Debt Management Masterclass: How to Regain Control and Rebuild Your Financial Freedom

A complete guide to managing, reducing, and eliminating debt. Learn practical strategies for financial freedom, budgeting, repayment methods, and smart debt management tailored for Kenya, Nigeria, and Africa.

Debt is not the enemy — unmanaged debt is.

Every successful entrepreneur, investor, and household manager has dealt with debt at some point. The difference between those who drown and those who rise is not income — it’s strategy, mindset, and consistency.

This is your practical guide to mastering debt: understanding it, controlling it, and turning it from a trap into a tool.

1. Understanding Debt in the Real World

Debt is simply borrowed money — a financial tool that can either accelerate your goals or chain your progress. Used wisely, it can grow a business, finance education, or purchase productive assets. Used recklessly, it destroys peace of mind and cash flow.

The Two Faces of Debt

-

Good Debt – Debt that creates income or builds value over time.

Examples:-

Business capital that yields profit

-

Education loans that increase earning potential

-

Mortgage for property that appreciates

-

-

Bad Debt – Debt that funds consumption and depreciating items.

Examples:-

Impulse shopping through credit

-

Mobile loans to fill short-term wants

-

Expensive gadgets bought on installments

-

The key rule is simple: If the debt doesn’t pay you back, it’s bad debt.

2. Why Most People Struggle With Debt

Before solving debt, you must understand its root causes. Most people don’t have a debt problem — they have a behavior and awareness problem.

Common Reasons People Fall Into Debt

-

Lack of financial education: Many borrow without understanding interest, repayment schedules, or consequences of default.

-

Impulse spending: The need for instant gratification overrides long-term logic.

-

Low income and high expectations: Social pressure leads people to borrow for image, not growth.

-

Poor budgeting: Without a spending plan, debt becomes a default survival tool.

-

Lifestyle inflation: Each time income rises, expenses rise faster.

Debt begins quietly. It feels manageable until interest compounds and payments outgrow your income. The good news? You can reverse it with a plan.

3. The Debt Audit — Your First Step to Freedom

You can’t manage what you don’t measure. The first and most important step in debt management is a debt audit — writing down exactly what you owe.

Create a Debt List

| Creditor | Amount Owed | Interest Rate | Monthly Payment | Due Date | Notes |

|---|---|---|---|---|---|

| Bank Loan | KES 250,000 | 15% | 10,000 | 5th | Salary loan |

| SACCO | KES 100,000 | 12% | 8,000 | 10th | Business capital |

| Mobile Loan | KES 20,000 | 45% | 5,000 | 20th | Urgent need |

| Credit Card | KES 30,000 | 30% | 3,000 | 25th | Shopping |

Total Owed: KES 400,000

When you see the total in black and white, it becomes real. Most people underestimate their total debt by 30–40%. Awareness is the beginning of control.

4. Build a Personalized Debt-Repayment Strategy

You need a structured, intentional plan to pay off your debt. There are two main methods used by financially smart individuals globally:

A. The Snowball Method – Build Momentum

Focus on paying off the smallest debts first while making minimum payments on the rest.

Each time you clear one, redirect that payment amount to the next debt.

Psychological advantage: you see progress faster, which motivates consistency.

B. The Avalanche Method – Save Interest

Focus on paying off debts with the highest interest rate first, while maintaining minimum payments on the rest.

Financial advantage: you save the most money long term because high-interest debts disappear sooner.

Which is better?

Choose the one that fits your personality. The best plan is the one you stick to.

5. The Budget Reset — Reclaiming Cash Flow

You can’t pay off debt without creating space in your cash flow. Debt management starts with budget redesign.

How to Reset Your Budget

-

Track everything for 30 days.

Use a notebook, Excel sheet, or an app like Chumz or Money Manager. -

Categorize expenses.

Essentials: rent, food, utilities.

Non-essentials: entertainment, subscriptions, impulse buys. -

Cut the excess.

Eliminate or reduce what doesn’t contribute to your goals. -

Reallocate savings.

Every shilling saved goes to debt payoff until you’re clear.

A budget gives direction to your money. Without it, your income becomes noise.

6. The Power of Automation

Debt thrives on inconsistency. The best way to eliminate that is automation.

Set automatic payments from your bank to your lenders or SACCO. When it happens automatically, it removes temptation and excuses.

If your bank doesn’t offer this, set calendar reminders. Consistency kills interest.

Automation is discipline disguised as technology.

7. The Psychological Side of Debt

Debt doesn’t just strain finances — it strains confidence and relationships.

Understanding its psychological impact helps you break free mentally as well as financially.

Mindset Shifts to Adopt

-

Stop shame, start strategy. Debt is common; what matters is progress.

-

Detach emotion from repayment. Treat it as a system, not a punishment.

-

Celebrate small wins. Every cleared loan is a milestone toward freedom.

-

Surround yourself with responsible spenders. Energy influences behavior.

Financial recovery is 80% behavior, 20% knowledge.

8. Smart Tools for Modern Debt Management

In today’s digital world, technology can simplify the process.

