A business with healthy cash flow can fund expansion without constant dilution. It can survive downturns. It can invest in customers. It can hire carefully. It can negotiate better because it is not always desperate for financing. Cash flow gives an owner time and choice.

For employees and households, the same concept applies personally. Personal cash flow is income minus outflow. A high-income household with negative cash flow is not financially strong. A moderate-income household with positive cash flow, savings discipline, and growing assets may be far healthier. Wealth begins when surplus appears and is directed toward debt reduction, investment, business ownership, or skill development.

Cuban’s practical lesson is to respect money movement. Profit on paper matters, but cash in hand keeps the game alive. If the numbers do not work, optimism will not fix them.

Own Equity Whenever You Can Understand the Risk

Cuban’s wealth came from ownership. He did not become a billionaire by earning wages alone. He owned businesses whose value grew dramatically. That is one of his most important lessons: wages can create stability, but equity creates upside.

Equity means ownership. It can be ownership in a private business, public company, startup, real estate project, intellectual property, or a venture you build yourself. Equity allows wealth to grow with the value of an asset rather than merely with hours worked.

The employee earns income. The owner owns the system that produces income. The employee may receive a raise. The owner may receive profits, appreciation, dividends, sale proceeds, or strategic control. This does not make ownership morally superior. It makes ownership economically different.

Cuban’s Broadcast.com outcome illustrates the asymmetry. The company’s sale to Yahoo created wealth because the founders and investors owned equity in an asset that a buyer valued highly. A salary from the company would not have produced the same result. The ownership stake was the wealth engine.

But equity is risky. A startup’s equity may become worthless. A small business may fail. A public stock may decline. A concentrated position may create wealth and then destroy it. Cuban’s own protective hedging after the Yahoo transaction shows that even large ownership wins need risk management.

For ordinary readers, the goal is not to chase every equity opportunity. It is to seek intelligent ownership. That may include starting a business, acquiring a small business, earning equity compensation, investing in broad stock-market funds, buying shares of companies you understand, owning income-producing real estate, or creating intellectual property. The form matters less than the principle: build claims on future value.

A responsible ownership strategy requires due diligence. What are you buying? How does it make money? What could go wrong? How liquid is it? What is the valuation? What rights do you have? How much can you afford to lose? What percentage of your net worth is exposed?

Cuban’s entrepreneurship-forward philosophy can inspire people to own more, but it should not tempt them to ignore concentration risk. Ownership builds wealth when the asset is valuable and the risk is survivable. It destroys wealth when optimism replaces analysis.

Technology Changes the Wealth Map

Cuban’s career repeatedly intersected with technological change: business software, networking, internet streaming, media distribution, healthcare pricing technology, and now artificial intelligence. His philosophy rewards people who notice where technology is reducing friction, lowering costs, or opening new markets.

This is why lifelong learning is not optional in Cuban’s worldview. The economy changes. Skills decay. Industries shift. A person who stops learning becomes vulnerable to younger competitors, new software, changing customer expectations, and business models that make old advantages less valuable.

Artificial intelligence is the current example. Cuban has argued that AI creates opportunities for small businesses because they can use it to compete more effectively and because many smaller firms need help implementing it. Recent reporting on his job-market advice noted that he encouraged graduates to look at small businesses in the AI era, where AI knowledge may create immediate value.

This aligns with Cuban’s broader principle: do not merely consume technology; learn how it changes value creation. Someone who understands AI tools can help a law firm organize research, a clinic reduce administrative work, a retailer improve inventory decisions, a contractor streamline estimates, a restaurant improve marketing, or a manufacturer analyze operations. The opportunity is often not in building the next giant AI company. It is in applying technology to messy real-world problems.

Technology also rewards curiosity. Cuban’s story is not just about having capital. It is about being early enough to see shifts before they became obvious. He learned software when business computing was expanding. He built internet streaming before it became normal. He moved into transparent drug pricing when consumers were frustrated with opaque healthcare costs.

