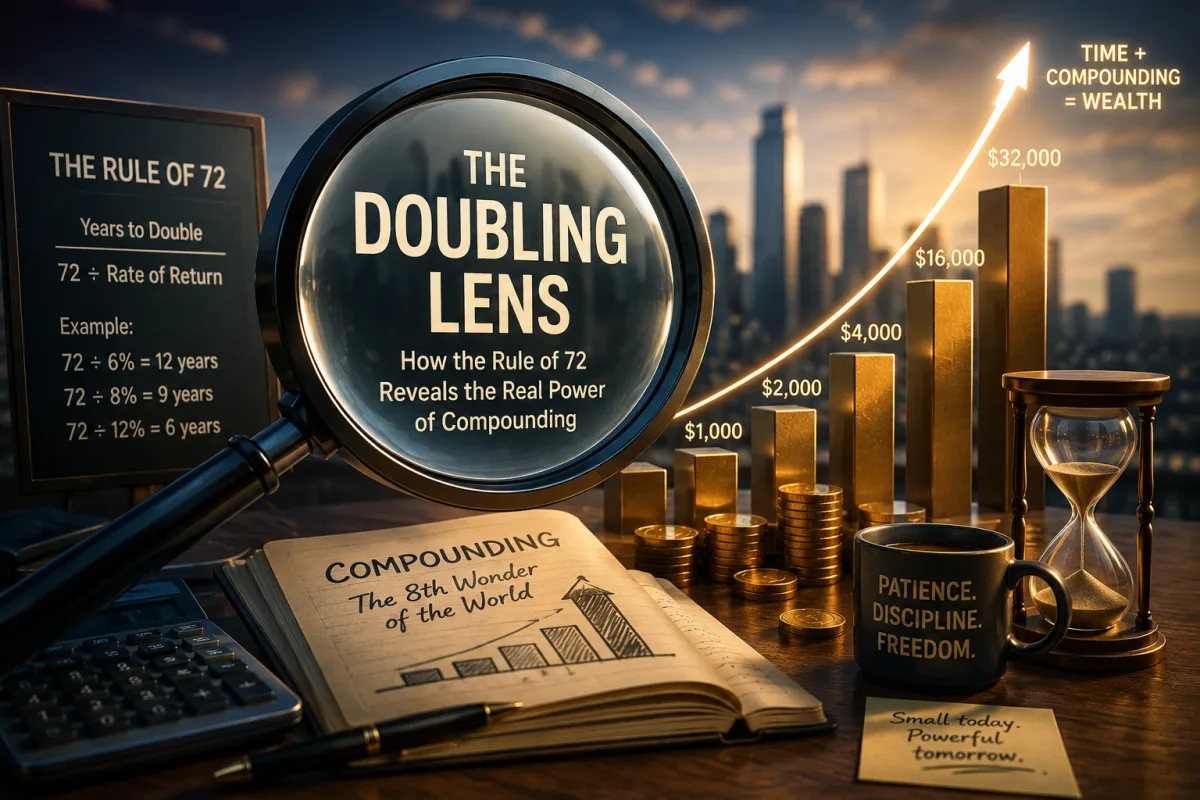

The Doubling Lens: How the Rule of 72 Reveals the Real Power of Compounding

The Rule of 72 is one of the simplest ideas in finance, but it explains one of the most powerful forces in wealth building.

It answers a question every investor eventually asks: how long will it take for my money to double?

The formula is easy. Divide 72 by the annual rate of return. The answer is the approximate number of years it takes money to double.

If an investment earns 6 percent per year, 72 divided by 6 equals 12. The money doubles in about 12 years. If it earns 8 percent, 72 divided by 8 equals 9. The money doubles in about 9 years. If it earns 12 percent, 72 divided by 12 equals 6. The money doubles in about 6 years.

This is why the Rule of 72 is so memorable. It turns compound interest from an abstract formula into a mental picture. It lets a saver, investor, borrower, business owner or retiree quickly estimate the impact of time and return without opening a spreadsheet.

But the Rule of 72 is more than a shortcut. It is a way of seeing money.

It shows why small differences in returns become large differences over time. It shows why starting early matters. It shows why inflation quietly cuts purchasing power. It shows why high-interest debt is dangerous. It shows why patient investing can build wealth without spectacular annual returns. It also shows why the promise of fast doubling should always be treated carefully.

