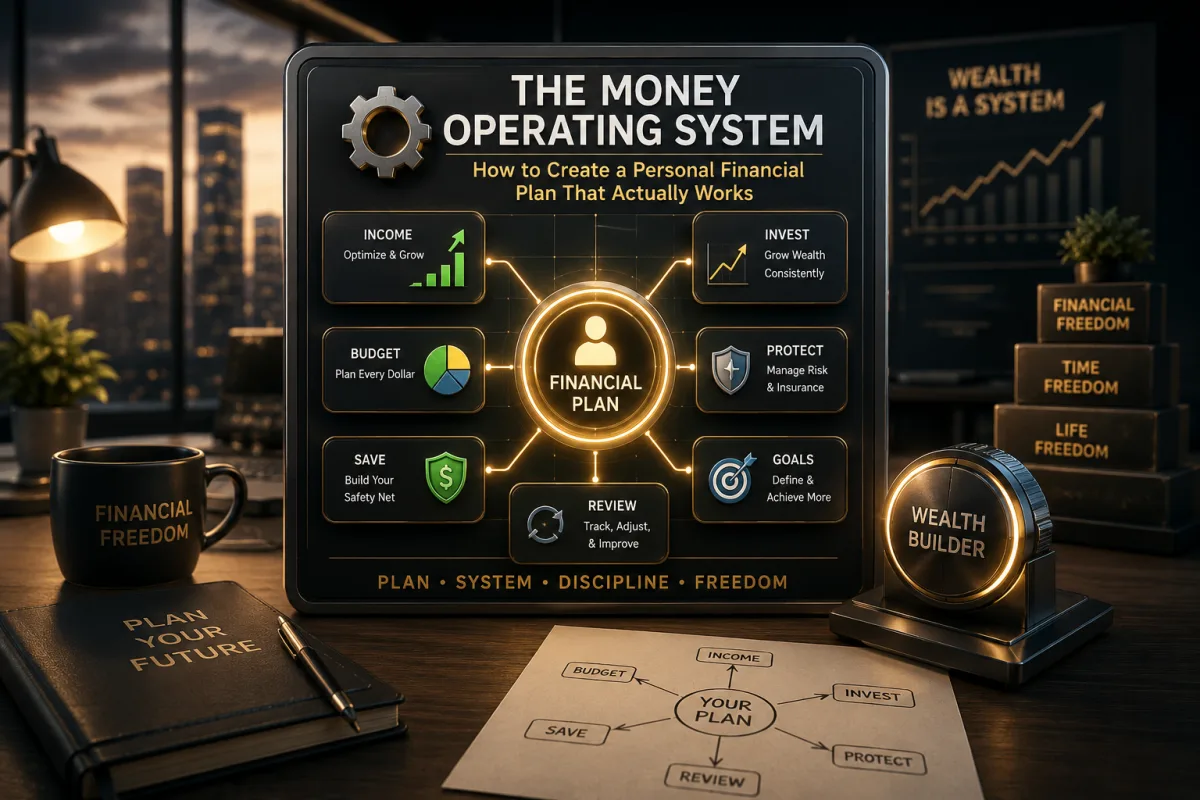

The Money Operating System: How to Create a Personal Financial Plan That Actually Works

A personal financial plan is not a document that sits forgotten in a folder.

It is an operating system for money. It tells income where to go before life absorbs it. It turns vague hopes into measurable goals. It protects against emergencies. It creates a path for debt repayment, saving, investing, insurance, retirement, family obligations and future choices. Most importantly, it connects daily financial behavior to the life a person actually wants to build.

Many people believe they need a financial plan only after they become wealthy. This is backwards. A financial plan is how many people begin becoming wealthy. It is the bridge between working hard and making progress. Without a plan, income can rise and disappear. Debt can grow quietly. Emergencies can reset years of effort. Investments can be delayed. Retirement can remain vague. The household may stay busy, stressed and financially reactive.

