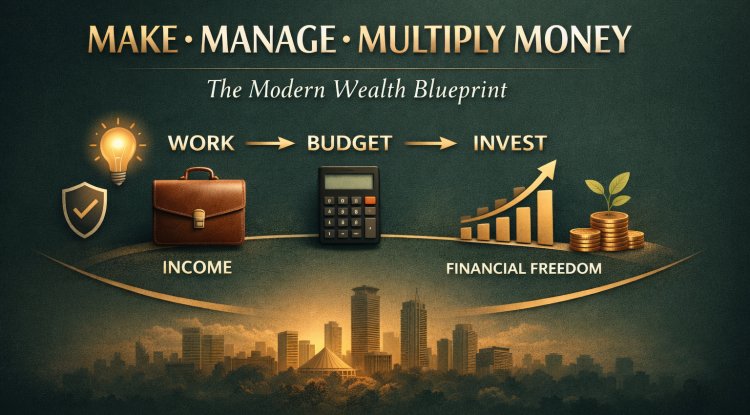

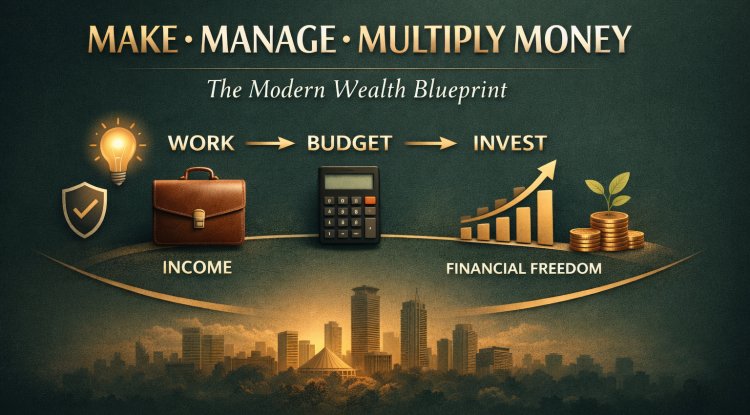

How to Make, Manage, and Multiply Money: The Complete Modern Wealth Blueprint

Learn the practical system to make money ethically, manage it with budgeting, and multiply it through investing—plus the new rules of money that create modern wealth.

How to Make, Manage, and Multiply Money: The Complete Modern Wealth Blueprint

Most people don’t struggle with money because they lack hustle. They struggle because they lack a system.

You can be hardworking, disciplined, and ambitious—yet still remain financially stuck if you don’t understand the correct sequence of wealth creation:

-

Make money (income creation)

-

Manage money (financial control)

-

Multiply money (wealth growth)

Ignore any stage and the whole structure collapses. Make money without management, and your income disappears. Manage money without multiplication, and you stay stable but never grow. Try to multiply money without a solid income foundation, and you end up chasing risky shortcuts.

This blog is a practical, modern blueprint that shows you how money actually works in real life—especially if you want financial freedom in Africa’s fast-changing economy.

By the end, you’ll know:

-

The ethical and reliable way to make money

-

The budgeting discipline that keeps money from leaking

-

The investment mindset that turns income into wealth

-

The new rules of money that matter in today’s world

-

The exact action steps to start implementing immediately

Part 1: How to Make Money (The Only Reliable Method)

Money is not created by luck. It is created by value.

The most dependable wealth principle is simple:

Money is a reward for solving problems, meeting needs, and delivering value.

People pay for results. They pay for convenience. They pay for access. They pay for skill. They pay for speed and clarity. They pay for what saves them time, reduces their stress, or improves their outcomes.

That’s why two people can be in the same city, with the same economy, yet one earns far more than the other. The difference is rarely “hard work.” The difference is value creation and value capture.

The Two Ways People Make Money

Every income path is essentially one of these two:

-

Working for others

-

Employment

-

Contract jobs

-

Freelance projects

-

Commission-based roles

-

Consulting retainers

-

-

Working for yourself

-

Business ownership

-

Trading

-

Content monetization

-

Products and services

-

Online business models

-

Both lanes can build wealth. The problem is not the lane. The problem is staying stuck in one lane without increasing your value, skills, and income strategy.

Part 2: How NOT to Make Money (The Traps That Keep People Poor)

Before we discuss building wealth, we need to eliminate the fake methods that destroy people’s finances. In every society, there are shortcuts that appear profitable at first—until you look at the long-term outcome.