Money that doubles every 12 years behaves very differently from money that doubles every 6 years. Debt that doubles every few years behaves even more dangerously. Prices that double over time reduce purchasing power even if the bank balance looks unchanged. The Rule of 72 helps reveal these hidden realities.

For beginners, the rule is a doorway into compounding. For experienced investors, it is a quick test of assumptions. For anyone managing money, it is a reminder that time and rate of return are not minor details. They are the engine.

What the Rule of 72 Means

The Rule of 72 is a simple approximation used to estimate how long it takes an amount of money to double at a fixed annual rate of return.

The formula is:

Years to double equals 72 divided by annual return percentage.

If the annual return is 4 percent, the doubling time is about 18 years. If the annual return is 6 percent, the doubling time is about 12 years. If the annual return is 9 percent, the doubling time is about 8 years. If the annual return is 10 percent, the doubling time is about 7.2 years.

The rule can also be reversed. If you want to know what return is required to double money in a certain number of years, divide 72 by the number of years.

To double money in 12 years, the approximate required return is 6 percent. To double money in 9 years, the required return is about 8 percent. To double money in 6 years, the required return is about 12 percent.

This simplicity is the reason the rule has lasted. It gives a quick estimate of compounding without requiring detailed calculations.

The Rule of 72 assumes the return is compounded annually and remains stable. Real investments rarely behave so neatly. Stock market returns fluctuate. Interest rates change. Dividends vary. Inflation moves. Fees and taxes reduce net returns. But as a mental model, the rule is useful because it shows direction and scale quickly.

The purpose is not exact precision. The purpose is insight.

Why the Rule Works

The Rule of 72 works because of compounding.

Compounding happens when returns are added to the original amount and future returns are earned on both the original amount and previous returns. In simple interest, money grows only on the original principal. In compound interest, money grows on a growing base.

Imagine investing $1,000 at 8 percent per year. In the first year, the investment earns $80. The next year, the return is earned on $1,080, not only on the original $1,000. The process continues. Over time, the investment begins to grow faster in dollar terms because the base is larger.

The Rule of 72 compresses that compounding process into a quick estimate.

At 8 percent, the rule says money doubles in about 9 years. That means $1,000 becomes roughly $2,000 in 9 years, $4,000 in 18 years, $8,000 in 27 years and $16,000 in 36 years, assuming the return is sustained and no money is withdrawn.

This is the deeper lesson. The first doubling may feel slow. Later doublings become more powerful because the amount being doubled is larger. Doubling $1,000 adds $1,000. Doubling $100,000 adds $100,000. The rate may be the same, but the dollar impact grows.

Compounding rewards time, consistency and patience.

The Rule of 72 in Action

Consider several annual return rates.

At 3 percent, money doubles in about 24 years. At 4 percent, it doubles in about 18 years. At 6 percent, it doubles in about 12 years. At 8 percent, it doubles in about 9 years. At 10 percent, it doubles in about 7.2 years. At 12 percent, it doubles in about 6 years. At 18 percent, it doubles in about 4 years.

These estimates show why return matters. A portfolio earning 4 percent doubles much more slowly than one earning 8 percent. A 4 percent return may be suitable for lower-risk or shorter-term money, but it cannot produce the same long-term growth as a higher-return investment unless contributions are much larger or the time horizon is longer.

But the table also shows why risk matters. Higher returns are not free. An investment promising 18 percent annually may double money quickly if successful, but it may involve much higher risk, volatility, illiquidity, leverage, business uncertainty or fraud risk. The Rule of 72 tells you how fast money could double. It does not tell you whether the return is realistic or safe.

A useful shortcut becomes dangerous when it is used without judgment.

How the Rule of 72 Helps Beginners Understand Investing

Beginners often think of investing only in terms of annual returns.

They hear that an investment may earn 5 percent, 8 percent or 10 percent per year, but the numbers can feel abstract. The Rule of 72 translates those rates into time. This makes the effect of returns easier to understand.