A good financial plan does not require perfection. It requires honesty. It begins with the truth about income, expenses, debt, assets and habits. It then creates a system for moving from the current situation toward a stronger one.

The reason many financial plans fail is that they are built like wish lists. They assume perfect discipline, stable income, no emergencies, no emotional spending, no family pressure and no unexpected costs. Real life does not behave that neatly. A plan that actually works must account for irregular expenses, weak months, human behavior, changing priorities and financial surprises.

The best personal financial plan is practical enough to follow and strong enough to grow with you.

Why Most People Do Not Have a Real Financial Plan

Many people have financial intentions, but not financial plans.

They intend to save more. They intend to pay off debt. They intend to start investing. They intend to buy a home, build a business, retire comfortably, support family or create financial freedom. But intention is not a system. Intention depends on memory and motivation. A plan depends on structure.

A real financial plan answers specific questions. How much money comes in? Where does it go? What must be paid first? How much should be saved? Which debts should be attacked? How much emergency cash is enough? What should be invested? What risks need insurance? What goals matter most? How will progress be measured?

Without answers, money is managed by urgency. The loudest bill gets paid. The most emotional purchase wins. The nearest deadline controls the month. The future waits for whatever remains, and often nothing remains.

A financial plan works because it changes the order. Instead of letting money drift, it assigns money deliberately. Instead of reacting to every pressure, it creates priorities. Instead of hoping progress happens, it measures whether progress is happening.

Start With the Financial Truth

The first step in creating a personal financial plan is seeing reality clearly.

This means calculating your current financial position without judgment. Many people avoid this step because it can feel uncomfortable. They may not want to know the total debt. They may not want to see how little is saved. They may not want to admit how much spending goes to convenience, status or impulse purchases. But avoidance is expensive. The numbers are influencing life whether they are reviewed or ignored.

Begin with income. List every source: salary, business income, freelance income, rental income, dividends, interest, commissions, bonuses, family support or irregular payments. For variable income, use a conservative monthly average and also identify the lowest typical month. Planning from the best month creates false confidence.

Then list expenses. Separate fixed expenses from variable expenses. Fixed expenses include rent or mortgage, insurance, loan payments, school fees, subscriptions, utilities, transport commitments and other recurring obligations. Variable expenses include food, dining, fuel, entertainment, clothing, gifts, medical costs, household supplies and personal spending.

Next, list irregular expenses. These are the costs that break many budgets because they do not appear every month: annual insurance, school terms, car repairs, holidays, family events, property maintenance, professional fees, medical checkups, taxes and equipment replacement. They are not surprises if they are predictable.

Then list debts. Include balances, interest rates, minimum payments, due dates and whether the debt is secured or unsecured. Credit card balances, overdrafts, personal loans, mobile loans, car loans, student loans, mortgages, business loans and family loans should all be visible.

Finally, list assets. Include cash, emergency savings, retirement accounts, investment accounts, business value, property equity, land, vehicles, valuable equipment and other assets. Be realistic with valuations.

This gives you the foundation: cash flow, debts, assets and net worth. A financial plan built without these numbers is guessing.

Calculate Net Worth

Net worth is one of the most important personal finance measurements.

It is calculated by subtracting liabilities from assets. If assets are worth $100,000 and debts are $40,000, net worth is $60,000. If assets are worth $20,000 and debts are $35,000, net worth is negative $15,000.

Income shows what flows through your life. Net worth shows what remains.

This distinction matters because income can be misleading. A person may earn a high salary and still have low net worth because spending, debt and lifestyle consume everything. Another person may earn modestly but build a growing net worth through saving, investing and careful debt management.

Track net worth regularly, but not obsessively. Monthly, quarterly or twice-yearly tracking can work depending on your personality. The goal is to see the trend. Are assets rising? Are debts falling? Is your financial position strengthening?