1) Stealing, Cheating, and Fraud

This is not only about crime. It includes:

-

misleading customers

-

selling what you cannot deliver

-

manipulating people

-

hiding important details

-

building a “hustle” that harms others

Even when it brings quick money, it comes at a hidden cost:

-

loss of reputation

-

constant fear and anxiety

-

unstable income

-

damaged relationships

-

legal consequences

-

spiritual and moral decline

Wealth built without integrity does not last.

2) Borrowing and Begging as a Lifestyle

Borrowing is not always bad. But borrowing as a default mindset is a serious warning sign.

If every time you have a financial need, your first instinct is:

-

“Who can I borrow from?”

-

“Who can send me something?”

-

“Who can rescue me?”

Then your problem is not just money. Your problem is that you don’t have a value creation system.

There is a better mindset:

-

“How do I increase my income?”

-

“What skill can I monetize?”

-

“What problem can I solve?”

-

“What service can I offer this week?”

-

“What unnecessary expense can I remove?”

3) Gambling, Betting, and Lottery

Betting thrives on desperation. It sells hope, not outcomes.

If gambling was a reliable wealth system, we would see:

-

stable gambling millionaires

-

generational gambling families

-

gambling as a respected wealth strategy

Instead we mostly see:

-

addiction

-

financial instability

-

broken families

-

debt cycles

The owners build wealth. The participants stay trapped.

4) Marriage as a Money Strategy

Marriage is a partnership—not an escape route from poverty.

Many people make the mistake of thinking:

-

“If I marry rich, I become rich.”

But wealth is not transferred through romance. If you don’t build your own financial system, you will still struggle—even inside a wealthy household.

A healthy marriage can accelerate financial growth through unity, shared goals, and structure. But marriage cannot replace personal responsibility.

5) Inheritance as Your Plan

Waiting for someone else to die so you can become financially comfortable is not a wealth plan.

Even when inheritance arrives, many people lose it because:

-

they never developed money discipline

-

they never built income skills

-

they never learned how wealth is managed and multiplied

The wealth you did not build is often the wealth you cannot sustain.

Part 3: The Real Starting Point — Your Income Audit

To move from financial confusion to financial control, you need awareness. And awareness begins with a simple audit.

Step 1: List 10 Ways You’ve Made Money in the Last 5 Years

This includes everything:

-

salary

-

commissions

-

side hustle earnings

-

one-time gigs

-

selling items

-

online work

-

consulting

-

services for friends or clients

-

any cash inflow

Why this matters:

-

it reveals what already works

-

it shows patterns and strengths

-

it helps you identify income you can expand

Step 2: List 30–50 Possible Ways You Could Make Money

Don’t judge the ideas. Just list them.

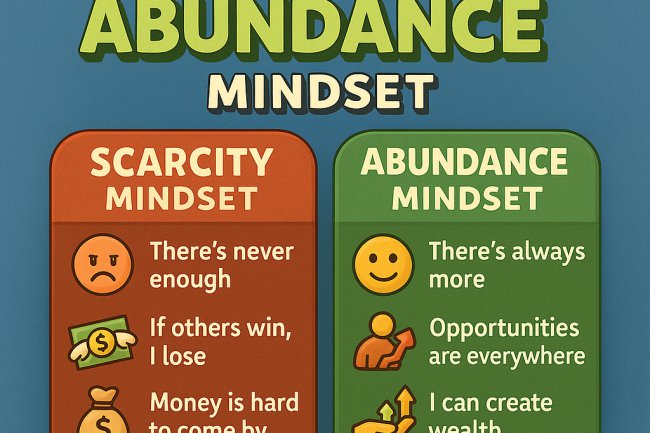

The goal is to break scarcity thinking. Scarcity is not only lack of money—it’s lack of options.

When your mind sees options, it stops behaving like a victim and starts behaving like a builder.

Part 4: How to Manage Money (Budgeting Is Financial Control)

You make money by working.

You manage money by budgeting.

Budgeting is the difference between:

-

earning money and staying broke

-

and earning money and building wealth

A budget is simply a plan that tells your money where to go.

Without a budget, money follows emotions, pressure, and lifestyle. With a budget, money follows your goals.

What Budgeting Really Does

A budget helps you:

-

estimate income and expenses

-

allocate money intentionally

-

control spending instead of being controlled by spending

-

stay within your means

-

track whether you’re moving toward financial goals

-

prepare for emergencies

-

reduce debt and avoid new debt

-

identify areas where you overspend

A key truth:

It’s not how much you make that matters most. It’s what you do with what you make.