The practical lesson is to study change before it becomes mainstream. Read widely. Test tools. Talk to customers. Watch where people are frustrated. Watch where incumbents are slow. Watch where regulation, technology, and customer dissatisfaction intersect. That is where new fortunes often begin.

Adaptability Is a Competitive Advantage

Cuban’s philosophy is not built around one industry. He has moved across software, streaming media, sports, entertainment, television, startups, healthcare, and technology. That range reflects adaptability, one of the most important wealth traits in a changing economy.

Adaptability does not mean chasing every trend. It means updating assumptions when evidence changes. It means learning new tools without becoming attached to old methods. It means admitting when a business model is weakening. It means being willing to sell, pivot, hedge, or rebuild.

Many people fail financially because they confuse consistency with rigidity. Consistency is valuable when applied to principles: spend less than you earn, avoid high-interest debt, learn continuously, serve customers, manage cash flow. Rigidity is dangerous when applied to tactics: this industry will always work, this job will always be safe, this marketing channel will always produce leads, this asset will always rise, this skill will always be enough.

Cuban’s wealth philosophy separates principles from tactics. The principle is value creation. The tactic changes. The principle is customer focus. The product changes. The principle is learning. The subject changes. The principle is ownership. The asset changes. The principle is cash discipline. The business environment changes.

Adaptability also matters for careers. A worker in an AI-disrupted field may need to redesign their role before an employer does it for them. A small business owner may need to integrate automation before competitors reduce prices. A professional may need to learn data analysis, AI prompting, customer acquisition, or digital distribution to remain competitive.

The wealth builder should ask a Cuban-style question every year: “What do I need to learn now so that I am not obsolete later?” That question is uncomfortable, but it is cheaper than denial.

Take Calculated Risks, Not Desperate Gambles

Cuban’s career contains major risks, but they were not random. Starting MicroSolutions after being fired was risky, but it was tied to skills he had developed and a customer need he understood. Building Broadcast.com was risky, but it sat inside a technological shift he believed in. Hedging Yahoo stock after the sale showed that even after a win, risk needed to be managed.

This is the difference between calculated risk and gambling. A calculated risk has research, rationale, downside awareness, and a learning process. A gamble depends mainly on hope, emotion, or crowd excitement.

Entrepreneurship always involves uncertainty. Customers may not buy. Competitors may respond. Technology may change. Costs may rise. Financing may disappear. Founders may burn out. But the risk can be reduced by testing demand, starting small, controlling fixed costs, preserving cash, and learning quickly from customer behavior.

Investing also requires calculated risk. Every asset has uncertainty. Stocks can fall. Bonds can lose value when rates rise. Real estate can suffer vacancy or maintenance shocks. Startups can fail. Cash can lose purchasing power to inflation. The question is not whether risk exists. The question is whether the investor understands the risk and sizes it appropriately.

Cuban’s advice to pay off high-interest debt before chasing investments is part of this risk framework. It prevents people from taking speculative risks while guaranteed losses compound against them. Financial strength comes before aggressive opportunity-seeking.

A useful rule is to risk only what failure can teach you without ruining you. A small business experiment that costs time and modest capital may be worth it if it builds skill and market insight. A leveraged bet that can wipe out savings is different. A career move that increases learning may be worth short-term discomfort. A move that creates financial fragility without clear upside may not be.

Cuban’s wealth philosophy encourages boldness, but not fantasy. The goal is not to avoid failure. The goal is to make failures survivable and educational while positioning for rare wins.

Customer Obsession Is a Wealth Strategy

Cuban’s business worldview repeatedly returns to customers. A business exists because customers choose it. Investors may fund it. Founders may love it. Employees may work hard on it. But customers decide whether value is real.

Customer obsession means understanding not only what people say they want, but what they actually pay for, repeat, recommend, and complain about. It means caring about service, speed, price, trust, usability, and outcomes. It means treating customer frustration as a map to opportunity.