A good financial plan should improve net worth over time. If income is rising but net worth is not, the plan is leaking.

Define What Money Is Supposed to Do

A financial plan needs goals because money without goals gets absorbed by life.

Goals give financial decisions direction. Saving becomes easier when the purpose is clear. Investing becomes more meaningful when tied to retirement, freedom, education, property ownership or business capital. Debt repayment becomes more urgent when it is linked to breathing room and future choices.

Good financial goals are specific. “I want to save more” is vague. “I want to build a three-month emergency fund within 18 months” is clearer. “I want to invest” is vague. “I want to invest 15 percent of income every month for retirement” creates action. “I want to reduce debt” is vague. “I want to eliminate my credit card balance within 12 months” is measurable.

Goals should also be personal. Do not copy someone else’s financial plan blindly. Your goals may include home ownership, debt freedom, business capital, caring for parents, children’s education, early retirement, relocation, travel, medical security or charitable giving. The plan should reflect your life, not social pressure.

Divide goals by time horizon. Short-term goals may be within one year: emergency fund, debt catch-up, insurance premium, school fees or moving costs. Medium-term goals may be one to five years: home deposit, business launch, car replacement, education fund or wedding costs. Long-term goals may include retirement, financial independence, children’s university funding or family wealth.

When goals compete, prioritize. Not everything can be funded equally at once. A strong plan decides what comes first.

Build a Budget That Can Survive Real Life

A budget is not a punishment. It is a decision-making tool.

The purpose of a budget is to assign income before the month begins. It should cover needs, debt payments, savings, investments, future expenses and some personal enjoyment. A budget that removes all enjoyment usually fails. A budget that ignores future goals also fails.

Start with essential expenses. Housing, food, transport, utilities, insurance, minimum debt payments and basic family obligations come first. Then assign money to emergency savings, debt repayment or investments depending on your stage. Then fund sinking funds for irregular expenses. Then define discretionary spending.

Many budgets fail because they are too optimistic. They assume groceries will suddenly cost half as much, transport will never vary, children will need nothing unexpected and social events will disappear. A working budget should be based on evidence from past spending, then improved gradually.

The best budget is the one you can actually follow. Some people prefer detailed categories. Others prefer a simpler structure: essentials, future goals, debt, giving and lifestyle. The method matters less than the outcome: money should be directed before it disappears.

A budget should also include review. At the end of the month, compare planned spending with actual spending. Do not treat differences as failure. Treat them as information. Adjust categories, identify leaks and improve the next month.

Create a Cash-Flow System

A financial plan works better when money is separated by purpose.

One account holding all money can create confusion. A person sees a healthy balance and assumes money is available, forgetting that some of it belongs to rent, school fees, taxes, debt payments or insurance. This leads to accidental overspending.

A cash-flow system prevents this. You might use one account for income, one for bills, one for emergency savings, one for sinking funds, one for daily spending and one for investments. The exact number of accounts depends on your needs, but the principle is separation.

When income arrives, move money according to the plan. Bills are funded. Savings are transferred. Debt payments are scheduled. Investment contributions are made. Lifestyle money remains available for ordinary spending.

This system reduces reliance on willpower. It also makes financial reality easier to see. If the daily spending account is low, you know lifestyle spending must slow down. You are not accidentally spending the emergency fund or future school fees.

Money becomes easier to manage when every major shilling or dollar has a job.

Build an Emergency Fund

An emergency fund is the financial shock absorber.

Without emergency savings, unexpected expenses become debt. A medical bill, car repair, job loss, delayed salary, family emergency or urgent travel can force borrowing. This is how many people lose progress repeatedly.

An emergency fund should be liquid, safe and separate from daily spending. It is not designed for high returns. It is designed for access and stability. Money needed for emergencies should not be invested in volatile assets.

Start with a small starter fund if you have no savings. Even a modest cushion can prevent the next surprise from becoming a loan. Then work toward one month of essential expenses. After that, build toward three to six months, depending on income stability, dependents, health, employment risk and business exposure.

