The Wealth Excuse Trap: Why Financial Progress Requires More Than Wanting to Be Rich

Most people do not fail to build wealth because they make one dramatic financial mistake. They fail because small patterns repeat for years.

They spend slightly more than they earn. They delay investing. They avoid learning skills that could increase income. They set vague goals and rarely review them. They treat a paycheck as the whole plan. They fear failure so much that they never test better opportunities. They assume wealth is only for the lucky, the connected, or the already rich. They confuse saving with hoarding and earning with freedom. They make excuses that feel reasonable in the moment but become expensive over time.

Yet any honest discussion of wealth must begin with an important distinction: financial outcomes are shaped by both personal behavior and external conditions. It is too simplistic to say that most people are not rich because they lack discipline. It is also too passive to say that wealth is only luck, inheritance, or social advantage. Both views are incomplete.

People do not start from the same place. Family background, access to education, health, geography, discrimination, economic cycles, inheritance, housing costs, wages, childcare costs, and medical expenses all influence financial outcomes. Some people face obstacles that others never have to think about. At the same time, choices still matter. Saving matters. Investing matters. Skill development matters. Debt management matters. Goals matter. Discipline matters. The presence of structural barriers does not erase the power of better decisions, but better decisions also do not erase the reality of unequal starting points.

The most useful financial education lives between those extremes. It refuses to shame people for circumstances they did not choose, but it also refuses to let them surrender the parts of their financial life they can influence.

The popular list of reasons people “will never be rich” includes ideas that range from useful to exaggerated. Some are strongly supported by personal finance evidence: spending less than you earn, investing consistently, learning new skills, setting financial goals, and practicing discipline. Others need more care. A traditional 9-to-5 job can absolutely build wealth. Saving and earning are not opposites. Taking advice should depend on expertise, not whether someone looks rich. Wealth is influenced by effort and planning, but also by luck, timing, and access.

The deeper lesson is not that most people are doomed. It is that wealth rarely arrives without a system. Wanting more money is not a system. Working hard is not a system. Complaining about the economy is not a system. Hoping for a lucky break is not a system. A system means earning, spending, saving, investing, learning, protecting, and reviewing in a way that can survive real life.

The difference between financial frustration and financial progress is often the willingness to stop defending habits that are not working.

The Myth That a 9-to-5 Job Cannot Build Wealth

One of the most common motivational claims is that people fail to become rich because they believe a 9-to-5 job is the only way in life. There is a useful warning inside that statement, but it is often presented too carelessly.

A traditional job is not a wealth trap by itself. Many households build meaningful wealth through employment. They earn steady income, advance in their careers, participate in retirement plans, receive employer benefits, invest consistently, avoid destructive debt, and let compounding work for decades. A stable job can be one of the strongest wealth-building tools available when income is managed well.

The danger is not having a job. The danger is treating a job as the entire financial strategy.

A paycheck can create comfort, but it can also create dependence. If every dollar goes toward bills, debt, and lifestyle, the worker remains vulnerable. The income may be high, but the structure is fragile. A job can be lost. A company can restructure. An industry can decline. Health can change. Technology can alter the value of certain skills. A person who depends entirely on one paycheck and owns no meaningful assets has limited freedom.

The better principle is this: use employment income as a wealth engine, not just a lifestyle engine.

A 9-to-5 job can fund emergency savings, retirement contributions, diversified investments, property ownership, education, business experiments, and long-term financial security. The employee who invests automatically and increases contributions with raises may build more wealth than the entrepreneur who earns irregularly, spends heavily, and never invests. Entrepreneurship can create large upside, but it can also create losses, stress, debt, and years of unstable income.

The question is not whether employment or entrepreneurship is superior. The question is whether your income source is being converted into assets.

Career Choices Should Balance Guidance, Skill, and Opportunity

Another popular claim is that people struggle financially because they make career choices based on society, parents, or outside expectations. This can be true in some cases. A person may pursue a field they dislike because it sounds respectable. They may ignore their strengths to satisfy family pressure. They may choose status over fit. Over time, that mismatch can reduce motivation, performance, and earning potential.

But the opposite mistake is also common: assuming passion alone should guide career choices. Passion without market demand can become financial frustration. Interest matters, but so do skills, wages, growth prospects, working conditions, barriers to entry, geographic demand, and long-term opportunity.

