The School of Money: Why Money Is Not What You Think (And How Wealth Is Really Created)

Most people think money is cash or bank balances. In reality, money is value exchange. Learn the real definition of money, the evolution of wealth, and how people actually become rich.

Many people spend their entire lives chasing money, yet very few truly understand what money is. Most people believe money is the paper currency in their pockets or the numbers in their bank accounts. They work hard, earn salaries, and hope that one day they will have enough money to live comfortably.

However, the reality is far deeper.

Money is not paper.

Money is not coins.

Money is not the numbers on your bank app.

Money is something much more fundamental.

Understanding this truth changes the way you think about wealth, work, business, and opportunity. Once you grasp the real nature of money, you stop chasing it—and instead begin attracting it.

In this article, we explore the real definition of money, the evolution of economic systems, and the principles that determine why some people become wealthy while others struggle financially.

This knowledge can transform how you approach wealth creation.

The Biggest Misconception About Money

The first mistake most people make is confusing money with currency.

Currency is simply a tool used to exchange value. Every country has its own currency:

-

Kenya uses the Kenyan Shilling

-

Nigeria uses the Naira

-

The United States uses the Dollar

-

The United Kingdom uses the Pound

But if you travel to another country, your currency may suddenly lose its usefulness. A Kenyan Shilling may not be accepted in Japan. A Nigerian Naira may not be accepted in Canada.

This reveals an important truth:

Currency is geographical, but money is universal.

Currency is just a system humans created to make trade easier. It is essentially a promise note that represents value.

Historically, currencies were backed by gold. When people deposited gold with banks, they received paper certificates representing that gold. These certificates later became the paper money we use today.

Eventually, many governments removed the gold backing entirely, meaning modern currency is largely based on trust rather than tangible value.

This is why governments can print more money, redesign currencies, or change financial systems.

But the deeper concept of money existed long before paper currency ever appeared.

The Evolution of Money and Wealth Creation

To understand money properly, we must examine how economic systems evolved over time.

Human civilization progressed through several major economic stages.

Each stage changed how wealth was created.

Stage One: The Hunter-Gatherer Economy

In the earliest stage of human civilization, people survived by hunting animals and gathering food.

There were no banks.

There was no currency.

There were no salaries.

People relied on two primary resources:

Energy and skill.

Energy represented the physical effort needed to hunt or gather food. Skill represented the knowledge required to catch animals, fish, or locate edible plants.

Those who had greater hunting skills survived better.

This means that in the earliest economy, the real currency was:

Energy and skill.

Even today, these two elements remain fundamental to wealth creation.

Stage Two: The Agrarian Economy

Eventually humans discovered agriculture. Instead of constantly hunting animals, people began farming crops and domesticating livestock.

This discovery transformed the economic system.

Now the focus shifted from hunting animals to cultivating land.

In the agrarian economy, the most valuable asset became land.

People who owned large amounts of land could grow more crops and produce more food. As a result, land ownership became a major source of wealth.

This period also introduced the concept of trade by barter.

People exchanged goods directly.

For example:

A farmer with tomatoes might exchange them for beans from another farmer.

Trade by barter functioned as an early form of money because it allowed people to exchange value without using currency.

However, this system had many limitations.

Sometimes two people could not agree on the value of their goods. Other times someone might need a product that the other person did not want in exchange.

These limitations eventually led to the development of more sophisticated economic systems.

Stage Three: The Industrial Economy

The industrial revolution marked the next major transformation.

Instead of relying primarily on farming, societies began developing factories and manufacturing industries.

At this stage, wealth was generated by extracting resources from under the ground, such as:

-

coal

-

gold

-

oil

-

minerals

Factories transformed raw materials into finished products.

This era also introduced several important institutions that still shape our world today:

The modern school system

Banking institutions

Salary-based employment

Paper currency

Schools were designed to train workers who could operate machines and manage industrial systems.

Jobs and wages became the dominant method of earning income.

Paper currency replaced barter systems and gold transactions because it made trade easier and more efficient.

However, this system also created a mindset where many people believed that employment was the only path to income.

Stage Four: The Information Economy

Today the world operates primarily in the information age.

In this era, wealth is no longer determined by land ownership or industrial production alone.

Instead, the most valuable asset is knowledge.

The richest individuals today often do not produce physical goods themselves.

They create ideas, systems, or technologies that solve large-scale problems.

For example:

Technology companies create digital platforms used by millions of people.

Software developers create programs that automate tasks.

Entrepreneurs build systems that deliver services efficiently across the world.

In the information economy, the focus has shifted from muscle power to brain power.

Ideas, creativity, and problem-solving ability now generate enormous wealth.

This explains why some of the most valuable companies in the world are technology companies.