A person with variable income, dependents or one household breadwinner may need a larger emergency fund. A person with stable income, low expenses and strong insurance may need less. The right amount depends on vulnerability.

Emergency savings are not idle money. They protect the entire financial plan.

Use Sinking Funds for Predictable Costs

Not every large expense is an emergency.

Many costs are predictable but irregular. School fees, insurance premiums, car maintenance, holidays, home repairs, annual subscriptions, professional licenses, medical checkups and family events may not occur monthly, but they will occur. When these costs are not planned, they disrupt the budget.

A sinking fund solves this by saving gradually. If annual insurance costs $1,200, save $100 per month. If car maintenance averages $600 per year, save $50 per month. When the expense arrives, the money is already waiting.

Sinking funds make a financial plan realistic. They recognize that life does not operate in equal monthly bills. They also reduce reliance on credit.

A person who uses sinking funds experiences fewer financial surprises because they have converted irregular expenses into monthly responsibilities.

Create a Debt Strategy

Debt must be managed deliberately.

A personal financial plan should separate destructive debt from strategic debt. Destructive debt usually includes high-interest credit cards, payday loans, mobile loans, overdrafts and consumer debt used for lifestyle. Strategic debt may include a reasonable mortgage, education debt with strong earning potential or business debt tied to profitable expansion. Even strategic debt can become dangerous if overused.

List debts by balance, interest rate and minimum payment. Then choose a repayment method. The debt avalanche method pays extra toward the highest-interest debt first while making minimum payments on others. This usually saves the most money. The debt snowball method pays extra toward the smallest balance first, creating quick wins and motivation. Both can work.

The most important rule is to stop adding new destructive debt while repaying old debt. Otherwise, the plan becomes a treadmill.

Debt repayment should be paired with emergency savings. Without even a small cushion, the next surprise may go back onto a credit card or loan. The plan should prevent relapse, not only reduce balances.

Once high-interest debt is gone, redirect the old payment toward savings and investments. This is where debt freedom becomes wealth building.

Decide Your Savings Rate

Your savings rate is the percentage of income directed toward savings, investments and debt reduction.

This number matters because it shows how much of your income is being converted into future strength. A person earning a lot but saving little may remain fragile. A person saving a high percentage of moderate income may build wealth steadily.

There is no universal savings rate that fits everyone. A person escaping debt may focus heavily on repayment first. A young professional may aim to invest a growing percentage of income. A family with high temporary child-related costs may save less for a season but should still maintain the habit. A person pursuing early financial independence may need a much higher savings rate.

The practical goal is to increase the savings rate over time. Start where you are. If you can save 5 percent, begin there. Increase to 10 percent. Then 15 percent or more as income grows and debt falls. Capture raises before lifestyle absorbs them.

A rising savings rate is one of the clearest signs that a financial plan is working.

Build an Investment Plan

Saving protects money. Investing grows money.

A personal financial plan should define when, why and how you will invest. Investing should be tied to goals and time horizons. Money needed within a few months should not be exposed to volatile markets. Money intended for retirement decades away can usually accept more market movement in exchange for growth potential.

An investment plan should answer several questions. What are the goals? What is the time horizon? How much will be invested monthly? Which accounts will be used? What asset allocation makes sense? How much risk can be tolerated? How will the portfolio be reviewed? What fees apply?

For many people, diversified funds are a sensible starting point. Broad funds reduce dependence on one company and simplify investing. Others may include individual shares, bonds, property, retirement plans, business ownership or other assets based on knowledge and risk tolerance.

The danger is investing randomly. Buying because of tips, trends, fear of missing out or social media excitement can damage wealth. A plan should guide decisions before emotions rise.

Investing consistently is often more important than trying to be perfect. Regular contributions, diversification, patience and cost control can build wealth quietly over time.

