Financial Guide: Building Wealth in Your 20s, 30s, and 40s in View of Retirement

Your 20s, 30s, and 40s are the most important decades for wealth creation. This financial guide breaks down clear strategies for each stage of life — from learning money basics in your 20s to scaling investments in your 30s and securing assets in your 40s. Discover the habits, systems, and tools you need to retire financially free, regardless of your income level.

Financial freedom doesn’t happen by accident — it’s the result of structured decisions made early and repeated consistently.

Your 20s, 30s, and 40s are the decades where your financial architecture is built, tested, and refined. The key difference between those who retire wealthy and those who retire struggling isn’t income; it’s timing, discipline, and financial literacy.

This guide breaks down what to prioritize in each decade — from foundational habits in your 20s to scaling assets in your 40s.

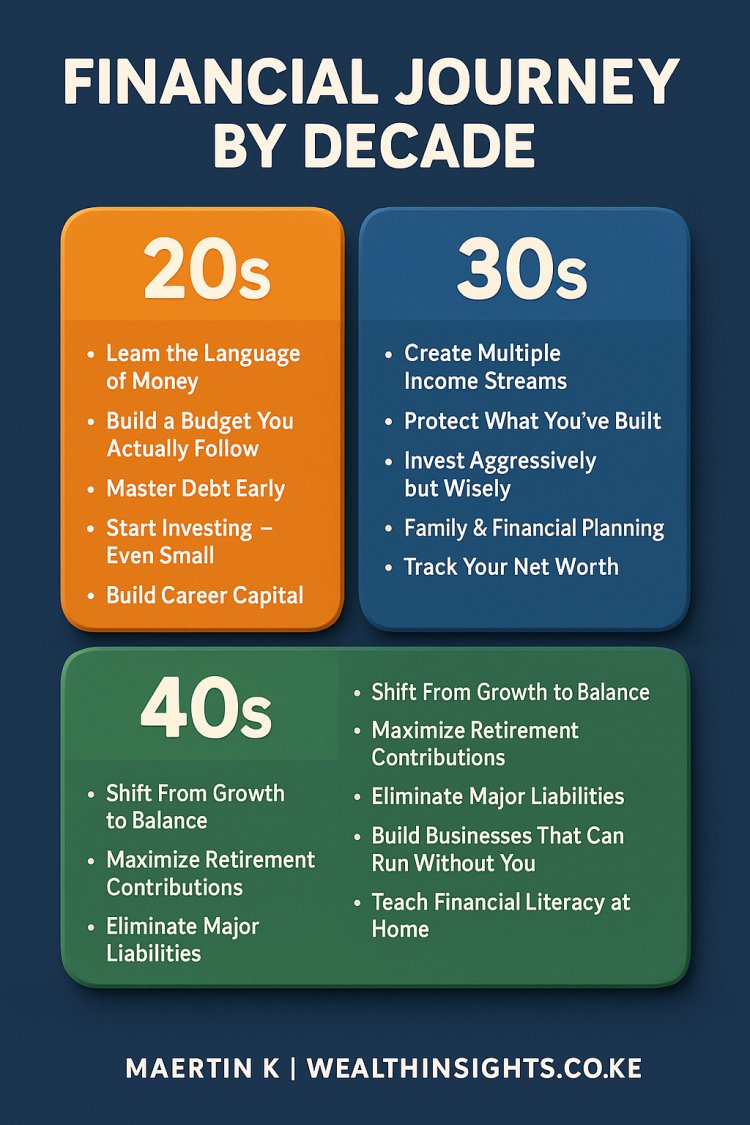

In Your 20s: The Foundation Decade

1. Learn the Language of Money

You don’t need to be rich to start — you need to start to be rich.

Your 20s are about education. Read about compound interest, investing, and risk management. Learn to understand inflation, debt, and asset classes.

Books to begin with: The Psychology of Money, Rich Dad Poor Dad, and The Millionaire Next Door.

2. Build a Budget You Actually Follow

Budgeting is not restriction; it’s direction. Use the 50/30/20 model:

-

50% on needs

-

30% on wants

-

20% on investments and savings

The goal is not perfection, but consistency. Track every shilling using mobile apps like Chumz, M-Pesa, or Absa App to identify leaks.

3. Master Debt Early

Avoid consumer debt. Use credit only if it builds assets or earns returns. Pay off credit cards and high-interest loans before they trap you in compound interest working against you.

4. Start Investing — Even Small

Your biggest asset at this age is time.