A mature career decision sits at the intersection of four questions. What am I good at or capable of becoming good at? What work has market demand? What kind of life will this career support? What trade-offs am I willing to accept?

Family guidance is not automatically harmful. Parents may offer wisdom, stability, and perspective. But advice should be evaluated, not obeyed blindly. A parent who grew up in one economic era may not fully understand another. A respected profession may become oversupplied. A risky field may offer strong opportunities for someone with the right skills. A safe job may be less safe than it appears if the industry is shrinking.

The wealth-building career is not necessarily the one that impresses others. It is the one that develops valuable skills, produces sustainable income, offers growth, and leaves room to build assets.

Fear of Failure Can Become a Hidden Tax

Fear of failure is not irrational. Failure can be costly. A failed business can drain savings. A career change can create instability. A poor investment can lose money. A public mistake can damage confidence. Prudence matters.

The problem is when fear becomes permanent avoidance. A person may stay in a low-growth job for years because applying elsewhere feels uncomfortable. They may avoid learning a difficult skill because they do not want to feel incompetent. They may never start investing because markets feel intimidating. They may never attempt a side business because someone might criticize them. They may never negotiate because hearing “no” feels personal.

This kind of fear charges a hidden tax. It taxes income growth. It taxes confidence. It taxes opportunity. It taxes time.

Financial progress often requires intelligent risk. Intelligent risk is different from reckless risk. Reckless risk ignores downside. Intelligent risk measures it. Reckless risk bets everything on hope. Intelligent risk tests, learns, and protects the base. Reckless risk borrows heavily without a plan. Intelligent risk builds reserves, develops skills, starts small, and adjusts based on evidence.

A person does not need to quit a job tomorrow to overcome fear. They can begin with smaller actions: apply for a better role, take a course, start investing a modest amount, ask for a raise with evidence, test a freelance offer, publish work, meet people in a stronger field, or study a business model before committing capital.

The goal is not to eliminate fear. It is to stop letting fear make every decision.

Advice Should Be Judged by Evidence, Not Appearances

“Do not take advice from unsuccessful people” is a popular line because it feels obvious. Why take money advice from someone who has not built wealth?

There is a useful caution here. People often accept financial opinions from relatives, friends, coworkers, influencers, or online personalities who have no expertise and no evidence. They hear warnings about investing from people who never invested. They hear business advice from people who never built a business. They hear career advice from people who stopped learning years ago. They hear debt excuses from people trapped in debt.

But the statement is still too crude. Financial success does not automatically make someone wise. A wealthy person may have inherited money, benefited from luck, taken risks that happened to work, or succeeded in one narrow field while knowing little about your situation. A person with modest wealth may still give excellent advice if they have expertise, discipline, and evidence. A financial planner, tax professional, teacher, researcher, attorney, or experienced mentor may be valuable even if they do not display luxury.

Advice should be judged by relevance, evidence, ethics, and competence.

Ask: Does this person understand the topic? Do they have experience with situations like mine? Can they explain the risks? Do they benefit if I follow their advice? Are they selling certainty where uncertainty exists? Is their advice based on principles or anecdotes? Does it align with my goals, timeline, and risk tolerance?

Bad advice is expensive. But judging advice only by someone’s lifestyle can be expensive too.

Saving Versus Earning Is a False Choice

Many motivational finance lists criticize people for focusing on saving instead of earning. This is only half right.

Saving alone has limits. A household can reduce expenses only so far. If income is too low, rent is high, childcare is expensive, healthcare costs are unavoidable, or family obligations are heavy, saving may be extremely difficult. Increasing income can dramatically improve financial capacity. Skills, career advancement, negotiation, business ownership, consulting, side income, or relocation can expand the gap between income and expenses.

But earning alone is not enough. High income without saving becomes high consumption. Many professionals earn impressive salaries and still have little net worth because lifestyle expands as fast as income. Larger homes, newer cars, private schools, luxury travel, expensive habits, and debt payments can absorb even very large paychecks.

Wealth requires both sides: earning more and retaining more.

The gap between income and expenses is the engine of wealth. Earning more can widen the gap. Spending discipline keeps the gap from closing. Investing puts the gap to work. Without earning, the gap may be too small. Without saving, the gap disappears. Without investing, the gap may not compound.