Match Investments to Time Horizons

Every goal has a time horizon, and the investment should fit that horizon.

Short-term money should be stable. If rent, school fees, tax payments or a home deposit are needed soon, the priority is preservation and liquidity. A sharp market decline at the wrong time could disrupt the goal.

Medium-term money requires balance. Goals three to five years away may need a mix of safety and modest growth depending on risk tolerance.

Long-term money can usually accept more volatility because there is time to recover from market declines. Retirement funds for a young investor, for example, may include more growth assets than money needed next year.

This matching prevents one of the most common mistakes: investing short-term money too aggressively or holding long-term money too conservatively.

A financial plan works when each goal has the right kind of money supporting it.

Protect Your Income

Your ability to earn is one of your greatest financial assets.

If income stops, the entire plan is affected. Bills, savings, investments, debt payments and family support may all depend on continued earning power. This is why a personal financial plan should include income protection.

Protection begins with employability. Skills, professional networks, certifications, reputation and adaptability reduce the risk of long-term unemployment. A person with marketable skills has more options when one job or client ends.

Protection also includes insurance. Disability or income protection insurance may be important if illness or injury would stop earnings. Life insurance may be necessary if dependents rely on your income. Health insurance can prevent medical costs from becoming financial catastrophe.

Business owners need additional protection. They should consider business interruption risk, key-person risk, liability, property damage, unpaid invoices and tax obligations. A business can be profitable and still fragile if risks are ignored.

A plan that focuses only on investing but ignores income risk is incomplete.

Review Insurance Properly

Insurance should solve specific financial problems.

Do not buy insurance simply because someone sells it well. Do not reject insurance simply because premiums feel unpleasant. Review risks honestly. What would happen if you died? What would happen if you could not work? What would happen after a major illness, car accident, house fire, theft, lawsuit or business interruption?

Insurance is most valuable for risks too large to absorb alone. Small risks can often be handled through savings. Catastrophic risks may require transfer to an insurer.

Read policy terms carefully. Understand premiums, exclusions, waiting periods, limits, claim conditions and renewal rules. Cheap insurance that does not pay when needed is not protection. Expensive insurance that covers the wrong risk is also poor planning.

As life changes, insurance should be reviewed. Marriage, children, property ownership, business growth, debt, divorce, retirement and health changes can all alter insurance needs.

Plan for Taxes

Taxes affect real cash flow.

A financial plan that ignores taxes may overstate income and investment returns. Employees may have taxes withheld automatically, but freelancers, landlords, investors and business owners often need to reserve tax money deliberately. Spending gross income as if it were net income creates future stress.

Keep records. Track income, deductible expenses, investment statements, rental documents, business costs, receipts and tax filings. Understand which taxes apply to salary, business profits, rental income, dividends, interest, capital gains and other income streams in your jurisdiction.

Tax planning is not tax evasion. It is arranging finances legally and intelligently. Retirement accounts, business structures, allowable deductions, timing of income and proper documentation can all matter.

As finances become more complex, professional advice becomes more valuable. A strong plan includes compliance and efficiency.

Create a Retirement Strategy

Retirement planning is not only for older people.

It is the process of building assets that can support you when active income decreases or stops. The earlier retirement planning begins, the more time compounding has to work. Delaying does not make the need disappear; it only increases future pressure.

A retirement strategy should estimate future expenses, expected lifestyle, housing situation, healthcare needs, dependents, inflation and desired retirement age. It should also identify income sources: pension, retirement accounts, investment portfolios, rental income, business income, annuities, government benefits or other assets.

Young investors may focus on growth and consistent contributions. Mid-career investors may need to increase contribution rates and diversify. Late-career investors may focus more on income, risk control, debt reduction and withdrawal planning.

Retirement should not depend on hope alone. It should be funded deliberately over time.

Plan for Major Life Goals

A financial plan should include the major events that shape money.