A 6 percent return does not sound dramatic. But if sustained, it can double money roughly every 12 years. Over 36 years, that can mean three doublings. One dollar becomes about eight dollars before fees and taxes. A 9 percent return doubles in about 8 years. Over 32 years, that can mean four doublings. One dollar becomes about sixteen dollars.

This does not mean investors should chase the highest number. It means they should respect the relationship between return and time.

A beginner who starts investing early with moderate returns may build more wealth than someone who starts late and tries to catch up with aggressive risk. Time reduces the need for heroic returns. Delay increases pressure.

The Rule of 72 helps make this visible. It shows that wealth building does not require doubling money every year. It requires letting reasonable returns compound long enough.

Starting Early Changes the Entire Equation

The Rule of 72 explains why starting early is so valuable.

Suppose two people invest at an average return of 8 percent per year. According to the Rule of 72, money doubles about every 9 years. A person who invests for 36 years gets about four doubling periods. A person who invests for 18 years gets about two doubling periods.

The difference is enormous.

If $10,000 is invested for 36 years at 8 percent, four approximate doublings can turn it into about $160,000 before costs and taxes. If the same $10,000 is invested for 18 years, two approximate doublings turn it into about $40,000. The return rate is the same. The difference is time.

This is why young investors have an advantage even when they start with small amounts. They have more years for money to double. A person who starts later can still build wealth, but they may need higher contributions, longer working years, lower expenses or more aggressive saving to compensate for lost time.

Starting early is not about perfection. It is about giving compounding enough years to matter.

The Rule of 72 and Regular Contributions

The Rule of 72 is easiest to understand when applied to a lump sum. But most people build wealth through regular contributions, not one single investment.

If someone invests a fixed amount every month, each contribution has its own doubling timeline. The first contribution has the longest time to compound. Later contributions have less time, but they still add to the growing base. Over decades, the combination of contributions and compounding can become powerful.

This is why automatic investing works. It adds new money consistently while old money compounds. The investor does not need to wait until they have a large sum. They can build the base gradually.

The Rule of 72 still helps because it gives a sense of how each invested amount may grow over time. A contribution invested at 8 percent may double in about 9 years. Contributions made early in a career may double several times before retirement.

Regular contributions provide the fuel. Compounding provides the multiplier.

How Inflation Uses the Rule of 72 Against You

The Rule of 72 is not only for investments. It can also show how inflation erodes purchasing power.

Inflation means prices rise over time. If prices rise at 6 percent per year, the Rule of 72 suggests that prices may double in about 12 years. If inflation averages 8 percent, prices may double in about 9 years. If inflation averages 3 percent, prices may double in about 24 years.

This matters because money sitting still loses purchasing power when prices rise. A bank balance may look unchanged, but what it can buy declines. If prices double and your money does not grow, your purchasing power is cut roughly in half.

Inflation is one reason long-term money usually needs to be invested. Cash is necessary for emergencies and short-term goals, but cash alone may not protect wealth over decades. Investments must aim not only to grow nominally, but to grow faster than inflation after taxes and fees.

The Rule of 72 makes inflation easier to feel. A 6 percent inflation rate is not just a number. It is a force that can double living costs in about 12 years.

The Rule of 72 and Debt

The Rule of 72 can also reveal the danger of high-interest debt.

If a credit card balance grows at 24 percent annually, 72 divided by 24 equals 3. That means unpaid debt could roughly double in about 3 years if interest compounds and payments are insufficient. At 18 percent, debt doubles in about 4 years. At 12 percent, it doubles in about 6 years.

This is why high-interest debt is so destructive. The same compounding that can build wealth through investments can destroy wealth through debt.

A borrower may focus on the minimum payment and ignore the rate. But the rate determines how aggressively the debt grows. If payments barely cover interest, progress is slow. If new borrowing continues, the debt may keep expanding.

The Rule of 72 helps borrowers see debt as an investment in reverse. The lender earns the return. The borrower pays it.

Paying off high-interest debt can therefore be one of the strongest financial moves available. It stops compounding from working against you and frees future income for saving and investing.

The Rule of 72 and Fees

Fees reduce returns, and the Rule of 72 shows how much that matters.

Suppose one investment earns 8 percent before fees and another earns 6 percent after higher costs. At 8 percent, money doubles in about 9 years. At 6 percent, it doubles in about 12 years. That three-year difference may not sound large once, but over a lifetime it can significantly reduce wealth.