The better rule is not “focus on earning instead of saving.” It is “increase income while preventing lifestyle inflation, then invest the surplus.”

Luck Matters, But It Is Not a Plan

Some people assume rich people simply got lucky. Others insist luck has nothing to do with wealth. Both positions are wrong.

Luck matters. The family, country, decade, health, school system, neighborhood, and economic conditions into which a person is born can influence opportunity. Timing matters. A founder may launch during a favorable technology cycle. An investor may begin during a strong market period. A homeowner may buy before a housing boom. A worker may enter a field just as demand rises. Some inherit capital, connections, or financial knowledge.

Acknowledging luck is not weakness. It is honesty.

But luck is not the whole story. Many people receive opportunities and waste them. Others start with little and build through skill, discipline, saving, investing, entrepreneurship, and persistence. Luck can open doors, but behavior often determines what happens after the door opens.

The practical lesson is to respect luck without depending on it. You cannot control whether you are born into the ideal circumstances. You cannot control market cycles. You cannot control every employer decision. But you can improve skills, reduce bad debt, invest consistently, build relationships, create savings, protect against risk, and prepare for opportunities.

Luck favors people differently. Preparation determines who can use it.

Failing to Invest Is One of the Costliest Mistakes

One of the strongest points on the list is failing to make investments. Saving money is important, but saving alone is often not enough to build long-term wealth. Inflation reduces purchasing power. Life expectancy can be long. Retirement may last decades. Large goals such as homeownership, education, business ownership, or financial independence usually require growth.

Investing allows money to participate in productive assets. Stocks represent ownership in businesses. Bonds represent lending arrangements that may pay interest. Funds provide diversified exposure. Real estate can produce rent and appreciation. Businesses can create profits and equity value. Retirement accounts may offer tax advantages depending on the jurisdiction.

The power of investing comes from compounding. Returns can generate more returns. Dividends can be reinvested. Portfolio growth can build on previous growth. The earlier and more consistently a person invests, the more time compounding has to work.

Many people avoid investing because they fear losing money. That fear is understandable. Markets fluctuate. Some investments fail. Fraud exists. Complexity can be intimidating. But refusing to invest also carries risk: the risk that savings do not grow enough to support future needs.

The answer is not reckless investing. It is educated investing. Understand your goals. Keep emergency savings separate. Avoid high-interest debt. Use diversified investments. Keep costs reasonable. Match risk to time horizon. Avoid products you do not understand. Do not chase hype. Invest consistently. Review the plan periodically.

The greatest investment mistake is often not volatility. It is never beginning.

Financial Goals Turn Vague Desire Into Direction

Not setting financial goals is another common barrier to wealth. Many people want to be “better with money,” “save more,” “get rich,” or “retire comfortably.” These phrases express desire, but they do not create direction.

A useful financial goal is specific enough to guide behavior. Build a three-month emergency fund. Pay off a credit card balance by a certain date. Invest a percentage of income each month. Increase retirement contributions after every raise. Save for a home deposit. Build a business reserve. Reach a certain net worth. Become debt-free except for a mortgage. Create an estate plan. Fund education accounts. Replace a percentage of employment income with asset income.

Goals help because they create trade-offs. Without a goal, every purchase competes equally. With a goal, money has priority. The question changes from “Can I afford this?” to “Does this move me closer to what I said matters?”

Goals also create feedback. A person can measure progress. Is the debt falling? Is the emergency fund growing? Are investments increasing? Is income improving? Is net worth rising? Without measurement, people often rely on feelings. Feelings can mislead. A person may feel broke while making progress or feel successful while debt rises.

Financial goals should be reviewed regularly. Life changes. Income changes. Family needs change. Markets change. Goals are not prison bars. They are navigation tools.

Spending More Than You Earn Blocks Wealth at the Source

Spending more than you earn is one of the most direct paths to financial fragility. It creates debt, drains savings, and prevents investment. If the pattern continues long enough, it can trap a household in permanent payment mode.

Overspending can happen at every income level. A low-income household may overspend because essentials exceed income. A middle-income household may overspend because lifestyle expectations are high. A high-income household may overspend because large income creates confidence and access to credit. In every case, the arithmetic eventually matters.

