THE SAVINGS CULTURE

Saving is the foundation of financial freedom. This global guide teaches you how to build a savings culture, automate your money, avoid common pitfalls, and transition into smart investments. Packed with strategies, case studies, and a 12-month roadmap, it empowers you to secure your financial future—whether you live in New York, Nairobi, London, or Lagos.

How Ordinary People Become Unbreakable—Then Wealthy

By Wealth Global Insights / Maertin K

Copyright & Disclaimer

© Wealth Global Insights. Educational purposes only. Not financial advice. Always do your own due diligence.

Dedication

To every hustler who chose discipline over drama—this book is your shortcut.

Table of Contents

-

The Big Promise

-

Why Saving Comes Before Investing

-

The 10 Blockers That Keep You Broke

-

Rewiring Your Money Mind

-

The Pay-Me-First System (10–30%)

-

The Savings Ladder (Where Money Lives at Each Stage)

-

Building Structures: Automation, Buckets & Windfalls

-

Africa Playbook: Kenya & Nigeria Examples

-

From Saver to Investor: Upgrading Your Money’s Job

-

Risk, Scams & Reality Checks

-

The 30-Day Sprint & 90-Day Plan

-

Scripts, Checklists & Dashboards

-

Stories from the Field

-

Frequently Asked Questions

-

Your Next 12 Months

1) The Big Promise

This book won’t teach you to “get rich overnight.” It will do something better: make you unbreakable. When emergencies no longer break you, opportunities finally meet you. Saving isn’t punishment—it’s permission. Permission to breathe. To say “yes” to land, a T-Bill, a course, a business—without begging or panicking.

Mantra: If I don’t save, I’m not safe. If I save, I’m unstoppable.

2) Why Saving Comes Before Investing

Saving is setting money aside for a purpose (safety).

Investing = sending money on assignment for a return (growth).

You can’t build a skyscraper on sand. First, stability: a buffer of 6–12 months of living expenses. Then, growth: move the surplus to productive assets (Treasury Bills/Bonds, funds, equities, and carefully vetted projects).

Rule of thumb:

-

Short-term goals (0–2 yrs) → keep safe & liquid.

-

Medium (2–5 yrs) → mix safety with modest growth.

-

Long (5+ yrs) → accept measured risk for better returns.

3) The 10 Blockers That Keep You Broke

-

Ignorance—no one showed you why saving matters.

-

Unwise comfort—you know, but don’t do.

-

No how-to—no system to start.

-

Pressing needs—every fire eats your future.

-

Procrastination—"I'll “start later” (later never comes).

-

Living only for now—no design for tomorrow.

-

Magical thinking—"money “will show up when I need it.”

-

Over-spiritualizing—under-planning the present life.

-

Youthful cover—parents/roommates handle bills.

-

Lack of discipline—feelings run the wallet.

Antidote: awareness → a simple system → automation → accountability.

4) Rewiring Your Money Mind

-

Identity shift: “I am a saver. I pay me first.”

-

Environment: separate bank/app for savings; unfollow spending triggers.

-

Language: replace “I can’t save” with “How can I pay me first?”

-

Tiny wins: start with 10%—raise by 2–5% each quarter.

-

Accountability: a friend, SACCO, or chama that sees your numbers.

5) The Pay-Me-First System (10–30%)

Step 1: Pick your number (start at 10%, target 20–30%+).

Step 2: Automate on payday (standing order/mobile wallet rule).

Step 3: Split into buckets (Emergency / Goals / Investing).

Step 4: Sweep all windfalls (bonuses, gifts, refunds) to savings.

Step 5: Every raise? Increase your saving rate before lifestyle.

Script to your bank/app:

“Move 20% of every inflow on payday to Savings–Emergency. Move 5% to Goals–Land/School. Keep repeating monthly.”