These may include marriage, children, education, home ownership, business launch, relocation, caring for parents, medical procedures, career change, sabbatical, divorce, inheritance, immigration, retirement or estate transfer. These events affect cash flow, risk, taxes and priorities.

Planning does not mean predicting everything perfectly. It means preparing for likely and meaningful costs before they arrive. A couple planning for children should think about medical costs, childcare, insurance, housing, education and reduced income possibilities. A person planning to buy property should think about deposit, taxes, legal fees, maintenance, furnishing, insurance and emergency reserves after purchase.

Major goals should be funded separately where possible. Mixing all goals into one account creates confusion and accidental spending.

Build Multiple Income Streams Carefully

A strong financial plan should eventually reduce dependence on one income source.

This does not mean starting five side hustles immediately. It means building income diversification carefully. First, stabilize primary income. Then create surplus. Then add one income stream that fits your skills, time and capital.

Additional income may come from freelancing, consulting, tutoring, rental property, dividends, interest, digital products, business ownership, royalties, affiliate income or part-time work. Some streams are active. Some are semi-passive. Some require capital. Some require skill.

The key is to use extra income strategically. If every new income stream becomes new spending, wealth does not grow. Extra income should reduce debt, build reserves, fund investments or acquire assets.

Multiple income streams are most powerful when they reinforce the plan instead of distracting from it.

Create Rules for Spending Decisions

Personal finance becomes easier when important decisions are guided by rules.

Rules reduce emotional spending. They prevent every purchase from becoming a negotiation. For example, you might decide that any purchase above a certain amount requires a 48-hour pause. You might require that bonuses be divided between investing, debt repayment, giving and enjoyment. You might decide never to carry credit card balances. You might set a housing cost limit as a percentage of income.

Rules are personal. They should address your weaknesses. If impulse buying is a problem, create delay rules. If lifestyle inflation is a problem, create raise allocation rules. If debt is a problem, create borrowing rules. If family requests destabilize your finances, create a giving budget.

A good financial plan protects you from predictable versions of yourself.

Prepare for Family and Social Pressure

Money decisions are rarely made in isolation.

Family, friends, culture, community, partners and social media can all influence spending. People may feel pressure to support relatives, attend events, lend money, upgrade lifestyle, host generously, pay for celebrations or appear successful. Some obligations are meaningful. Others can damage financial progress if unmanaged.

A working plan includes boundaries. Decide how much you can give or lend without harming essentials. Create a monthly family support or giving category if needed. Communicate honestly when you cannot fund something. Avoid using debt to maintain appearances.

Generosity is strongest when it is sustainable. A person who destroys their own foundation may eventually be unable to help anyone.

Build Estate and Legacy Planning Into the System

Estate planning is not only for the wealthy.

If you have dependents, property, savings, investments, insurance, business interests or debts, you need a plan for what happens if you die or become incapacitated. Without documents and clear records, families may face legal delays, conflict and financial confusion.

At minimum, consider a will, beneficiary updates, emergency contacts, account records, insurance details, property documents and instructions for key responsibilities. Business owners may need succession plans and agreements. Parents may need guardianship considerations.

Estate planning protects the people who depend on you. It also protects the wealth you are building.

Automate What Matters

Automation makes a financial plan more reliable.

When savings, investments, debt payments and bills happen automatically, progress does not depend entirely on memory or mood. Automation reduces missed payments, late fees and inconsistent saving. It also helps pay yourself first.

Automate emergency savings. Automate retirement contributions. Automate investment deposits. Automate debt payments. Automate transfers to sinking funds. Then review regularly to ensure the amounts still make sense.

Automation should not replace awareness. It should support discipline. A person should still review statements, track progress and adjust the plan as life changes.

The best financial system makes the right behavior easier than the wrong behavior.

Review the Plan Regularly

A financial plan is not finished once written.