Persistent overspending turns future income into repayment for past decisions. Credit cards, personal loans, car loans, buy-now-pay-later plans, and lifestyle debt all reduce future flexibility. The borrower may still earn money, but part of each paycheck already belongs to lenders.

The solution begins with visibility. Know monthly income. Know fixed expenses. Know debt payments. Know interest rates. Know what is essential and what is discretionary. Many people avoid these numbers because they fear shame. But shame does not fix money. Clarity does.

Once the numbers are visible, the household can decide whether the main problem is income, spending, debt, or all three. Some households need expense cuts. Some need income growth. Some need debt restructuring or professional help. Some need a temporary austerity period. Some need to stop using credit while rebuilding cash reserves.

Wealth cannot grow if every month moves backward.

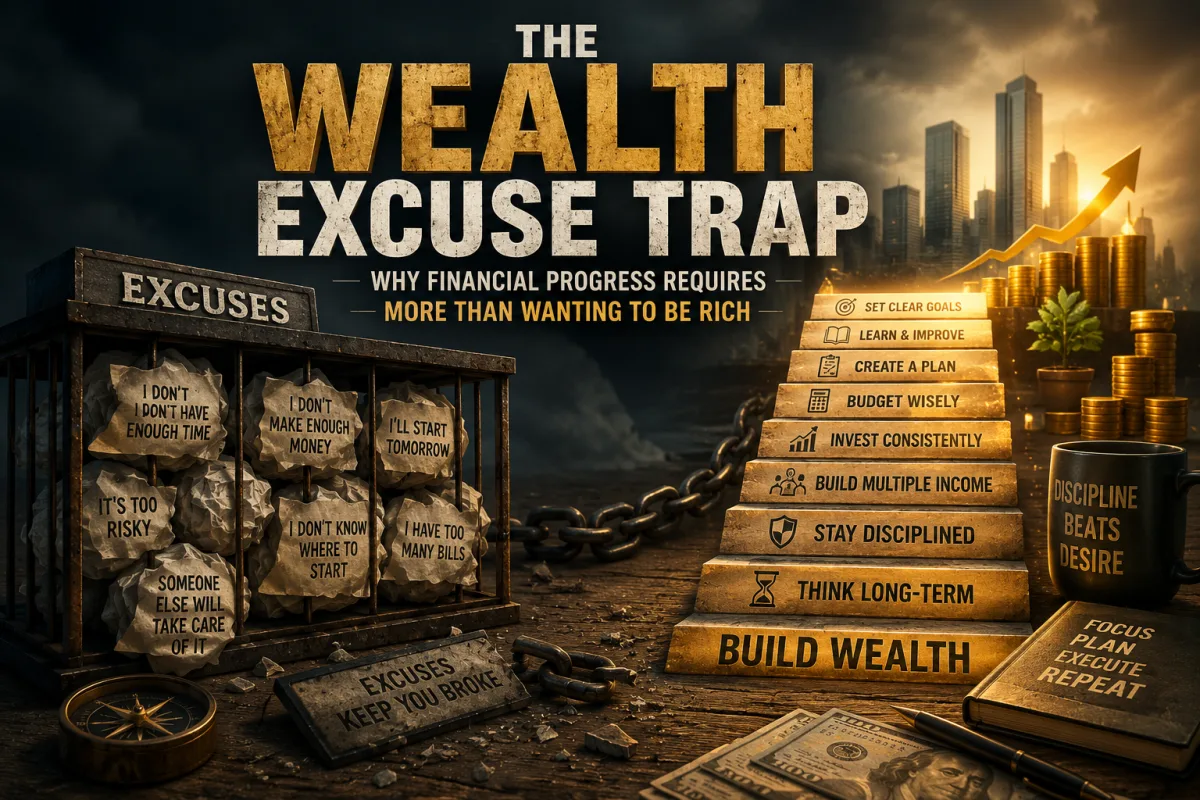

Excuses Feel Safe, But They Preserve the Problem

“Constantly making excuses” is a harsh phrase, but it points to a real behavioral pattern. People often protect themselves from discomfort by explaining why change is impossible.

Some excuses are not excuses at all. They are real constraints. Low wages, illness, caregiving, job loss, discrimination, debt from emergencies, and high housing costs can materially limit choices. A serious financial framework must acknowledge this.