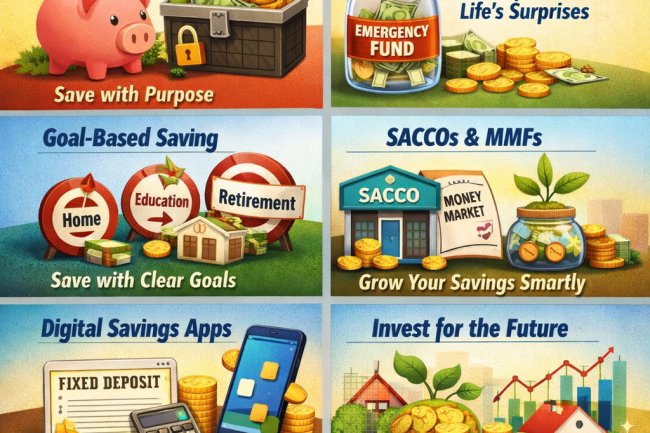

6) The Savings Ladder (Where Money Lives at Each Stage)

Stage A—Parking (Safety First)

-

Savings Account / Mobile Wallet sub-account: easy access while you build the first ₦/Ksh 50k–500k.

-

Money Market Fund (MMF): low risk, daily accrual, quick redemptions—ideal for emergency fund after the first base is set.

Stage B—Planned Safety (Laddering)

-

Treasury Bills (91/182/364-day): government paper; ladder maturities monthly/quarterly for cash flow.

-

Fixed/Term Deposits: when you know the timeframe.

Stage C—Purpose Pools

-

SACCOs / Cooperatives / Chamas: forced monthly saving, cheaper loans; use for big goals (land, school fees).

-

Goal accounts: “Travel,” “School,” “Land deposit.”

Stage D—Hedges & Diversifiers

-

Bonds: medium/long-term stability & income.

-

Gold: a store-of-value hedge (volatile—not your emergency fund).

Graduation: After 6–12 months of expenses are secured, redirect new savings from low-yield parking into productive assets (government paper, funds, equities, and vetted real estate projects).

7) Building Structures: Automation, Buckets & Windfalls

Automation beats willpower. Make your default the right thing.

-

Direct debit/standing order: salary → Emergency/Goals.

-

Rules in wallet apps: every deposit triggers a % sweep.

-

Windfall protocol: 100% of bonuses/gifts/refunds → savings.

-

Separate homes for money: different banks/apps to reduce “peeking.”

-

Ring-fence income streams: e.g., rental income never touches lifestyle; it buys the next asset.

8) Africa Playbook: Kenya & Nigeria Examples

Kenya (Nairobi example)

-

Open a SACCO account (deduct Ksh monthly via payroll).

-

Create MMF (for emergency fund) + T-Bill ladder (91/182/364-day).

-

Use M-Pesa rules/standing orders on payday (20% to savings; 5% to goals).

-

Chama for group land purchase—insist on governance (constitution, elected signatories, audited statements, site visits).

Nigeria (Lagos example)

-

Join a credible Co-op; set up a standing order from your salary.

-

Build an emergency in MMF, then buy DMO T-Bills/Bonds through your broker/bank.

-

Use a target account for school fees/house deposit.

-

For investment clubs, demand audited accounts, legal structure, clear exit terms, and proof of underlying assets.

9) From Saver to Investor: Upgrading Your Money’s Job

-

Stability (6–12 months expenses).

-

Income (T-Bills/Bonds/MMFs; ladder maturities).

-

Growth (broad funds/equities; skill-based businesses).

-

Projects (vetted real estate, private deals—only when you fully understand the engine of returns).

Rule: if you can’t explain how it makes money in one paragraph, don’t fund it.

10) Risk, Scams & Reality Checks

-

“20–30% p.a. guaranteed”? Demand audited statements, licenses, collateral, cash-flow proof, independent references, and an exit plan. Walk away if anything smells vague.

-

Gold is a hedge, not a piggy bank. Expect price swings.