Life changes. Income changes. Expenses change. Children are born. Jobs end. Businesses grow. Markets move. Health changes. Parents age. Goals shift. A plan that is never reviewed becomes outdated.

Review cash flow monthly. Review net worth quarterly or twice yearly. Review insurance annually. Review investments at least annually. Review goals whenever major life changes occur. Review estate documents after marriage, divorce, birth, death, property purchase or business changes.

The review should ask practical questions. Did net worth improve? Did debt fall? Did savings rise? Are investments on track? Are expenses growing too fast? Is insurance still appropriate? Are goals still accurate? Is the emergency fund sufficient?

Regular review keeps the plan alive.

What a Simple Personal Financial Plan Looks Like

A personal financial plan does not need to be hundreds of pages.

A simple plan can include one page for current financial position, one page for goals, one page for monthly cash flow, one page for debt strategy, one page for savings and emergency funds, one page for investments, one page for insurance, one page for taxes and one page for review dates.

The plan should be clear enough that you can act on it. If it is too complicated to use, it will be ignored.

For example, a working plan may say: build a starter emergency fund in three months, pay off the highest-interest debt within 12 months, save monthly for annual insurance, invest 10 percent of income into a diversified retirement portfolio, review spending every month, review net worth every quarter and increase investment contributions with every raise.

That is more powerful than a beautiful plan with no behavior attached.

Common Mistakes That Make Financial Plans Fail

The first mistake is building a plan without real numbers. A plan based on guesses will fail when reality arrives.

The second mistake is being too strict. A plan with no room for irregular expenses or personal enjoyment usually collapses.

The third mistake is ignoring debt. Investing while high-interest debt grows can weaken progress.

The fourth mistake is having no emergency fund. One surprise can undo the plan.

The fifth mistake is failing to automate. Manual systems depend too much on motivation.

The sixth mistake is copying someone else’s goals. A plan must fit your life.

The seventh mistake is ignoring insurance and taxes. These can quietly destroy progress.

The eighth mistake is never reviewing. A plan must adapt.

The ninth mistake is trying to do everything at once. Financial progress is built in stages.

The tenth mistake is confusing planning with action. The plan matters only when it changes behavior.

The Order of Priorities

While every situation is different, many people benefit from a clear order.

First, create visibility. Know income, expenses, debts and assets. Second, create a small emergency fund. Third, stop adding destructive debt. Fourth, pay off high-interest debt aggressively. Fifth, build a fuller emergency fund. Sixth, begin or increase investing for long-term goals. Seventh, protect income and family through insurance. Eighth, plan for taxes and major life goals. Ninth, build additional income streams. Tenth, review and adjust.

This order can overlap. For example, someone may contribute enough to capture an employer retirement match while paying debt. A business owner may need tax reserves immediately. A parent may need insurance before investing heavily. The sequence should be adapted, but the foundation should not be ignored.

A plan works best when it builds stability before complexity.

Final Thoughts

A personal financial plan that actually works is not built on motivation alone.

It is built on truth, structure and repetition. It begins with knowing where money goes, what is owed, what is owned and what matters most. It creates a budget that reflects real life. It builds emergency savings. It uses sinking funds for predictable expenses. It attacks destructive debt. It invests for long-term growth. It protects income through insurance. It plans for taxes, retirement, family responsibilities and major goals. It is reviewed often enough to remain useful.

The purpose of a financial plan is not to make life feel restricted. It is to make money serve life more intelligently. A good plan reduces anxiety because decisions are clearer. It reduces waste because money has direction. It reduces vulnerability because emergencies are expected. It increases wealth because surplus is converted into assets.

Financial planning does not require being rich first. It requires deciding that every dollar or shilling should have a purpose before someone else gives it one.

The plan will not be perfect. No plan survives life unchanged. But a flexible plan is better than drifting. A simple plan followed consistently is better than an impressive plan ignored completely.

Money becomes powerful when it is directed. A personal financial plan is the system that provides that direction.