But there is also a category of explanation that becomes self-protection. “I will start investing when I earn more.” “I am just not good with money.” “The market is rigged.” “People like me cannot build wealth.” “I deserve to spend because I work hard.” “I will save next month.” “It is too late to start.” “I do not have time to learn.” “Everyone has debt.”

These thoughts may contain pieces of truth, but they can become permission to stay still.

The antidote is not blind positivity. It is responsibility for the next controllable action. If you cannot invest much, can you invest a small amount? If you cannot pay off all debt, can you stop adding to it? If you cannot change careers immediately, can you learn one skill? If you cannot build a six-month emergency fund, can you build the first $500? If you cannot solve everything, can you solve one thing?

Excuses often focus on the size of the whole mountain. Progress begins with the next step.

Not Learning New Things Is Financially Dangerous

The economy rewards useful learning. Skills become outdated. Industries change. Technology alters work. New tools appear. Old business models weaken. Financial products become more complex. Scams become more sophisticated. A person who stops learning becomes economically exposed.

Learning does not always require formal education. It may involve certifications, apprenticeships, reading, practice, mentorship, online courses, workplace training, professional associations, financial literacy, or deliberate experience. The key is that learning must improve capability.

Valuable learning usually falls into three categories. First, career skills that increase earning power. Second, financial skills that improve money decisions. Third, life skills that reduce costly mistakes.

Career skills may include technical expertise, communication, sales, leadership, coding, data analysis, project management, design, trade skills, healthcare knowledge, financial analysis, writing, negotiation, or operations. Financial skills include budgeting, debt, investing, taxes, insurance, retirement planning, estate planning, and risk management. Life skills include decision-making, emotional regulation, time management, health habits, and relationship management.

Learning creates adaptability. Adaptability creates options. Options create freedom.

The danger is confusing information consumption with learning. Watching financial videos, reading motivational posts, or following market commentary can feel productive, but if behavior does not change, little has been learned. Real learning shows up in better decisions, higher income, lower debt, stronger investments, improved negotiation, or greater resilience.

Self-Discipline Is the Bridge Between Knowledge and Wealth

Most people know more than they practice. They know they should save. They know they should invest. They know high-interest debt is harmful. They know skills matter. They know lifestyle inflation is dangerous. They know goals are useful. Knowledge is not the bottleneck. Discipline often is.

Self-discipline is not about being harsh or joyless. It is the ability to act in alignment with long-term interests despite short-term temptation. In finance, it means spending less than you earn, investing regularly, resisting unnecessary debt, reviewing progress, improving skills, and staying patient when results are slow.

Discipline becomes easier when supported by systems. Automatic savings reduce the need for willpower. Payroll retirement contributions happen before money reaches the spending account. Separate accounts create boundaries. Written goals create clarity. Debt payoff plans create sequence. Budget reviews create awareness. Investment policies reduce emotional trading. Accountability partners or advisers can help maintain direction.

The best financial discipline is not constant self-denial. It is designing a life where good decisions happen by default.

Discipline also includes recovery. No one makes perfect financial decisions forever. A disciplined person can make a mistake, learn from it, and return to the plan. An undisciplined person uses one mistake as proof that the plan has failed.

The Missing Factors: What Motivational Lists Often Ignore

Lists about why people will never be rich often focus on mindset and behavior. Those matter, but they are not the whole story. Serious wealth analysis must include factors outside individual control.

Access to quality education can shape lifetime income. Health and disability can determine earning capacity and expenses. Recessions can damage careers and portfolios. Geographic location affects wages, housing costs, taxes, and opportunity. Family responsibilities can reduce savings capacity. Childcare costs can reshape career choices. Discrimination can limit income and access. Medical expenses can destroy savings. Housing affordability can determine whether a household can build equity or remain rent-burdened. Family wealth can provide down payments, education support, business capital, and emergency help.

These factors do not mean individual action is meaningless. They mean the path is not equally steep for everyone.

Financial education should empower without blaming. It should say: here are the habits that improve your odds, and here are the realities that may affect your path. It should teach people how to increase control while recognizing that not everything is controllable.