This is especially important in crowded markets. When many companies offer similar products, customer experience can become the difference. A faster response, clearer pricing, better onboarding, more honest communication, or simpler process can become an advantage.

Cost Plus Drugs is a clear example of a customer problem translated into a business mission. Prescription drug pricing in the United States has long frustrated consumers because prices can be opaque and difficult to understand. Cuban’s official biography describes Cost Plus Drugs as launching with transparent pricing and a limited markup model. Whether one evaluates it as a business, public-health intervention, or brand strategy, the principle is Cuban-like: attack a visible customer pain point with clarity.

For smaller entrepreneurs, customer obsession does not require a massive mission. A cleaning company can win by being reliable and transparent. A local contractor can win by communicating clearly. A software product can win by saving users from repetitive work. A consultant can win by delivering measurable results instead of vague advice. A retailer can win by curating better choices and handling problems gracefully.

Wealth often comes from trust repeated at scale. Customers return. They refer. They tolerate mistakes when they believe the company is honest. They pay premium prices when the value is clear. Cuban’s practical capitalism is not abstract. It begins with making the customer’s life better in a way the customer recognizes.

Small Businesses May Be the New AI Opportunity

One of the most current extensions of Cuban’s philosophy is the role of artificial intelligence in small business. Much of the public conversation about AI focuses on giant technology companies, chipmakers, and large enterprise platforms. Cuban’s recent career advice points in another direction: smaller companies may offer unusually good opportunities for people who understand AI because they need practical help applying it.

This is a very Cuban idea. It is not enough to admire technology from a distance. Wealth comes from applying technology where it solves a real problem. A small law office may not need an AI theorist. It may need someone who can automate intake, summarize documents, improve scheduling, and reduce administrative work. A dental practice may need better follow-up systems. A logistics company may need routing analysis. A retailer may need demand forecasting. A local service business may need better customer communication.

The opportunity is not only for founders. Employees who can bring AI productivity to smaller firms may become unusually valuable. They may grow faster, earn more responsibility, negotiate better compensation, or identify business ideas from inside real operations. The person who understands both technology and customer pain has leverage.

There is also a warning. AI skills must be paired with judgment. Tools can produce errors, privacy risks, compliance problems, and overconfidence. Businesses need people who can use technology responsibly, not merely enthusiastically. The most valuable workers will understand workflows, ethics, data, customer experience, and financial impact.

For readers looking to apply Cuban’s advice, the path is practical. Learn AI tools. Then learn an industry. The combination matters more than either alone. AI plus healthcare administration, AI plus accounting workflows, AI plus construction estimating, AI plus insurance documentation, AI plus local marketing, AI plus logistics, AI plus education support—these combinations are where value can appear.

Cuban’s broader lesson is that every technological shift creates winners among those who learn early and apply practically. The question is not whether AI is interesting. The question is where it can save time, reduce cost, improve decisions, or create revenue now.

Do Not Confuse Public Fame With the Actual Wealth Formula

Mark Cuban is famous, and fame can distort how people interpret his success. It is easy to focus on the visible symbols: the Mavericks, “Shark Tank,” media appearances, billionaire status, and public opinions. But the wealth formula underneath is less theatrical.

He built skill in a growing field. He started businesses. He sold to strategic buyers. He protected capital after a major liquidity event. He bought assets. He invested in companies. He kept learning across sectors. He used media to expand deal flow and reputation. He entered industries where customer frustration was high.

That sequence is more useful than the celebrity image. Most readers cannot replicate Cuban’s exact opportunities. They can replicate the principles. Learn a valuable field. Sell. Solve problems. Avoid high-interest debt. Preserve liquidity. Build or buy equity. Study technology. Take calculated risks. Protect wins.