Investment fees, advisory fees, fund expense ratios, platform fees, transaction costs and tax inefficiencies all reduce the net return investors actually keep. The Rule of 72 should be applied to net returns, not headline returns.

An investor who earns 10 percent before fees but keeps 7 percent after costs is not doubling at the 10 percent rate. They are doubling at the 7 percent rate, which is about 10.3 years.

This does not mean every fee is bad. Good advice, tax planning, risk management and professional service can be worth paying for. But every fee should justify itself. Unnecessary costs slow compounding.

The Rule of 72 and Taxes

Taxes also affect doubling time.

An investment may earn 8 percent before tax. But if taxes reduce the return to 6 percent, the approximate doubling time changes from 9 years to 12 years. This is a major difference over decades.

Tax treatment depends on the country, account type, investment type and investor circumstances. Dividends, interest, rent, capital gains and business profits may all be taxed differently. Some retirement accounts or tax-advantaged accounts allow money to grow tax-deferred or tax-free under specific rules. These structures can improve long-term compounding.

The lesson is not to avoid taxes illegally. It is to plan intelligently. Net return after fees, taxes and inflation is what determines real wealth growth.

The Rule of 72 becomes more useful when applied to what the investor actually keeps.

Nominal Return Versus Real Return

Nominal return is the return before adjusting for inflation. Real return is the return after inflation.

If an investment earns 8 percent and inflation is 4 percent, the real return is roughly 4 percent before considering taxes and fees. The investment balance may grow, but purchasing power grows more slowly.

The Rule of 72 can estimate both nominal and real doubling. At an 8 percent nominal return, money doubles in about 9 years. At a 4 percent real return, purchasing power doubles in about 18 years.

This distinction is critical for long-term planning. A person may feel wealthier because the account balance rises, but if living costs rise nearly as fast, real progress is smaller.

Retirement planning, education planning and financial independence planning should focus on real purchasing power. The goal is not only to have more money in name. The goal is to afford more life in reality.

Why Faster Doubling Is Not Always Better

The phrase “double your money faster” can be dangerous.

Everyone wants money to double quickly. But the only ways to increase doubling speed are higher returns, more frequent compounding, more contributions, leverage or accepting more risk. Some of these are useful. Others can be destructive.

A diversified investment portfolio may earn higher long-term returns than cash because it accepts market risk. A business may generate high returns because the owner accepts operational risk. A rental property may build equity through leverage, but debt increases vulnerability. A speculative scheme may promise fast doubling because the risk is hidden or the promise is false.

The Rule of 72 should therefore be used as a reality check. If someone promises to double money in 2 years, the implied return is about 36 percent per year. If they promise doubling in 1 year, the implied return is 72 percent. Those returns may be possible in rare business situations, but they are not normal low-risk returns.

When promised returns are unusually high, ask why. What risk is being taken? Is the return guaranteed? Who guarantees it? Is the investment regulated? How does it generate cash? Can capital be lost? Can money be withdrawn? What fees apply? What happens in a bad market?

Fast doubling is attractive. Sustainable compounding is more important.

The Rule of 72 and Business Growth

The Rule of 72 can help business owners think about growth rates.

If a business grows revenue at 12 percent per year, revenue may double in about 6 years. If profit grows at 18 percent per year, profit may double in about 4 years. If expenses grow at 24 percent per year while revenue grows at 12 percent, cost pressure can become dangerous quickly.

Business owners can use the rule to evaluate whether growth targets are realistic. A company expecting to double sales in 3 years needs an approximate annual growth rate of 24 percent. That may require new customers, pricing power, expansion capital, staff, systems, inventory and execution. The rule turns ambition into a measurable requirement.

It can also reveal expense risks. If rent, payroll, marketing costs or debt service grow faster than revenue, profitability can shrink. A business may be growing and still becoming weaker if costs compound faster than income.

For entrepreneurs, the Rule of 72 is not only about investments. It is about understanding how growth rates shape business value and risk.

The Rule of 72 and Salary Growth

The Rule of 72 can also apply to personal income growth.

If salary grows at 3 percent per year, it doubles in about 24 years. If income grows at 6 percent per year, it doubles in about 12 years. If income grows at 10 percent per year through promotions, skills, business growth or career moves, it doubles in about 7.2 years.