Part 5: The Two Levers That Create More Financial Room

There are only two ways to increase the money available to you:

-

Increase your income

-

Reduce your expenditure

That’s it.

If you want a bigger financial life, these two levers must be adjusted.

Lever 1: Increase Your Income

Income increases when you increase:

-

your skills

-

your value

-

your results

-

your reach

-

your ability to solve problems

-

your ability to sell and negotiate

Practical ways to increase income:

-

learn a high-income skill (sales, copywriting, design, video editing, ads, coding, bookkeeping)

-

add a premium offer to your business

-

improve your marketing and distribution

-

build referral and repeat-customer systems

-

create digital products (templates, guides, courses)

-

position your expertise as content (Facebook, blog, YouTube)

Lever 2: Reduce Your Expenditure

Reducing spending is not suffering. It’s optimization.

Ask yourself:

-

What subscriptions am I paying for but not using?

-

What expenses are repeating without clear value?

-

What purchases are emotional rather than strategic?

-

What can I downgrade temporarily to free money for investing?

You don’t cut spending forever. You cut spending until your income and investments grow.

Part 6: How to Multiply Money (Wealth Is Built Here)

You multiply money by investing.

Savings is important, but savings alone does not build wealth.

Savings vs Investment

-

Saving is setting money aside for a purpose.

-

Investing is sending money on assignment for a return.

Saving keeps you stable. Investing makes you grow.

A wise foundation:

-

Build an emergency fund (often 6–8 months of living expenses)

-

Then invest consistently

Part 7: Key Investment Areas to Know

1) Stocks and Shares

Buying shares means you own a portion of a company.

Possible returns include:

-

capital appreciation (price increases)

-

dividends (profit sharing)

-

bonus issues (additional shares, depending on company policy)

Important:

-

Decide whether you are a long-term investor or short-term trader

-

Understand risk

-

Diversify

-

Avoid investing emotionally

2) Real Estate

Real estate is powerful because it can:

-

appreciate over time

-

generate rental income

-

store value

Strategies include:

-

land banking

-

rental housing

-

commercial rentals

-

partnerships and fractional ownership

A simple principle:

Buy land and wait. Don’t wait to buy land.

3) Business Investment

You can invest by:

-

starting your own business

-

investing into someone else’s business

-

buying equity in a growing venture

The goal is to build systems that produce profit—not just a job you own.

4) Intellectual Property

Examples:

-

books

-

courses

-

templates

-

media

-

training programs

-

software

Intellectual property is leverage: build once, sell many times—especially when you have distribution.

5) Online Business

Legitimate online wealth is built through:

-

service delivery

-

content + monetization

-

ecommerce

-

digital products

-

affiliate marketing (ethical and transparent)

-

consulting and coaching (with real value)

Online is not magic. Online is leverage.

Part 8: The New Rules of Money (Modern Wealth Thinking)

The world is changing fast. The same hustle approach that worked years ago is not enough today.

Rule 1: Knowledge Is the New Money

In the modern economy, people pay for:

-

skill

-

insight

-

speed

-

clarity

-

strategy

-

problem-solving

That’s why the most powerful investment is:

investing in yourself.

When you grow your knowledge:

-

your value rises

-

your confidence improves

-

your opportunities expand

-

your income potential increases

Make personal development a lifelong project:

-

be deliberate

-

be intentional

-

be consistent

-

be strategic

Rule 2: Learn How to Use Debt (Wisely)

Debt is not always evil. There is a difference between:

-

bad debt (bondage)

-

good debt (leverage)

Bad debt:

-

borrowing for lifestyle

-

borrowing for consumption

-

borrowing with no repayment plan

-

borrowing for things that don’t produce returns

Good debt:

-

borrowing for investment

-

borrowing for assets or projects that produce cash flow

-

borrowing when returns exceed borrowing costs

-

borrowing with clear structure and discipline

Debt should be used like a tool, not like a lifestyle.

The Wealth Blueprint Summary (Your Action Plan)

If you want a simple roadmap, use this:

-

Stabilize income

-

Budget every month

-

Cut financial leakage

-

Build emergency savings

-

Start investing consistently

-

Increase income streams over time

-

Upgrade your knowledge and strategy

-

Use leverage wisely, avoid traps

Final Words

Wealth is not built by motivation. It’s built by systems.

If you follow the blueprint:

-

you stop chasing money blindly,

-

you gain control over spending,

-

and you start building assets that grow over time.

Start where you are. Use what you have. Apply structure.

And let your financial life become predictable.

What's Your Reaction?