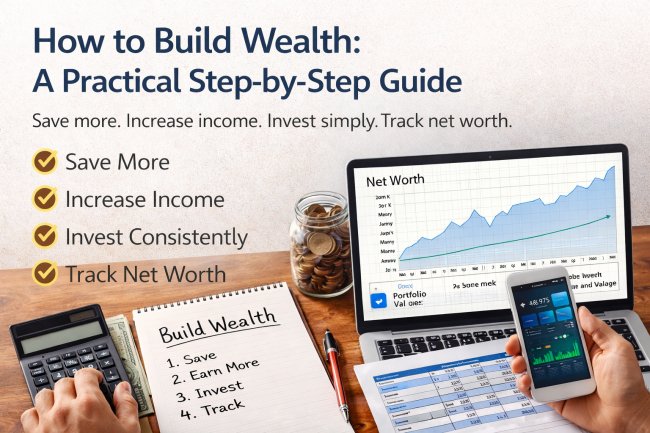

How to Become Rich in Any Year: A Simple Plan That Works

Learn how to become rich with a simple system: earn more, spend with rules, invest steadily, and track net worth. Build real wealth step by step.

How to Become Rich in Any Year: A Simple Plan That Works

Most people want to be rich. Few have a plan.

Money grows when your habits become automatic. Your plan must survive stress.

This guide shows how to become rich using simple steps. You will learn how to earn more, save more, invest better, and track progress.

What “Rich” Really Means

Rich is not a shopping spree. Rich is freedom and options.

A useful definition is net worth. Net worth is assets minus debts.

Use these three levels

- Stable: you can handle surprises without debt.

- Comfortable: you invest every month and still enjoy life.

- Rich: your assets can support your lifestyle choices.

Why net worth matters more than income

Income is what you earn. Net worth is what you keep.

Many high earners stay broke. Many quiet savers get wealthy.

The Rich Formula You Can Actually Control

Wealth looks complex, but it comes from a few levers.

Focus on what you can control every month.

The four levers

- Earn more: raise your income ceiling.

- Keep more: increase your saving rate.

- Invest better: grow money with time.

- Protect progress: avoid big financial mistakes.

Do not chase perfection. Chase consistency.

Step 1: Stabilize Your Money First

Rich people invest. Broke people react to emergencies.

Stability stops panic decisions.

1) Build a starter emergency fund

Start small if needed. Aim for $500 to $1,000 first.

This fund prevents small shocks from becoming debt.

2) Create a simple money system

Complex budgets fail fast. Use a system that runs itself.

- Bills account: fixed costs and minimum debt payments.

- Spending account: food, transport, personal spending.

- Wealth account: savings and investing.

Automate transfers on payday. Automation beats motivation.

3) Track your numbers monthly

Track once per month. Keep it simple.

- cash

- debts

- investments

- net worth

- saving rate

Step 2: Increase Your Saving Rate Without Hating Life

Your saving rate is your wealth engine.

It is the percent of income you keep and invest.

Pick a realistic target

- 5% to 10%: start here if you feel stuck.

- 15% to 20%: solid progress for most people.

- 25%+: faster wealth with tighter choices.

Use the “raise and save” rule

This rule makes wealth feel easier.

- When income rises, save half of the increase.

- Use the other half to improve your life.

- Repeat every time income grows.

Cut costs with a value filter

Do not cut everything. Cut low-value spending first.

- subscriptions you do not use

- fees and penalties

- impulse shopping triggers

- convenience habits that became default

Keep what you love. Remove what you barely notice.

Step 3: Grow Your Income Like a Rich Person

Saving helps, but income growth changes everything.

Rich people increase their earning power.

Choose one income path

- Career growth: promotions and better roles.

- Freelance: skill-based services for clients.

- Business: products, teams, and systems.

Build one high-income skill

High income follows rare and useful skills.

Pick one skill you can improve for 12 months.

- sales and negotiation

- copywriting and marketing

- data and analytics

- software and automation

- design that drives business results

- project management

A simple skill plan that works

- Learn the basics from one reliable source.

- Practice weekly using real projects.

- Get feedback from someone ahead of you.

- Collect proof of results and improvements.

Proof gets you paid. Certificates rarely do.

Use a clear income goal

Pick a number that changes your savings rate.

Example: “Increase income by $300 per month in 90 days.”

Then choose one move that supports that number.

Step 4: Handle Debt the Smart Way

Debt can delay wealth for years.

Paying it off creates breathing room and momentum.

Know the debt types

- High-interest debt: usually credit cards and costly loans.

- Low-interest debt: can be manageable with a plan.

Pick one payoff method

Choose the method you will follow for months.

- Snowball: smallest balance first for quick wins.

- Avalanche: highest interest first for lower cost.

Use a “debt firewall”

Debt often returns after a surprise expense.

Build your emergency fund while paying debt.

This keeps progress from resetting.

Step 5: Invest Simply and Stay Consistent

Investing is how money grows while you sleep.

It rewards patience, not constant action.

Investing order that protects you

- starter emergency fund

- any employer match, if available

- high-interest debt payoff

- long-term investing

- extra investing and business growth

Keep your strategy boring

Boring investing often wins long-term.

- diversified investments

- low costs and fees

- long time horizon

- automatic contributions

How much should you invest?

Start with an amount you can repeat.

Even $25 per week builds the habit.

Increase when income rises. Use the raise and save rule.

What to do during market drops

Market drops are normal. Panic selling is optional.

- keep investing on schedule

- avoid checking prices daily

- do not sell from fear

- remember your long-term plan

Step 6: Build Multiple Income Streams the Right Way

Multiple streams sound great. The order matters.

Do not start five streams with one weak base.

The best order

- stabilize your main income

- add a skill-based side income

- build something scalable

- grow investment income over time

Simple second-stream ideas

- freelance services from your current skills

- tutoring or coaching in one focused topic

- editing, design, writing, or marketing support

- digital products after you have real proof

The one-hour rule

Add one focused hour, four days per week.

That becomes over 200 hours per year.

Used well, that can change your income.

Step 7: Avoid the Mistakes That Keep People Poor

Wealth is not only about doing more.

It is also about avoiding expensive errors.

Common wealth killers

- lifestyle inflation after a raise

- buy-now habits with high interest

- investing money you need soon

- cosigning loans you cannot afford

- mixing business and personal money

- chasing quick wins and hype

A strong rule for big purchases

Wait 72 hours before any big purchase.

Ask if it supports your plan or your ego.

A Simple 12-Month “Become Rich” Plan

This plan builds stability first, then speed.

Use it as a checklist, not a stress test.

Months 1 to 3: Build control

- track net worth once per month

- save $500 to $1,000 for emergencies

- remove one recurring expense

- automate saving on payday

- start a debt payoff method

Months 4 to 6: Build momentum

- increase saving rate by 2% to 5%

- start consistent investing

- build one high-income skill weekly

- create a simple side income offer

- track spending for 10 minutes weekly

Months 7 to 12: Build growth

- raise income using proof and results

- increase investing using the raise and save rule

- build emergency fund toward 3 to 6 months

- reduce high-interest debt as fast as possible

- review goals and adjust once per quarter

Conclusion

Getting rich is not magic. It is math plus behavior.

When your system runs, wealth becomes predictable.

- Define rich as net worth and freedom.

- Stabilize money with a simple system.

- Increase saving rate without misery.

- Grow income with one strong skill.

- Invest steadily and avoid big mistakes.

CTA: Start today. Calculate your net worth and automate one wealth transfer on payday.

What's Your Reaction?