This shows why skill development matters. A person who increases earning power faster can create more surplus for saving and investing. But income growth only builds wealth if spending does not rise equally.

If income doubles and lifestyle doubles, wealth may not improve. If income doubles and expenses rise modestly, the surplus can expand dramatically. That surplus can then buy assets.

The Rule of 72 reveals the power of income growth, but discipline determines whether the growth becomes wealth.

How to Use the Rule in Retirement Planning

Retirement planning depends heavily on compounding, inflation and withdrawal needs.

A younger investor can use the Rule of 72 to estimate how many doubling periods remain before retirement. If they are 30 years from retirement and expect a 7 percent return, money may double roughly every 10.3 years. That allows nearly three doubling periods. A $50,000 portfolio could become approximately $400,000 before additional contributions, fees, taxes and market variation are considered.

A person closer to retirement has fewer doubling periods. This does not mean retirement planning is hopeless. It means contributions, savings rate, expense control, asset allocation and retirement timing become more important.

Inflation should also be included. If living costs double every 18 years at 4 percent inflation, retirement expenses may be much higher than today’s expenses. A retirement plan based only on current prices may underestimate future needs.

The Rule of 72 helps retirement savers see both sides: investments can double, but costs can double too.

How to Use the Rule for Education Planning

Education costs can rise over time, and the Rule of 72 can help families plan.

If education costs rise at 6 percent per year, they may double in about 12 years. A parent with a young child should not assume today’s school or university costs will remain unchanged. The longer the timeline, the more inflation matters.

Investment returns can help offset rising costs, but the investment strategy should match the time horizon. Money needed in one year should be safer than money needed in fifteen years. As the education date approaches, reducing volatility may become important.

The Rule of 72 provides a quick estimate of both cost growth and investment growth. It helps families understand why early saving matters and why education funds should not be built from hope alone.

How to Use the Rule for Property Investing

Property investors often think in terms of appreciation and rental income.

If property values grow at 6 percent per year, the Rule of 72 suggests values may double in about 12 years. If rents grow at 4 percent per year, rents may double in about 18 years. If maintenance costs grow faster than rent, cash flow may weaken.

This can help investors test assumptions. A property promoter may claim that values will double in 5 years. The implied annual growth rate is about 14.4 percent. That may be possible in a booming location, but it should not be accepted casually. The investor should ask what would drive such growth: infrastructure, population demand, income growth, zoning changes, scarcity, credit expansion or speculation.

Property also includes leverage. If a mortgage is used, returns on equity can be magnified. But leverage increases risk if rent falls, interest rates rise, vacancy occurs or repairs are higher than expected.

The Rule of 72 can help estimate growth, but property investing still requires full cash-flow analysis.

The Limits of the Rule of 72

The Rule of 72 is useful, but it has limits.

First, it assumes a constant annual return. Real investments fluctuate. A stock portfolio may gain 20 percent one year, lose 15 percent the next, and grow 8 percent after that. The average return may be useful, but actual doubling time depends on the sequence of returns.

Second, the rule is an approximation. It is most accurate for moderate return rates and less precise at very low or very high rates. It gives a useful estimate, not a guarantee.

Third, it ignores contributions and withdrawals. Most investors add money regularly. Retirees withdraw money. Businesses reinvest or distribute profits. These cash flows change results.

Fourth, it ignores fees, taxes and inflation unless you adjust the return. A headline return may look attractive, but the real after-tax return may double purchasing power much more slowly.

Fifth, it does not measure risk. Two investments may both offer 10 percent expected returns, but one may be far riskier than the other. The Rule of 72 only estimates doubling time if the return occurs.

A good financial shortcut should inform judgment, not replace it.

How to Double Money Faster Safely

There is no risk-free way to double money quickly, but there are responsible ways to improve long-term doubling potential.

The first is to start earlier. More time creates more doubling periods.

The second is to invest consistently. Regular contributions increase the base that can compound.

The third is to choose an asset allocation appropriate for long-term growth. Money held entirely in cash may double slowly. Diversified growth assets may increase long-term return potential, though they bring volatility.

The fourth is to reduce fees. Lower costs improve net returns.