Public fame may amplify Cuban’s opportunities, but it did not create the original foundation. The foundation was marketable knowledge and ownership. This distinction matters because many people chase attention before value. They want followers before customers, branding before product, funding before revenue, and visibility before competence.

Cuban’s career suggests the reverse order. Become useful. Build something. Sell it. Learn from customers. Create cash flow. Own upside. Visibility can help later, but it is not a substitute for economics.

Cuban Compared With Buffett, Dalio, Ferriss, and Naval

Cuban’s wealth philosophy overlaps with other influential thinkers but has its own center. Warren Buffett emphasizes patience, rationality, business quality, and compounding ownership in public markets. Ray Dalio emphasizes economic cycles, principles, diversification, and risk balance. Tim Ferriss emphasizes leverage, systems, automation, and lifestyle design. Naval Ravikant emphasizes specific knowledge, accountability, leverage, and ownership.

Cuban is closest to the operator. He wants people to build useful skills, sell real solutions, understand customers, generate cash flow, and own equity. He is less focused than Buffett on buying public companies at attractive valuations. He is less focused than Dalio on macroeconomic regimes. He is more operational than Ferriss, less philosophical than Naval, and more bluntly practical than many personal finance voices.

Where Cuban and Buffett align is ownership. Both understand that wealth comes from owning productive assets. Where they differ is path. Buffett’s public image is the disciplined allocator. Cuban’s is the builder and dealmaker. Where Cuban and Dalio align is risk management. Cuban’s debt avoidance and cash discipline are practical forms of risk control. Dalio’s version is more institutional and portfolio-based. Where Cuban and Ferriss align is leverage through business and technology. Cuban, however, tends to emphasize hard work, customer value, and cash flow more than lifestyle design.

The ordinary reader can combine the lessons. Use Cuban to increase earning power. Use Buffett to think like an owner. Use Dalio to respect risk and cycles. Use Ferriss to design systems and leverage. Use Naval to seek specific knowledge and accountability. Together, they form a more complete wealth philosophy.

The Cuban Wealth Framework for Ordinary People

A practical Cuban-inspired wealth plan begins with financial stabilization. Pay off high-interest consumer debt. Stop using credit cards to finance a lifestyle. Build a cash reserve. Know your monthly cash flow. Reduce expenses that exist mainly for status. This creates the base.

The second step is skill investment. Choose one or two skills that can materially increase earning power. Sales, AI, software, data analysis, negotiation, communication, industry expertise, and leadership are strong candidates. Do not learn randomly. Learn skills connected to market demand.

The third step is income expansion. Use new skills to earn more through a better job, promotion, consulting, freelancing, or a business experiment. The point is to convert learning into cash flow. Education that never changes earning power may be personally valuable, but it is not yet a wealth engine.

The fourth step is business thinking. Even if you remain an employee, learn to think like a business owner. What problem does your company solve? How does it make money? Where are margins created? What do customers complain about? Which processes are inefficient? Which technologies could improve results? Employees who understand business economics become more valuable.

The fifth step is ownership. Once the foundation is stable, begin acquiring or building assets. This may mean retirement investments, broad index funds, equity compensation, a small business, intellectual property, real estate, or private investments if appropriate. Ownership should be matched to knowledge and risk tolerance.

The sixth step is adaptability. Review your skills and industry exposure every year. What is changing? What could automate your work? What new tool could make you more productive? What customer problem is becoming more urgent? What business model is weakening? What opportunity is opening?

The seventh step is protection. When you win, protect the win. Avoid concentration that can ruin you. Avoid lifestyle inflation that absorbs gains. Avoid assuming a boom will last forever. Cuban’s hedging after the Broadcast.com sale is an extreme example of protecting a major gain. Ordinary investors can apply the same principle through diversification, cash reserves, insurance, tax planning, and disciplined spending.