The Balanced Framework for Building Wealth

A more evidence-based wealth framework begins with earning more than you spend. This creates the surplus that funds everything else. Without surplus, financial progress is difficult.

Next, build an emergency fund. Emergency savings reduce dependence on credit and protect long-term plans from short-term shocks. The right amount depends on job stability, household size, income variability, and obligations.

Then avoid or eliminate high-interest consumer debt. Debt that compounds against you can overwhelm even strong income. Paying it down can create an immediate improvement in cash flow and reduce stress.

Invest consistently in diversified assets. Investments allow savings to grow and participate in productive economic activity. Consistency matters because market timing is difficult, and compounding needs time.

Increase skills and earning potential. Income growth expands the wealth-building gap. Valuable skills also create career resilience.

Set measurable financial goals. Goals turn desire into direction and provide feedback.

Protect assets with insurance, legal planning, and estate documents. Wealth that is not protected can be lost through illness, liability, death, disability, fraud, or family confusion.

Think long term. Wealth usually grows through repeated actions over many years. Patience allows compounding to work.

Review and adjust. A plan should change as income, family, markets, health, and goals change.

The Role of Ownership

One of the largest differences between people who build wealth and people who remain financially fragile is ownership. Ownership means holding assets that can grow, pay income, or create value beyond direct labor.

A paycheck pays for work. Assets can pay because capital is working. A worker may earn income from one employer. An investor owns small pieces of many businesses. A landlord owns property that may generate rent. A business owner owns systems and customer relationships. A creator may own intellectual property. A retiree may live partly from portfolio withdrawals, dividends, interest, rent, or business proceeds.

Ownership is not risk-free. Assets can decline. Businesses can fail. Properties can become expensive. Markets can disappoint. But without ownership, a person remains almost entirely dependent on labor income.

The wealth-building goal is to convert a portion of income into ownership every month or every year. At first, the amount may be small. Over time, the ownership base can grow. Eventually, assets may begin to support the household alongside employment income. That is when financial freedom becomes more realistic.

Why High Income Still Fails Without Habits

Many people believe that if they simply earned more, their financial problems would disappear. Sometimes that is true. More income can be life-changing, especially for households struggling with basic expenses. But after a certain point, income alone is not enough.

High earners can remain broke because spending rises with income. They buy larger homes, expensive cars, luxury experiences, private services, and status goods. They may borrow against future income because lenders trust their salary. They may assume the income will continue indefinitely. They may delay saving because they believe they can catch up later.

The result is a high-income trap. The household looks wealthy but has little flexibility. Job loss becomes terrifying. Retirement is underfunded. Debt payments are large. The lifestyle is expensive to maintain.

This is why the basics matter at every income level. Spend less than you earn. Invest consistently. Avoid destructive debt. Keep emergency reserves. Protect assets. Increase skills. Review goals. These habits do not become unnecessary when income rises. They become more powerful.

Why Low Income Requires a Different Starting Point

For lower-income households, the advice must be practical. Telling someone to invest aggressively when they cannot cover rent is not useful. The first priority may be stabilization: secure income, essential expenses, benefits, debt relief, transportation, childcare support, health needs, and emergency cash.

The first financial win may be small. Avoiding one overdraft fee. Building a small emergency buffer. Reducing one high-interest balance. Increasing work hours. Applying for a better job. Learning a skill. Using community resources. Avoiding a predatory loan. Opening a retirement account with a small contribution. These actions may not look like wealth, but they create movement.

Small progress matters because it changes trajectory. A person who builds a $500 emergency fund is less likely to borrow for a minor crisis. A person who pays off one debt frees future cash flow. A person who learns a marketable skill can raise income. A person who invests small amounts begins the habit.

The wealth-building principles still apply, but the order and pace must respect reality.

The Danger of Financial Cynicism

Cynicism can feel intelligent. It says the system is unfair, rich people are lucky, investing is rigged, employers exploit workers, and ordinary people cannot get ahead. Sometimes cynicism points to real problems. Markets are not perfectly fair. Opportunity is unequal. Some people do exploit others. Some financial products are harmful. Some employers underpay. Some systems reward inherited advantage.

But cynicism becomes dangerous when it turns into paralysis. If everything is rigged, why save? If rich people are only lucky, why learn? If investing is impossible, why start? If effort does not matter, why improve?