They operate primarily with knowledge and intellectual capital rather than physical labor.

The True Definition of Money

Once we understand economic evolution, we can clearly define money.

Money is not currency.

Money is any medium of exchange.

In other words, anything that can be exchanged for value is money.

For example:

Knowledge can be exchanged for income.

Skills can be exchanged for salary.

Services can be exchanged for payment.

Ideas can be exchanged for business profits.

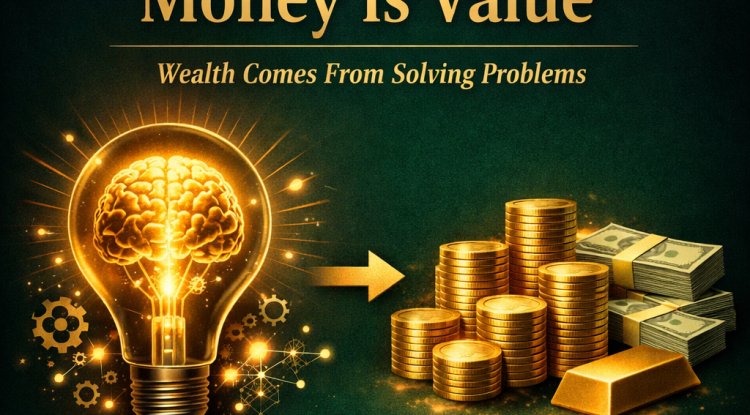

Therefore, money is essentially the result of value exchange.

This leads us to an even more important principle.

Money is a reward for solving problems.

When you solve small problems, you earn small amounts of money.

When you solve larger problems, you earn larger amounts of money.

When you solve problems that affect millions of people, you can generate enormous wealth.

This principle explains why entrepreneurs who solve global problems can become billionaires.

Why Some People Become Wealthy

Wealth is not random.

People who become wealthy usually do one thing exceptionally well.

They solve valuable problems.

Consider the difference between two individuals.

One person may work very hard performing repetitive tasks that create limited value.

Another person may develop a solution that improves efficiency for thousands of businesses.

Even though both individuals work hard, the second person's contribution creates far greater value.

Therefore, they earn significantly more income.

This principle applies across industries.

Doctors earn money because they solve health problems.

Engineers earn money because they solve technical problems.

Entrepreneurs earn money because they solve market problems.

Wealth flows toward those who provide solutions.

The Role of Skills in Wealth Creation

Skills remain one of the most powerful forms of money.

When you develop valuable skills, you increase your ability to exchange value in the marketplace.

Examples of valuable skills include:

Problem-solving

Communication

Leadership

Technical expertise

Digital skills

Strategic thinking

The more valuable your skills become, the more opportunities you create for income generation.

This is why continuous learning is essential in the modern economy.

People who refuse to upgrade their skills often struggle financially because the market evolves rapidly.

Those who continually learn, adapt, and innovate remain competitive.

The Power of Ideas

In today's economy, ideas can generate massive wealth.

An idea that solves a widespread problem can lead to businesses that serve millions of customers.

Many successful companies started as simple ideas designed to improve convenience, efficiency, or accessibility.

When ideas are combined with execution and persistence, they can transform industries.

This is why creativity and innovation are critical assets in the information age.

Why Many People Remain Financially Stuck

Many individuals struggle financially not because they lack potential, but because they misunderstand how money works.

Common mistakes include:

Chasing money instead of solving problems

Relying solely on employment income

Failing to develop new skills

Avoiding entrepreneurship or innovation

Ignoring opportunities to create value

When people focus only on earning wages, they often limit their income potential.

But when individuals shift their focus toward creating value, new opportunities emerge.

The Wealth Mindset

A wealth mindset focuses on value creation.

Instead of asking, "How can I make money?"

Successful individuals ask, "What problem can I solve?"

This shift changes everything.

It encourages innovation, creativity, and entrepreneurship.

The marketplace always rewards those who improve people's lives, save time, increase productivity, or solve meaningful challenges.

Money simply follows value.

Conclusion

Money is often misunderstood.

It is not the paper in your wallet or the balance in your bank account.

Money is value.

Money is exchange.

Money is the reward for solving problems.

Throughout history, economic systems evolved from hunting to farming, from factories to technology-driven economies. Each stage required different skills and different forms of value creation.

Today we live in an era where knowledge, innovation, and problem-solving determine wealth.

Anyone willing to learn, adapt, and develop valuable skills can participate in this system.

Instead of chasing money, focus on creating value.

When you consistently solve problems and contribute meaningful solutions, money will naturally follow.

Understanding this principle may be one of the most important financial lessons you will ever learn.

What's Your Reaction?