The Limits of Cuban’s Approach

Cuban’s philosophy is powerful, but it has limits. Entrepreneurship is not equally accessible to everyone. Family obligations, health constraints, local economies, education, discrimination, capital access, and personal temperament all shape opportunity. Telling everyone to start a business ignores real constraints.

Entrepreneurship also has a high failure rate. A failed business can damage savings, credit, confidence, and relationships. Cuban’s story includes extraordinary successes, but it should not be read as proof that risk always pays. Survivorship bias is real. Many talented founders work hard and still fail because of timing, competition, capital constraints, or market changes.

Another limitation is concentration. Business ownership can build major wealth, but it can also concentrate risk in one asset. Cuban’s own story includes a famous protective hedge after Broadcast.com, which underscores the importance of managing concentration after a large win.

There is also a danger in overvaluing hustle. Cuban is known for intensity, but not every problem is solved by working longer. Strategy, customer selection, timing, margins, and health matter. Burning out in an unprofitable business is not noble. It is a signal to rethink the model.

AI enthusiasm also requires caution. Learning AI is valuable, but not every AI business will succeed. Many tools will become commodities. Some applications will face privacy, accuracy, legal, or ethical issues. The durable opportunity is not “AI” as a buzzword. It is using AI to solve expensive problems better than existing alternatives.

The mature version of Cuban’s philosophy is not reckless hustle culture. It is disciplined value creation. Learn. Sell. Solve. Save. Own. Adapt. Protect.

The Deeper Lesson: Become Useful Before You Become Rich

The heart of Cuban’s wealth philosophy is usefulness. Be useful to customers. Be useful to employers. Be useful to partners. Be useful in a changing economy. The more valuable the problem you can solve, the more opportunities you create.

This is a healthy antidote to speculative wealth culture. Many people want the outcome of wealth without becoming the kind of person who can create, manage, and protect it. Cuban’s message is less comforting: get good at something the market values. Learn faster than others. Work on real problems. Sell effectively. Manage money carefully. Take risks that make sense.

Usefulness also creates resilience. Markets change, but useful people can adapt. A person who understands customers, technology, sales, and cash flow can move across industries. A person who has only memorized one task may be vulnerable. Cuban’s career demonstrates reinvention across multiple sectors, and his current focus on AI and healthcare shows that he continues to look for practical inefficiencies rather than resting on past wins.

For readers, the question is direct: what are you becoming excellent at that the market will reward? If the answer is unclear, that is the next investment. Not a stock tip. Not a trend. A skill.

The Final Measure of Getting Rich According to Mark Cuban

To get rich according to Mark Cuban is to build value before chasing returns. It is to understand that the first asset is your own earning power. It is to learn skills that matter, especially in technology, sales, communication, and industry-specific problem-solving. It is to avoid high-interest debt because guaranteed financial leaks destroy future freedom. It is to live below your means so opportunity does not find you unprepared.

Cuban’s path is entrepreneurial, but not reckless. He believes in risk, but calculated risk. He believes in ownership, but not blind concentration. He believes in cash, but not permanent fear. He believes in technology, but only when it solves real problems. He believes in ideas, but only when execution turns them into customer value.

The most practical lesson is that wealth is built in stages. First, stabilize. Then learn. Then earn more. Then solve problems. Then own assets. Then protect gains. Then adapt again. The cycle repeats because the economy keeps changing.

Cuban’s philosophy is especially useful for people who feel stuck at the beginning of the wealth journey. It does not require inherited capital. It does not begin with sophisticated investing. It begins with becoming more capable. That is demanding, but it is also empowering. A person may not control the stock market, interest rates, or the next economic cycle. They can control what they learn, how they spend, how they sell, how they serve customers, and whether they prepare for opportunity.

Getting rich, in Cuban’s view, is not about appearing rich. It is about building the skills, cash flow, discipline, and ownership that create real options. The visible rewards may come later. The foundation begins quietly: read more, learn faster, spend less than you earn, pay off expensive debt, solve real problems, and keep adapting before the market forces you to.