A better stance is clear-eyed agency. See the obstacles. Study the system. Avoid scams. Recognize luck. Understand inequality. Then act where action is possible.

Cynicism protects the ego from disappointment, but it also protects bad habits from challenge.

The Wealth Builder’s Mindset

A wealth builder does not necessarily believe everything is easy. They believe progress is worth pursuing. They ask better questions.

Instead of “Why is this impossible?” they ask, “What part is controllable?” Instead of “How do I look successful?” they ask, “How do I become financially stronger?” Instead of “How can I afford the payment?” they ask, “What does this do to my future cash flow?” Instead of “What stock will make me rich?” they ask, “What investment plan can I follow for decades?” Instead of “Why did they get lucky?” they ask, “What can I learn from their path without ignoring their advantages?”

This mindset is practical, not magical. It does not assume thoughts create money. It assumes thoughts guide behavior, and behavior repeated over time shapes financial outcomes.

What to Avoid

Avoid believing a job is the enemy of wealth. A job can be a powerful funding source if income is managed well. Avoid choosing a career only for approval while ignoring skills, demand, and personal fit. Avoid letting fear of failure become a reason to avoid all risk. Avoid taking financial advice from people without expertise, evidence, or understanding of your circumstances. Avoid treating earning and saving as opposites. Avoid assuming wealth is only luck. Avoid failing to invest because markets feel intimidating.

Avoid vague goals. Avoid spending more than you earn. Avoid making excuses that protect habits you know are harmful. Avoid letting your skills become outdated. Avoid relying on motivation instead of systems. Avoid judging yourself harshly for past mistakes. Shame is less useful than a plan.

What to Do

Build a clear financial picture. Know your income, expenses, debts, assets, and net worth. Create a gap between income and spending. Build emergency savings. Pay down high-interest debt. Invest consistently in diversified assets suited to your goals and time horizon. Increase your skills and earning power. Set measurable financial goals. Review progress monthly or quarterly. Protect your household with appropriate insurance and estate planning. Let raises increase your savings rate, not only your lifestyle.

Choose advice carefully. Learn from people with expertise, evidence, and integrity. Study those who have built wealth, but do not copy blindly. Their circumstances may differ from yours.

Take intelligent risks. Apply for better roles. Learn valuable skills. Start small experiments. Invest steadily. Build relationships. Improve your ability to solve valuable problems. Protect the downside while expanding the upside.

The Real Reason Many People Do Not Build Wealth

Most people do not miss wealth because of one flaw. They miss it because their financial system is not designed to produce wealth.

Their income is not intentionally increased. Their spending is not intentionally controlled. Their savings are not automatic. Their investments are delayed. Their debt is normalized. Their skills are not upgraded. Their goals are vague. Their risks are uninsured. Their estate plans are absent. Their habits depend on motivation. Their excuses go unchallenged.

Change the system, and the outcome can begin to change.

Not everyone will become rich. That is an honest statement. Income, time, health, obligations, opportunity, markets, and luck all vary. But more people can become financially stronger than they are today. More people can reduce debt, increase savings, own assets, improve skills, invest consistently, and create options. More people can move from financial reaction to financial control.

The goal is not to worship wealth or blame those who struggle. The goal is to understand that financial progress requires both realism and responsibility.

The Quiet Path Forward

The path to wealth is often quieter than motivational posters suggest. It is not always quitting a job, ignoring parents, taking wild risks, or proving doubters wrong. Sometimes it is less dramatic: tracking spending, negotiating a raise, learning a skill, opening an investment account, paying off a credit card, building an emergency fund, reading better books, choosing a lower-cost car, increasing retirement contributions, or refusing to inflate lifestyle after a raise.

These actions do not create instant riches. They create direction. Direction repeated becomes momentum. Momentum sustained becomes wealth.

The people who make financial progress usually stop waiting for perfect conditions. They begin with the next controllable step. They accept that luck exists but do not build a life around waiting for it. They acknowledge obstacles but do not let obstacles become identity. They learn. They invest. They protect. They adjust. They continue.

Wealth is not guaranteed. But financial stagnation becomes far more likely when people overspend, avoid investing, stop learning, ignore goals, and excuse every delay.

The future is shaped by systems. Build one that gives your money a chance to grow.