Start with SACCOs, money market funds, and low-cost index funds. Even KSh 2,000 a month compounded at 10% over 30 years can grow into millions.

Automation is key — set standing orders so you invest before you spend.

5. Build Career Capital

Your job is your first investment vehicle. Learn transferable skills — sales, digital literacy, communication, data analytics. The more value you offer, the higher your earning potential.

In Your 30s: The Expansion Decade

By now, your income is rising — and so are your responsibilities. The danger here is lifestyle inflation — the temptation to match your earnings with new expenses.

1. Create Multiple Income Streams

Never depend on a single paycheck. Build parallel income sources through:

-

Freelancing or consulting

-

Rental property

-

Dividend-paying stocks

-

Small business or digital products

The goal: turn earned income into invested income.

2. Protect What You’ve Built

Insurance is not a luxury — it’s a defensive asset. Health, life, and income protection ensure that emergencies don’t wipe out years of progress.

3. Invest Aggressively but Wisely

At this age, your risk tolerance is still high. Allocate more to equities, SACCOs, or business ownership. Diversify across industries and geographies — combine local investments (e.g., Safaricom, Equity Bank, KCB) with global ETFs or mutual funds.

4. Family & Financial Planning

If you have dependents, create a financial safety net — an emergency fund covering six months of expenses, plus a will and life cover.

Start planning for your children’s education early using long-term instruments like unit trusts or education policies.

5. Track Your Net Worth

Your wealth is not your salary — it’s what remains after subtracting liabilities from assets.

Review your net worth quarterly. This practice keeps your decisions aligned with long-term goals, not short-term comfort.

In Your 40s: The Acceleration Decade

This is your prime earning window. You’ve learned, built, and invested — now the focus is optimizing and protecting your legacy.

1. Shift From Growth to Balance

Start rebalancing your portfolio to reduce risk. Keep 60–70% in growth assets (stocks, business, real estate) and 30–40% in conservative assets (bonds, money market funds, cash equivalents).

2. Maximize Retirement Contributions

Top up your pension plan or employer retirement scheme. Explore private retirement benefits schemes or offshore diversification for currency protection.

3. Eliminate Major Liabilities

The 40s should be the decade you clear mortgages, car loans, and consumer debts. Entering your 50s debt-free accelerates your ability to reinvest and retire comfortably.

4. Build Businesses That Can Run Without You

Transition from self-employment to systemized entrepreneurship.

Document processes, train managers, and digitize operations — this creates cash flow even when you’re not active daily.

5. Teach Financial Literacy at Home

Generational wealth starts with knowledge transfer. Teach your children about budgeting, investing, and entrepreneurship. Let them see wealth as creation, not consumption.

Universal Financial Principles for All Decades

-

Automate Investing: Your emotions are unreliable; automation ensures consistency.

-

Track Progress: Review your finances monthly. Adjust as life changes.

-

Protect Health: Your body is your first asset; invest in fitness and preventive care.

-

Keep Learning: Markets evolve. Stay informed through finance blogs, podcasts, and books.

-

Network Intentionally: Wealth grows faster in strong ecosystems — connect with financially disciplined peers.

Financial Tools to Use

-

Budgeting: Chumz, Mint, Absa App, Excel

-

Investing: Hisa, Bamboo, Zimele, Cytonn, StashAway

-

Tracking: Google Sheets Net Worth Tracker

-

Education: WealthInsights.co.ke, CFA Kenya, Centonomy

Retirement Readiness Checklist

-

Emergency fund (6 months of expenses)

-

Debt-free or manageable liabilities

-

Pension or investment portfolio consistently funded

-

Multiple income streams

-

Health and life insurance

-

Updated will and estate plan

-

Passive income that can replace at least 60–80% of expenses

Key Insight

The earlier you start, the less you need to invest to retire free. A 25-year-old investing KSh 10,000 monthly for 30 years at 10% annual return will retire with over KSh 20 million. A 40-year-old starting with the same amount will retire with under KSh 5 million.

The difference isn’t income — it’s time and consistency.

Final Thought

Financial success is built on small, disciplined decisions repeated for decades.

Your 20s are for learning.

Your 30s are for scaling.

Your 40s are for securing.

Start where you are, with what you have. Every shilling invested today buys freedom tomorrow.

By Maertin K | WealthInsights.co.ke

Building Africa’s Financially Free Generation

Join the Wealth Insights community to start your financial freedom journey.

What's Your Reaction?