Recommended Tools and Apps

-

M-Pesa or Chumz: Track spending and set auto-savings goals.

-

Hisa or Bamboo: Learn to invest once debt is managed.

-

Google Sheets / Notion / Excel: For custom debt tracking templates.

-

Budget Planner by Money Lover: Categorizes expenses and reminds you of due dates.

Leverage tech to stay accountable. Financial freedom is no longer manual—it’s manageable.

9. When to Consider Consolidation

If you’re juggling too many loans with high interest rates, consider debt consolidation.

This means combining multiple debts into one with a lower interest rate or longer term.

Pros

-

Simplifies repayment (one payment per month)

-

Often reduces total interest cost

-

Can improve credit score with consistent payment

Cons

-

Might stretch debt over a longer period

-

May require collateral

-

Risk of relapse if spending habits don’t change

Only consolidate after fixing the root cause — otherwise, it’s like repainting a leaking roof.

10. How to Negotiate With Creditors

Lenders prefer communication over default. If you’re struggling, be proactive.

How to Negotiate Effectively

-

Contact creditors early and explain your situation honestly.

-

Ask for extended repayment terms or reduced interest.

-

Offer to pay something regularly, even if small.

-

Get all new agreements in writing.

A calm, cooperative tone works better than avoidance.

11. Avoiding Future Debt Traps

Eliminating debt is step one; staying debt-free is step two.

Long-Term Discipline Tips

-

Build an emergency fund (3–6 months of expenses).

-

Never borrow for consumption.

-

Compare loan options; always read terms.

-

Pay credit cards in full monthly if used at all.

-

Keep your debt-to-income ratio below 30%.

-

Build side income streams so you don’t rely on loans during crises.

Debt freedom isn’t permanent unless habits change.

12. Debt in the African Context

In Africa, debt often comes from necessity rather than luxury.

Mobile loans, SACCO advances, and informal credit are part of daily life. But these systems also encourage short-term borrowing that traps millions.

The Smart African Approach

-

Use SACCOs for structured, low-interest loans.

-

Avoid instant mobile credit for consumption.

-

Use debt only for productive goals — business, education, or assets.

-

Study your credit score and history; protect your financial reputation.

Debt should build your capacity, not limit your creativity.

13. Transitioning From Debt to Investment

Once your high-interest debts are cleared, redirect those payments into investments.

The same discipline that paid off loans can now fund your growth.

Example Transition Plan

| Month | Action | Purpose |

|---|---|---|

| Month 1–6 | Pay off high-interest mobile loans | Free up cash flow |

| Month 7–12 | Reduce credit card and SACCO debt | Increase savings ratio |

| Month 13+ | Direct previous debt payments to MMF or ETF | Build assets |

You’re already used to sending that money out—now let it start working for you.

14. Practical Case Study

Case: Kevin, Nairobi-based designer, owed KES 420,000 across loans and cards.

Strategy:

-

Created a debt inventory

-

Used the Avalanche method

-

Cut subscriptions and dining out

-

Increased freelance income by 25%

-

Reinvested savings after 10 months

Result: Cleared all high-interest loans within 18 months and invested his freed-up cash in a money market fund.

Real stories like this prove that anyone can recover with discipline and clarity.

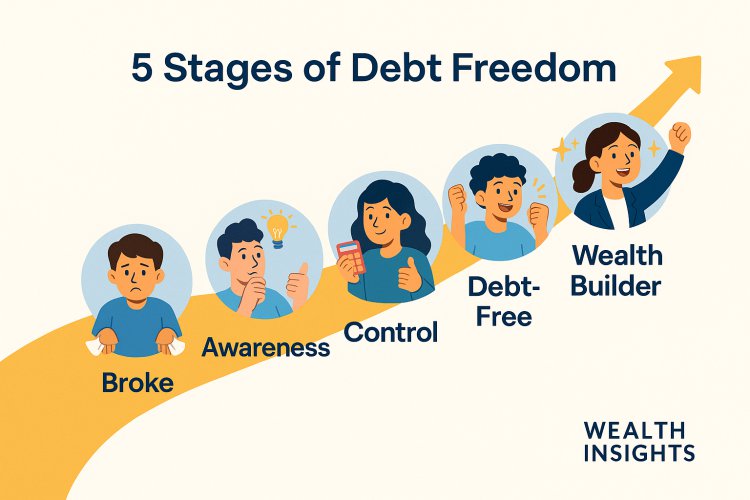

15. The New You — Financially Free and Focused

Debt management is not about deprivation. It’s about direction.

It’s choosing long-term peace over short-term comfort.

When you master debt, you regain control of your time, energy, and potential. You make decisions based on opportunity, not obligation.

Debt freedom doesn’t just change your wallet — it changes your identity.

Conclusion

Debt management is not just financial housekeeping — it’s financial transformation.

It’s the bridge between financial stress and financial stability.

Start with awareness. Build a strategy. Apply discipline.

Every payment you make is a vote for your future freedom.

You don’t have to be perfect — just consistent.

And when you look back a year from now, you’ll see how every small step added up to something life-changing.

— Maertin K | Wealth Insights Kenya

What's Your Reaction?