The fifth is to use tax-advantaged accounts where legally available and appropriate.

The sixth is to reinvest dividends, interest and distributions during the accumulation phase.

The seventh is to increase income and invest part of every raise.

The eighth is to avoid destructive debt so compounding works for you rather than against you.

The ninth is to diversify. Avoid losing years of progress through concentration in one failed asset.

The tenth is to stay disciplined during market declines. Panic selling interrupts compounding.

The responsible way to double money faster is not to chase impossible promises. It is to improve the inputs that drive compounding while managing risk.

Examples of Doubling Paths

Consider three investors who each begin with $10,000 and make no additional contributions.

At 4 percent per year, the Rule of 72 suggests the money doubles every 18 years. After 36 years, two doublings could turn $10,000 into about $40,000.

At 8 percent per year, the money doubles every 9 years. After 36 years, four doublings could turn $10,000 into about $160,000.

At 12 percent per year, the money doubles every 6 years. After 36 years, six doublings could turn $10,000 into about $640,000.

The differences are enormous, but they should be interpreted carefully. A 12 percent return is harder to sustain and may come with more risk. A 4 percent return may be more stable but grows slowly. The right choice depends on goals, time horizon and risk tolerance.

Now add regular contributions, and the results become stronger. The Rule of 72 does not calculate those contributions directly, but it helps explain why each early contribution matters. Every amount invested begins its own doubling journey.

The Rule of 72 as a Mindset Tool

The greatest value of the Rule of 72 may be psychological.

It encourages long-term thinking. Instead of seeing investing as a one-year contest, the investor begins seeing wealth in doubling periods. A decade becomes meaningful. Two decades become powerful. Three decades become transformative.

It also discourages financial laziness. If cash earns little while inflation rises, the rule reveals how purchasing power can be lost. If debt carries high interest, the rule shows how quickly liabilities can grow. If fees reduce returns, the rule shows how compounding slows.

The rule also creates healthy skepticism. Any promise of fast doubling should trigger questions. What return is implied? What risk is involved? Is the investment legitimate? Who benefits if I believe this promise?

Used well, the Rule of 72 makes money less mysterious. It turns time and return into something understandable.

Common Mistakes When Using the Rule of 72

The first mistake is treating it as exact. It is an estimate, not a contract.

The second mistake is applying it to gross returns instead of net returns. Fees, taxes and inflation matter.

The third mistake is ignoring risk. A high return may double money quickly only if capital survives.

The fourth mistake is assuming returns are stable. Real investments fluctuate.

The fifth mistake is forgetting contributions. Regular investing changes the final outcome.

The sixth mistake is using the rule to justify speculation. A promised doubling period is meaningless if the investment is unsafe or fraudulent.

The seventh mistake is ignoring inflation. Doubling the account balance is not the same as doubling purchasing power.

The eighth mistake is delaying action because the first doubling seems slow. The first doubling often feels slow, but later doublings become more powerful.

Final Thoughts

The Rule of 72 is simple enough to learn in a minute, but deep enough to change how a person thinks about money.

It shows that a 6 percent return can double money in about 12 years. An 8 percent return can double money in about 9 years. A 12 percent return can double money in about 6 years. It also shows that inflation can double prices, fees can slow growth and high-interest debt can double liabilities with frightening speed.

The rule is not a magic formula. It does not guarantee returns. It does not remove risk. It does not replace diversification, cash-flow planning, tax awareness, investment research or professional judgment. But it gives a clear mental model for the relationship between return and time.

For investors, the lesson is to start early, invest consistently, keep costs low, reinvest returns, increase contributions and avoid emotional interruption. For borrowers, the lesson is to eliminate high-interest debt before it compounds against the future. For families, the lesson is to plan for inflation before rising costs create pressure. For business owners, the lesson is to understand how growth rates affect revenue, costs and value.

The fastest safe path to doubling money is rarely a dramatic shortcut. It is usually a disciplined combination of time, return, contribution and risk control.

The Rule of 72 does not promise wealth. It reveals the engine that builds it. Once you understand that engine, every financial decision becomes clearer: what you save, what you invest, what you borrow, what you spend, what you pay in fees and how long you allow money to work.

Compounding rewards people who respect time. The Rule of 72 helps them see why.