Comprehensive Guide to Financial Education: Building Wealth with Confidence

Discover how to manage money, save wisely, invest, and protect wealth. A complete financial education guide for Kenyans seeking financial freedom

Introduction

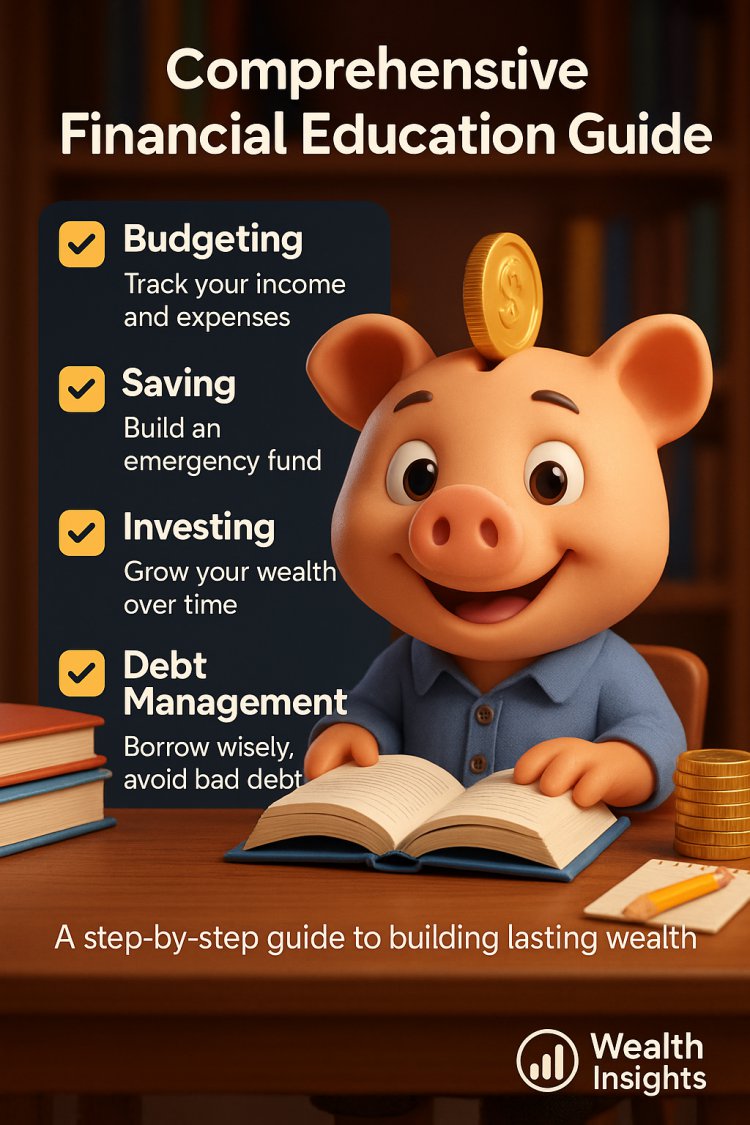

Financial education is the foundation of long-term wealth and financial freedom. Without it, even the highest income can be lost to poor money habits, debt traps, or bad investments. With it, even modest earnings can be transformed into sustainable wealth.

In this guide, we’ll break down the core pillars of financial literacy—budgeting, saving, investing, debt management, and wealth protection—into practical steps that you can apply today.

1. Understanding Money Mindset

Your relationship with money is the starting point.

-

Scarcity vs. Abundance: A scarcity mindset believes money is limited; an abundance mindset sees opportunities to create wealth.

-

Delayed Gratification: Wealth is built by resisting short-term pleasures for long-term gains.

-

Financial Goals: Clarity about what you want (buy a home, retire early, educate your kids) guides your money decisions.

Action Step: Write down your top 3 financial goals for the next 5 years.

2. Budgeting – The Cornerstone of Financial Management

A budget tells your money where to go instead of wondering where it went.

-

The 50/30/20 Rule:

-

50% Needs (rent, food, transport, insurance)

-

30% Wants (entertainment, lifestyle, travel)

-

20% Savings & Investments (retirement, emergency fund, debt repayment)

-

-

Zero-Based Budgeting: Assign every shilling a job before you spend it.

???? Action Step: Create a monthly budget using tools like Excel, Mint, or even a notebook.

3. Saving – Building a Financial Cushion

Savings are your first line of defense against emergencies.

-

Emergency Fund: Save at least 3–6 months of expenses.

-

Short-Term Savings: For upcoming expenses like school fees, vacations, or business capital.

-

High-Interest Accounts: Use savings accounts, SACCOs, or Money Market Funds (MMFs) for better returns.

Kenyan Context: CIC, Sanlam, or NCBA MMFs offer 9–12% annual returns—much higher than ordinary savings accounts.

4. Debt Management – Master Borrowing Wisely

Debt can either be a wealth killer or a growth tool.

-

Good Debt: Student loans, mortgages, or business loans (when used productively).

-

Bad Debt: Credit card balances, payday loans, or digital loan apps that charge high interest.

-

Debt Payoff Strategies:

-

Snowball Method (pay smallest debt first)

-

Avalanche Method (pay highest interest debt first)

-

Action Step: Write down all your debts, interest rates, and payment timelines. Create a payoff plan.

5. Investing—Making Money Work for You

Saving keeps money safe, but investing grows it.

-

Stocks & Bonds: NSE-listed shares, government Treasury Bills (T-Bills), and Treasury Bonds.

-

Mutual Funds & ETFs: Pool your money with others for diversified investing.

-

Real Estate: Land, rentals, and REITs (Real Estate Investment Trusts).

-

Business Investments: Use your skills to start ventures that generate cash flow.

-

Dollar Investments: Apps like Hisa and Chumz let Kenyans invest globally.

Rule of Thumb: Invest consistently, even with small amounts. Time in the market beats timing the market.

6. Protecting Wealth – Insurance and Estate Planning

Wealth is not just about building—it’s about safeguarding.

-

Insurance: Health, life, and property insurance protect you from financial shocks.

-

Succession Planning: Wills and trusts ensure your wealth endures for future generations.

-

Diversification: Don’t put all your money in one asset class. Spread risks.

Action Step: Review your insurance coverage and write a simple will.

7. Financial Education for Families

Teaching money skills early creates generational wealth.

-

Teach Kids Saving & Budgeting: Use allowances to build money discipline.

-

Encourage Investments Early: Open a junior savings account or CDS account.

-

Family Financial Meetings: Discuss goals, savings, and investments openly.

8. Common Money Mistakes to Avoid

-

Living paycheck to paycheck.

-

Ignoring retirement planning until it’s too late.

-

Lifestyle inflation (upgrading lifestyle with every salary raise).

-

Falling for get-rich-quick schemes.

-

Failing to track expenses.

9. Building Multiple Income Streams

One paycheck is risky—develop side hustles and passive income.

Examples:

-

Online business (e-commerce, freelancing, content creation).

-

Rental income (real estate).

-

Dividend-paying stocks.

-

Digital assets (ebooks, courses, affiliate marketing).

10. The Roadmap to Financial Freedom

-

Build an emergency fund.

-

Eliminate high-interest debt.

-

Create multiple income streams.

-

Invest consistently.

-

Protect wealth with insurance.

-

Plan for retirement early.

-

Leave a legacy (succession planning).

Conclusion

Financial education is not just about money—it’s about creating freedom, security, and options for yourself and your family. Start small, be consistent, and watch your financial life transform.

Remember: The goal isn’t just to get rich. The goal is to live a rich life—healthy, free, and fulfilled.

What's Your Reaction?