-

Emergency funds must be safe and liquid (MMF, T-bill ladder, savings).

-

Lifestyle creep kills momentum—raise saving rate before raising lifestyle.

-

Documentation: constitutions (for chamas), signatures, board minutes, escrow, custody—treat your money like a business.

11) The 30-Day Sprint & 90-Day Plan

Days 1–3

-

Write your Pay-Me-First % (start at 10–20%).

-

List monthly expenses; set Emergency Target = 6–12× expenses.

-

Open three: Emergency, Goals, and Investing.

Days 4–7

-

Automate transfers on payday.

-

Sweep all windfalls to Emergency.

Week 2

-

Join a SACCO/Co-op or MMF; set a standing order.

-

Start a T-Bill ladder (even small).

Week 3

-

Kill two leaks (subscriptions, impulse eats). Redirect to savings (+2–5%).

Week 4

-

Review: hit 80–100% of targets? Add +2% to Pay-Me-First for next month.

90-Day Outcome

-

2–3 months of expenses saved.

-

Active ladder (T-Bills or MMF).

-

Lifestyle capped; saving rate rising.

12) Scripts, Checklists & Dashboards

Bank Script (email/branch):

“Please set a standing order for 25% of all incoming salary to [Account: Emergency Fund] on payday, and 5% to [Account: Goals–Land]. Continue monthly until revoked.”

Chama/SACCO Checklist

-

✓ Registered entity & constitution

-

✓ Elected signatories & minutes

-

✓ Audited financials (annual)

-

✓ Clear contributions & penalties

-

✓ Investment policy & exit terms

-

✓ Custody/bank mandates

Personal Dashboard (monthly)

-

Saving rate: __%

-

Emergency fund: __ months (goal 6–12)

-

Windfalls captured: __%

-

Leaks eliminated: __

-

Next ladder maturity date: __

13) Stories from the Field

John the Tenant → John the Landlord (Lagos):

He saved 15% for 18 months via co-op. Took a 3x savings low-cost loan, bought a small plot on the outskirts, later flipped at 60% gain. Lesson: discipline + structure beats income level.

Amina the Analyst (Nairobi):

Emergency fund in MMF, then a T-Bill ladder. When her role was downsized, she had 9 months runway—pivoted into data consulting. Lesson: saving is career freedom.

14) Frequently Asked Questions

Q: Save while in debt?

A: Pay minimums, build a mini-buffer (₦/Ksh 50k–100k), then run a debt snowball while still paying yourself 5–10% to protect momentum.

Q: How much is enough emergency?

A: Single income/volatile job: 9–12 months. Dual income/stable: 6 months.

Q: Should I convert all cash to gold?

A: No. Gold is a hedge. Keep emergency safe & liquid; consider gold only as a small diversifier.

Q: What if my income is irregular?

A: Use percent-based rules (e.g., 30% of each payment). Build a bigger buffer (9–12 months).

15) Your Next 12 Months

-

Quarter 1: Build 3 months of expenses; start T-Bill/MMF ladder.

-

Quarter 2: Reach 6 months; raise saving rate by +5%; set two goal accounts.

-

Quarter 3: Maintain 6–9 months; start income assets (bonds/equities/funds).

-

Quarter 4: Review, rebalance, celebrate wins, and set next year’s Pay-Me-First rate.

Final Word:

Saving is not the finish line—it’s the starting engine. When your base is strong, you stop chasing money. Money starts applying to work for you.

Bonus: Visual & Content Pack (for your team)

-

Cover: Pixar-style 4D: three glowing jars—Emergency, Goals, and Investing—over the Nairobi/Lagos skyline.

-

Infographic: “The Savings Ladder” (A→D).

-

Reels/TikTok hooks: “If you don’t save, you’re not safe,” “Pay-Me-First in 20 seconds.”

-

Printable checklist: Bank scripts, SACCO checklist, 30-day sprint calendar.

What's Your Reaction?